Medical Biomimetics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

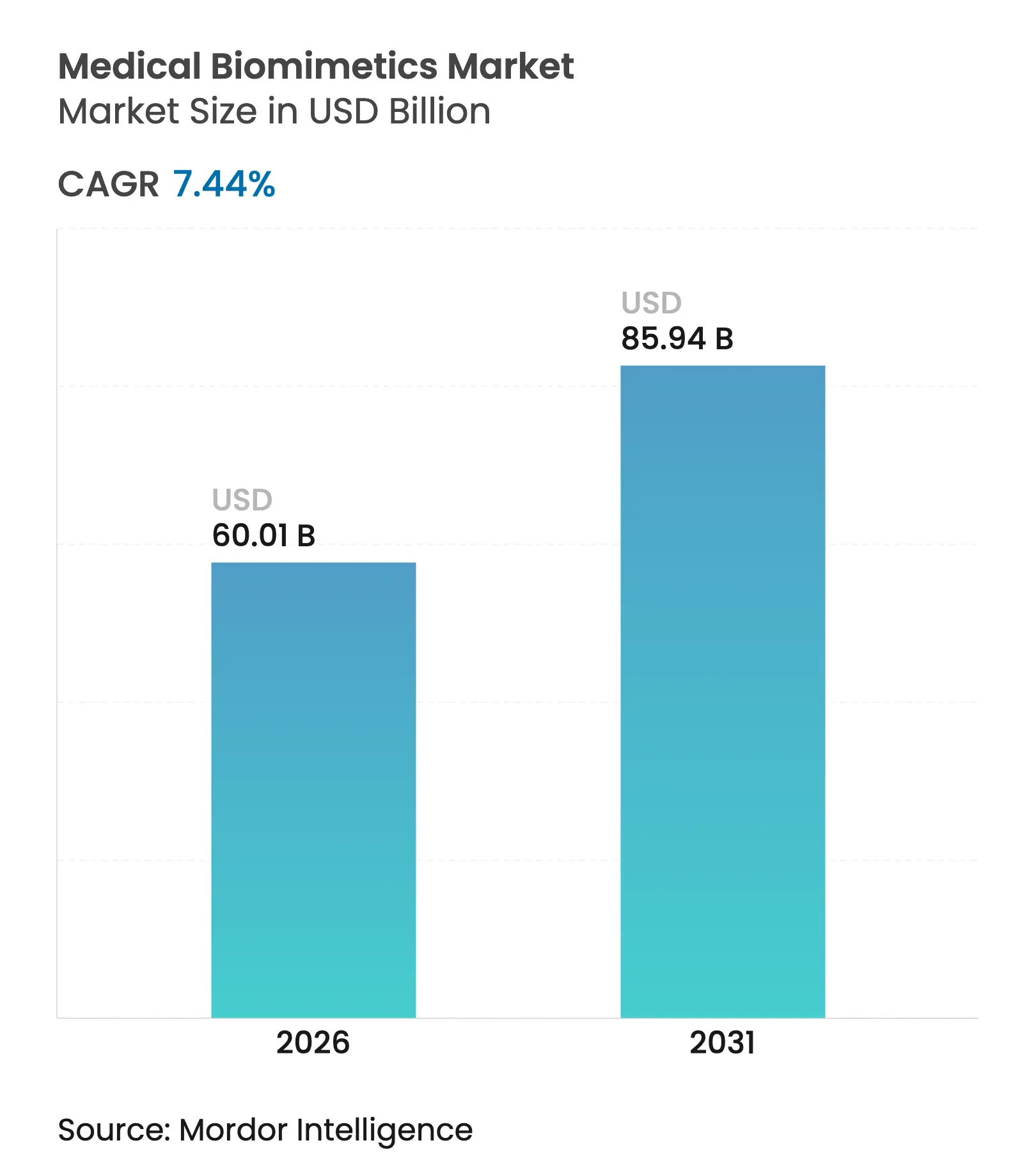

| Market Size (2026) | USD 60.01 Billion |

| Market Size (2031) | USD 85.94 Billion |

| Growth Rate (2026 - 2031) | 7.44 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

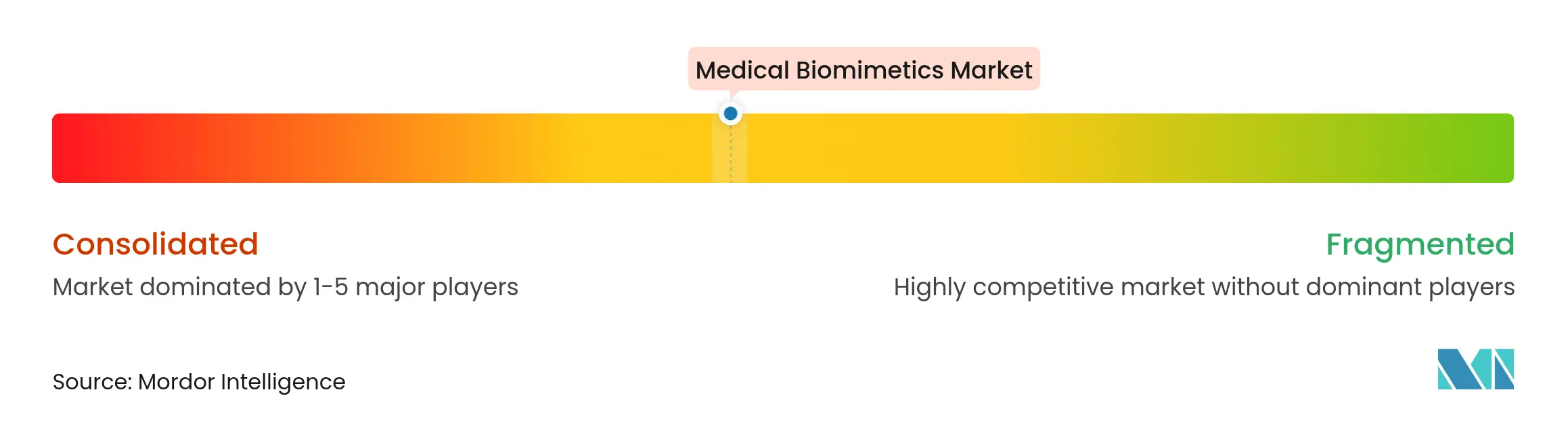

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Medical Biomimetics Market Analysis by Mordor Intelligence

The medical biomimetics market size in 2026 is estimated at USD 60.01 billion, growing from 2025 value of USD 55.86 billion with 2031 projections showing USD 85.94 billion, growing at 7.44% CAGR over 2026-2031. Growth is supported by rising demand for organ-replacement alternatives as U.S. transplant waiting lists exceed 100,000 patients, which expands the clinical need for engineered constructs that bypass donor dependence. Advances in nanoscale manufacturing are improving replication of extracellular matrix features, which increases integration and durability in vivo. Regulatory modernization that enables greater use of non-animal methods, including organ-on-chip, strengthens preclinical workflows and reduces development risk. As health systems prioritize curative solutions over palliative care, biomimetic scaffolds and devices that restore function gain traction across high-burden conditions in the Medical biomimetics market.

Key Report Takeaways

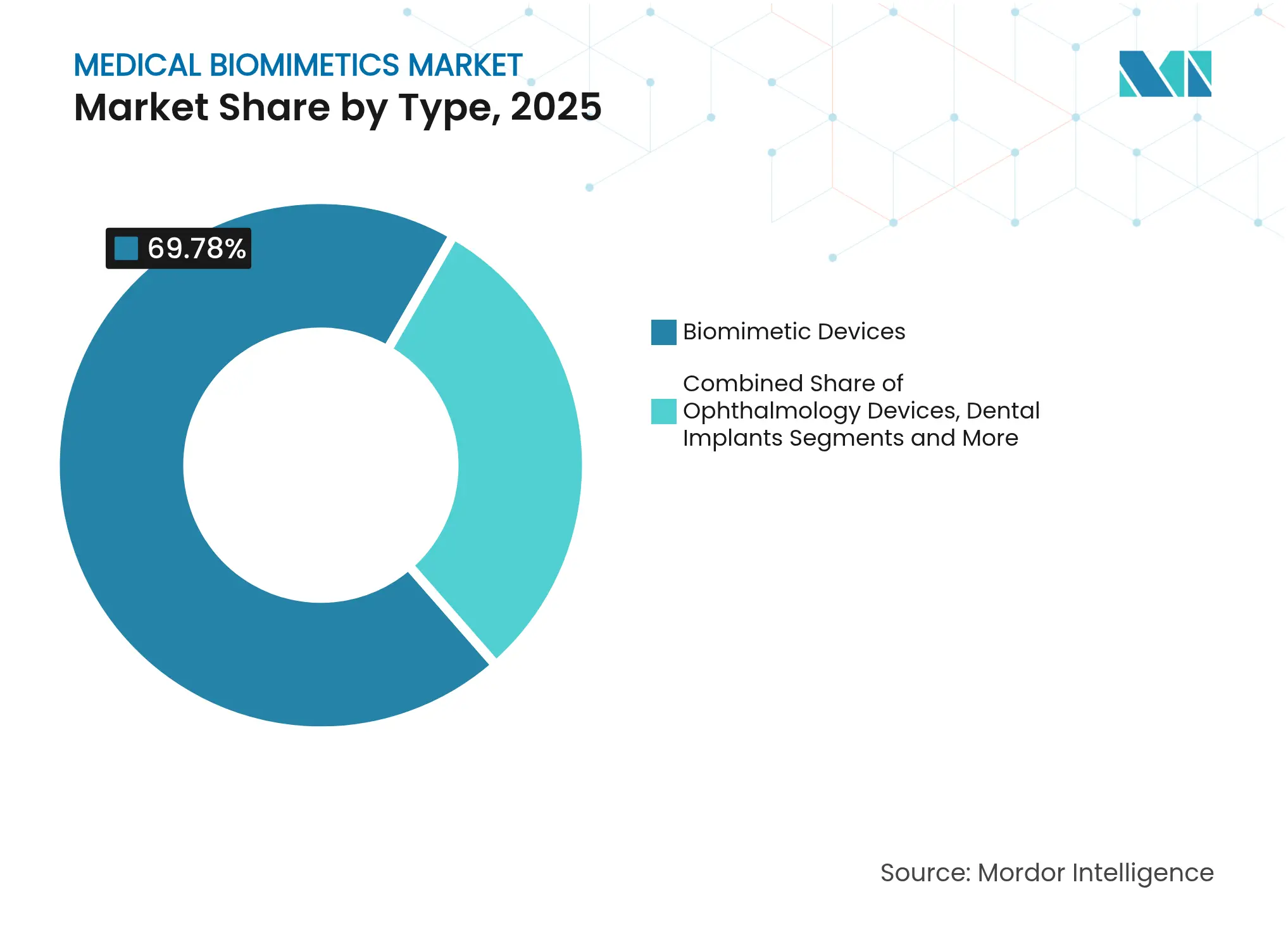

- By type, biomimetic devices led with 69.78% of the Medical biomimetics market share in 2025. Biomimetic Systems is the fastest growing at a 9.41% CAGR through 2031.

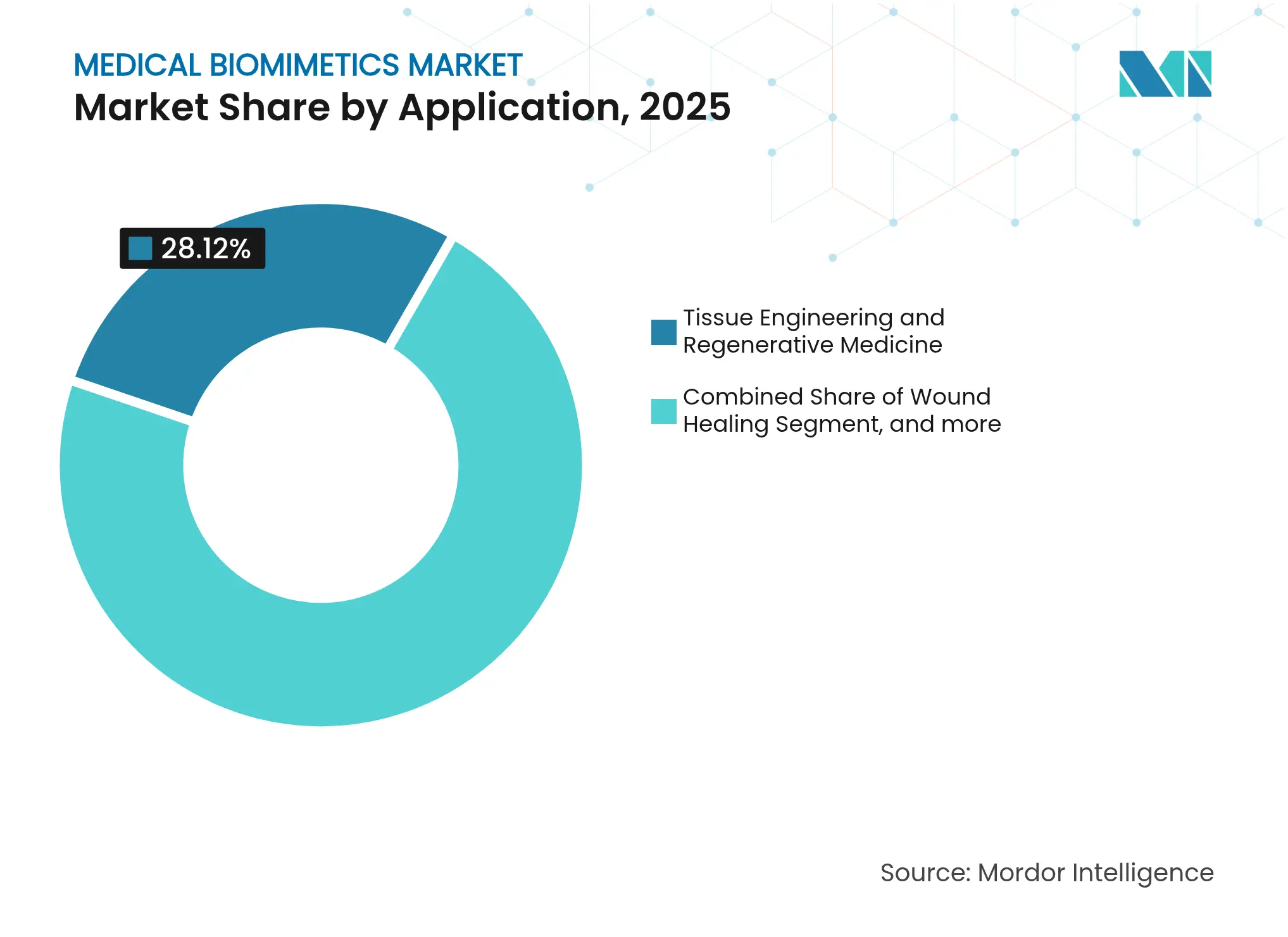

- By application, tissue engineering & regenerative medicine accounted for a 28.12% share of the Medical biomimetics market size in 2025. Neurology & Sensorimotor recorded the highest projected CAGR at 9.52% through 2031.

- By end user, hospitals captured 51.72% of the Medical biomimetics market share in 2025. Research & Academic Institutes is the fastest growing at a 10.24% CAGR through 2031.

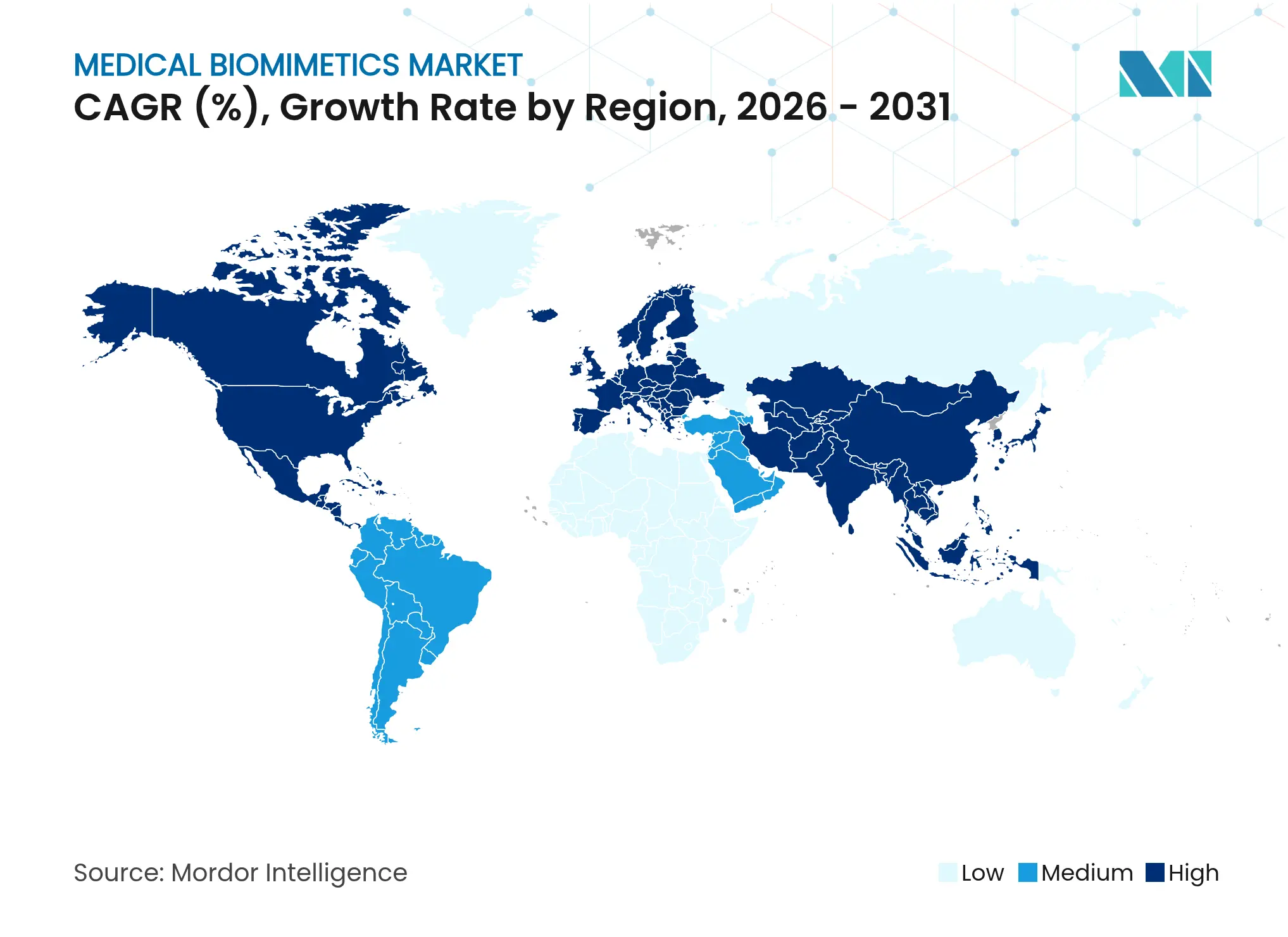

- By geography, North America held 43.85% share in 2025. The Asia-Pacific region is the fastest-expanding region, growing at an 8.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Biomimetics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand for tissue engineering and regenerative medicine Rising demand for tissue engineering and regenerative medicine | +1.8% | Global, with concentrated activity in North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global, with concentrated activity in North America & Europe | Impact Timeline:Medium term (2-4 years) |

Increasing prevalence of chronic diseases and degenerative conditions Increasing prevalence of chronic diseases and degenerative conditions | +1.5% | Global, acute pressure in Asia-Pacific due to aging demographics | Long term (≥ 4 years) | |||

Advancements in nanotechnology and biomimetic materials Advancements in nanotechnology and biomimetic materials | +1.2% | North America & Europe for innovation; Asia-Pacific for manufacturing scale | Short term (≤ 2 years) | |||

Growing applications in orthopedic, cardiovascular, and dental segments Growing applications in orthopedic, cardiovascular, and dental segments | +1.4% | North America, Europe, with spillover to Middle East medical tourism hubs | Medium term (2-4 years) | |||

Expansion of healthcare infrastructure in emerging economies Expansion of healthcare infrastructure in emerging economies | +1.0% | Asia-Pacific core, with expansion into Middle East & Africa | Long term (≥ 4 years) | |||

Increasing investments in biomimetic research and development Increasing investments in biomimetic research and development | +0.6% | Concentrated in North America, Europe, with emerging clusters in Singapore, South Korea | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Tissue Engineering and Regenerative Medicine

A persistent shortage of transplantable organs is accelerating adoption of engineered constructs, with U.S. kidney transplant wait times exceeding 1,800 days in 2024 and fueling the search for biomimetic alternatives that can be produced on demand[1]Organ Procurement and Transplantation Network, “Data Reports on Organ Waiting Times,” optn.transplant.hrsa.gov. Bioprinting now produces vascularized tissue patches at production costs near USD 15,000 per unit, which compares favorably to the lifetime cost of immunosuppression after traditional transplant. Academic centers such as Cleveland Clinic and Johns Hopkins expanded tissue engineering capacity by 40% in 2024 and have codified protocols for implanting lab-grown cartilage, dermal matrices, and vascular grafts that report 85% patency at 24 months. The FDA’s Regenerative Medicine Advanced Therapy program granted 28 biomimetic tissue products priority review status in 2024, which shortens approval timelines and increases patient access. These developments strengthen clinical readiness and move specific therapies from investigational to standard of care in limited indications, particularly for pediatric populations that benefit from growth-adaptive devices in the Medical biomimetics market.

Increasing Prevalence of Chronic Diseases and Degenerative Conditions

WHO estimates 620 million people live with cardiovascular disease in 2024, while diabetic complications in the United States drive 180,000 lower-limb amputations each year, which anchors long-run demand for vascular stents and nerve guidance conduits with biomimetic design[2]World Health Organization, “Cardiovascular Diseases: Key Facts 2024,” who.int. Osteoarthritis cases surpass 500 million globally, concentrated in populations above 65 years of age, with the 65-plus cohort expanding by 3.2% annually in Asia-Pacific. Hydroxyapatite nanocrystal bone grafts that mirror natural mineral composition have reported 30% faster osseointegration versus conventional titanium implants in published research. Neurodegenerative conditions, including Parkinson’s and Alzheimer’s, affect an estimated 55 million individuals worldwide, and biomimetic neural interfaces are in ongoing clinical evaluations for precise neuromodulation. As payers and providers weigh long-term outcomes against recurring treatment costs, restorative approaches tend to align with value-based care, which adds tailwinds for the Medical biomimetics market.

Advancements in Nanotechnology and Biomimetic Materials

Nanofabrication now enables biomaterial surfaces with features near 10-nanometer resolution that mirror extracellular matrix cues, which in turn directs cell behavior and reduces immune activation. Graphene-based constructs combine tensile strength exceeding 130 gigapascals with pore architectures that maintain nutrient diffusion, addressing durability and integration together in load-bearing uses. Electrospinning methods deliver fibers between 50 and 500 nanometers, which match collagen fibril dimensions and encourage aligned tissue regeneration rather than scar formation. Universities including MIT and ETH Zurich established nanobiomaterials laboratories in 2024 and partnered with device makers to scale GMP production toward 10,000-unit batches with less than 5% variability, which is important for regulatory acceptance. These advances allow the Medical biomimetics market to extend into spinal fixation, orthopedic reconstruction, and cardiac valves where legacy synthetics have shown durability limits.

Growing Applications in Orthopedic, Cardiovascular, and Dental Segments

Orthopedic procedures exceed 7 million joint replacements annually across developed markets, and biomimetic coatings that release bone morphogenetic proteins in controlled profiles have reduced implant loosening rates from 12% to under 4% at ten-year follow up in longitudinal cohorts. In cardiology, bioresorbable stents provide temporary mechanical support and then degrade into inert byproducts, which mitigates late thrombosis documented at 2% to 3% among recipients of permanent metal stents. Dental restoration now adopts biomimetic resin composites tuned to enamel’s elastic modulus, which distributes occlusal forces more evenly and reduces microcracking relative to conventional ceramics in selected cases. Sports medicine protocols in elite leagues incorporate rapid-deployment biomimetic patches to accelerate ligament healing, with recovery timelines for ACL reconstruction now reported at near 5 months in selected programs versus 9 months historically. Residency curricula across major medical centers include these techniques, which increases surgeon familiarity and improves diffusion across the Medical biomimetics market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent Multi-Region Regulatory Approvals Stringent Multi-Region Regulatory Approvals | -1.40% | Global, particularly severe in EU under MDR | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.40% | Geographic Relevance:Global, particularly severe in EU under MDR | Impact Timeline:Short term (≤ 2 years) |

High Production And Customization Costs High Production And Customization Costs | -0.90% | Global, affecting SMEs disproportionately | Medium term (2-4 years) | |||

Nanotoxicity And Long-Term Safety Unknowns Nanotoxicity And Long-Term Safety Unknowns | -0.60% | Global, with stricter oversight in North America & EU | Long term (≥ 4 years) | |||

Limited Reimbursement Frameworks For Novel Implants Limited Reimbursement Frameworks For Novel Implants | -0.80% | North America & EU primarily, expanding globally | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Biomimetic Devices and Materials

Premium pricing remains a key barrier, with bioresorbable cardiovascular scaffolds priced at USD 5,000 to USD 8,000 against USD 2,000 for metallic stents in major markets, which translates into 150% to 300% price differentials[3]U.S. Food and Drug Administration, “Premarket Approval (PMA) and Device Classifications,” fda.gov. Manufacturing costs are elevated by clean-room operations, multi-stage surface modification, and rigorous testing that can account for 40% to 50% of final device cost, which limits scale-driven price compression. Public procurement in lower-income regions emphasizes high-volume, low-cost devices to expand access, which reduces the formulary presence of advanced biomimetics in public hospitals. Out-of-pocket spending for noncovered procedures can exceed USD 20,000 in certain indications, which narrows addressable demand to higher-income patients in developing regions. Health technology agencies such as NICE and IQWiG demand robust cost-effectiveness and measurable QALY gains before coverage, which is difficult to demonstrate when mortality risk is low despite strong quality-of-life benefits.

Stringent Regulatory Approvals and Safety Requirements

Class III biomimetic devices under FDA PMA require full biocompatibility across ten ISO 10993 standards, long-term degradation studies, and 200 to 500-patient trials, which often translates to 5 to 7 years and USD 50 million to USD 100 million prior to launch. Novel nanostructured materials face additional cytotoxicity and inflammatory response evaluations that extend timelines by 18 to 24 months versus established materials, which raises development risk and cost. Global commercialization requires separate approvals through EU MDR, Japan’s PMDA, and China’s NMPA with unique data, labeling, and quality system expectations that fragment resources. Post-market surveillance and periodic recertification sustain compliance costs, and real-world safety signals can trigger restrictions or withdrawal of approvals. ISO 13485 and GMP compliance require facilities, documentation systems, and trained personnel, which favors established firms in the Medical biomimetics market over startups.

Segment Analysis

By Type: Devices Lead but Systems Accelerate Fastest

Biomimetic Devices accounted for 69.78% of the Medical biomimetics market size in 2025, reflecting the momentum of cochlear implants, drug-eluting stents, and joint prostheses that mirror natural function and benefit from mature regulatory pathways. Regulatory familiarity and established reimbursement continue to support procedure volumes for device categories where clinical evidence is deep and post-market risk is well characterized. Systems-based platforms are scaling as organ-on-chip models win acceptance in preclinical research, with uptake reinforced by FDA modernization that permits greater use of new approach methodologies. Materials provide the foundation for both devices and systems through hydroxyapatite grafts, collagen scaffolds, and bioactive glass that translate nanostructural insights into clinical-grade products. The Medical biomimetics market benefits from a portfolio mix where devices deliver near-term revenue while systems expand the total addressable opportunity for drug development partners.

Biomimetic Systems is the fastest growing type with a 9.41% CAGR through 2031 because pharmaceutical developers value human-relevant microenvironments that improve toxicology prediction and lower late-stage failures. University-origin platforms move to market through licensing and codevelopment models, which avoid large capital outlays and let academic teams focus on novel functions. Regulatory expectations extend traditional quality controls to include software validation where systems incorporate data capture and analytics, with the FDA’s Computer Software Assurance guidance informing practice. Materials remain differentiated by their ability to replicate ECM structure and bioactivity while meeting GMP requirements for lot consistency. Together, the type segmentation reflects a Medical biomimetics industry progression that pairs robust near-term device cash flows with high-growth system platforms that broaden use cases for sponsors and contract research partners.

Note: Segment shares of all individual segments available upon report purchase

By Application: Regenerative Medicine Dominates with Neurological Applications Surging

Tissue Engineering & Regenerative Medicine commanded a 28.12% share of the Medical biomimetics market size in 2025 because burn care, joint preservation, and vascular bypass procedures have clear indications and durable clinical endpoints. Payers read value in procedures that restore function and reduce long-term care costs, which supports steady adoption where follow-up data demonstrate durable outcomes. Cardiovascular repair continues to contribute significant volume through bioresorbable stents and valve replacements that aim to remove long-term foreign body burden. Dental restoration and sports medicine add a mix of high-volume and premium niches, with aesthetic outcomes and faster recovery shaping demand in private-pay settings. Wound healing and reconstructive uses broaden clinical exposure for engineered scaffolds and matrices across trauma centers and specialized surgical units in the Medical biomimetics market.

Neurology & Sensorimotor is the fastest growing application at a 9.52% CAGR through 2031 because brain-computer interfaces and advanced neural prostheses are moving from research to controlled clinical deployment with improved signal fidelity. Assistive communication and motor control capabilities for stroke and spinal cord injury patients demonstrate tangible gains in independence that translate to payer interest. Ophthalmology and corneal implants show promise where donor tissue access is limited and biocompatibility is the primary barrier. Plastic and reconstructive surgery ties adoption to trauma and oncology follow-up volumes, which vary by center and region. As clinical training diffuses, more specialties incorporate biomimetic approaches, which widens the application mix across the Medical biomimetics market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals Lead but Academic Institutes Accelerate

Hospitals captured 51.72% share in 2025 because complex biomimetic implant procedures require operating rooms, intensive care, and multidisciplinary teams that are not available in most ambulatory settings. Tertiary and quaternary care centers also house tissue processing facilities and maintain quality systems for surgical implants, which concentrates advanced procedures where safety oversight is strong. Specialty clinics and ambulatory centers grow into indications suited to lower risk and shorter recovery, including dental restoration and select orthopedic interventions. As care pathways standardize, procedures often migrate from hospitals to ambulatory settings to reduce cost and increase throughput without compromising outcomes. These shifts shape a Medical biomimetics market delivery mix that matches procedure complexity with the appropriate site of care across health systems.

Research & Academic Institutes is the fastest growing end-user group at a 10.24% CAGR through 2031, reflecting the dual role as innovation hubs and early clinical users that support first-in-human studies. Universities are investing in translation infrastructure and partnering with startups and device manufacturers, which speeds movement from lab to clinic. Institutional Review Boards and research coordinators enable investigational device trials that generate publishable evidence and build the base for regulatory submissions. As academic centers validate efficacy and safety, adoption spreads to community hospitals and specialty clinics that follow established protocols. This progression supports a Medical biomimetics market where knowledge transfer and training lower barriers to broader deployment.

Geography Analysis

North America held 43.85% share in 2025, supported by strong device manufacturing clusters in Massachusetts, California, and Minnesota, integrated supplier ecosystems, and robust reimbursement for approved biomimetic therapies. NIH funding for biomedical research exceeds USD 40 billion annually and includes programs dedicated to tissue engineering and regenerative medicine that advance academic-industry collaboration. FDA policies for expedited review of breakthrough devices and RMAT designations streamline approval for innovative biomimetics with strong clinical rationale. Health plans align coverage to FDA labeling and clinical guidelines, which gives manufacturers line of sight to revenue and supports investment in clinical and manufacturing capacity. This environment continues to shape the Medical biomimetics market size trajectory for companies that prioritize rigorous evidence and quality systems.

Europe retains significant share through its established medical technology base in Germany, Switzerland, and Ireland, with the Medical Device Regulation framework intended to strengthen product quality and post-market surveillance despite near-term certification bottlenecks. The region benefits from clinical research centers with deep surgical expertise in orthopedics, cardiovascular intervention, and neuroscience that are central to biomimetic adoption. Asia-Pacific is the fastest growing region at an 8.31% CAGR through 2031 as China and India expand hospital infrastructure, Japan maintains expedited pathways for novel devices through Sakigake designation, and regional manufacturing reduces costs. Healthy China 2030 and Ayushman Bharat add volume through public funding and benefit designs that include procedures using biomimetic technologies. These forces create a Medical biomimetics market that is increasingly diversified by geography, regulatory approach, and price points.

Middle East and Africa show concentrated momentum in Gulf Cooperation Council countries where government health investments exceed USD 60 billion annually and where medical tourism destinations offer advanced biomimetic procedures at competitive prices. Sub-Saharan Africa faces constraints tied to limited infrastructure and low per-capita health expenditure under USD 100 in many markets, which narrows near-term adoption prospects. South America has moderate growth led by Brazil’s SUS coverage expansion and Colombia’s medical tourism presence in dental and cosmetic procedures that use biomimetic materials. Regulators such as Health Canada, Australia’s TGA, and Swissmedic uphold review rigor similar to FDA and EMA, while India and Brazil apply risk-based frameworks that streamline lower-risk biomimetic materials and devices. These differences influence time to market and evidence strategies that companies adopt across the Medical biomimetics market.

Competitive Landscape

Market Concentration

The medical biomimetics market shows moderate consolidation as the top 10 companies hold about 45% combined share while more than 200 smaller firms and university spin-outs address niche needs such as custom bone grafts, neural interfaces, and targeted tissue scaffolds. Larger device makers pursue acquisition and partnership strategies to secure biomimetic IP and clinical capabilities that fit established commercial channels. Portfolio strategies balance incremental biomimetic enhancements of existing systems with platform bets such as organ-on-chip that expand into drug development services. The competitive field rewards companies that combine material science depth, clinical trial execution, and manufacturing discipline in regulated environments. These capabilities reinforce a Medical biomimetics market where evidence, quality, and scale shape durable advantage.

White-space opportunities are visible in pediatrics where growth-adaptive implants could reduce revision surgeries and improve long-term outcomes and costs. University spin-outs are advancing bioprinting that uses autologous cells to reduce immunogenic risk and align with personalized medicine goals. Partnerships with pharmaceutical companies accelerate validation for organ-chip testing as drug developers seek more predictive models before first-in-human trials. Contract research and manufacturing partners with GMP capacity help early-stage companies bridge the scale-up gap to meet regulatory and commercial requirements. These dynamics support a Medical biomimetics market that integrates device, diagnostics, and preclinical services into a broader health technology value chain.

Standard-setting efforts remain important as ISO Technical Committee 150 refines test methods for implants that increasingly use biomimetic coatings and scaffolds. Recent strategic moves by leading companies show continued investment, including facility expansions for orthopedic coatings, bioresorbable stent approvals, and organ-chip center buildouts that consolidate R&D and preclinical testing. Partnerships for growth factor-enabled bone grafts and acquisitions in cardiac reconstruction technologies indicate portfolio shaping around high-burden procedures with clear endpoints. This pattern is consistent with a Medical biomimetics market where clinical evidence depth and manufacturing readiness are decisive for scale.

Medical Biomimetics Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Abbott received FDA approval for the Tendyne transcatheter mitral valve replacement system, the first device enabling mitral valve replacement without open-heart surgery. This system addresses patients with severe mitral annular calcification who are not surgical candidates.

- May 2025: Zimmer Biomet reported Q1 2025 revenue growth of 1.1%, driven by innovations in hip and knee product lines, including the Z1 Triple-Taper Femoral Hip System and Oxford Cementless Partial Knee, with updated guidance reflecting the Paragon 28 acquisition impact

- April 2025: Abbott initiated the ASCEND CSP pivotal clinical trial for its investigational Conduction System Pacing ICD lead, following successful first-in-world leadless left bundle branch area pacing procedures that received FDA Breakthrough Device Designation.

- March 2025: Abbott announced two-year TRILUMINATE Pivotal trial data showing that the TriClip transcatheter edge-to-edge repair system reduced heart failure hospitalizations by 27% and that 84% of patients reached moderate or less tricuspid regurgitation grade.

Table of Contents for Medical Biomimetics Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Demand for Tissue Engineering and Regenerative Medicine

- 4.2.2Increasing Prevalence of Chronic Diseases and Degenerative Conditions

- 4.2.3Advancements in Nanotechnology and Biomimetic Materials

- 4.2.4Growing Applications in Orthopedic, Cardiovascular, and Dental Segments

- 4.2.5Expansion of Healthcare Infrastructure in Emerging Economies

- 4.2.6Increasing Investments in Biomimetic Research and Development

- 4.3Market Restraints

- 4.3.1High Cost of Biomimetic Devices and Materials

- 4.3.2Stringent Regulatory Approvals and Safety Requirements

- 4.3.3Limited Awareness and Adoption in Developing Regions

- 4.3.4Technical Complexities in Mass Production and Commercialization

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Type

- 5.1.1Biomimetic Materials

- 5.1.2Biomimetic Systems

- 5.1.3Biomimetic Devices

- 5.2By Application

- 5.2.1Plastic & Reconstructive Surgery

- 5.2.2Wound Healing

- 5.2.3Tissue Engineering & Regenerative Medicine

- 5.2.4Orthopedic & Sports Medicine

- 5.2.5Cardiovascular Repair

- 5.2.6Dental Restoration

- 5.2.7Neurology & Sensorimotor

- 5.2.8Ophthalmology & Vision Restoration

- 5.3By End User

- 5.3.1Hospitals

- 5.3.2Specialty Clinics

- 5.3.3Ambulatory Surgical Centers

- 5.3.4Research & Academic Institutes

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Abbott

- 6.3.2AVINENT Science & Technology

- 6.3.3BioHorizons

- 6.3.4Boston Scientific

- 6.3.5CeramTec

- 6.3.6CorNeat Vision

- 6.3.7Curasan Inc.

- 6.3.8Dentsply Sirona

- 6.3.9Johnson & Johnson (DePuy Synthes)

- 6.3.10Keystone Dental Group

- 6.3.11Medtronic

- 6.3.12Organogenesis Holdings

- 6.3.13Osteopore Ltd.

- 6.3.14Smith & Nephew

- 6.3.15Stryker Corporation

- 6.3.16SynTouch Inc.

- 6.3.17TISSIUM

- 6.3.18Veryan Medical

- 6.3.19Xeltis

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Medical Biomimetics Market Report Scope

As per the scope, medical biomimetics refers to the application of biological principles and natural models to develop medical technologies. It involves designing materials, devices, and systems that imitate the structure and function of living organisms.

The Biomimetic Medical Devices Market is Segmented by Product Type (Orthopedic Implants, Ophthalmology Devices, and More), Application (Plastic & Reconstructive Surgery, Wound Healing, and More), Material Type (Metallic Biomimetics, Polymeric, and More), End User (Hospitals, Specialty Clinics, and More), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.