Softgel Capsules Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

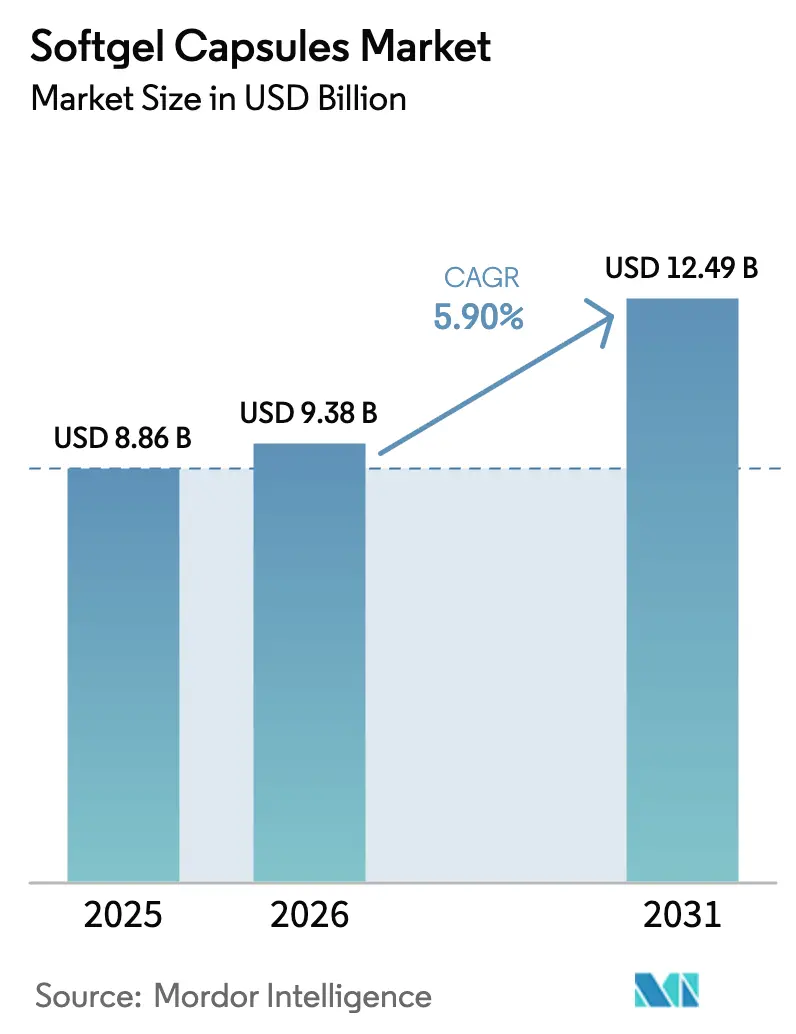

| Market Size (2026) | USD 9.38 Billion |

| Market Size (2031) | USD 12.49 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

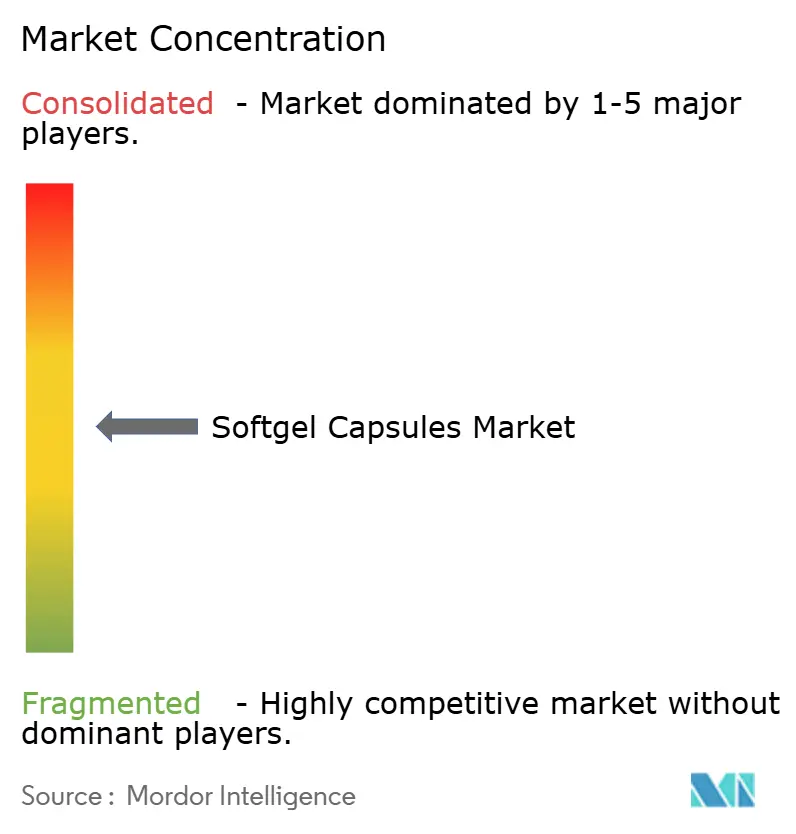

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Softgel Capsules Market Analysis by Mordor Intelligence

The Softgel Capsules market size is expected to grow from USD 8.86 billion in 2025 to USD 9.38 billion in 2026 and is forecast to reach USD 12.49 billion by 2031 at 5.9% CAGR over 2026-2031. Ongoing shifts toward plant-based shells, precision drug delivery, and regionally diversified manufacturing underpin this trajectory. Pullulan-based Plantcaps and HPMC variants are gaining favor as regulatory pressure on animal sourcing intensifies and consumers gravitate toward clean-label products. Technological breakthroughs—such as Evonik’s plasticizer-free EUDRAGIT FL 30 D-55 and GELITA’s one-step DELASOL system—accelerate formulation cycles, broaden biologics applicability, and reduce cost overruns. Meanwhile, supply-chain localization in Asia-Pacific and CDMO consolidation in North America and Europe add capacity and shorten lead times, supporting steady expansion despite raw-material volatility.

Key Report Takeaways

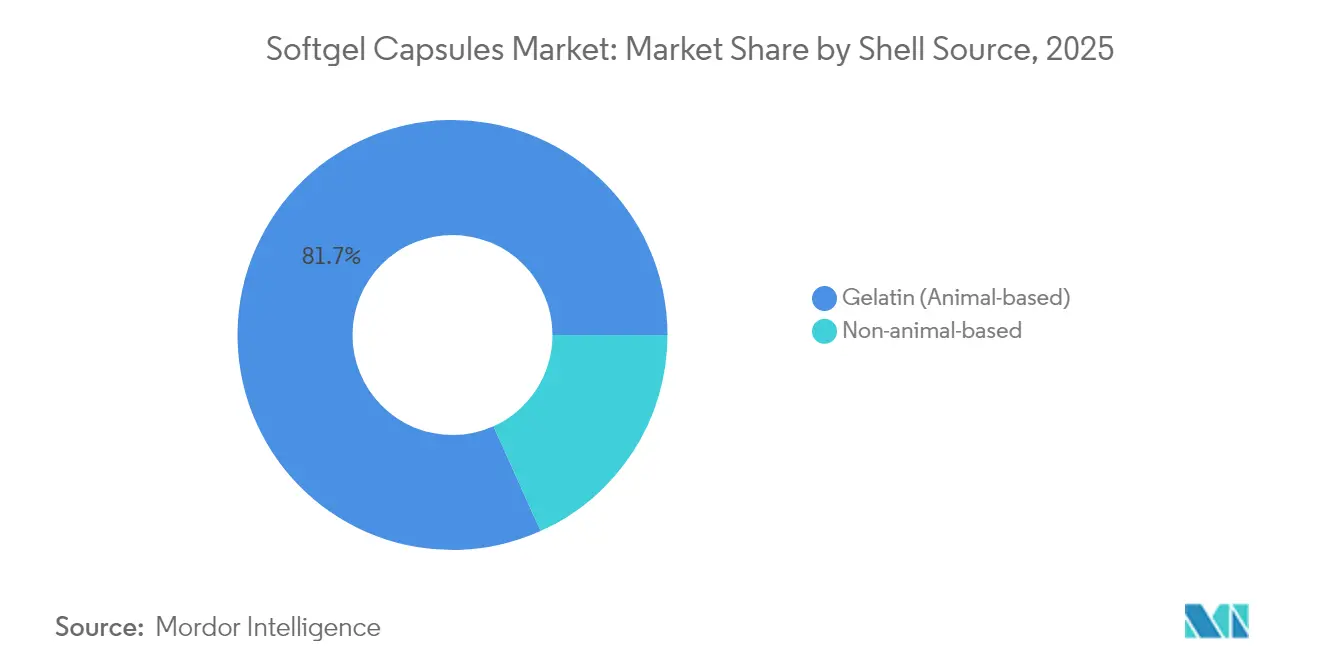

- By shell source, gelatin retained 81.72% of softgel capsules market share in 2025; non-animal shells are projected to grow at a 6.9% CAGR to 2031.

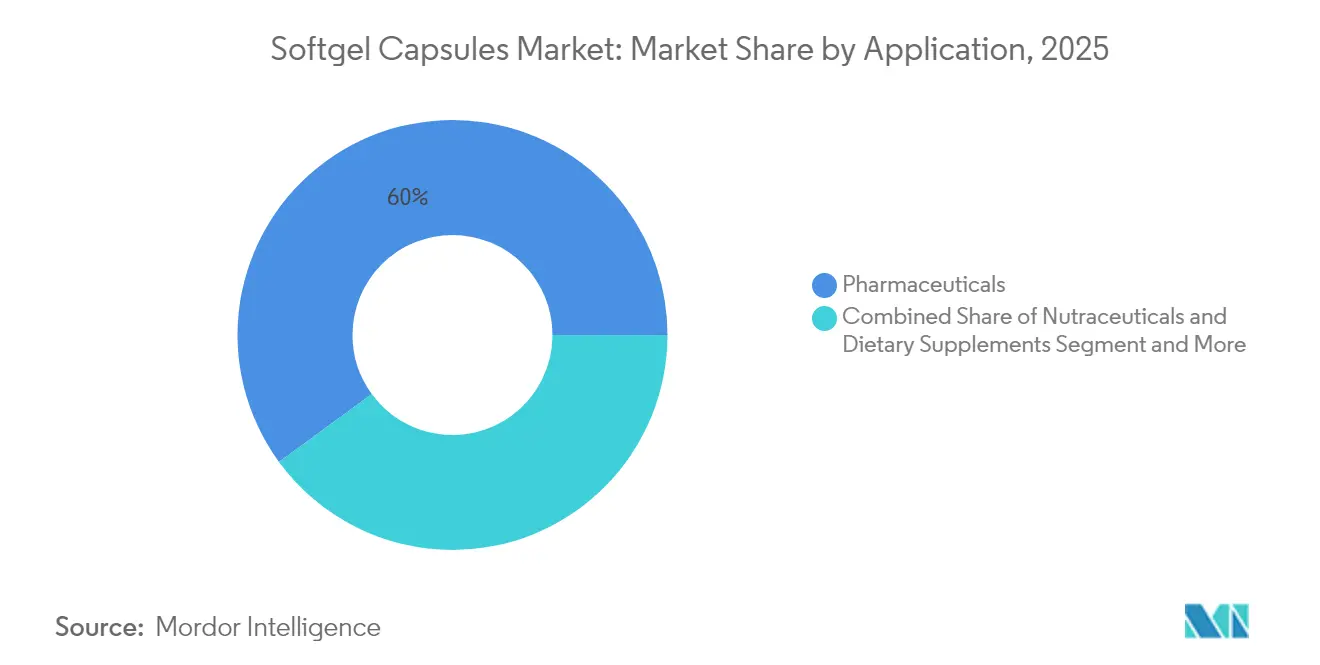

- By application, pharmaceuticals led with 60.05% revenue share in 2025; nutraceuticals are forecast to expand at a 7.55% CAGR through 2031.

- By geography, North America captured 33.22% of the softgel capsules market in 2025, while Asia-Pacific is set to register the fastest 7.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Softgel Capsules Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements and rising R&D spend | +1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Growing demand from health-conscious consumers | +0.9% | Global, led by North America and developed APAC markets | Short term (≤ 2 years) |

| Aging population seeking easy-to-swallow formats | +0.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Precision enteric softgels for biologics pipeline | +0.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Subscription-based personalised nutrition models | +0.5% | North America, Western Europe | Short term (≤ 2 years) |

| APAC CDMO capacity race (supply-chain security) | +0.6% | APAC core, spill-over to global supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements and Rising R&D Spend

Pharmaceutical developers are reallocating budgets toward delivery formats that boost bioavailability, with softgels emerging as a preferred option for poorly soluble APIs. Evonik’s EUDRAGIT FL 30 D-55 cuts preparation times by 70%, thus compressing scale-up windows and reducing capital lock-in.[1]Source: Evonik Industries, “The Gold Standard for Enteric Coatings Has Gone Platinum,” healthcare.evonik.com Patent filings for thioureylene liquids targeting hyperthyroidism and Bacopa monnieri complexes underscore the platform’s versatility. Integrated CDMOs now bundle formulation, analytical, and commercial production under one roof, trimming tech-transfer friction and speeding launches, a trend highlighted by Novo Holdings’ Catalent takeover.

Growing Demand from Health-Conscious Consumers

Shifts toward plant-centric, transparent labeling continue to amplify HPMC and pullulan adoption. Nearly half of supplement users now prefer capsules, citing easier swallowing, odor masking, and quicker onset. Manufacturers are responding by investing in vegan-certified production lines and developing innovative shell materials like carrageenan and pectin-based systems that maintain functionality while meeting dietary restrictions. The convergence of health consciousness and ethical consumption patterns is reshaping product development priorities across the industry.

Aging Population Seeking Easy-to-Swallow Formats

Global aging trends elevate demand for dosage forms tailored to dysphagia. Softgels dissolve in 20-30 minutes and present a smooth contour that eases ingestion, thereby improving adherence in cardiovascular and cognitive therapies. Mechanical optimization studies using differential scanning calorimetry reveal enhanced shell elasticity, mitigating fracture risk during transport. Nutraceutical brands leverage these traits to deliver omega-3, collagen, and vitamin D regimens aimed at joint, vision, and skin health.

Precision Enteric Softgels for Biologics Pipeline

Enteric capsules that protect payloads from gastric pH while ensuring duodenal release are vital for peptides and probiotics. GELITA’s DELASOL one-step technology meets United States Pharmacopeia dissolution criteria without separate coating, trimming QA steps and energy consumption by up to 30%. Lonza’s Enprotect achieves 98% buffer release in 30 minutes and won the 2023 Medicine Maker Innovation Award. MDPI research demonstrated a two-year shelf-life for lactoferrin pellets housed in enteric systems, showcasing viability for fragile biologics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product leakage and heat-humidity stability issues | -0.8% | Global, particularly tropical and humid regions | Short term (≤ 2 years) |

| Stringent sourcing / BSE-free gelatin regulations | -0.6% | Europe, North America, with spillover to global trade | Medium term (2-4 years) |

| Omega-3 supply volatility inflating fill costs | -0.5% | Global, with acute impact on nutraceutical segment | Short term (≤ 2 years) |

| Scale-up barriers for plant-based shell sealing | -0.4% | Global, concentrated in markets transitioning to vegan alternatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Product Leakage and Heat-Humidity Stability Issues

Moisture uptake can weaken seams and hasten oxidation, a critical concern for temperature-sensitive omega-3 fills in tropical regions. Traditional gelatin shells exhibit moisture absorption rates that can compromise seal integrity under extreme conditions, leading to product leakage and reduced shelf-life stability. Advanced Healthcare Materials research published in 2024 emphasized the critical importance of shell formulation optimization using differential scanning calorimetry and mechanical testing to ensure product quality throughout storage conditions.[2]Source: Naharros-Molinero et al., “Shell Formulation in Soft Gelatin Capsules,” onlinelibrary.wiley.com Advances in moisture-barrier coatings and plasticizer blends demonstrate lab-scale promise but await regulatory clearance for broad commercial use.

Stringent Sourcing / BSE-Free Gelatin Regulations

Enhanced surveillance following EFSA’s 2024 assessment compels exhaustive traceability, elevating procurement timelines and raw-material costs.[3]Source: EFSA Panel on Biological Hazards, “BSE Risk Posed by Ruminant Collagen and Gelatine Derived from Bones,” wiley.com Smaller firms, lacking robust audit infrastructures, face disproportionate hurdles, spurring accelerated plant-based adoption. Dual-sourcing strategies—combining bovine-free gelatin with HPMC reserves—are gaining favor as companies strive for uninterrupted supply. Companies are increasingly investing in dual-sourcing strategies that combine traditional gelatin with plant-based alternatives to maintain regulatory compliance while meeting diverse market demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Shell Source: Plant-Based Innovation Accelerates

The gelatin category controlled 81.72% of softgel capsules market share in 2025, supported by reliable supply chains and proven mechanical strength. Nevertheless, non-animal shells are expanding at a 6.9% CAGR as regulatory scrutiny over BSE and consumer ethics motivates formulators to switch. HPMC shells provide moisture protection and faster disintegration, while pullulan offers superior oxygen barriers that safeguard antioxidants and probiotics. Carrageenan and pectin systems are advancing but still face commercial-scale hurdles. Competitive differentiation hinges on balancing shell clarity, seal integrity, and line throughput.

Expanded capacity for plant-based capsules is reshaping supply dynamics. IFF Pharma Solutions markets non-GMO HPMC options designed for hygroscopic botanicals. Gelatin suppliers respond with specialty grades such as low-endotoxin bovine and porcine derivatives compliant with strict pharmacopeial limits. Innovation remains two-pronged: upgrade traditional gelatin while commercializing next-generation vegan alternatives. The softgel capsules market continues to reward players that can flex production lines between both materials without downtime.

By Application: Pharmaceuticals Lead, Nutraceuticals Surge

Pharmaceutical applications accounted for 60.05% of 2025 revenue, buoyed by a wave of poorly soluble NCEs that benefit from lipid-based fills. The softgel capsules market size for pharmaceuticals is projected to grow in the coming years, reflecting regulatory harmonization that unifies bioequivalence pathways. Precision enteric formats address biologic stability challenges, widening the pipeline of therapeutic candidates.

Nutraceuticals, the fastest-growing slice at a 7.55% CAGR, leverage personalized subscription services that bundle micronutrients into daily packs shipped directly to consumers. The softgel capsules market size for nutraceuticals is expected to flourish as data-driven formulations pivot toward immunity, women’s health, and joint care. Cosmetic-nutrition hybrids, often branded “beauty-from-within,” employ co-encapsulation of collagen peptides and biotin to differentiate in a crowded supplement aisle

Geography Analysis

North America maintained leadership with 33.22% of 2025 revenue, powered by deep R&D pipelines, extensive CDMO capacity, and clear FDA pathways that shorten time-to-market. The region benefits from an aging demographic that values swallowable formats and a mature e-commerce nutraceutical channel that promotes personalized packs. Canada’s tax incentives for pharmaceutical R&D and Mexico’s cost-competitive fill-finish sites complement U.S. capacity, fostering a regional cluster effect.

Europe ranks second, characterized by high quality standards and strict gelatin provenance checks following the 2024 EFSA risk reassessment. Germany’s Aenova Group runs multi-site gelatin and vegan softgel lines, while Italy, France, and Spain house specialized CDMOs supporting regional brand owners. Eastern European facilities in Croatia and Poland attract investment as lower-cost hubs that still meet EU GMP.

Asia-Pacific is the fastest riser at 7.7% CAGR, fueled by new plants in Thailand, South Korea, and India that diversify supply chains beyond China. Sirio Pharma’s USD 40 million Thai site and SK pharmteco’s USD 260 million Korean expansion exemplify the regional capacity race. Japan’s stringent quality culture and Australia’s regulatory efficiency serve as gateways for APAC exports destined for Western markets. Rising healthcare expenditure, urbanization, and digital pharmacy adoption underpin sustained demand.

Regulatory Landscape

Softgel capsule development and manufacturing sit across pharmaceutical GMP and dietary supplement CGMP, depending on the end market. In the United States, 21 CFR Part 111 governs dietary-supplement softgels, and FDA inspection regimes shape documentation expectations and quality controls. Large contract facilities that handle regulated materials also navigate DEA registration requirements, as reflected in Federal Register notices in 2025 and 2026.

Outside the US, supplier qualifications and certifications help de-risk sourcing for both gelatin and non-animal shells. Certifications such as NSF International GMP, UL GMP, Halal credentials, and licenses for Japanese pharmaceutical, quasi-drug, and cosmetic manufacturing support global supply chains. EFSA's 2024 risk assessment on BSE-free gelatin reinforces traceability requirements for gelatin supply chains and supports parallel qualification of plant-based shells, while ongoing regulatory actions around import registrations and facility registrations affect how quickly capabilities can be deployed.

Competitive Landscape

The softgel capsules market features a mid-range concentration, following Novo Holdings’ USD 16.5 billion Catalent acquisition. Vertical integration offers one-stop development through commercial production, while smaller innovators carve out niches in vegan shells and high-potency fills. Lonza’s Enprotect won the 2023 Medicine Maker award and the firm subsequently announced plans to divest capsule operations to favor higher-margin CDMO segments.

European CDMOs are scaling vegan capacity as clean-label demand grows; Aenova launched VegaGels and expanded German lines to secure local clients. Asian manufacturers emphasize cost and speed: WuXi STA enlarged peptide and oligonucleotide lines, offering integrated API and dose manufacturing under one Quality Management System. Supply contracts increasingly bundle formulation optimization, analytical method development, and regulatory dossier preparation, shrinking timelines from candidate selection to commercial launch.

Technological competition centers on shell-material science and continuous manufacturing. Patent filings for wax-based sustained release and lipid multiparticulate systems indicate rising R&D spend to solve bioavailability gaps. Companies that can scale plant-based shells without compromising seam integrity or machine throughput stand to capture share as consumer ethics drive purchasing decisions.

Softgel Capsules Industry Leaders

Fuji Capsule Co., Ltd.

Soft Gel Technologies, Inc.

Catalent Inc.

Lonza (Capsugel)

CAPTEK Softgel International

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity is emerging where regulatory documentation needs align with clean-label positioning, with brands looking for auditable traceability and non-animal shells such as HPMC and pullulan without sacrificing throughput. In 2025, gelatin accounted for 81.72% of softgel capsules, and non-animal shells have room to grow as plant-based shell development and GMP certifications broaden formulation flexibility. Non-animal shells are tracking a 6.9% CAGR through 2031, reflecting shifting consumer and retailer preferences toward vegan and clean-label formats.

In pharmaceutical and research supply chains, regulated materials handling continues to widen the qualified supplier base. DEA registration actions for importers and manufacturers of controlled substances illustrate how CDMOs are expanding the capability set to support formulation, analytical validation, and regulatory documentation for softgel development.

Recent Industry Developments

- May 2026: In Asia-Pacific, Fuji Capsule Co. Ltd. reported the successful conclusion of CPHI Japan 2026 held in April 2026. The event signals continued regional engagement for gelatin and alternative-shell softgels. Supplier qualification activities remain a focus as manufacturers pursue dual-shell capabilities.

- February 2026: Catalent announced OptiGel DR softgel technology for enteric release without coating. The technology reduces processing steps and accelerates development timelines for enteric applications. The update reinforces Catalent's focus on specialized softgel platforms for regulated markets.

- October 2025: Soft Gel Technologies Inc. announced PlantOmega, a vegan softgel for algal oil. The launch expands plant-based shell options to nutraceuticals and supports clean-label positioning in omega-3 segments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue earned from manufacturing and supplying softgel capsules, including both gelatin and non-gelatin shells, that are filled and sold for pharmaceuticals, dietary supplements, and selected consumer health uses across major regions.

Scope exclusions: We exclude hard empty capsules, bulk gelatin as a raw material market, and finished nutraceutical brands where the capsule is only one input cost.

Segmentation Overview

- By Shell Source

- Gelatin (Animal-based)

- Non-animal-based

- By Application

- Pharmaceuticals

- Nutraceuticals and Dietary Supplements

- Cosmetics and Personal Care

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping demand and supply signals that can be checked repeatedly, and then aligning them with how softgels are manufactured and sold. We review public health and trade data that indicate supplement and medicine consumption patterns, along with how capsule inputs move across borders.

Common public sources used include US FDA databases and guidance for dosage forms, NIH Office of Dietary Supplements pages, CDC health statistics where relevant to supplement use, UN Comtrade trade statistics for capsule-related and gelatin-related flows, and World Bank macro indicators used for normalization. This is then supported with company annual reports, investor presentations, press releases, and reputable trade publications, plus selective paid subscriptions for company financials and intelligence and patent databases to track formulation and shell innovations. These desk research sources are illustrative and not exhaustive, and many other references were used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Fieldwork focuses on aligning the model to real pricing, capacity behavior, and buying patterns, since public data rarely shows how softgel value split changes by shell type and end use. We spoke with capsule manufacturers, contract manufacturers, ingredient suppliers, and downstream buyers, and we kept the respondent mix across major consuming regions to confirm utilization, average selling prices, and substitution trends between gelatin and non-gelatin shells.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 42% |

| Mid tier: 54% | Functional/Unit leaders: 29% | EMEA: 33% |

| Smaller Players: 15% | Managers: 58% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built by reconstructing the demand pool from end use, then translating it into softgel capsule value using realistic conversion steps. We apply both top-down and bottom-up logic in a practical sequence, where demand is formed from supplement and prescription indicators and then checked against supplier-side signals.

To keep totals grounded, we corroborate the top-down outputs with selective bottom-up approximations, such as sampled price points for gelatin versus non-gelatin shells, capacity and utilization checks shared by manufacturers, and channel checks on contract manufacturing share when softgels are outsourced. Key inputs that materially move the model include the gelatin versus non-gelatin shell mix, the share of softgels within dietary supplements, regional capacity additions and utilization rates, average selling price progression by shell type, and the application mix shift toward higher value formulations.

For forecasting, we use scenario analysis supported by variable-level expectations gathered in interviews, where demand growth is tied to supplement adoption, regional production expansion, and gradual pricing changes from raw material swings. Where bottom-up inputs are missing for smaller countries, gaps are handled through proxy ratios based on comparable markets, then rechecked against trade and macro indicators before finalization.

Data Validation & Update Cycle

Before sign-off, outputs are cross-checked against independent signals, such as trade movement patterns for key inputs, announced capacity expansions, and major demand shifts in supplements and oral dosage forms. Large variances are investigated by revisiting assumptions, rerunning sensitivity checks on the highest-impact variables, and re-contacting relevant respondents when a data point looks inconsistent.

A second analyst reviews the model logic and the final numbers to confirm calculations can be reproduced from the stated inputs. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive an updated view based on the latest available information.

Mordor Intelligence's Softgel Capsules Market Estimate Compared With Other Published Estimates

Published market sizes for softgel capsules often differ because each publisher draws the market boundary differently, and because they use different base years, pricing logic, and currency timing. In this market, the biggest swings usually come from whether the estimate is counting only capsule manufacturing revenue, or also folding in contract fill-finish services and finished supplement brand value.

By tracking capacity utilization and shell mix shifts, then refreshing regional ASP assumptions with interview checks, Mordor Intelligence keeps the total aligned to capsule manufacturing value. This reduces the risk of accidentally including adjacent finished-product revenues that sit outside the market scope.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.38 B (2026) | |

| Trade Publisher A | USD 7.90 B (2024) | Uses an earlier base year and applies a faster growth curve into the forecast window, and parts of the sizing appear to blend capsule value with finished supplement pricing assumptions. |

| Industry Tracker B | USD 8.02 B (2024) | Anchors the estimate to 2024 and uses a more uniform regional progression, with limited visibility into utilization and non-gelatin penetration, which can mute mix-driven value changes. |

Taken together, the spread is mainly explained by year alignment and what revenue layer is being counted. When scope is kept at capsule manufacturing value and the pricing and mix assumptions are rechecked against supply-side reality, the resulting market size becomes easier to trace and update with repeatable steps.

Key Questions Answered in the Report

What is the projected value of the softgel capsules market by 2031?

The market is expected to reach USD 12.49 billion by 2031 at a 5.90% CAGR.

Which shell material is growing fastest?

Non-animal shells, primarily HPMC and pullulan, are growing at a 6.9% CAGR to 2031.

Why are softgels preferred for biologics?

Enteric softgel technologies protect fragile APIs from gastric acid, ensuring targeted intestinal release and higher bioavailability.

Which region shows the highest growth potential?

Asia-Pacific is set to post an 7.7% CAGR through 2031 on the back of new manufacturing investments and healthcare spending.

How are regulations influencing shell sourcing?

Stricter BSE-free mandates in Europe and North America push manufacturers to adopt fully traceable bovine sources and accelerate plant-based alternatives.

Page last updated on: