Pharmaceutical Gelatin Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 1.85 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

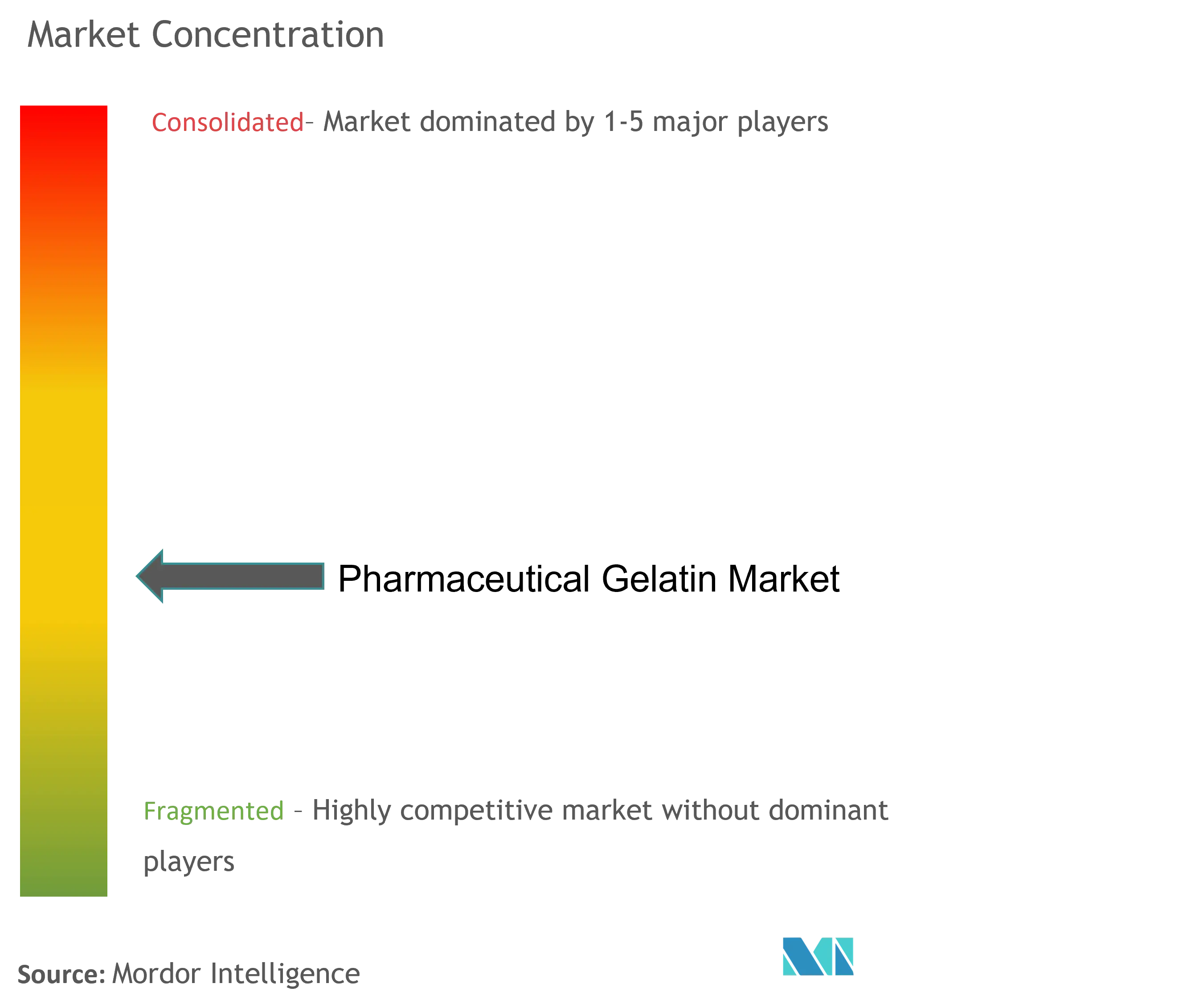

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Gelatin Market Analysis by Mordor Intelligence

The pharmaceutical gelatin market size is expected to grow from USD 1.35 billion in 2025 to USD 1.42 billion in 2026 and is forecast to reach USD 1.85 billion by 2031 at 5.39% CAGR over 2026-2031. Solid growth reflects sustained capsule usage over 70% of global oral solid dosage forms and widening adoption in biologics, vaccines and 3-D printed medicines. Fish-skin grades are expanding fastest because halal certification and non-mammalian sourcing lower regulatory friction, while African swine fever continues to unsettle porcine supply. Soft-gel technology is becoming pivotal for poorly soluble actives, and low-bloom customized grades now support mRNA vaccine stability. Moderate fragmentation persists, yet scale investments by global leaders and brisk CAPEX by Asian capsule OEMs are tightening competitive pressure.

Key Report Takeaways

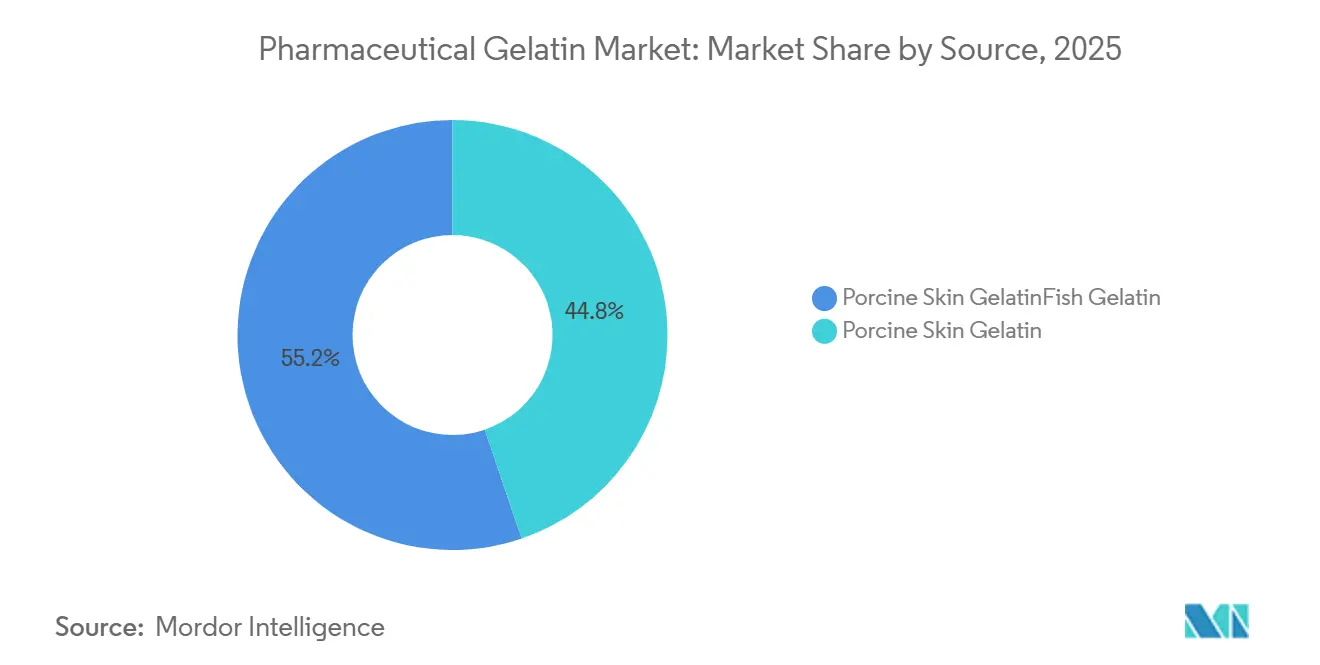

- By source, porcine skin gelatin retained 44.78% pharmaceutical gelatin market share in 2025, whereas fish gelatin is projected to grow at 6.45% CAGR to 2031.

- By application, hard capsules commanded 73.05% share of the pharmaceutical gelatin market size in 2025; soft capsules are on track for a 6.84% CAGR through 2031.

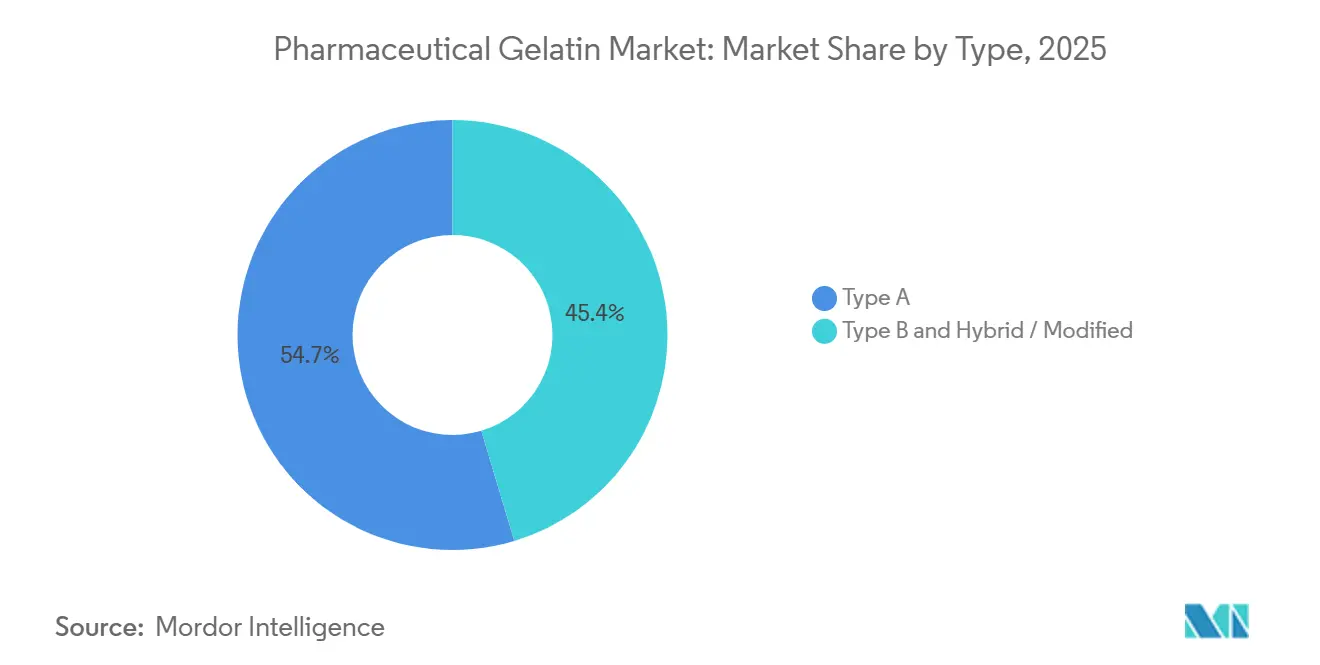

- By type, Type A led with 54.65% share in 2025; Type B is expected to expand the fastest at 7.26% CAGR.

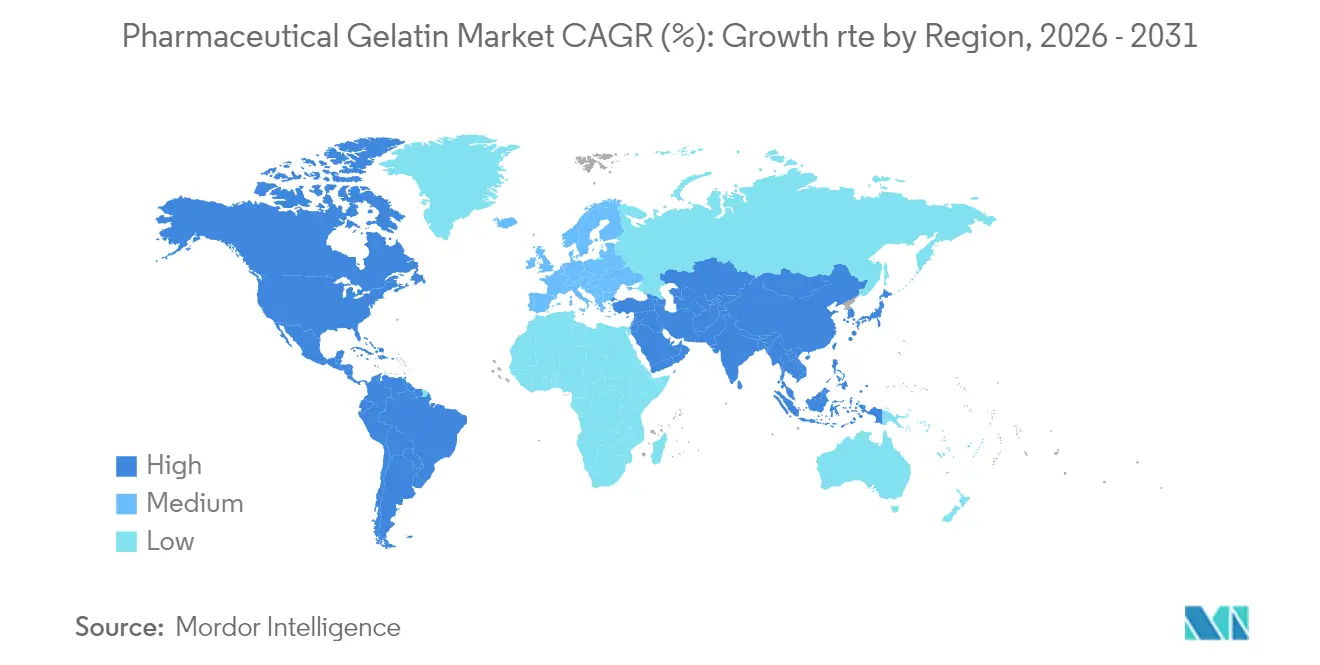

- By geography, Europe held 39.42% revenue in 2025, while Asia-Pacific is poised for the highest 7.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Gelatin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming Nutraceutical Soft-Gel Demand | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growth of Biologics Requiring Gelatin Stabilizers | +0.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| CAPEX Expansion by Capsule OEMs in Asia | +0.9% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Rising Use of Gelatin In 3-D Printed Drug Delivery | +0.4% | North America & EU, pilot programs in APAC | Long term (≥ 4 years) |

| Scale-Up of Fish-Skin Gelatin to Meet Halal Demand | +0.6% | Global, with emphasis on MEA & APAC Muslim markets | Medium term (2-4 years) |

| Low-Bloom Customized Grades for mRNA Vaccines | +0.3% | Global, led by North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Nutraceutical Soft-Gel Demand

Soaring demand for omega-3, vitamin D and other fat-soluble supplements keeps soft-gel consumption rising faster than traditional hard capsules. Soft-gels deliver higher bioavailability and consumer convenience, so supplement brands in the United States and Germany now specify pharmaceutical-grade gelatin with lower residual moisture and tighter metal limits. Suppliers such as GELITA market tailored grades for omega-3 encapsulation, expanding contract volumes with nutraceutical fillers. Regional regulatory familiarity with animal-derived excipients supports continued dominance of gelatin over synthetic film alternatives. Meanwhile, private-label vitamin lines at large retailers rely on legacy soft-gel equipment, locking in gelatin demand for the medium term.

Growth of Biologics Requiring Gelatin Stabilizers

Biologic therapies, including monoclonal antibodies and viral-vector vaccines, need excipients to protect fragile proteins during freezing, lyophilization and transport. Collagen-derived peptides with ultra-low endotoxin profiles safeguard antigen integrity and offer proven compatibility with fill-finish lines. VacciPro, a GELITA collagen peptide, entered multiple pandemic-response vaccine formulations and is now incorporated in next-generation influenza programs. Premium pricing for such grades is widening supplier margins and prompting investment in purification technology. As biologics outpace conventional small molecules, demand for pharmaceutical-grade gelatin stabilizers should remain resilient well beyond 2030.

CAPEX Expansion by Capsule OEMs in Asia

Asian contract manufacturers are enlarging capsule capacity to serve both regional generics and multinational innovators. Lonza’s initiative to add 30 billion extra capsules annually, including major lines in Suzhou and Gujarat, illustrates confidence in long-term outsourcing volumes. Nitta Gelatin’s USD 7.2 million Kerala upgrade prioritizes collagen peptides destined for soft-gels and wound-care dressings. Local incentives, tax holidays, and proximity to bovine and marine raw materials shorten lead times, encouraging global pharma to dual-source Asian capsules even for regulated markets.

Rising Use of Gelatin In 3-D Printed Drug Delivery

Personalized medicine leverages gelatin methacrylate (GelMA) bioinks to print dosage forms with tailored release kinetics and patient-specific geometries. GelMA’s tunable cross-link density and biocompatibility allow tablets that dissolve in layers or orodispersible films for pediatric use. Academic pilot studies have already printed complex polypill structures incorporating poorly soluble APIs and live probiotics. Commercial scale remains modest, but leading gelatin producers are partnering with 3-D printer OEMs to co-develop pharmacopeial-grade GelMA, pre-empting future regulatory submissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Porcine Supply Chain & ASF Outbreaks | -0.7% | Global, with acute impact in APAC & Europe | Short term (≤ 2 years) |

| Regulatory Push Towards Plant-Based Capsules | -0.5% | North America & EU, expanding globally | Medium term (2-4 years) |

| Chronic Shortages of Pharma-Grade Bone Gelatin | -0.3% | Global, with supply concentrated in specific regions | Medium term (2-4 years) |

| High Energy Costs for Collagen Extraction | -0.4% | Europe & North America, moderate impact in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Porcine Supply Chain and ASF Outbreaks

African swine fever periodically removes 10-30% of regional pig herds, triggering sudden rawhide shortages and 20-40% swings in gelatin input costs. European capsule fillers now dual-source fish and bovine hides to hedge against future shocks, while Malaysian investors are commissioning ASEAN’s first JAKIM-certified halal gelatin complex to guarantee Muslim-friendly supply theedgemalaysia.com. Such diversification increases logistics complexity and working-capital needs for pharmaceutical buyers.

Regulatory Push toward Plant-based Capsules

The European Medicines Agency continues to evaluate titanium-dioxide restrictions and carbon-footprint targets, encouraging formulators to shift toward hydroxypropyl-methylcellulose (HPMC) shells. Roquette’s 2025 purchase of IFF Pharma Solutions fast-tracks large-scale vegetarian capsule output for both drugs and supplements pharma.iff.com. Although gelatin remains favored for complex soft-gels, plant-based alternatives could cap long-term demand in fast-mover solid doses, particularly for OTC lines marketed on sustainability claims.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Fish Gelatin Gains Momentum

Porcine skin continued to dominate, holding 44.78% of pharmaceutical gelatin market share in 2025, but fish-derived options are climbing at a 6.45% CAGR owing to halal compliance and supply diversification motives. Researchers have improved marine gel strength 25% using furcellaran blends, removing historical barriers to capsule production. The pharmaceutical gelatin market benefits as coastal processors in Vietnam and Norway secure scale contracts with vaccine and nutraceutical firms. Concurrently, ASEAN governments fund halal-audited extraction lines that shorten approval cycles for Middle-East export dossiers. Bone-derived gelatin still faces BSE-related controls, restricting any sizable rebound.

Rising consumer scrutiny of animal welfare and traceability keeps pressure on supply chains. Producers respond with blockchain lot tracking and dedicated fish gelatin lines to avoid cross-contact. As a result, pharmaceutical buyers gain clearer audit trails, yet carry higher qualification costs. Moving forward, the pharmaceutical gelatin market will see marine collagen extend into chewable gummies, topical films and hemostats, reinforcing multi-source risk mitigation strategies.

By Application: Soft Capsules Drive Innovation

Hard capsules captured 73.05% of pharmaceutical gelatin market size in 2025 as mainstream oral solids retained volume dominance. However, soft-gels are projected to post a 6.84% CAGR, reflecting drug-maker appetite for solubilizing lipid-based APIs and taste-masking pediatric antivirals. Catalent’s German soft-gel revamp underscores how CDMOs re-tool to meet specialty pharma briefs. EASYSEAL film technology, which prevents content leakage, now anchors long-run commercial batches for vitamin K analogs.

Tablet coating and binding retain stable volumes because modified-release generics flourish in Latin America and CEE. Vaccine stabilizers and biotech excipients are the most lucrative niche, commanding 30-40% price premiums over dietary grades. Emerging 3-D printed dosage forms add high-margin micro-volumes today, yet their personalization promise keeps R&D pipelines active. Consequently, the pharmaceutical gelatin market continues allocating capex toward soft-gel film casting, crosslink-resistant grades and bioink intermediates.

By Type: Type B Gelatin Outpaces Traditional Grades

Type A remained the largest, holding 54.65% share in 2025, but Type B is accelerating at 7.26% CAGR on the back of superior alkaline stability and stronger tablet binding. Formulators developing once-weekly hormone therapies report cleaner compression with Type B, especially in high-drug-load matrices. Newly launched low-bloom variants enable safe viscosity ranges for lipid nanoparticle vaccines, aligning with WHO pharmacopeial purity limits. Hybrid grades that graft polyethyleneglycol chains onto Type B promise even finer rheology control.

Demand from high-value biologics spurs suppliers to install additional ion-exchange and ultrafiltration banks, raising capex but unlocking premium price tiers. North American developers of 3-D printed buccal films prefer Type B for its predictable photo-cross-link profile, further lifting volumes. These advances collectively widen the pharmaceutical gelatin market size devoted to modified and bespoke gelatin families.

Geography Analysis

Europe led revenue with 39.42% in 2025 because stringent GMP enforcement and dense CDMO clusters keep regional buyers sourcing locally. Germany and the United Kingdom drive consumption, leveraging advanced biologics pipelines and occupational know-how in collagen extraction. Yet soaring utility prices and impending sustainability mandates raise operating costs, nudging some plants toward solar thermal pre-heaters and biomass boilers to retain margin parity.

Asia-Pacific is the fastest-growing territory, advancing at a 7.72% CAGR. China’s provincial grants let gelatin firms retrofit food-grade lines to pharmaceutical standards within two years. India’s capacity build highlighted by Nitta Gelatin’s USD 24 million multi-phase investment accelerates collagen peptide outputs geared to both domestic ANDA launches, and US-FDA inspected exports. Southeast Asian sites capture halal premiums, making Malaysia a supply nerve center for GCC importers.

North America sustains high per-capita demand on the back of nutraceutical proliferation and sustained biologics R&D. The United States houses several leading soft-gel CMOs, ensuring continuous throughput even as plant-based capsule lobbying intensifies. Canada’s incentive program for biomanufacturing has attracted new collagen hydrolysis pilots, catering to gene-therapy stabilizers. Smaller but expanding markets such as Brazil and Saudi Arabia invest in gelatin-based hemostat lines to localize surgical supply chains, broadening global diversification options within the pharmaceutical gelatin market.

Competitive Landscape

Moderate fragmentation defines competition as the top three suppliers GELITA AG, Rousselot, and PB Leiner. All three run multi-continent facilities, lowering freight risk and smoothing regulatory audits. GELITA posts EUR 839 million annual revenue across 22 plants, embedding vertical integration from raw hide to specialty peptides. Rousselot’s 2024 launch of the Nextida collagen platform broadened its functional-ingredient appeal in pharmaceutical gummies and sachets. PB Leiner focuses on solubilized peptides and has just commissioned a continuous extractor to cut energy per tonne by 15%.

Regional players leverage agility and cost advantages. Nitta Gelatin adds marine collagen capacity in India, positioning to serve Asian halal and kosher markets. Sanichi Technology’s Melaka project targets 12,000 tonnes of halal fish gelatin once fully built, challenging traditional pork-skin dominance. Supply shocks are spurring long-term off-take agreements; European vaccine makers now lock in three-year gelatin contracts to avoid 2020-style shortages. Automation, inline NIR monitoring, and digital batch records are emerging as clear differentiators when tendering to stringent biologics clients.

M&A momentum remains active. Roquette’s 2025 acquisition of IFF Pharma Solutions inverts the gelatin narrative by fusing plant-based capsule technology with conventional excipients, broadening its toolkit amid sustainability debate. Barentz’s June 2025 purchase of China’s Fengli Group strengthens excipient distribution in the region, providing a route-to-market for niche fish gelatin lots.

Pharmaceutical Gelatin Industry Leaders

Gelita AG

Weishardt

Darling Ingredients Inc

Tessenderlo Group (PB Leiner)

NITTA GELATIN, INC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Barentz acquired China’s Fengli Group to boost excipients distribution in APAC.

- May 2025: Roquette completed the acquisition of IFF Pharma Solutions, expanding vegetarian capsule capacity.

- May 2025: Nitta Gelatin launched a ₹60 crore expansion in Kerala focused on collagen peptides.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study at Mordor Intelligence defines the pharmaceutical gelatin market as pharmaceutical-grade collagen derivatives sourced mainly from porcine, bovine, and marine raw material sold to drug makers for hard and soft-gel capsules, tablet binding, absorbable hemostats, and vaccine stabilizers.

We exclude every use of gelatin in food, cosmetics, photography, and industrial adhesives from this valuation.

Segmentation Overview

- By Source

- Porcine Skin Gelatin

- Bovine Gelatin

- Fish Gelatin

- Other Sources

- By Application

- Hard Capsule Manufacturing

- Soft Capsule Manufacturing

- Tablet Binding & Coatings

- Hemostats & Medical Devices

- Vaccines & Biotechnology

- Others

- By Type

- Type A

- Type B

- Hybrid / Modified

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held in-depth conversations with capsule contract manufacturers, hemostat formulators, regulators, and gelatin processors across North America, Europe, and Asia-Pacific. Their insight on average selling prices, halal/kosher premiums, and seasonal raw-hide constraints allowed us to refine desk assumptions and align regional mix splits.

Desk Research

We mapped supply and demand by merging UN Comtrade trade codes, USDA hide output, EMA certificate lists, and capsule production data from the International Pharmaceutical Excipients Council. Analyst access to D&B Hoovers, Dow Jones Factiva, and Questel patents filled revenue, capacity, and innovation gaps, while government tenders, pharmacopeial monographs, and peer-reviewed pharmacokinetic papers grounded technical ratios. These sources illustrate, rather than exhaust, the evidence stack supporting each figure.

Market-Sizing & Forecasting

Our top-down build starts with regional capsule and hemostat unit volumes, applies validated gelatin loading factors, and converts tonnage to value using weighted average prices. Supplier roll-ups plus sampled contract quotes act as bottom-up reasonableness checks. Key drivers, chronic prescription growth, biologics fill-finish capacity, fish-skin adoption rates, livestock inventory cycles, and purity-linked price differentials feed a multivariate regression that projects demand through 2030. When bottom-up gaps appear, regional substitution ratios agreed during interviews plug the holes.

Data Validation & Update Cycle

We run dual analyst reviews; anomalies trigger re-calculation. Models refresh each year, with mid-cycle updates if trade bans, disease outbreaks, or major capacity additions reshape fundamentals. A final pre-publication sweep ensures clients receive the latest view.

Why Our Pharmaceutical Gelatin Baseline Commands Credibility

Published estimates often diverge because some firms mix nutraceutical gummies, lock in outdated base years, or freeze exchange rates.

Through a disciplined scope, yearly refresh, and multi-angle triangulation, we keep Mordor's baseline firmly grounded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.35 B (2025) | Mordor Intelligence | - |

| USD 1.30 B (2024) | Global Consultancy A | excludes hemostats, one global price |

| USD 1.10 B (2022) | Industry Tracker B | older base year, static FX rates |

| USD 1.69 B (2023) | Trade Journal C | combines pharma and nutraceutical gelatin |

When scope, pricing, and refresh cadence are normalized, Mordor Intelligence provides a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is driving the rapid growth of fish gelatin?

Fish gelatin satisfies halal requirements, avoids swine-related disease volatility and aligns with regulators’ push for non-mammalian excipients, enabling a 6.45% CAGR through 2031.

How large is the pharmaceutical gelatin market today?

The market is valued at USD 1.42 billion in 2026 and is projected to hit USD 1.85 billion by 2031, growing at a 5.39% CAGR.

Why are soft-gel capsules gaining traction?

Soft-gels improve bioavailability for lipid-soluble drugs and vitamins, and technology advances such as EASYSEAL reduce leakage, supporting a 6.84% CAGR for this format.

What supply-chain risks threaten gelatin availability?

African swine fever periodically disrupts porcine hide supply, causing price spikes and prompting buyers to diversify into fish and bovine sources.

Are plant-based capsules a major competitive threat?

Regulatory sustainability agendas in Europe and North America encourage hydroxypropyl-methylcellulose shells, but gelatin retains technical advantages for soft-gels and biologic stabilizers, limiting near-term displacement.

Page last updated on: