Pet Service Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 32.13 Billion |

| Market Size (2031) | USD 47.61 Billion |

| Growth Rate (2026 - 2031) | 8.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pet Service Market Analysis by Mordor Intelligence

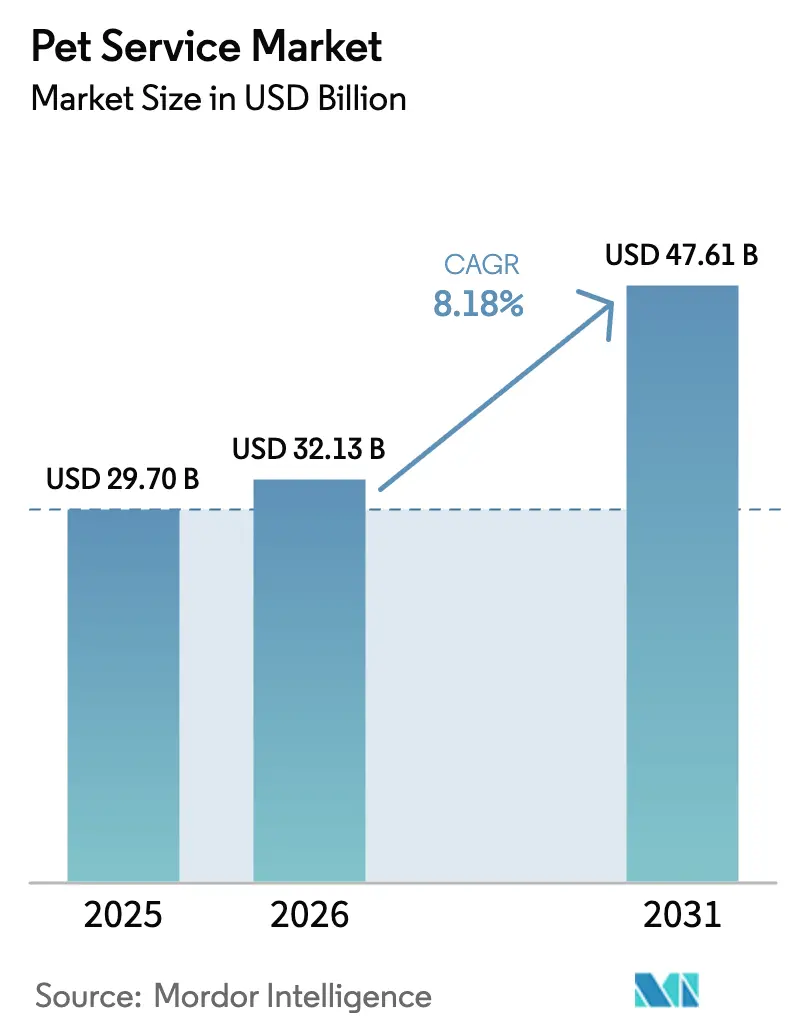

The pet service market size in 2026 is estimated at USD 32.13 billion, growing from 2025 value of USD 29.7 billion with 2031 projections showing USD 47.61 billion, growing at 8.18% CAGR over 2026-2031. The trajectory is propelled by owners who increasingly treat companion animals as family, sustained venture-capital inflows, and software-driven efficiencies that compress scheduling and logistics costs. Recurring-revenue models, notably subscriptions that bundle wellness, grooming, and walking services, foster predictable cash flow and deepen customer loyalty. Digital booking platforms amplify capacity utilization, while mobile vans and in-home offerings satisfy time-pressed urban professionals. Mobile service adoption accelerated approximately 30% in 2025, driven by AI-powered scheduling platforms and consumer preference for in-home convenience. Consolidation is accelerating as private-equity sponsors deploy scale economics to offset wage inflation and compliance overhead.

Key Report Takeaways

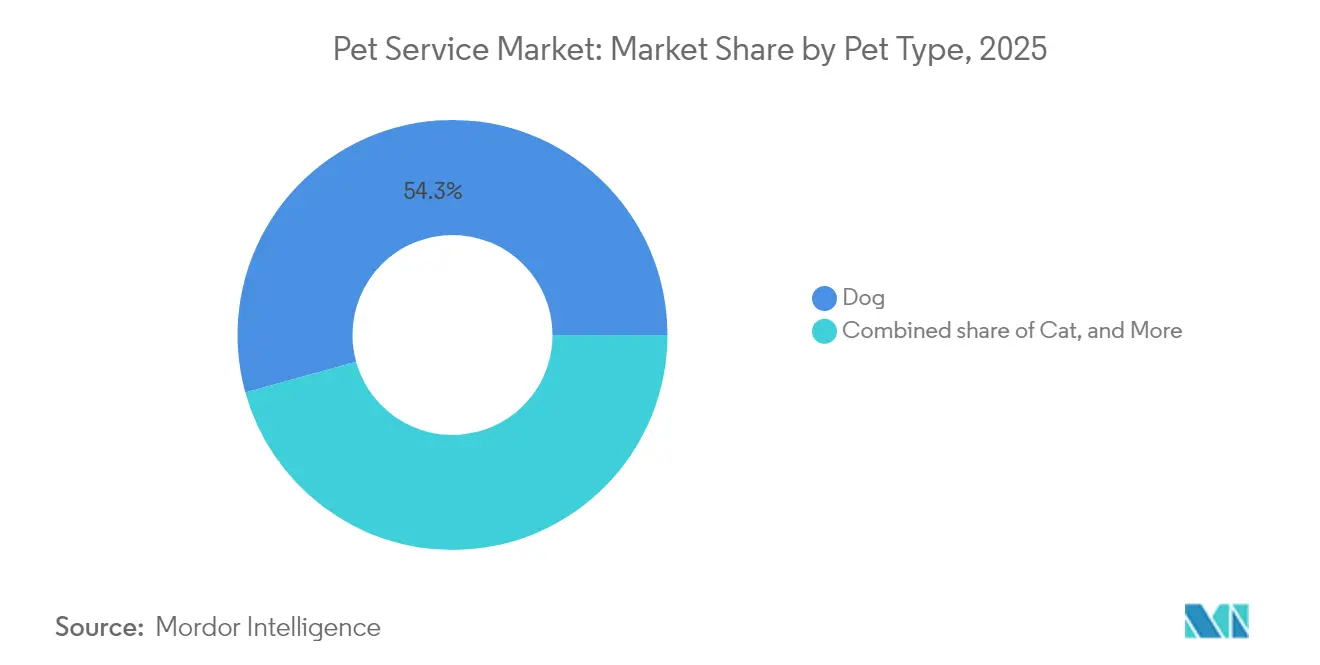

- By pet type, dogs accounted for 54.30% of the pet service market share in 2025, while cat services are projected to grow at a 7.18% CAGR to 2031.

- By service type, grooming led with a 37.90% of the pet service market size in 2025, whereas walking is forecast to expand at a 9.24% CAGR through 2031.

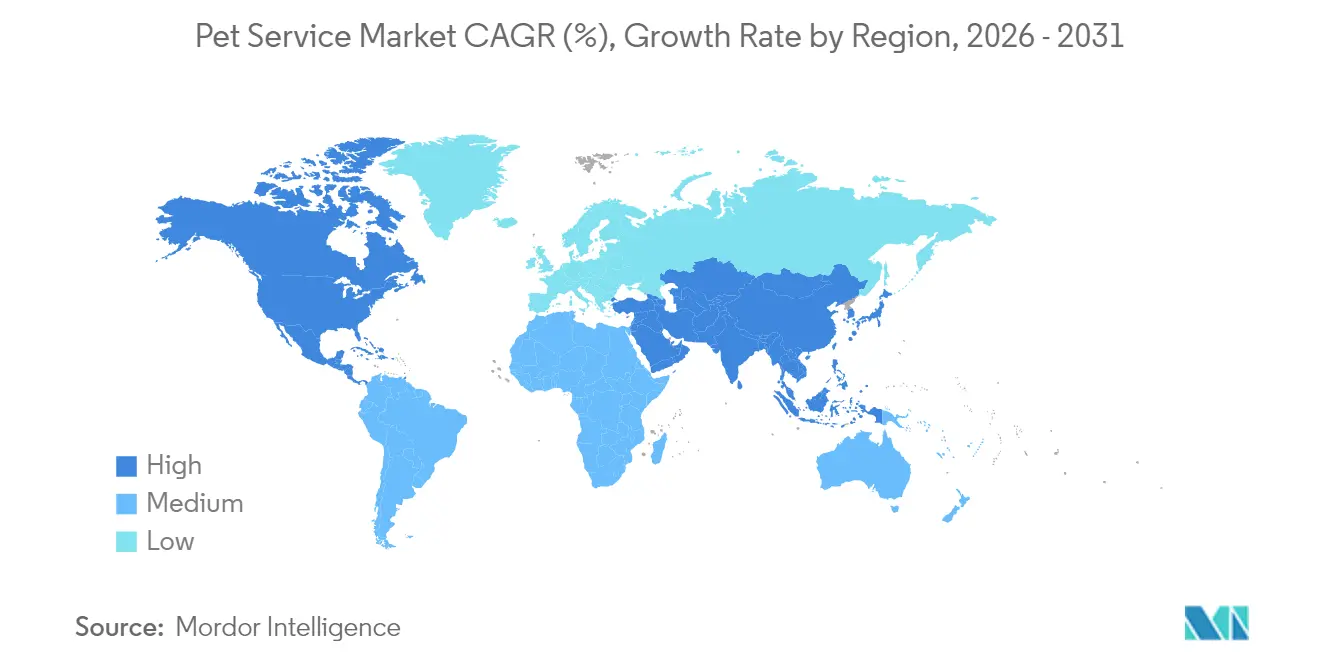

- By geography, North America commanded 38.30% of revenue in 2025. Asia-Pacific is advancing at a 7.74% CAGR and is the fastest-growing region to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trend of Pet Humanization and Premiumization | +1.8% | Global, with the strongest impact in North America and Europe | Long term (≥ 4 years) |

| Growth of Mobile and In-Home Service Models | +1.5% | North America and the Asia-Pacific core, expanding to Europe | Medium term (2-4 years) |

| Rise in Pet Health-Insurance Utilization | +1.2% | North America and Europe, and emerging in the Asia-Pacific | Medium term (2-4 years) |

| AI-Enabled Service Personalization and Scheduling | +0.9% | Global, led by North America, and developed the Asia-Pacific markets | Short term (≤ 2 years) |

| Subscription-Based Pet-Wellness Bundles | +0.8% | North America and Europe, pilot programs in the Asia-Pacific | Medium term (2-4 years) |

| Venture-Capital Funding Spurring Capacity Expansion | +0.7% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Trend of Pet Humanization and Premiumization

Seventy-one percent of owners now describe pets as family members, elevating expectations for salon-quality grooming and hotel-style boarding services[1]Source: Consumer Technology Association, “The Rapid Growth of Pet Tech,” CTA, cta.tech. Luxury facilities feature live-stream video for owners, organic shampoos, and climate-controlled suites that echo human hospitality standards. Behavioral training, senior-pet wellness plans, and allergy-friendly spa packages have become routine offerings rather than niche add-ons. Retail-as-a-service shelves inside salons recommend breed-specific nutrition or dermatology products, converting trust into ancillary revenue. Providers with specialist credentials gain pricing power, sidestepping commodity pricing pressures that encumber basic-care operators.

Growth of Mobile and In-Home Service Models

Demand for door-to-door grooming, walking, and vet-teletriage climbed about 30% in 2025, enabled by route-optimization apps and cashless checkout. Purpose-built vans deliver professional equipment curbside, eliminating rent while capturing a convenience premium. The model eases pet stress by avoiding unfamiliar settings and appeals to apartment dwellers with limited transport options. Technology platforms like MoeGo, SuperSaaS, and Time To Pet facilitate seamless booking and route optimization, making mobile operations scalable for multi-vehicle fleets. This shift particularly benefits working professionals who value time savings and pets who experience reduced stress from familiar environment care.

Rise in Pet Health-Insurance Utilization

Pet insurance adoption accelerates service utilization as coverage reduces cost barriers for preventive care and specialized treatments, creating downstream demand for complementary services. Petco's partnership with Nationwide Insurance exemplifies how service providers integrate insurance offerings to reduce customer acquisition costs while increasing lifetime value through covered service utilization. The insurance trend enables more frequent grooming visits, behavioral training sessions, and wellness check-ups as owners face reduced out-of-pocket expenses. Digital-first platforms like Pawp expand access through employer benefit programs, making pet healthcare more accessible to younger demographics who drive service innovation adoption.

AI-Enabled Service Personalization and Scheduling

Artificial intelligence revolutionizes operational efficiency through personalized service recommendations and automated scheduling systems that optimize resource utilization across service categories. Platforms like My AI Front Desk, Cuddles, and PetExec demonstrate widespread AI adoption for customer interaction management and appointment optimization, reducing administrative overhead while improving customer experience. AI-powered grooming tools enable precision styling based on breed-specific requirements and individual pet preferences, creating differentiated service quality that commands premium pricing. The technology facilitates predictive maintenance scheduling for equipment and inventory management, reducing operational disruptions that impact customer satisfaction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Wage and Real-Estate Costs | -1.4% | Global, most severe in North America and Europe | Short term (≤ 2 years) |

| Regulatory Hurdles for Cross-Border Pet Transport | -0.8% | Global, particularly Europe and Asia-Pacific routes | Medium term (2-4 years) |

| Shortage of Skilled Groomers and Care Professionals | -1.1% | North America and Europe, and emerging in the Asia-Pacific | Long term (≥ 4 years) |

| Allergy and Zoonotic-Disease Concerns Among Consumers | -0.6% | Global, heightened awareness in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Wage and Real-Estate Costs

Groomer salaries exceed USD 2,000-5,000 monthly, while certification programs add USD 6,630-8,800 in entry barriers, curbing talent pipelines [2]Source: California Veterinary Medical Board, “2025 Citations and Disciplinary Actions,” vmb.ca.gov. Prime storefront rents climb faster than service prices, squeezing single-location owners. Some operators pivot to suburban warehouses, and others downsize into mobile fleets that trade rent for vehicle financing. Subscriptions hedge against margin compression by locking in recurring revenue that smooths payroll spikes. Mobile service models emerge as partial solutions by eliminating fixed real estate costs, though vehicle acquisition and maintenance create alternative capital requirements. Service providers increasingly adopt subscription pricing models to improve cash flow predictability and offset rising operational expenses through recurring revenue streams.

Shortage of Skilled Groomers and Care Professionals

Training capacity lags behind demand, and apprenticeships are unable to scale quickly enough to replace retiring professionals. Instances of unlicensed practice highlight the presence of underground operators who lower prices but diminish consumer trust. Premium salons attract graduates with signing bonuses and continued-education incentives. Employee turnover remains significant. While AI can optimize basic tasks, intricate breed styling continues to rely on human expertise. Service providers are addressing these challenges through apprenticeship programs and the adoption of technology to enhance worker efficiency, though human expertise remains essential for complex grooming and behavioral services.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Dogs Hold Scale, Cats Accelerate

Dogs delivered 54.30% of the pet service market share in 2025, reflecting higher visit frequency for walking, daycare, and grooming. Owner's willingness to purchase GPS-tracked adventures and social-play packages sustains volume. The pet service market size for dogs is poised to advance in lockstep with premium health offerings such as hydrotherapy pools and orthopedic daycare sessions. The cat segment is projected to grow at a CAGR of 7.18% through 2031, driven by urban pet owners seeking nutritional services, grooming for stress management, and automated litter box systems. Rising disposable income elevates feline services from occasional to scheduled visits, pushing the pet service market share for cats upward in multi-pet households.

Technology adoption diverges. Canine platforms emphasize route tracking, social media sharing, and wearable activity monitors that encourage add-on walks. Feline solutions favor health analytics from litter-box sensors and mood-scoring algorithms that signal stress triggers. Operators therefore zone facilities to separate aromas, acoustics, and lighting conducive to each species, earning premiums for species-specific expertise.

Note: Segment shares of all individual segments available upon report purchase

By Service Type: Grooming Dominates, Walking Surges

Grooming maintained 37.90% of 2025 revenue, positioning it as the anchor for cross-selling vaccines, dental cleanings, and retail shampoos. The segment’s recurring nature enhances customer lifetime value, keeping the pet service market size healthy despite rising wages. Walking, however, is on track for a 9.24% CAGR, driven by urban labor participation and remote work fatigue that leaves pets needing midday relief. Real-time GPS routes and push-notification report cards turn trust into retention, buoying subscription uptake. Hybrid operators pair grooming with walks in bundled plans, boosting occupancy across morning and afternoon slots.

AI trimmers that scan coat density deliver consistent finishes in half the time, freeing groomers for high-margin creative styling. Walk aggregator apps match certified walkers with neighborhood clusters, minimizing dead-heading miles. The economics incentivize multi-service providers to leverage a single Customer Relationship Management for cross-promotions and loyalty rewards.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America commanded 38.30% of the revenue in 2025, reflecting mature pet ownership and disposable incomes that can afford premium monthly plans. Subscription penetration exceeds 25% of customers, providing a stable cash flow for expansion through targeted acquisitions. Venture capital funding is directed toward AI software that automates check-ins and dynamic pricing. Regulatory oversight from agencies like the USDA emphasizes quality differentiation, with audited compliance serving as a key marketing factor.

Asia-Pacific posts the fastest 7.74% CAGR as rising wages and smaller household sizes spur companion-animal adoption. Megacities adopt mobile-van formats that circumvent high rents and traffic congestion. Governments in China and Hong Kong revise import protocols, acknowledging economic upside while requiring stricter welfare standards. Owners in Tokyo, Seoul, and Singapore are embracing tech-centric experiences, from robotic treat dispensers to on-demand cat grooming subscriptions.

Europe sustains steady growth in line with household income, anchored by robust welfare regulations that certify facilities and limit overcrowding. Operators differentiate themselves through ethical sourcing and eco-friendly products to resonate with consumers' sustainability priorities. Cross-border transport compliance remains complex, favoring multinational consolidators with in-house legal teams. Middle East and Africa are nascent yet promising, expatriate populations and urbanization seed demand for international-standard boarding and veterinary hybrid hubs that integrate grooming, training, and retail.

Competitive Landscape

The Pet Service Market exhibits extreme fragmentation with over 160,000 establishments, indicating vast headroom for roll-ups and tech-enabled disruptors. Private-equity firms target fragmented clusters, acquire single shops, and then integrate Point of Sale (POS) and procurement to extract scale economies. The USD 8.6 billion merger between Mission Veterinary Partners and Southern Veterinary Partners highlights the strong demand for stable, recession-resistant cash flow in the market. Strategic imperatives include subscription migration, AI workforce augmentation, and geographic adjacency plays that minimize marketing spend.

Mobile specialists attract funding by eliminating rent and widening service radii through vans fitted with solar power, wastewater containment, and hospital-grade sanitation. Brands such as TrustedHousesitters promote sharing-economy models that monetize idle household capacity for sitting and boarding [3]Source: TrustedHousesitters, "The freedom to travel, "trustedhousesitters.com. White-space niches in senior-pet wellness, allergy-friendly spas, and behavior modification garner premium pricing because the depth of skill deters commoditization. Regulatory compliance now shapes competitive moats, investment in documented care protocols shields against fines, and differentiates at the point of sale.

Supply-chain scrutiny intensifies as retailers distance themselves from breeders cited for welfare violations. Accordingly, vertically integrated players source directly from rescue partnerships, aligning brand values with consumer ethics. Subscription model innovators capture first-party data, which informs targeted upsells and improves churn prediction. Regulatory compliance capabilities increasingly differentiate operators as enforcement actions intensify across jurisdictions, creating barriers to entry for undercapitalized competitors while rewarding investment in professional standards and operational excellence.

Pet Service Industry Leaders

-

PetSmart Inc. (BC Partners LLP)

-

Wag! Group Co.

-

PetBacker Pte. Ltd.

-

Rover Group, Inc. (Blackstone Inc.)

-

Petco Health and Wellness Company, Inc. (CVC Capital Partners and CPPIB)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: General Mills bought Whitebridge Pet Brands for USD 1.45 billion, signaling CPG interest in downstream service ecosystems.

- September 2024: Mission Veterinary Partners and Southern Veterinary Partners outlined a merger covering more than 730 clinics at USD 8.6 billion, the sector’s largest consolidation to date.

- February 2024: Blackstone finalized its acquisition of Rover, affirming institutional conviction in tech-enabled pet-care marketplaces and establishing a valuation benchmark for future exits.

Global Pet Service Market Report Scope

Pet service is a component of the pet care market, which includes services exclusively meant for pet care activities, like pet grooming, pet walking, pet sitting, pet transportation, and pet boarding. These are the non-medical services that focus on pets. These services include bathing and grooming, pet sitting or boarding, obedience training, and pet health insurance.

The pet service market is segmented by pet type (dog, cat, and other animals), service type (grooming, pet transportation, pet boarding, pet sitting, pet walking, and other service types), and geography (North America, Europe, Asia-Pacific, South America, and Africa). The report offers the market size and forecasts regarding value in USD for all the above segments.

| Dog |

| Cat |

| Other Animals |

| Grooming |

| Pet Transportation |

| Pet Boarding |

| Pet Sitting |

| Pet Walking |

| Other Specialized Services |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Spain | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| Segmentation by Pet Type | Dog | |

| Cat | ||

| Other Animals | ||

| Segmentation by Service Type | Grooming | |

| Pet Transportation | ||

| Pet Boarding | ||

| Pet Sitting | ||

| Pet Walking | ||

| Other Specialized Services | ||

| Segmentation by Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the pet service market in 2026?

The pet service market size is USD 32.13 billion in 2026.

What is the projected growth rate through 2031?

The market is projected to expand at an 8.18% CAGR to 2031.

Which service category is growing the fastest?

Walking services are on pace for a 9.24% CAGR, the highest among all segments.

Which region is the fastest growing?

Asia-Pacific is advancing at a 7.74% CAGR through the forecast period.

How fragmented is competition?

No company controls more than 5% share; more than 160,000 establishments operate globally.

Why are investors drawn to pet services?

Recurring revenue, recession resilience, and consolidation upside make the sector attractive to private-equity capital.