Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.26 Billion |

| Market Size (2031) | USD 7.66 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cat Litter Market Analysis by Mordor Intelligence

The cat litter market size is projected to be USD 6.01 billion in 2025, USD 6.26 billion in 2026, and reach USD 7.66 billion by 2031, growing at a CAGR of 4.14% from 2026 to 2031. The cat litter market is expanding on the back of steady indoor cat ownership, which keeps purchase frequency stable across income cycles and retail formats. Premium litter formats with stronger odor control, lower dust, and added health-monitoring functions are lifting spending per purchase faster than unit growth. Apartment living is also supporting demand for cleaner, easier-to-manage litter systems that fit small homes and routine daily use. Competitive activity is shifting toward differentiated formulas, digital replenishment, and retailer-specific packs rather than simple price-led growth. Smart litter ecosystems are adding a new layer of recurring revenue because compatible consumables can create real switching costs in the cat litter market.

Key Report Takeaways

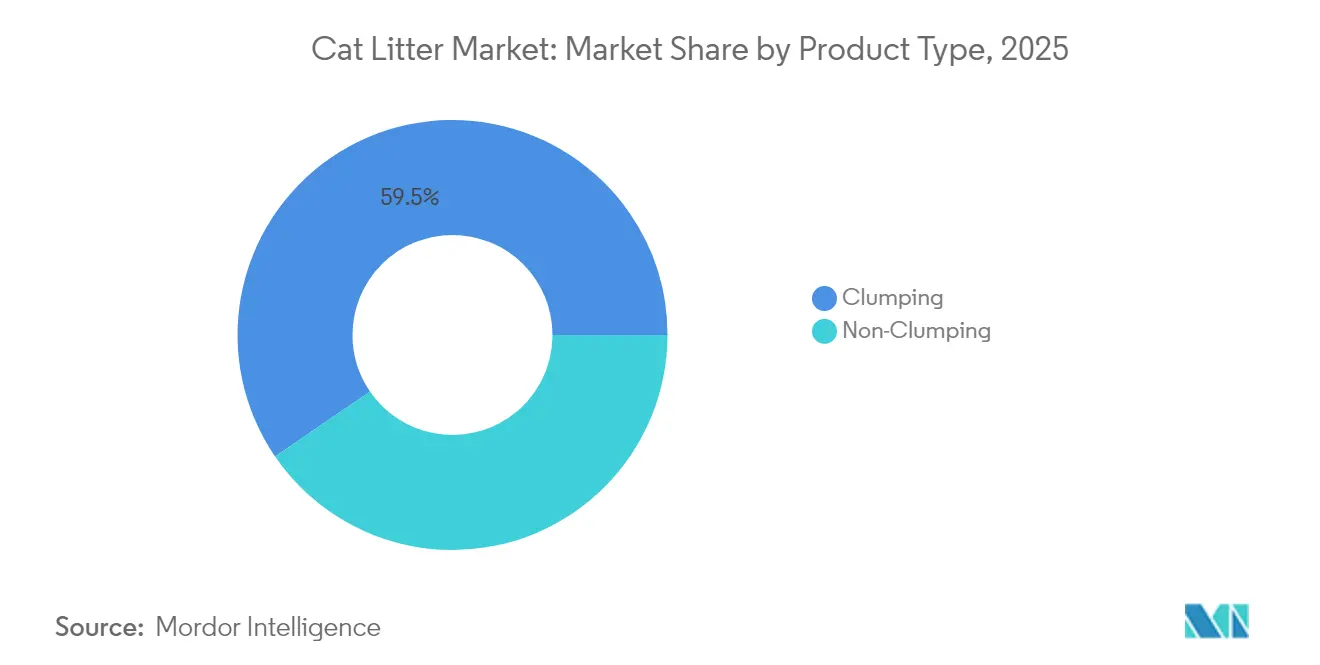

- By product type, clumping litter was the largest segment, accounting for 59.5% of the cat litter market share in 2025, while non-clumping litter accounts for the fastest-growing segment and is forecast to expand at a 3.5% CAGR through 2031.

- By raw material, clay was the largest segment with a 58.4% share in 2025 and is also the fastest-growing segment, projected to grow at a 4.3% CAGR through 2031.

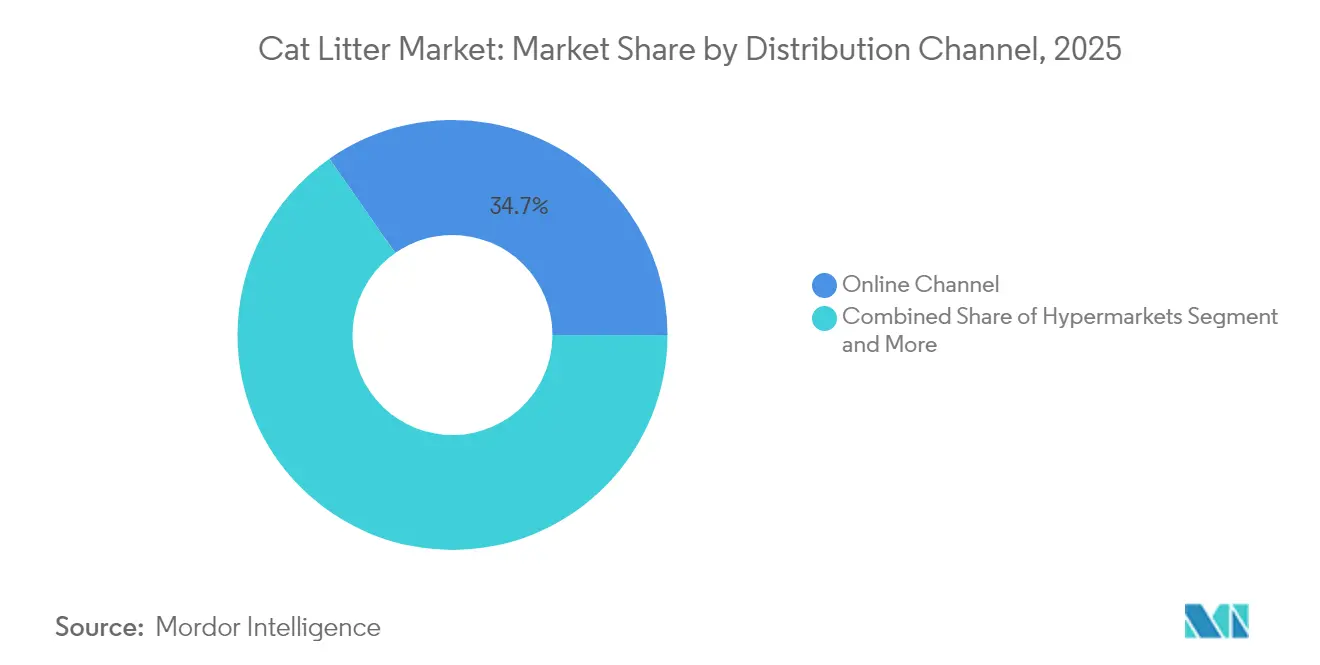

- By distribution channel, the online channel was the largest segment, accounting for 34.7% of the cat litter market in 2025, and also the fastest-growing segment, projected to advance at a 4.5% CAGR through 2031.

- By geography, Europe was the largest segment with 37.6% of cat litter market share in 2025, while North America remains the fastest segment and is forecast to grow at a 4.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cat Litter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising indoor cat ownership and premium pet care spending | +1.2% | Global, with concentration in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| E-commerce subscriptions and auto-replenishment deepen recurring purchasing | +0.8% | North America and Europe core, spillover to Asia-Pacific | Medium term (2-4 years) |

| Clumping, low-dust, and odor-control premiumization expands average selling price | +0.7% | Global, particularly North America and Western Europe | Long term (≥ 4 years) |

| Plant-based and biodegradable litter adoption broadens category appeal | +0.5% | Europe and North America core, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Increased pet humanization | +0.4% | North America and Europe core, early gains in China and Japan | Medium term (2-4 years) |

| Smart litter boxes and health-monitoring systems pull demand for compatible premium litter | +0.3% | North America, Western Europe, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Indoor Cat Ownership and Premium Pet Care Spending

Indoor cat ownership remains one of the most dependable demand anchors in the cat litter market. Households that keep cats indoors purchase litter on a routine cycle, which makes demand steadier than many other pet care categories. Younger adult owners also tend to favor products that reduce dust, improve odor control, and support cleaner home environments. That preference is lifting average selling prices because buyers are choosing better-performing litter instead of only buying more volume. Premium spending is therefore becoming a bigger growth lever than simple unit expansion. This pattern supports continued investment in specialized inputs, cleaner formulations, and better product design across the cat litter market.

E-Commerce Subscriptions and Auto-Replenishment Deepen Recurring Purchasing

Digital replenishment is reducing the time when consumers reconsider brands, which is strengthening recurring demand in the cat litter market. Litter is bulky, heavy, and frequently repurchased, so subscription delivery solves a clear convenience problem for households.Church & Dwight Co., Inc. reported that global online sales accounted for 22.9% of total consumer sales in the first quarter of 2025, an increase from 21.4% for the full year of 2024. This highlights the growing importance of digital channels in routine replenishment decisions[1]Source: Church & Dwight Co., Inc., “Church & Dwight Reports Q4 2025 and 2025 Results and Provides 2026 Outlook,” churchdwight.com. Online purchasing also gives brands better visibility into reorder timing, pack preference, and retention. That data can be used to refine pack architecture, pricing, and product claims. The result is a cat litter market where logistics capability and digital shelf strength matter more each year.

Clumping, Low-Dust, and Odor-Control Premiumization Expands Average Selling Price

Premiumization is one of the main reasons revenue in the cat litter market is growing faster than unit demand. Shoppers are responding to formulas that combine stronger clumping, cleaner pouring, and more durable odor control in one product. These features improve daily use in visible ways, which makes price premiums easier to defend. In February, 2026, Church & Dwight Co., Inc. stated that Arm & Hammer Hardball plant-based clumping litter achieved a 48% repeat rate, 14% points above the category average, which shows that strong performance can translate into repeat buying rather than trial alone. The margin opportunity is real, but so is input risk when better bentonite or plant binders become more expensive. Brands that pair formula claims with supply depth will hold pricing power more effectively in the cat litter market.

Plant-Based and Biodegradable Litter Adoption Broadens Category Appeal

Plant-based litter is expanding the addressable market for cat litter by attracting consumers who do not want to rely on mined clay. These products appeal to buyers who value lighter packs, lower dust, and a more favorable waste profile at home. Retailers are also giving these formats more space because they fit broader shelf narratives around sustainability and cleaner living. In Germany, which remains one of Europe’s most important pet care markets, a mature cat owner base and strong pet retail infrastructure continue to support category trade-up and product experimentation. Plant-based litter also benefits from a practical value message because better absorbency can reduce full-box replacement frequency. That combination is helping plant-based products gain relevance across the cat litter market, even where shelf prices still run above conventional clay.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental scrutiny of clay mining and landfill disposal | -0.5% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Premium price gaps slow adoption of plant-based and smart litter | -0.4% | South America, Middle East, Africa, and price-sensitive Asia-Pacific segments | Medium term (2-4 years) |

| Private-label expansion compresses branded pricing power | -0.6% | North America and Europe | Short term (≤ 2 years) |

| Flushability claims face tighter wastewater and labeling scrutiny | -0.3% | North America, Canada, and European Union member states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Scrutiny of Clay Mining and Landfill Disposal

Environmental pressure on mined inputs is becoming a longer-term cost and reputation issue in the cat litter market. Clay remains central to category performance, but its sourcing and disposal profile draws more scrutiny than plant-derived alternatives. A March 2025 toxicology review by ToxStrategies evaluated potential non-occupational respiratory risks from airborne crystalline silica in bentonite cat litter, adding another layer of caution around dust exposure and product handling[2]Source: ToxStrategies, “Airborne Silica from Bentonite Clay Cat Litter, An Evaluation of Potential Non-Occupational Exposure and Respiratory Health Risks,” toxstrategies.com. Used bentonite litter also remains a landfill burden because it does not break down quickly after disposal. Retailers and regulators are therefore placing more attention on lifecycle impact, dust profile, and sourcing transparency. Brands without alternative raw material pathways could face rising pressure as the cat litter market moves through the forecast period.

Premium Price Gaps Slow Adoption of Plant-Based and Smart Litter

Price still limits how quickly premium formats can spread through the cat litter market, especially outside higher-income urban centers. Plant-based products, crystal health-monitoring products, and compatible smart-system litter often sit well above standard clay at the shelf. In price-sensitive markets, many households continue to prioritize low upfront cost over improved performance or added functionality. The problem is not only affordability, but also the difficulty of explaining long-term value when shoppers compare packs mainly on immediate price. Subscription models can reduce some friction, but they work best where digital retail and home delivery are already well developed. Until production scale improves further, this restraint will continue to slow premium adoption in parts of the cat litter market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Clumping Innovation Challenges Clumping's Dominance

Market share remained concentrated in clumping litter, the largest product type in the cat litter market, with 59.5% in 2025. Clumping has held that lead because it aligns with long-established cleaning habits and supports quick waste removal in everyday use. It also fits many automatic litter systems, which reinforces repeat purchase through functional compatibility. This installed preference makes the segment hard to displace quickly, even when new materials enter the shelf. In practical terms, clumping still sets the baseline performance standard for much of the cat litter market.

Market size growth is stronger in non-clumping litter, the fastest product type, which is projected to expand at a 3.5% CAGR through 2031. Plant-based pellets, tofu-based formats, and crystal substrates are helping the segment reach consumers who want lower dust, lighter packs, or different waste handling characteristics. Health-monitoring functionality is also more naturally aligned with certain non-clumping crystal systems, which gives the segment a clear premium use case. Nestlé Purina PetCare’s Petivity platform supports the broader shift toward litter-linked monitoring and reinforces interest in performance beyond basic cleanup. The fastest growth, therefore, sits with formats that offer a new reason to switch rather than a small variation on clay.

By Raw Material: Silica Gains Ground in a Clay-Dominated Market

Clay is the largest raw material segment in the cat litter market, with 58.4% in 2025, and is also the fastest-growing segment, projected to grow at a 4.3% CAGR through 2031. Clay remains difficult to replace because it combines clumping strength, moisture absorption, and price accessibility at scale. That performance keeps it central to both mass retail and many premium clumping products. The segment also benefits from user familiarity, which lowers the risk of trial disappointment for everyday buyers. For now, clay continues to define the operating center of the cat litter market.

Silica supports low-dust handling and moisture control, and it is especially relevant in products that emphasize cleanliness, convenience, or health-linked observation. Its role in premium crystal litter makes it more exposed to trade-up behavior than to broad entry-level demand. At the same time, plant-based inputs are forming a credible secondary growth cluster because they address lighter weight and reduced reliance on mined materials. That leaves the cat litter market with a more varied raw material mix, even though clay remains the largest base.

By Distribution Channel: Digital Platforms Redefine Cat Litter Retailing

Market share was highest in the online channel, the largest distribution segment in the cat litter market, at 34.7% in 2025. This lead reflects the fact that litter is heavy, repetitive, and easy to reorder on a schedule. Digital retail also makes it easier for shoppers to compare pack sizes, read reviews, and subscribe without having to carry large bags home. Church & Dwight Co., Inc. reported rising online sales exposure which supports the broader role of digital commerce in high-frequency household replenishment. The online lead is therefore rooted in both shopper convenience and strong repeat economics for brands.

Online channel which are projected to rise at a 4.5% CAGR through 2031 as large retailers expand shelf depth for premium and value packs. Hypermarkets remain important for first-time purchases, visible price comparison, and multi-pack promotions that drive basket efficiency.. Specialized pet shops still matter because they support guided selection for odor-sensitive, low-dust, and health-focused products. This leaves the cat litter market with a genuinely multi-channel structure rather than a single winning route to consumer demand.

Geography Analysis

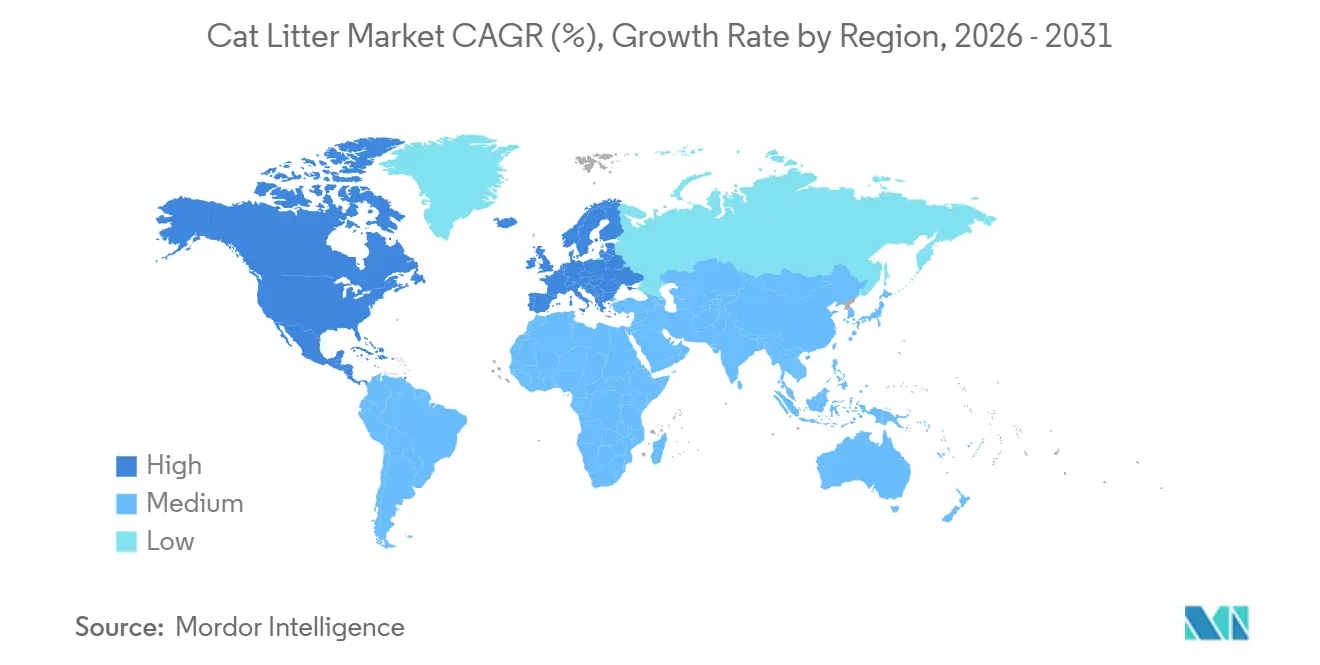

Europe was the largest regional segment in the cat litter market with 37.6% share in 2025. Germany anchors that position because it combines high cat ownership with a broad pet retail reach across specialist chains, discounters, and online formats. Industrieverband Heimtierbedarf (IVH) reported that Germany’s stationary retail cat litter market reached EUR 370 million (USD 400 million) in 2025, while the country’s domestic cat population stood at 15.7 million[3]Source: Industrieverband Heimtierbedarf (IVH) e.V., “Der Deutsche Heimtiermarkt 2025,” ivh-online.de. That scale gives Europe a stable demand base even when consumer spending becomes more selective. It also supports the faster rollout of plant-based, silica, and premium odor-control products across the cat litter market.

North America is the fastest regional segment in the cat litter market and is forecast to grow at a 4.44% CAGR through 2031. The region benefits from dense digital retail networks, strong premium acceptance, and a high pace of product refresh from established suppliers. North America also leads in smart litter adoption because hardware, subscription, and branded consumables are advancing together. Regulatory scrutiny of disposal and labeling may increase compliance requirements, but it is unlikely to diminish the region’s importance in the cat litter market.

Asia-Pacific, South America, the Middle East, and Africa represent the longer-range expansion frontier for the cat litter market. In the Asia-Pacific region, urban cat ownership is rising among younger consumers who treat pet spending as part of their household routine rather than as an occasional discretionary purchase. Church & Dwight Co., Inc. identified Arm & Hammer as its largest international litter brand in China, suggesting ample room for premium and locally adapted formats in the region. South America, the Middle East, and Africa remain more price sensitive, so value products and local supply will shape adoption speed. Even so, the cat litter market in these regions should widen as distribution improves and awareness of indoor cat care becomes more established.

Competitive Landscape

The cat litter market remains moderately concentrated globally, with leadership split between large multinational suppliers and strong regional brand owners. Nestlé SA and The Clorox Company hold entrenched positions in North America, while European competition includes established regional names that benefit from local retail familiarity. The field is broad enough that no single supplier defines the category worldwide. That breadth keeps pricing, product claims, and channel execution highly contested across the cat litter market.

Strategic competition in the cat litter market is now centered on innovation, omnichannel execution, and consumer retention rather than on scale alone. The Clorox Company executed a major Fresh Step brand refresh in February 2026, using clearer shelf communication and new packaging formats to improve brand visibility and shopper conversion. Nestlé Purina PetCare has continued to build relevance around health-linked monitoring through Petivity, which gives the brand a stronger position in premium care conversations. These moves show that leading companies are trying to build moats that private-label rivals cannot easily copy.

The cat litter market is also widening at the edges, where smaller and regional players can still compete through focused positioning. Private-label suppliers are gaining ground in mature channels, especially where formula differences are not obvious to the average buyer. At the same time, brands with stronger sourcing control, premium claims, or health-related utility are more likely to defend price and shelf space. The result is a market that is active and competitive, but not consolidated enough to shut out targeted challengers.

Cat Litter Industry Leaders

Mars Inc.

Nestlé SA (Purina)

The Clorox Company

Church and Dwight Co. Inc.

Oil-Dri Corporation of America

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Church & Dwight Co., Inc. launched Arm & Hammer dual defense with Microban Clumping Litter, combining proprietary odor-elimination technology with Microban antimicrobial product protection, available exclusively at a leading mass retailer, targeting germ-conscious cat owners and extending the brand's functional differentiation in the competitive clumping segment.

- April 2025: Pets Choice Ltd acquired the Pettex Cat Litter and Small Animal business, integrating Pettex's established United Kingdom and international cat litter brands into its portfolio alongside the Felight cat litter brand, with the acquisition excluding Pettex's reptile and aquatics division, strengthening Pets Choice Ltd's position across grocery, independent pet retail, and online channels.

- March 2025: Oil-Dri Corporation launched Cat’s Pride Antibacterial Clumping Litter at the Global Pet Expo. This clay-based litter is the first and only EPA-approved antibacterial formula in the United States, designed to eliminate 99.9% of odor-causing bacteria. It is promoted as being up to 40% lighter than conventional heavy clay litter.

Global Cat Litter Market Report Scope

Cat litter is one of the major necessities for a cat owner, along with cat food. A litter box collects cat urine and feces.

The cat litter market is segmented by product type (clumping and conventional), raw material (clay, silica and plant-based), distribution channel (specialized pet shops, internet sales, hypermarkets, and other sales channels), and geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Product Type

| Clumping |

| Non-Clumping |

By Raw Material

| Clay | |

| Silica | |

| Plant-based | Corn |

| Wheat | |

| Wood and bamboo | |

| Paper | |

| Soy |

By Distribution Channel

| Specialized Pet Shops |

| Online Channel |

| Hypermarkets |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Clumping | |

| Non-Clumping | ||

| By Raw Material | Clay | |

| Silica | ||

| Plant-based | Corn | |

| Wheat | ||

| Wood and bamboo | ||

| Paper | ||

| Soy | ||

| By Distribution Channel | Specialized Pet Shops | |

| Online Channel | ||

| Hypermarkets | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is driving growth in cat litter demand through 2031?

Growth is being supported by indoor cat ownership, premiumization in odor-control and low-dust products, and wider use of digital replenishment. The category is projected to rise from USD 6.26 billion in 2026 to USD 7.66 billion by 2031 at a 4.14% CAGR.

Which product type leads sales and which one is growing fastest?

Clumping litter was the largest product type with 59.5% share in 2025, while non-clumping litter is the fastest-growing product type with a 3.5% CAGR through 2031.

Why are online sales so important for this category?

Litter is bulky and frequently repurchased, so subscriptions and home delivery solve a real convenience need. That is why the online channel held the largest distribution share at 34.7% in 2025.

Which region is the strongest right now?

Europe was the largest regional segment with 37.6% share in 2025, supported by a large cat population and mature retail structure, especially in Germany.

Which region is expanding the fastest?

North America is forecast to grow the fastest at a 4.4% CAGR through 2031 because it combines premium product adoption, strong digital infrastructure, and faster rollout of new litter concepts.

What is changing competition among leading suppliers?

Competition is moving toward differentiated formulas, omnichannel execution, and health-linked or device-compatible products. That makes innovation and recurring purchase systems more important than broad shelf presence alone.

Page last updated on: