Biohacking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

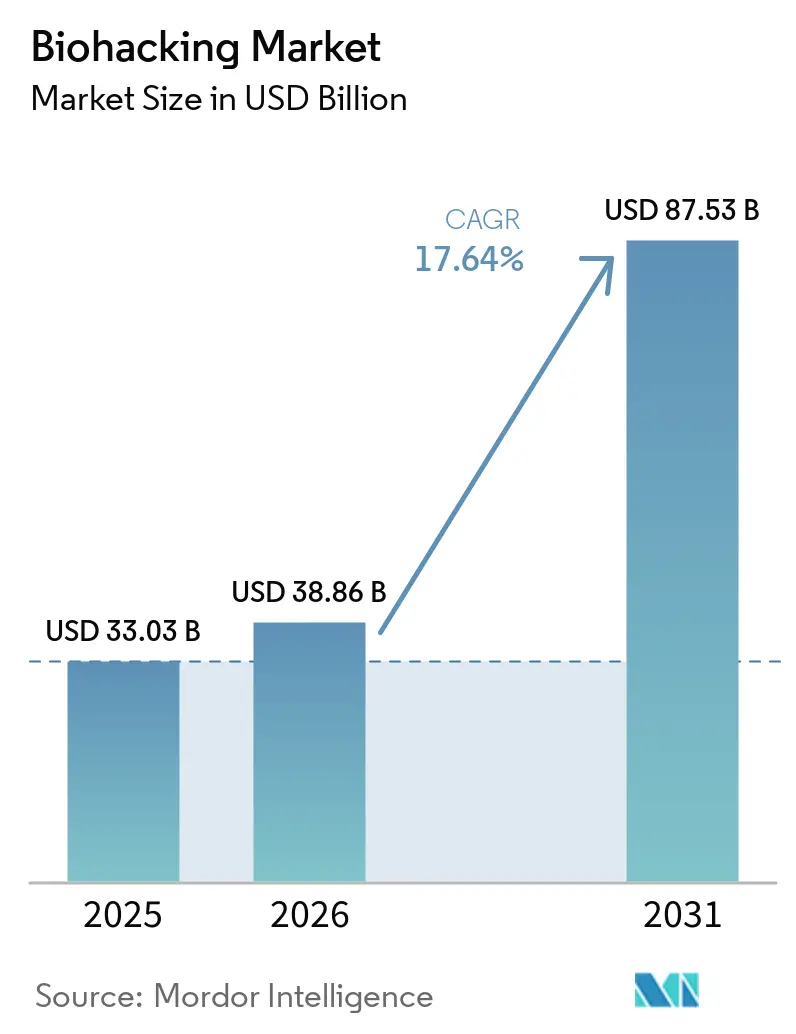

| Market Size (2026) | USD 38.86 Billion |

| Market Size (2031) | USD 87.53 Billion |

| Growth Rate (2026 - 2031) | 17.64% CAGR |

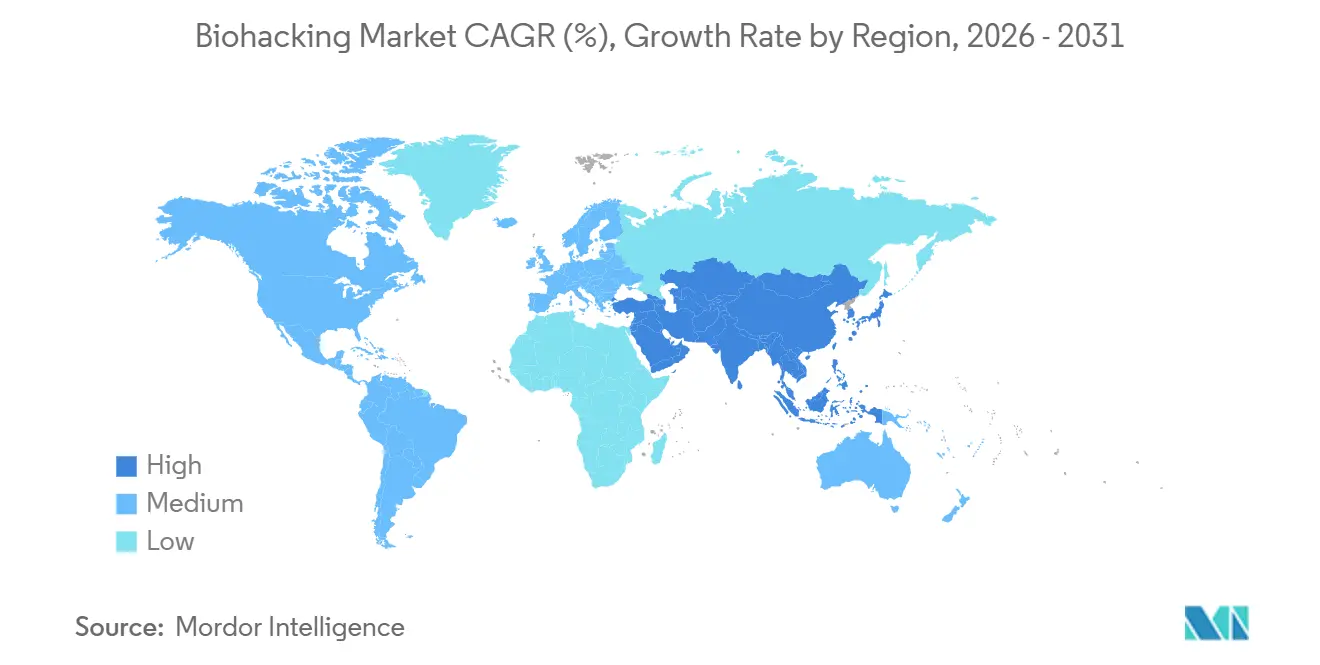

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biohacking Market Analysis by Mordor Intelligence

The Biohacking Market size is projected to expand from USD 33.03 billion in 2025 and USD 38.86 billion in 2026 to USD 87.53 billion by 2031, registering a CAGR of 17.64% between 2026 to 2031.

Demand growth reflects a shift from physician-centric care toward self-directed performance optimization enabled by affordable genetic tests, consumer-grade biosensors, and AI-driven coaching. Mainstream wearables have normalized continuous glucose, heart-rate-variability, and sleep-stage monitoring, while falling reagent prices now let hobbyists run CRISPR demonstrations for less than USD 2 per kit. Rapid venture-capital inflows into human-augmentation start-ups have broadened the innovation pipeline from passive data logging to active biological modification devices. Corporate wellness programs are integrating biometric platforms to lower absenteeism and health-care costs, accelerating enterprise demand.

Key Report Takeaways

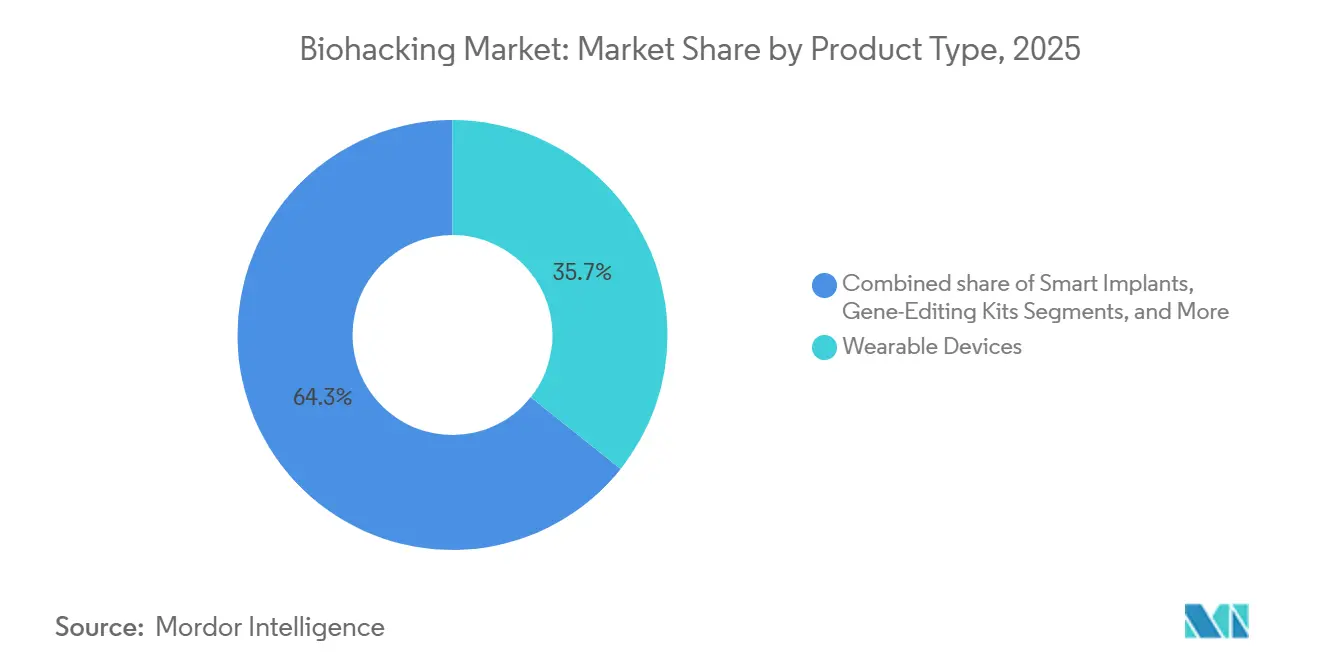

- By product type, wearable devices led with 35.70% of the biohacking market share in 2025, while gene-editing kits recorded the highest projected CAGR at 17.88% through 2031.

- By biohacking type, nutrigenomics accounted for 29.75% of the biohacking market size in 2025 and DIY biology is advancing at an 18.15% CAGR to 2031.

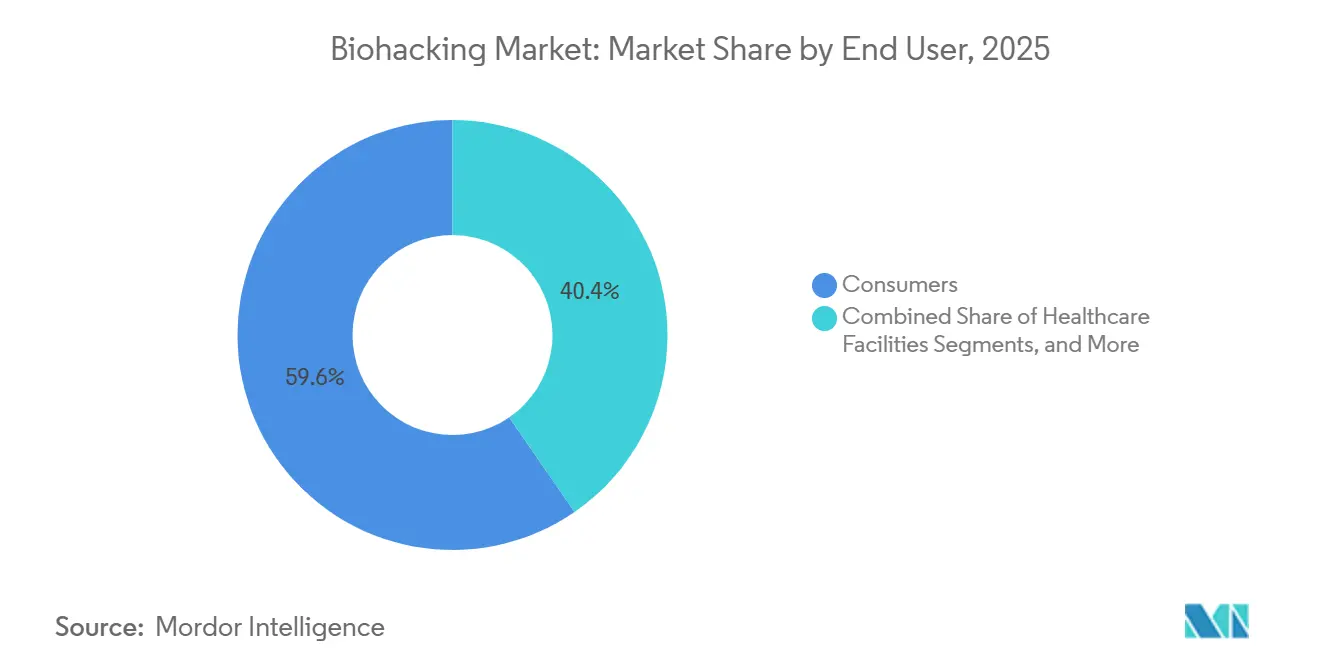

- By end user, consumers held 59.55% of demand in 2025; research and academic institutes show the fastest expansion at a 18.71% CAGR through 2031.

- By geography, North America claimed 41.75% revenue share in 2025, whereas Asia-Pacific is forecast to progress at a 19.24% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biohacking Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream uptake of consumer wearables | +4.2% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Venture capital inflows into human-augmentation start-ups | +3.8% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Declining cost of genetic-testing kits | +2.9% | Global, with fastest adoption in APAC | Medium term (2-4 years) |

| Corporate wellness programs adopting biometric tracking | +2.1% | North America & Europe | Short term (≤ 2 years) |

| Open-source bio-protocol libraries & DIY labs | +1.4% | Global, concentrated in tech hubs | Long term (≥ 4 years) |

| Military R&D into human-performance enhancement | +1.1% | North America, Europe, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mainstream Uptake of Consumer Wearables

Consumer wearables have evolved from simple step counters into multi-sensor health platforms capable of ECG-grade heart monitoring and continuous glucose measurements, exemplified by Abbott’s Lingo winning top honors at CES 2025. Apple’s forthcoming AI-driven “Project Mulberry” underscores Big-Tech commitment to proactive health coaching using on-device analytics rather than cloud processing to protect privacy. University of Hong Kong engineers recently demonstrated organic electrochemical transistors that run machine-learning models inside the sensor itself, further minimizing data-leak risks. Continuous biosensing combined with edge AI shifts biomonitoring from passive data collection to real-time, closed-loop recommendations, widening the user base beyond early adopters. As prices converge with conventional smartwatches, the biohacking market gains a mass-market entry point.

Venture Capital Inflows into Human-Augmentation Start-ups

Funding patterns show a pivot from lifestyle wearables toward clinically actionable enhancement tools. Elemind secured USD 12 million in 2024 to commercialize neuromodulation headbands aimed at sleep optimization and cognitive resilience. General-partner term sheets increasingly emphasize proprietary data sets and algorithmic IP instead of commodity hardware, reflecting investor belief that defensible value resides in longitudinal multimodal biometrics. Mega-rounds in North America spill over into secondary hubs such as Singapore and Berlin, seeding regional innovation clusters. The link between performance enhancement and preventive health positions the biohacking market for blended reimbursement models combining out-of-pocket spending with employer stipends. As exits via SPACs and trade sales mature, capital recycling should fuel successive cohorts of start-ups.

Declining Cost of Genetic-Testing Kits

CRISPR education kits retail near USD 2, a 10-fold drop in three years, democratizing genome editing demonstrations in high-school classrooms. Commercial direct-to-consumer tests now analyze more than 70 nutrition-related genes for personalized diet advice at sub-USD 150 price points, undercutting 2023 tariffs by 40%. Scale economics mirror Moore’s-law curves in sequencing reagents, lowering barriers for nutrigenomic subscription services that bundle meal planning with continuous metabolic telemetry. California’s 2025 rule mandating safety labels on DIY CRISPR kits illustrates regulators’ adaptive stance: enabling educational use while signaling guardrails for unsupervised self-experimentation. Integration of genotype with wearable phenotype data drives precision protocols that expand the addressable biohacking market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty on human enhancement | -2.7% | Global, most restrictive in Europe | Medium term (2-4 years) |

| Data-privacy concerns around continuous biometrics | -1.9% | Europe & North America, spreading globally | Short term (≤ 2 years) |

| Bio-risk of at-home CRISPR experimentation | -1.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Ethical backlash against elective implants | -0.8% | Europe & North America, cultural resistance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corporate Wellness Programs Adopting Biometric Tracking

Employers are shifting from one-size-fits-all screenings to continuous biometric engagement using wrist, arm, or ear-based sensors connected to AI dashboards. Pilots at Fortune 100 retailers report injury-incident reductions of 20% after adopting movement-analysis wearables for warehouse staff, while self-insured tech firms cite double-digit cuts in cardiometabolic claims by nudging high-risk employees toward lifestyle changes. Samsung’s enterprise mobility division provides secure containers that separate personal and corporate health data, easing HIPAA-adjacent privacy worries. As wellness stipends become table stakes in tight labor markets, program differentiation leans on scientifically validated biohacking interventions such as continuous glucose trend alerts rather than generic step challenges. However, unions are pressing for algorithmic transparency to prevent discriminatory use of biometric scoring.

Regulatory Uncertainty on Human Enhancement

The European Union’s Medical Device Regulation classifies neural interfaces as Class III devices, mandating multi-year clinical trials and post-market surveillance that extend commercialization timelines by up to five years relative to less stringent regions. California’s new law requiring consumer warning labels on DIY gene-editing kits hints at a patchwork U.S. approach likely to raise compliance costs for interstate e-commerce. The International Society for Stem Cell Research now recommends labeling commercial CRISPR tools to discourage in vivo self-experimentation, signaling wider professional skepticism. Unpredictable approval pathways deter early-stage investors from backing invasive enhancement devices, skewing capital toward lower-risk software layers. Market incumbents hedge by simultaneous filings in multiple jurisdictions, inflating regulatory budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wearables Dominate While Gene-Editing Accelerates

Wearable devices commanded 35.70% of the 2025 biohacking market share, reflecting mass adoption of smartwatches and arm-based continuous glucose monitors that have crossed over from medical diabetology into mainstream wellness. Gene-editing kits, though niche, are projected to post an 17.88% CAGR, the fastest within the category, as low-cost CRISPR reagents reach educator and hobbyist audiences. The biohacking market size for gene-editing products is expected to surpass USD 5.35 billion by 2031 if current funding momentum persists. In parallel, smart implants such as USC’s battery-less pain-management neurostimulator illustrate future migration from external wearables to embedded therapeutics.

The competitive field is converging on integrated ecosystems that merge sensors, cloud analytics, and personalized interventions. Continuous ketone, lactate, and cortisol sensors under development aim to extend data density beyond heart rate and glucose, heightening platform stickiness. Established medical-device firms leverage regulatory know-how to re-label clinical assets for over-the-counter use, while start-ups exploit agile cycles to iterate firmware and algorithms weekly. Consolidation pressures may surface once component commoditization erodes hardware margins, shifting value capture to subscription insights that mine aggregated biometric databases. Product-level interoperability standards will influence adoption curves, as consumers favor unified dashboards over fragmented app silos.

By Biohacking Type: Nutrigenomics Leads as DIY Biology Surges

Nutrigenomics accounted for 29.75% of 2025 revenue, supported by double-digit growth in direct-to-consumer saliva test kits that guide micronutrient selection and meal planning. DIY biology is forecast to grow 18.15% annually, propelled by open-hardware centrifuges and cloud-based protocol repositories that lower barriers for garage-level experimentation. The biohacking market size for DIY biology tools could triple by 2031 if insurance reimbursements emerge for validated at-home assays. Grinder subculture implants—RFID chips, magnetic fingertips—remain a visible but small slice, constrained by limited clinical validation. Quantified-self tracking continues steady expansion as software platforms synthesize multiyear personal datasets into actionable longitudinal baselines.

Synergies between categories amplify adoption. Nutrigenomic reports increasingly sync with continuous glucose monitors to verify glycemic load responses meal-by-meal, driving repeat-test revenues. Community labs also act as showrooms where novices gain hands-on experience before purchasing commercial kits, blurring education and retail channels. Meanwhile, ethical-risk committees at leading DIY hubs have adopted ISO-like safety audits to pre-empt external regulation, reinforcing public trust and fostering responsible growth of the biohacking market.By Biohacking Type: Nutrigenomics Leads as DIY Biology Surges

By End User: Consumer Primacy With Institutional Acceleration

Consumers generated 59.55% of 2025 demand as wellness culture prioritized personalized data over generalized advice. Research and academic institutes, while only mid-teens on revenue today, show the highest CAGR at 18.71% through 2031, signaling mainstream scholarly acceptance of biohacking methodologies. Hospital systems are piloting closed-loop metabolic monitoring to reduce diabetic readmissions, an early indication of clinical adoption. The biohacking market size attached to higher-education procurement is expected to outpace consumer growth after 2027 as grant funding aligns with precision-health mandates.

Cross-fertilization between consumer and institutional spheres accelerates product validation. Universities provide independent efficacy studies that bolster consumer marketing claims, while aggregated consumer datasets furnish large-N cohorts for academic exploratory analytics. Corporations extend wellness initiatives to dependents, expanding unit economics beyond employees. On-premise data federations address privacy rules by keeping sensitive biometrics within institutional firewalls, creating a parallel channel alongside direct-to-cloud consumer models.

Geography Analysis

North America controlled 41.75% of 2025 revenue, buoyed by FDA fast tracks for over-the-counter biosensors and abundant venture finance clusters in California and Massachusetts. Policy pragmatism—evidence thresholds lower than therapeutic devices yet higher than consumer electronics—has created a predictable pathway for wellness-grade technologies. However, emerging state-level rules on gene-editing kits may fragment domestic compliance regimes, spurring platform providers to build modular regulatory kernels capable of state-specific toggles.

Europe blends funding incentives with strict privacy standards. Horizon-Europe grants finance translational wearables, yet GDPR enforcement obliges data-minimization architectures that raise fixed costs, an entry hurdle for resource-constrained start-ups. The European Court of Justice has already ruled that constant heart-rate streaming constitutes sensitive health data, restricting ad-tech monetization models common in North America. Nonetheless, high disposable incomes and a public-health orientation support premium subscription tiers focused on preventive longevity.

Asia-Pacific posts the fastest CAGR at 19.24% as governments digitize health infrastructure and middle-class populations pursue longevity. China’s strategic biotech plan allocates multibillion-yuan budgets to omics research and sensor fabrication, accelerating domestic scale production that can undercut global prices. Japan leverages its aging-society imperative to pilot AI-linked exoskeletons for elder mobility, translating into favorable reimbursement precedents. India’s digital-health mission integrates wearable data into its national health stack, offering start-ups a massive testing ground. Diverse regulatory maturity across ASEAN markets lets firms tailor risk-based rollouts, learning from early pilots before expanding westward.

Competitive Landscape

The biohacking market sits at a moderate-fragmentation stage. Abbott and Dexcom leverage clinical CGM legacies to secure first-mover consumer mindshare, bundling sensor hardware with subscription analytics. Technology conglomerates such as Apple and Alphabet embed biosensing in broader device ecosystems, erecting data-lock-in moats that smaller rivals struggle to breach. Neuralink’s UK clinical trial demonstrates crossover between medical neuroprosthetics and performance enhancement applications, foreshadowing potential consumer spin-offs.

Start-ups differentiate via vertical depth—single-biomarker mastery—or horizontal breadth—multi-omic integration dashboards. Patent analysis shows rising claims in wireless power transfer for subcutaneous implants and federated-learning algorithms that keep raw biometric data on-device. As sensor hardware commoditizes, algorithmic accuracy and longitudinal data quality become decisive purchase criteria. Partnerships between sensor makers and AI-analytics platforms are proliferating, aiming to deliver turnkey insights to employers and insurers. M&A activity is expected to intensify after 2026 once cohort-level revenue stabilizes, with established med-techs likely to acquire niche AI specialists to shore up platform gaps.

Biohacking Industry Leaders

Apple Inc.

Fitbit, Inc.

Nuanic

Health Via Modern Nutrition Inc

Thriveport, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Biohacking Index Report was released as the first physician-curated, invite-only edition, marking a pivotal shift in the wellness and biohacking ecosystem. This edition reinforces the platform’s guiding principle that credibility, rather than sponsorship or popularity, should determine visibility, setting a new standard for transparency and trust in the industry.

- June 2025: University of Southern California researchers unveiled a wireless AI-powered implant for chronic-pain relief that operates without batteries.

- May 2025: Abbott’s Lingo biowearable received a CES 2025 innovation award for bringing medical-grade glucose sensing to wellness consumers.

Global Biohacking Market Report Scope

As per the scope, biohacking or body hacking is the practice of putting RFID chip implants, sensors, magnets, and other tech implants under the skin.

The Biohacking Market is segmented by Products (Genetic Engineering and Gene Editing Tools, DIY Biology Kits and Biohacking Accessories, Implantable Devices and Wearables, Cognitive Enhancement and Nootropics, and Others), Applications (Medical Diagnostics and Monitoring, Biohacking for Personalized Treatment Plans, Cognitive Enhancement for Mental Performance, Genetic Editing for Personalized Gene Therapies, and Others), End Users (Pharmaceutical and Biotechnology Companies, Research Institutes and Academic Centers, Hospitals and Healthcare Facilities, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). he market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Wearable Devices |

| Smart Implants |

| Gene-Editing Kits |

| Nootropics & Supplements |

| Sensors & Biomonitoring Patches |

| Others |

| Nutrigenomics |

| DIY Biology |

| Grinder (Implantable) |

| Quantified-Self Tracking |

| Performance Pharmacology |

| Others |

| Consumers |

| Healthcare Facilities |

| Research & Academic Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Value) | Wearable Devices | |

| Smart Implants | ||

| Gene-Editing Kits | ||

| Nootropics & Supplements | ||

| Sensors & Biomonitoring Patches | ||

| Others | ||

| By Biohacking Type (Value) | Nutrigenomics | |

| DIY Biology | ||

| Grinder (Implantable) | ||

| Quantified-Self Tracking | ||

| Performance Pharmacology | ||

| Others | ||

| By End User (Value) | Consumers | |

| Healthcare Facilities | ||

| Research & Academic Institutes | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What revenue level is the biohacking market expected to reach by 2031?

Forecasts place the biohacking market at USD 87.53 billion in 2031 based on a 17.64% CAGR.

Which product category currently dominates sales?

Wearable devices lead with 35.70% of 2025 sales owing to mainstream smartwatch and continuous glucose monitor adoption.

Which region is growing fastest in biohacking adoption?

Asia-Pacific is projected to expand at a 19.24% CAGR through 2031, outpacing all other regions.

Why are genetic-testing kits gaining traction?

Sub-USD 150 price points and expanded gene panels make personalized nutrition and health insights accessible to mass-market consumers.

What is the biggest regulatory hurdle facing biohacking companies?

Unclear approval pathways for human-enhancement technologies create multi-year delays and elevated compliance costs, especially in Europe.

Page last updated on: