Bone Wax Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

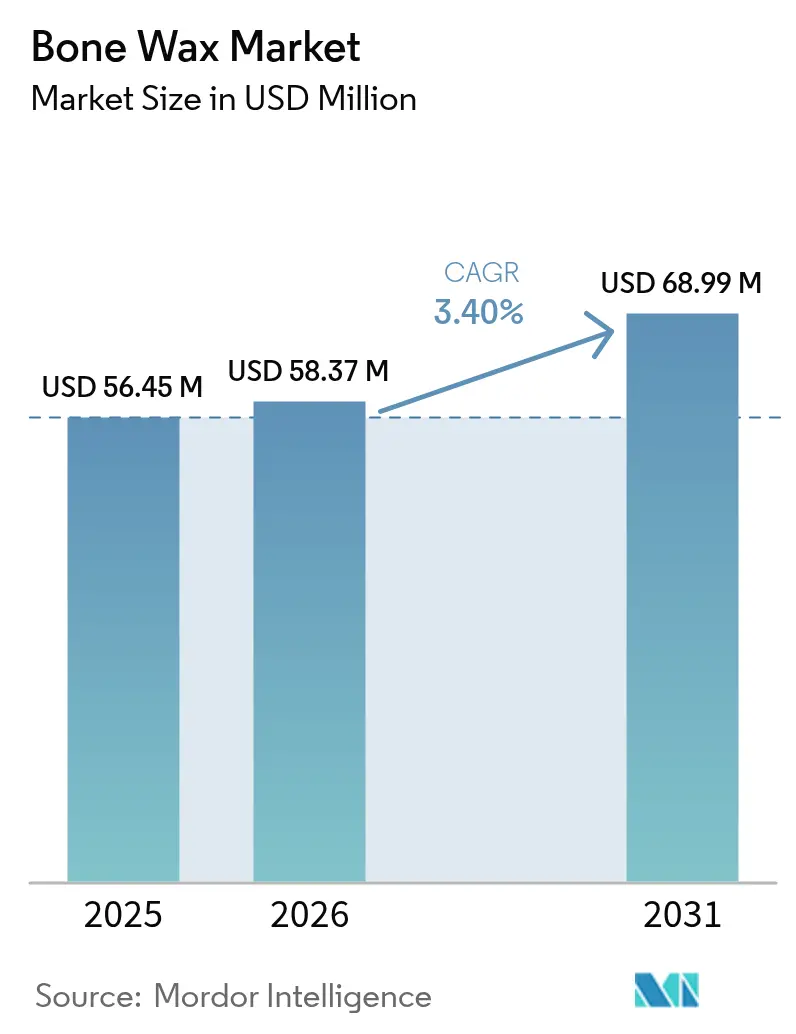

| Market Size (2026) | USD 58.37 Million |

| Market Size (2031) | USD 68.99 Million |

| Growth Rate (2026 - 2031) | 3.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bone Wax Market Analysis by Mordor Intelligence

The bone wax market size was valued at USD 56.45 million in 2025 and estimated to grow from USD 58.37 million in 2026 to reach USD 68.99 million by 2031, at a CAGR of 3.40% during the forecast period (2026-2031). Demand is shaped by the transition from beeswax-based, non-absorbable formulations to synthetic, fully absorbable alternatives that lower infection risk and support bone regeneration. Strategic acquisitions by diversified device leaders signal confidence in next-generation hemostats as critical differentiators in surgical outcomes. Regional performance remains uneven: North America benefits from deep ambulatory surgical center (ASC) penetration, while Asia-Pacific registers the fastest growth as infrastructure spending lifts surgical volumes. Competitive intensity is rising as supply chain volatility in medical-grade beeswax accelerates interest in synthetic substitutes that offer consistency and predictable pricing.

Key Report Takeaways

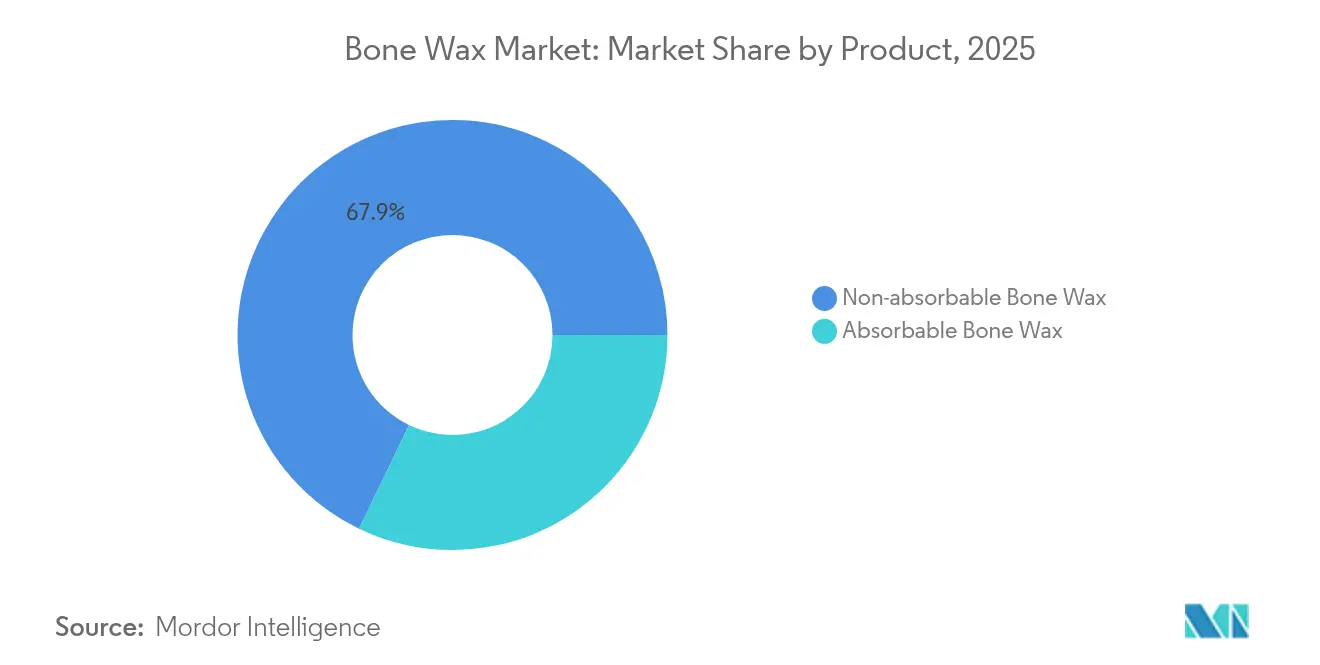

- By product, non-absorbable wax held 67.85% of bone wax market share in 2025; absorbable variants are advancing at a 5.08% CAGR through 2031.

- By material composition, beeswax formulations accounted for 54.12% of the bone wax market size in 2025, whereas β-TCP/starch composites are projected to expand at a 5.57% CAGR to 2031.

- By form, sticks led with 55.21% revenue share in 2025; putty is the fastest-growing at a 4.86% CAGR through 2031.

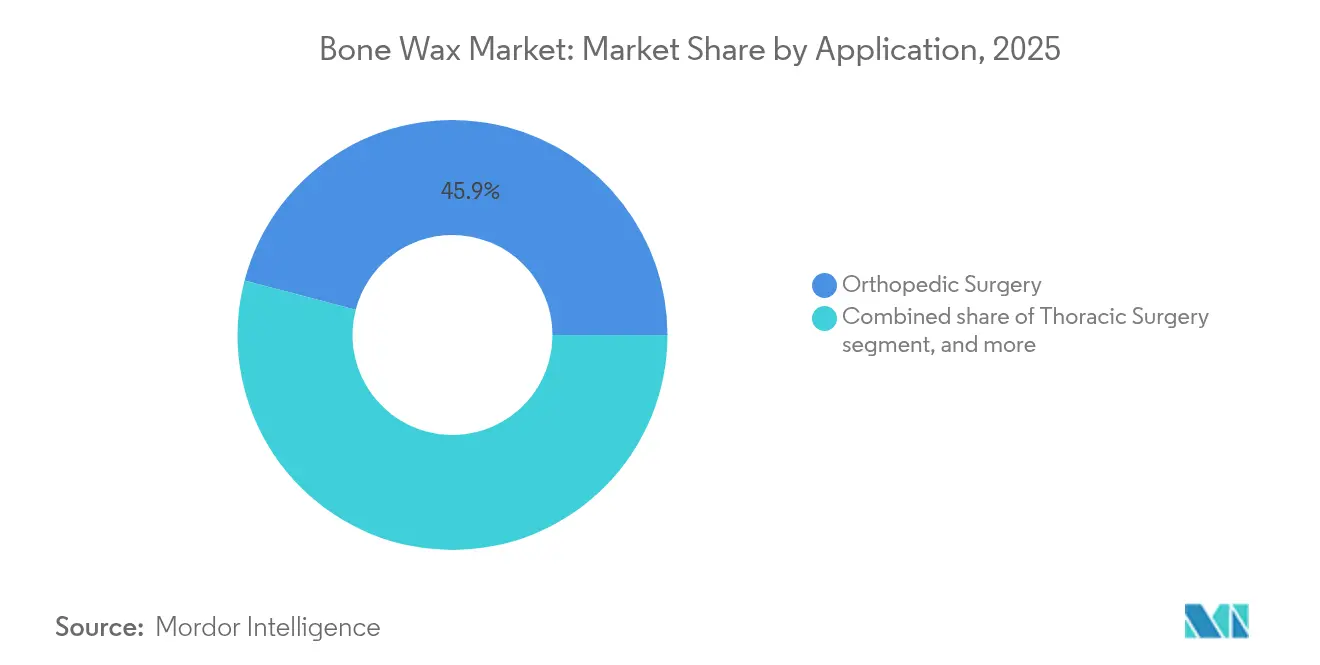

- By application, orthopedic surgery commanded 45.92% share of the bone wax market size in 2025, while neurosurgery records the highest 5.89% CAGR to 2031.

- By end-user, hospitals held 57.25% of bone wax market share in 2025, yet ASCs are scaling quickest at a 6.12% CAGR through 2031.

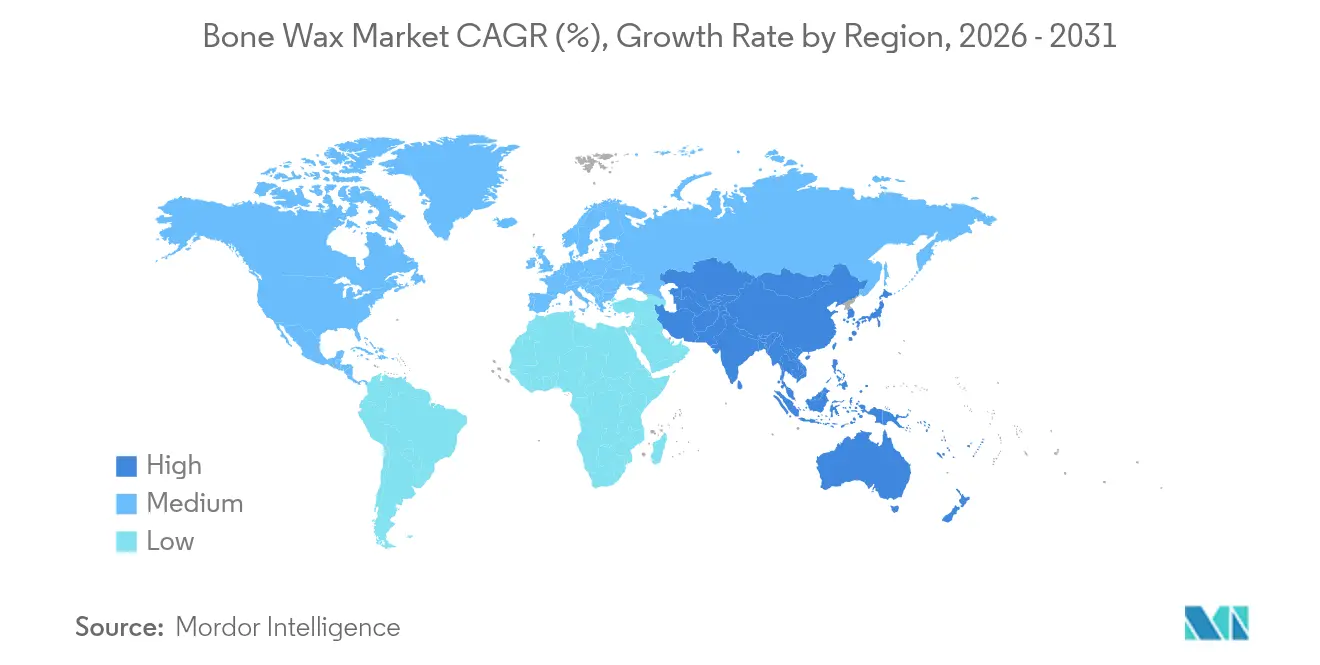

- By geography, North America led with 41.26% revenue share in 2025; Asia-Pacific is forecast to post a 4.64% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bone Wax Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of orthopedic and trauma surgeries | +0.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Growing adoption of absorbable hemostatic technologies | +0.7% | North America & Europe leading, Asia-Pacific following | Long term (≥4 years) |

| Expanding ambulatory surgical center infrastructure | +0.6% | North America core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Increasing healthcare expenditure in emerging economies | +0.5% | Asia-Pacific core, spill-over to MEA & South America | Long term (≥4 years) |

| Technological advancements in biocompatible hemostats | +0.4% | Global, R&D centered in North America & Europe | Long term (≥4 years) |

| Strategic military and disaster-preparedness procurement | +0.2% | North America, Europe, select Asia-Pacific markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Orthopedic and Trauma Surgeries

Orthopedic case volumes continue to climb as aging populations drive demand for joint replacements and complex spine fusion procedures. Randomized studies confirm that intraoperative bone wax lowers postoperative blood loss in total knee arthroplasty, reducing transfusion requirements and enhancing recovery. Trauma centers also favor rapid-acting wax because emergency interventions require immediate bleeding control without compromising later bone healing. The march toward minimally invasive orthopedic techniques heightens the need for precisely applied, moldable wax capable of sealing cancellous bone through narrow surgical corridors. Artificial-intelligence-guided planning tools are further tightening operating times, rewarding products that deliver reliable hemostasis on the first pass.

Growing Adoption of Absorbable Hemostatic Technologies

Clinical preference is shifting toward resorbable formulations that disappear within weeks, sidestepping foreign-body reactions typical of beeswax. Pre-clinical work with β-tricalcium-phosphate–starch composites shows full bone regeneration inside six weeks while maintaining bleeding control equivalent to conventional wax. The United States Food and Drug Administration (FDA) now weighs resorption profiles more heavily in 510(k) reviews, steering hospitals toward absorbable alternatives[1]U.S. Food and Drug Administration, “Premarket Notification 510(k) Review Guidance,” fda.gov. Synthetic alkylene-oxide copolymers match the handling of traditional sticks yet dissolve fully, reducing chronic inflammation risks. Mounting evidence of non-absorbable wax–linked osteitis in revision surgeries is prompting value-conscious payers to embrace absorbables even at higher unit costs.

Expanding Ambulatory Surgical Center Infrastructure

ASC procedure volumes are projected to outpace in-patient settings through 2030, propelled by payer incentives and patient preference for lower-cost sites. Industry analyses forecast a 22% jump in ASC orthopedic cases over the next decade, creating steady pull-through for lightweight, room-temperature-stable hemostats that simplify inventory management. Baxter’s enhanced Hemopatch eliminates refrigeration, dovetailing with ASC logistics constraints and enabling broader shelf deployment. Device firms that tailor packaging sizes for smaller stockrooms and cross-specialty use gain an edge as ASC administrators rationalize formularies.

Increasing Healthcare Expenditure in Emerging Economies

Rising per-capita spending and government-backed insurance rollouts in Asia-Pacific expand surgical capacity and widen access to modern hemostats. Localized manufacturing clusters in India, Malaysia, and Vietnam lower landed costs for bone wax producers, enhancing supply-chain resilience. Hospitals in these regions favor formulations that forgo cold-chain logistics, opening the door for synthetic, shelf-stable absorbables that ease rural distribution challenges. Investment in tele-surgery platforms further broadens market reach, bringing advanced orthopedic procedures—and their hemostatic requirements—to secondary cities.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory and sterility compliance requirements | -0.9% | Global, most stringent in North America & Europe | Medium term (2-4 years) |

| Availability of advanced polymeric substitute products | -0.6% | North America & Europe leading, expanding globally | Long term (≥4 years) |

| Concerns over postoperative infection and healing complications | -0.4% | Global, heightened awareness in developed markets | Medium term (2-4 years) |

| Volatility in medical-grade beeswax supply chain | -0.3% | Global; sourcing concentrated in Asia-Pacific & Africa, impacting North American / European buyers | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Sterility Compliance Requirements

The FDA’s Quality Management System Regulation, effective February 2026, compels alignment with ISO 13485:2016, elevating quality-system costs for small and mid-tier suppliers. Ethylene-oxide sterilization capacity cuts add scheduling bottlenecks, and mandatory supply-chain disruption notifications intensify administrative burden. European Union Medical Device Regulation (EU-MDR) post-market surveillance demands further escalate evidence-generation expenses. Collectively, these mandates may accelerate consolidation as only well-capitalized firms can amortize the compliance load.

Availability of Advanced Polymeric Substitute Products

Breakthroughs in bio-inspired hydrogels and chitosan-based dressings deliver faster clotting and intrinsic antimicrobial properties, diverting surgeon attention from classic bone wax. Blood-imbibing and cross-linking microparticles achieve superior clot strength in pre-clinical trials. FDA clearance of plant-derived hydrogels for trauma care underscores the pace of substitute innovation, eroding the legacy franchise of beeswax-centric products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Absorbable Innovation Challenges Traditional Dominance

Non-absorbable wax retains scale, but the narrative of the bone wax market is tilting toward products that vanish after surgery. Non-absorbables held 67.85% share in 2025, yet absorbables, riding a 5.08% CAGR, are catching up. In dollar terms, the segment’s contribution to bone wax market size could approach USD 31.6 million by 2031 if uptake continues. Surgeons cite lower chronic inflammation and smoother revision surgery when choosing dissolving waxes. Hospital value-analysis committees increasingly factor readmission penalties when selecting hemostats, favoring resorbables with documented healing benefits.

Regulators reinforce this shift: the FDA’s emphasis on biocompatibility and resorption data accelerates 510(k) clearance for absorbable products. Baxter’s OSTENE, which liquefies within 48 hours, illustrates how immediate hemostasis and rapid resorption can coexist baxter.com. As supply disruptions in beeswax unfold, absorbables also provide procurement stability because their ingredients originate from industrially synthesized polymers rather than agricultural supply chains.

By Material Composition: Synthetic Alternatives Disrupt Beeswax Dominance

Beeswax formulas accounted for 54.12% revenue in 2025, anchored by clinician familiarity and low price. Yet β-TCP/starch composites are sprinting ahead, clocking a 5.57% CAGR and gaining endorsements for osteoconductivity. The bone wax market size attached to synthetic materials is primed to double by 2031, reducing reliance on unpredictable wax harvests. Paraffin-based blends and alkylene-oxide copolymers serve as transitional solutions for institutions not yet ready to leap into fully bioactive territory.

Research indicates β-TCP integration accelerates trabecular bridging, making the material attractive for high-risk fusion procedures. Contract manufacturers, facing polytetrafluoroethylene shortages, now diversify into starch-based lines to de-risk supply. Sustainability agendas within hospital groups further nudge adoption of synthetic resorbables, positioning them as long-term replacements for beeswax.

By Form: Putty Innovation Drives Surgical Efficiency

Sticks remained dominant with 55.21% of 2025 revenue because they dovetail with standardized instrument trays and sterile technique. However, putty formulations now expand at 4.86% CAGR, winning favor for irregular bony contours in craniofacial and spine surgery. Pellets carve a niche in minimally invasive settings, where precise dosing prevents excess foreign body.

Putty’s malleability addresses procedural pain points: it molds to decorticated surfaces and stays put in gravity-challenged orientations. Endoscopic spine specialists refine the “bone wax on pattie” approach to avoid lens contamination while maintaining seal integrity. Across the bone wax market, form factor evolution supports faster closure times and reduced instrument exchanges, critical in outpatient centers that prize throughput.

By Application: Neurosurgery Leads Growth Through Technical Sophistication

Orthopedic surgery delivered 45.92% of 2025 sales given the sheer volume of joint replacements. Yet neurosurgery registers the steepest 5.89% CAGR, reinforcing its status as the innovation beachhead of the bone wax market. Cerebral procedures demand impeccable hemostasis, and willingness to pay for premium resorbables is high. FloSeal’s 20-year clinical run in cranial and spinal cases underscores the cost savings linked to reliable bleeding control.

Thoracic teams continue to rely on wax to prevent marrow emboli during sternotomies, but adoption growth is steadier. As robotics penetrates spine surgery, wax that adheres under irrigation gains traction. Evidence-based guidelines stress selecting agents proven to minimize postoperative hematoma, especially in anticoagulated patients.

By End-user: Ambulatory Centers Drive Market Transformation

Hospitals absorbed 57.25% of 2025 demand, yet ASC procurement headcounts now swell. ASCs log a 6.12% CAGR as payers reward site-neutral reimbursement and surgeons migrate high-throughput orthopedic lists to outpatient suites. Room-temperature technology meets ASC storage realities, eliminating cold boxes while freeing capital for advanced implants. Specialty clinics and dental offices represent a consistent but smaller tail, using wax for maxillofacial graft stabilization and periodontal surgeries.

ASC administrators rationalize SKUs, selecting single wax lines that cover orthopedics, ENT, and spine. Device firms supplying unit-dose, peel-pack putty gain first-mover advantage. For the bone wax industry, mastering ASC logistics—short lead times, auto-replenishment portals, and consignment inventory—emerges as a decisive differentiator.

Geography Analysis

North America commanded 41.26% of 2025 revenue, anchored by entrenched reimbursement pathways and dense ASC networks. Academic centers streamline hemostat formularies, netting USD 1 million savings through protocol enforcement that favors clinically validated absorbables. Recent weather events, such as Hurricane Helene, highlighted vulnerabilities in sterile-fluid plants and prompted federal invocation of the Defense Production Act to shore up domestic manufacturing capacity. These disruptions amplify hospital preference for suppliers with regional warehousing and redundant sterilization hubs. Regulatory vigilance remains intense; manufacturers face spot audits as the FDA tracks ethylene-oxide emissions, nudging the bone wax market toward low-residue sterilization alternatives.

Asia-Pacific emerges as the fastest-growing territory at 4.64% CAGR, fueled by aggressive infrastructure build-out and favorable demographic momentum. Governments extend universal health schemes that unlock deferred elective surgeries. Singapore’s integrated ASC campuses underscore the region’s shift to value-based models, pairing day surgery volume with stringent quality metrics. Local device production in India and China shortens lead times and cushions currency volatility. These trends bolster the bone wax market as surgeons gain access to contemporary absorbable options without import delays.

Europe contributes steady revenue underpinned by sophisticated clinical practice guidelines and an innovation-oriented device ecosystem. Adoption pace of synthetic β-TCP wax aligns with the region’s orthopedic centers of excellence, which publish outcome data that ripple globally. The evolving EU-MDR regime extends product life-cycle surveillance, compelling suppliers to launch post-marketing studies that enhance formulary acceptance. In the Middle East & Africa and South America, rising surgical tourism and public-private partnership hospitals open fresh niches. Providers in these regions favor shelf-stable wax products that circumvent cold-chain gaps, gradually enlarging the addressable bone wax market.

Competitive Landscape

The bone wax market shows moderate concentration as multinationals harness scale in R&D, regulatory affairs, and distribution. Stryker’s USD 4.9 billion purchase of Inari Medical in February 2025 broadened its endovascular footprint and, by extension, access to hemostatic product bundles. Merit Medical’s USD 120 million acquisition of Biolife in May 2025 signals a land-grab for niche bleeding-control platforms. These moves reshape share dynamics and hint at portfolios that entwine vascular, orthopedic, and neuro-hemostats.

Technology differentiation intensifies. Synthetic resorbables that double as osteoconductive scaffolds headline product pipelines. Blood-imbibing microparticle research at university labs forms the distant competitive horizon, promising clot formation within seconds. Quality-system reforms scheduled for 2026 elevate entry barriers, favoring incumbents with ISO-aligned sites and digital traceability. Meanwhile, smaller innovators leverage contract manufacturing to circumvent capex yet must fend off scale-driven pricing from giants.

Digital supply-chain initiatives gain urgency post-pandemic. Artificial-intelligence forecasting tools optimize resin and wax feedstock purchases, reducing stock-outs. 3D-printed applicators tailored to patient anatomy are under evaluation, potentially bundling with bone wax cartridges for personalized hemostasis. Midsize firms pursue geographic adjacencies—Latin America, Southeast Asia—to hedge against saturated North American accounts. The net result is a bone wax market where scale, technology, and regulatory readiness interlock as primary success factors.

Bone Wax Industry Leaders

Baxter International Inc.

Johnson & Johnson (Ethicon)

B. Braun Melsungen AG

Medtronic plc

Abyrx Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Baxter released Hemopatch Sealing Hemostat formulated for room-temperature storage, targeting ASC demand for refrigeration-free products.

- May 2025: Merit Medical closed a USD 120 million deal for Biolife, adding proprietary bleeding-control devices to its surgical portfolio.

- April 2025: Baxter released Hemopatch Sealing Hemostat formulated for room-temperature storage, targeting ASC demand for refrigeration-free products.

- February 2025: Teleflex bought BIOTRONIK’s Vascular Intervention unit for EUR 760 million (USD 820 million), integrating drug-coated balloons and stents that complement bone hemostat usage.

- February 2025: Stryker completed its USD 4.9 billion acquisition of Inari Medical, entering high-growth peripheral vascular therapy and expanding its thrombectomy-focused hemostatic toolkit.

- December 2024: The FDA approved Symvess, the first acellular tissue-engineered vessel for extremity vascular trauma, opening new frontiers for regenerative hemostasis.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the bone wax market as the global sales value of sterile bees-wax or synthetic formulations applied directly on bone surfaces to secure mechanical hemostasis during orthopedic, neurosurgical, thoracic, oral, and trauma procedures. According to Mordor Intelligence, the baseline year 2025 total stands at USD 56.45 million.

Scope exclusion: The sizing leaves out collagen sponges, gelatin foams, flowable sealants, and bone graft substitutes that deliver hemostatic benefits but are not classified as bone wax.

Segmentation Overview

- By Product

- Absorbable Bone Wax

- Non-absorbable Bone Wax

- By Material Composition

- Beeswax-based

- Paraffin / Petroleum-based

- Synthetic Alkylene-Oxide Copolymers

- ?-TCP / Starch Composite Resorbables

- By Form

- Sticks

- Pellets

- Putty

- By Application

- Orthopedic Surgery

- Thoracic Surgery

- Neurosurgery

- Other Applications

- By End-user

- Hospitals

- Ambulatory Surgical Centers

- Specialty & Dental Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed orthopedic and cardiothoracic surgeons, procurement heads at hospitals and ASCs, and regulatory consultants across North America, Europe, and Asia-Pacific. These discussions tested preliminary demand pools, current stick-per-case norms, pricing dispersion, and the shift toward fully resorbable blends, supplying the critical reality check before final modeling.

Desk Research

We screened publicly available sources such as the US FDA 510(k) database, WHO Global Health Observatory surgery counts, Eurostat hospital discharge files, and national trauma registries to benchmark procedure volumes. Trade associations, including the International Society of Orthopaedic Surgery and the Society of Thoracic Surgeons, provided guideline updates that influence wax usage per case. Company filings retrieved through D&B Hoovers and news archives from Dow Jones Factiva helped validate average selling prices and competitive moves. Peer-reviewed journals (Journal of Bone & Joint Surgery, Neurosurgery, Annals of Thoracic Surgery) offered incidence ratios and absorbable adoption trends, while import-export dashboards such as Volza clarified shipment patterns into emerging markets. The sources listed illustrate our desk research foundation; many additional datasets were consulted for cross-checks.

Market-Sizing & Forecasting

A top-down model reconstructs demand by multiplying country-level orthopedic, neurosurgical, and sternotomy volumes with validated wax utilization rates, which are then adjusted by absorbable penetration percentages and average selling price corridors. Select bottom-up roll ups, supplier shipment audits and channel checks, are used to fine-tune regional totals. Key inputs include elective hip and knee replacement counts, spinal fusion growth, the ratio of absorbable to non-absorbable units, ASC surgical share, and ASP erosion tied to competitive tender cycles.

Multivariate regression against these drivers underpins the 2025-2030 forecast, while scenario analysis captures upside from faster ASC expansion or downside from alternative sealant uptake. Data gaps in low-reporting geographies are bridged with proxy procedure ratios drawn from comparable income clusters and validated by local experts.

Data Validation & Update Cycle

Outputs run through variance checks versus independent shipment tallies, outlier flags trigger analyst peer review, and senior review signs off the file. Reports refresh annually, with mid-cycle revisions if device recalls, regulation, or currency swings materially alter the baseline.

Why Mordor's Bone Wax Baseline Commands Reliability

Published figures often diverge because firms select different device baskets, currency years, and refresh rhythms. Our disciplined scope and yearly update cadence minimize those blind spots.

Key gap drivers include inclusion of adjacent hemostats, region-limited procedure audits, and single ASP assumptions that over- or understate value in mixed-income markets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 56.45 million (2025) | Mordor Intelligence | |

| USD 54.82 million (2024) | Regional Consultancy A | excludes absorbable variants; currency fixed at 2023 averages |

| USD 71.48 million (2024) | Global Consultancy B | bundles synthetic resorbable sealants; uses one global ASP |

| USD 53.10 million (2023) | Industry Journal C | sources limited to North American hospital surveys; biennial updates |

The comparison shows that when scope, pricing granularity, and update frequency are carefully aligned, Mordor delivers a balanced, transparent baseline clients can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the bone wax market?

The bone wax market is valued at USD 58.37 million in 2026 and is forecast to reach USD 68.99 million by 2031.

Why are absorbable bone wax products gaining traction?

Absorbable waxes resorb within weeks, reduce foreign-body reactions, and align with FDA preferences for biocompatible, resorbable devices, driving a 5.08% CAGR in this segment.

Which region is growing fastest for bone wax demand?

Asia-Pacific posts the highest 4.64% CAGR through 2031 thanks to expanding surgical infrastructure and rising healthcare spending.

How are ambulatory surgical centers influencing the bone wax industry?

ASCs emphasize cost-efficient, outpatient procedures, spurring demand for room-temperature-stable waxes and contributing a 6.12% CAGR in ASC purchases.

What key restraint could slow bone wax market growth?

Stringent regulatory and sterility compliance demands—such as new FDA Quality Management System Regulation mandates—add cost and complexity, potentially reducing smaller suppliers’ competitiveness.

Which material category shows the strongest growth outlook?

Β-TCP/starch composite resorbables lead material innovation with a projected 5.57% CAGR, capitalizing on superior biocompatibility and regenerative properties.

Page last updated on: