PET Film Coated Steel Coil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 17.20 Billion |

| Market Size (2031) | USD 22.14 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PET Film Coated Steel Coil Market Analysis by Mordor Intelligence

The PET Film Coated Steel Coil Market size is expected to grow from USD 16.35 billion in 2025 to USD 17.20 billion in 2026 and is forecast to reach USD 22.14 billion by 2031 at 5.18% CAGR over 2026-2031. Asia-Pacific continues to anchor demand as appliance and electrical-equipment production migrates to India and China, while Europe and North America accelerate specification of chlorine-free laminates to meet low-VOC (Volatile Organic Compound) and circular-economy rules. The structural pivot away from PVC toward polyethylene terephthalate coatings is reinforced by scratch-resistant, color-stable finishes that shorten OEM (Original Equipment Manufacturer) assembly cycles and reduce warranty claims. Corrosion regulations in coastal infrastructure and renewable-energy assets are moving substrate choice toward galvalume and aluzinc, stimulating new coating-line investments. Integrated mills are tightening supply chains by pairing captive cold-rolling capacity with in-house PET lamination, securing film offtake in a market exposed to Asian resin concentration and trade-remedy investigations.

Key Report Takeaways

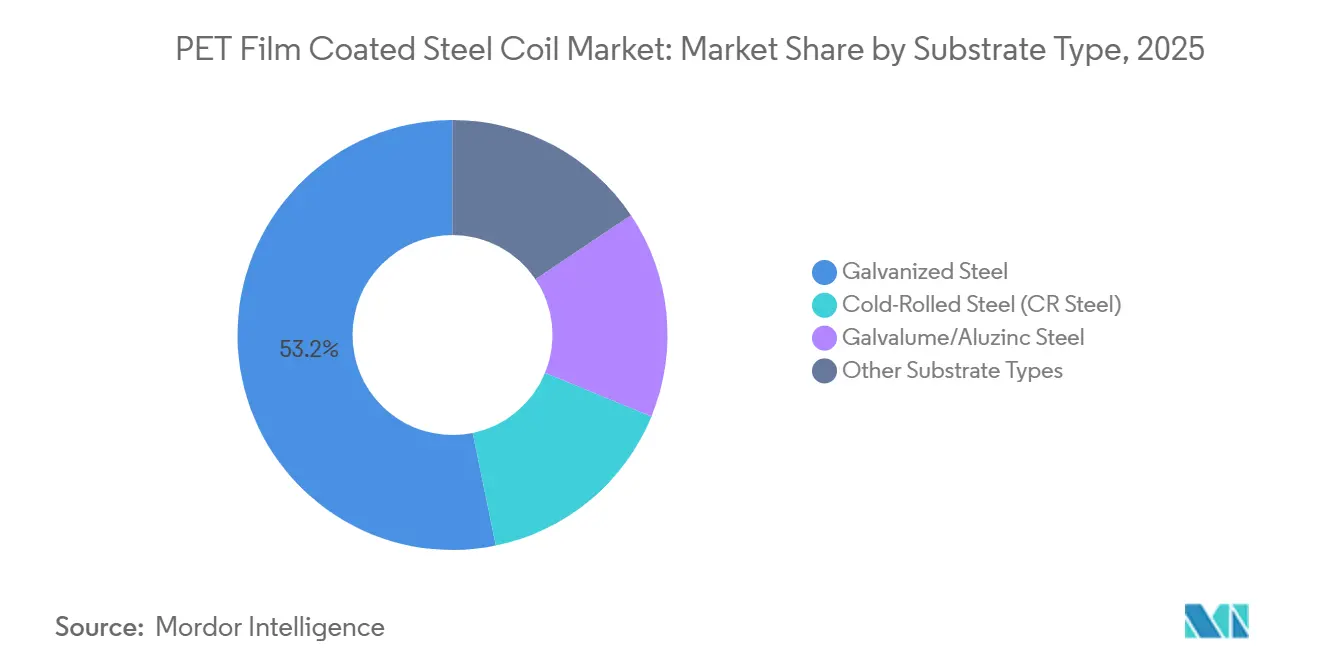

- By substrate type, galvanized steel held 53.22% of the PET film coated steel coil market share in 2025, while galvalume/aluzinc is forecast to record a 5.81% CAGR to 2031.

- By coating type, Single-side PET film coating captured 63.35% share in 2025; antibacterial and functional PET films are set to expand at a 5.97% CAGR through 2031.

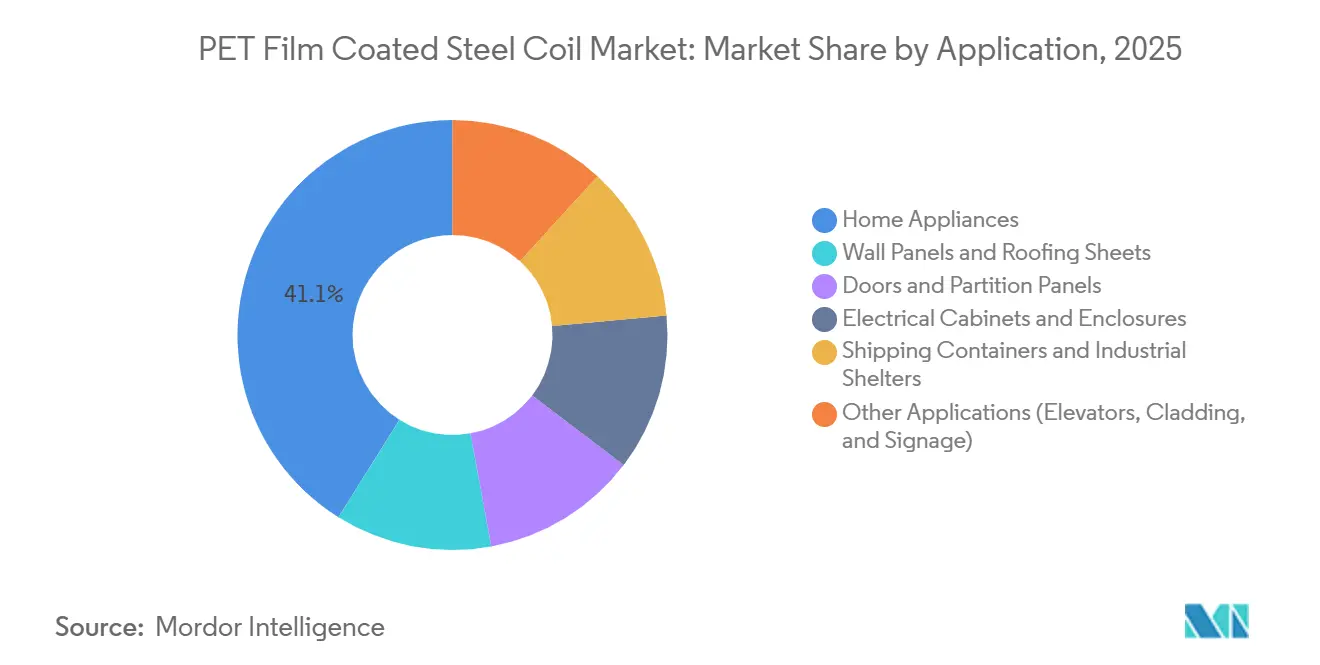

- By application, home appliances accounted for 41.11% of the market size in 2025, whereas electrical cabinets and enclosures are projected to grow at a 6.23% CAGR during the forecast period (2026-2031).

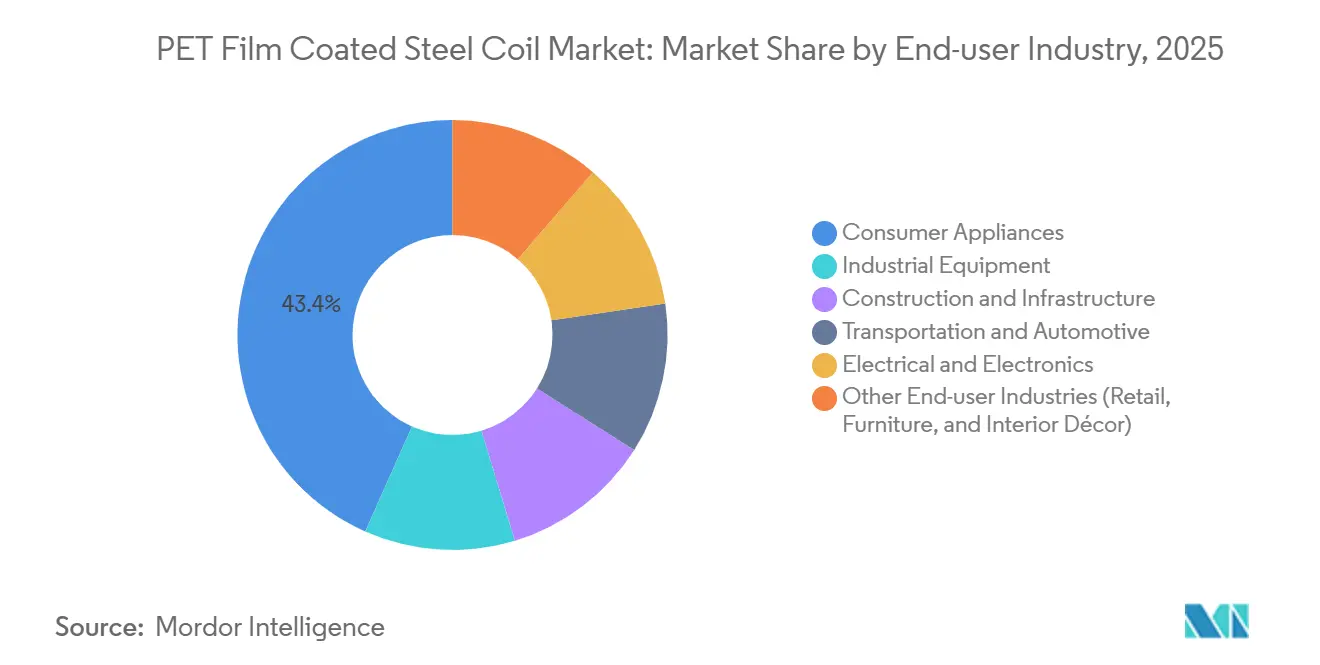

- By end-user industry, consumer appliances dominated with 43.36% revenue share in 2025, while electrical and electronics are expected to grow with a 6.32% CAGR during the forecast period (2026-2031).

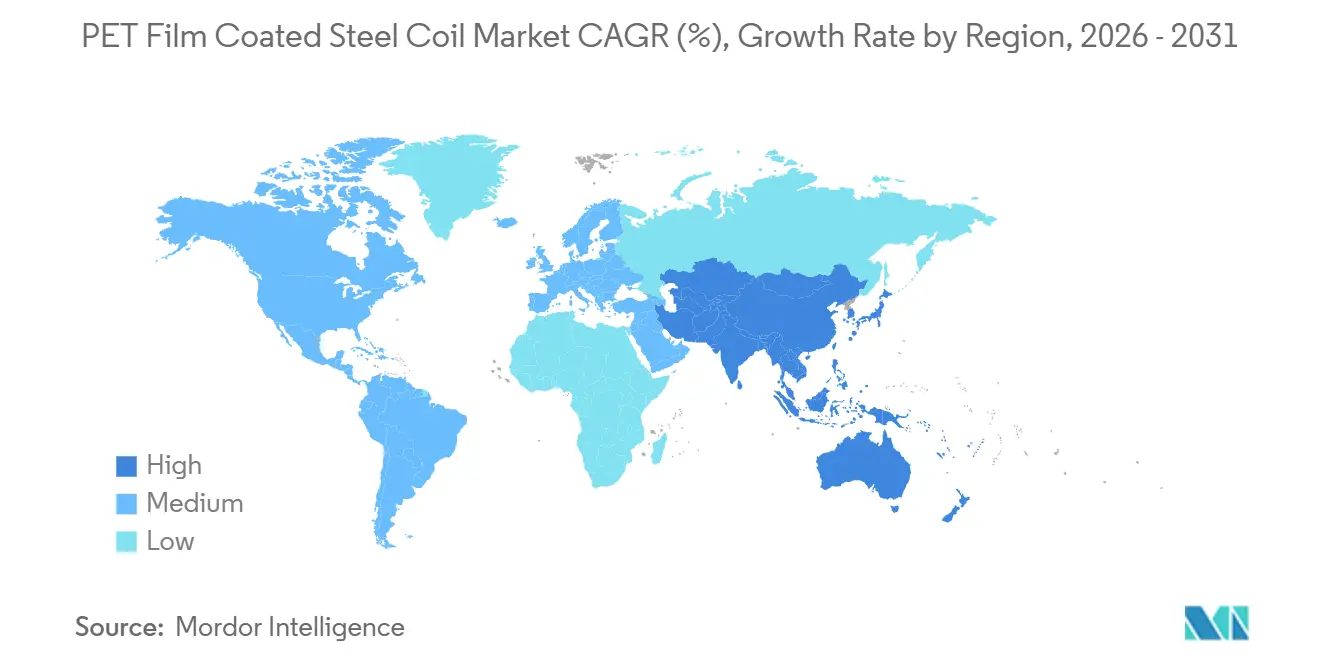

- By region, Asia-Pacific commanded 52.26% share in 2025 and remains the fastest-growing geography at a 6.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global PET Film Coated Steel Coil Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of appliance manufacturing using aesthetic steel panels | +1.2% | Asia-Pacific (China, India, ASEAN), spill-over to North America | Medium term (2-4 years) |

| Preference for PET-coated steel over PVC on sustainability grounds | +0.9% | Global, with regulatory acceleration in Europe and North America | Long term (≥4 years) |

| Improved scratch resistance and color retention driving OEM usage | +0.8% | Global, concentrated in Consumer Appliances and Electrical & Electronics | Short term (≤2 years) |

| Adoption in smart-home exterior panels requiring IR-reflective coatings | +0.6% | North America, Europe, urban APAC markets | Medium term (2-4 years) |

| Emergence of ultra-thin PET films enabling laser micro-perforation for ventilation | +0.4% | APAC core (China, Japan, South Korea), early adoption in Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of Appliance Manufacturing Using Aesthetic Steel Panels

White-goods producers in Asia-Pacific are specifying PET laminates to avoid post-assembly painting, cut volatile-organic-compound emissions, and deliver uniform gloss. Jindal India’s February 2026 coating line lifts value-added capacity by 60% to 300,000 tons/year, targeting refrigerators, washer housings, and solar structures[1]Jindal India, “New Metal Coating Line Commissioning,” jindalindia.com. ArcelorMittal Nippon Steel India aims to raise value-added revenue share to 75% with two new coated brands positioned for appliance OEMs. As e-commerce distribution grows, dent-resistant, scratch-proof panels maintain a showroom finish through long logistics chains, shifting margin pools toward downstream lamination.

Preference for PET-Coated Steel Over PVC on Sustainability Grounds

Regulators are phasing out PVC because of chlorine chemistry and poor recyclability. Germany’s December 2024 National Circular Economy Strategy introduces polymer-specific recycled-content quotas and digital product passports, encouraging mono-material PET designs[2]Federal Ministry for the Environment, “National Circular Economy Strategy,” bmuv.de. The European Union’s draft Packaging Regulation seeks 70% recycling by 2030, making chlorine-free PET laminates preferable to PVC coatings that hinder material recovery. Peer-reviewed work shows PET-coated steel eliminates spray-paint VOCs while maintaining barrier integrity.

Improved Scratch Resistance and Color Retention Driving OEM Usage

Appliance makers value PET for its higher surface hardness and gloss retention versus polyester paints. Twenty-year outdoor exposure tests confirm color shift below ΔE (Delta E) 5, supporting premium warranties. Antibacterial PET films with silver ions achieve more than 99% bacterial reduction per ISO 22196, serving hospitals and food plants. February 2026 research reported Cu@Ag nanoparticle PET films preserving 108.79 MPa tensile strength and expanding antimicrobial halos without degrading thermal stability.

Adoption in Smart-Home Exterior Panels Requiring IR-Reflective Coatings

Smart-building facades embed sensors that raise enclosure temperatures; IR-reflective PET coatings mitigate heat without active cooling. Tata BlueScope reports 15% HVAC (Heating, Ventilation, and Air Conditioning) savings from solar-reflective steels in India. Vacuum-metalized PET delivers radiant-barrier performance while offering decorative holographic finishes for high-end construction. Green-building labels such as LEED (Leadership in Energy and Environmental Design) embed cool-roof metrics, lifting demand in North America and Europe.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited recyclability of multilayer coated substrates | -0.7% | Global, acute in Europe due to PPWR and NCES mandates | Medium term (2-4 years) |

| Technical challenges in adhesion and film delamination | -0.5% | Global, concentrated in high-forming applications (automotive, deep-draw appliances) | Short term (≤2 years) |

| Scarce global PET-grade film supply outside of Asia | -0.4% | North America, Europe, MEA | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Limited Recyclability of Multilayer Coated Substrates

Fused polymer-metal interfaces resist mechanical separation, complicating European recycling targets. Cleaner-Production reviews find multilayer films already 17% of flexible output, yet advanced recovery routes raise GHGs by 21% versus incineration at the current scale. Chemical depolymerization options are unproven commercially, pressuring manufacturers to trial water-soluble adhesives or split-layer designs.

Technical Challenges in Adhesion and Film Delamination

Deep drawing can exceed 30% substrate strain, risking edge peeling if surface preparation, adhesive chemistry, or laminate tension deviates from spec. Two-layer PET on food cans survived 2 meters per second ironing only when the total polymer exceeded 12.5 µm. Outdoor moisture accelerates interface disbondment, demanding stringent ISO 9227 salt-spray and ISO 6270-1 condensation tests.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Type: Corrosion-Resistant Galvalume Accelerates

Galvanized coil delivered 53.22% revenue in 2025, but galvalume/aluzinc steel is forecast to grow at a 5.81% CAGR during the forecast period (2026-2031) as coastal infrastructure adopts ISO 12944 C4-C5 durability. Salt-spray tests show galvalume loses only 0.03 mm/year after 2,000 hours, extending field life beyond 20 years. The PET film coated steel coil market size for galvalume substrates is therefore set to expand faster than for galvanized, even considering its USD 150/ton price premium. Producers are recalibrating adhesion layers to match the higher aluminum oxide content that can impair bonding and require modified primers.

Advanced AI quality-control on new coating lines supports uniform galvalume thickness control and raises yield. Predictive maintenance has already cut unplanned downtime 50% at Chinese mills, tipping project economics toward high-grade metallic coatings. As renewable-energy farms and data-center campuses cluster near humid coastal zones, PET film coated steel coil market demand for galvalume and aluzinc will keep climbing through 2031.

By Coating Type: Functional Films Earn Hygiene Premiums

Single-side PET film coating retained 63.35% revenue in 2025 because most appliance back panels require only front-face protection. The PET film coated steel coil market size for antibacterial and functional PET films, however, is growing at a 5.97% CAGR for the forecast period (2026-2031) as hospitals, canteens, and cleanrooms specify ISO 22196-compliant solutions. Silver-ion coatings maintain more than 99% bacterial suppression for a decade without discoloration.

Double-side, matte, and UV-stable products serve architectural interiors and elevator cabins where both faces are visible or sunlight exposure is severe. Functional differentiation shields margins from Asian commodity overcapacity: nanoparticle, anti-fingerprint, and IR-reflective variants command 20-40% premiums, helping suppliers offset resin cost spikes. Market leaders that integrate co-extrusion of additives are positioned to widen their PET film coated steel coil market share over strip-paint rivals.

By Application: Electrical Enclosures Register Fastest Growth

Home appliances still led revenue at 41.11% in 2025, yet data-center and renewable-energy build-outs push electrical cabinets and enclosures to a 6.23% CAGRfor the forecast period (2026-2031). The PET film coated steel coil market size for ISO 12944 C3-C5-rated cabinets will expand as OEMs adopt factory-finished shells that skip on-site painting. Modular data halls favor plug-and-play skids where pre-laminated steel shortens commissioning schedules, while EV-charging rollouts need outdoor-rated housings resistant to salt spray and UV degradation.

Wall panels, roofing sheets, and doors adopt reflective PET films to cut thermal loads. Shipping containers gain from corrosion protection and lighter weight versus paint systems, although mechanical delamination risk in high-strain deformation still limits penetration. Suppliers able to certify IP67 ingress ratings and UL-listed flammability have a clear lane to capture advanced-electronics enclosures within the PET film coated steel coil market.

By End-user Industry: Electronics Outpaces Appliances

Consumer appliances delivered 43.36% revenue in 2025, but electrical and electronics are expected to grow at 6.32% CAGR during the forecast period (2026-2031) as smart-home devices, EV chargers, and power inverters multiply enclosure counts. PET film coated steel coil market demand rises alongside Nippon Steel’s JPY 213 billion (USD 1.43 billion) program to upgrade electrical-steel lines for high-grade laminations. Construction, infrastructure, and transportation also integrate cool-roof laminates and corrosion-proof container panels. Decorative furniture and retail fixtures adopt wood-grain PET prints, broadening aesthetic applications without added weight.

Momentum in electronics stems from three shifts: distributed solar adding inverter boxes, hyperscale data centers standardizing modular electrical rooms, and IoT (Internet of Things) sensors embedding in façade panels. Inline metallization and laser-perforated PET films answer these use cases with electromagnetic shielding and condensation control, reinforcing the PET film coated steel coil market’s orientation toward high-spec functional layers.

Geography Analysis

Asia-Pacific generated 52.26% revenue in 2025 and will grow at 6.12% CAGR through 2031. India’s newly commissioned INR 11 billion (approximately USD 132 million) line lifts domestic coated-steel capacity, aiming at 300,000 tons/year for appliances and solar racks. ArcelorMittal Nippon Steel is shifting 75% of revenue to value-added grades, leveraging India’s 10% annual appliance demand growth. China’s resin surplus powers exports even as anti-dumping cases rise, sustaining utilization near 75%. ASEAN tinplate expansions further embed PET laminates into regional supply chains.

North America and Europe show slower volume growth yet command higher per-ton margins driven by VOC caps and recycled-content quotas. The U.S. EPA (Environmental Protection Agency) moved iron-and-steel air-rule compliance to April 2027, affecting substrate costs for domestic laminators. Germany’s circular-economy program mandates digital product passports by 2030, boosting traceable PET coatings. Freight premiums lifted Q4 2025 BOPET (Biaxially Oriented Polyethylene Terephthalate) prices in the United States despite soft converter demand.

South America and the Middle East & Africa remain smaller, opportunity-rich regions where infrastructure megaprojects and petrochemical plants need corrosion-proof cladding. Their dependence on Asian film imports intensifies volatility, yet localized slitting centers could shorten lead times and lift PET film coated steel coil market penetration.

Competitive Landscape

The PET film coated steel coil market is moderately fragmented. Strategic priorities among incumbents include long-term offtake agreements with Asian BOPET manufacturers, investment in chemical recycling partnerships to meet European regulatory requirements, and the development of ultra-thin, laser-perforable films for ventilated smart-home cladding. Suppliers that successfully combine functional innovation with traceable low-carbon supply chains are expected to gain market share despite fluctuations in resin costs.

PET Film Coated Steel Coil Industry Leaders

ArcelorMittal

DONGKUKHOLDINGS CO., LTD.

JFE Steel Corporation

Lampre s.r.l.

MARCEGAGLIA CARBON STEEL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hyundai Steel has announced the selection of Donaldsonville, Louisiana, as the site for a USD 5.8 billion steel mill that will utilize direct reduced iron technology. Additionally, this initiative aligns with Hyundai Steel's focus on expanding its portfolio, including PET film-coated steel coils, to meet evolving market demands for advanced and sustainable steel solutions.

- September 2024: Marcegaglia invested in a new electric arc furnace in Sheffield, UK. This facility is expected to enhance annual stainless steel production capacity to over 500,000 tons. The investment also supports the company’s efforts to diversify its offerings, including PET film-coated steel coils, catering to the growing demand for innovative and eco-friendly steel products.

Global PET Film Coated Steel Coil Market Report Scope

PET film coated steel coil combines high-strength steel (cold-rolled or galvanized) with a durable, decorative polyethylene terephthalate (PET) film layer. It offers superior corrosion resistance, aesthetic versatility, and eco-friendly properties, commonly used for home appliances (refrigerators, washers), construction (roofing, walls), and automotive parts.

The PET Film Coated Steel Coil market is segmented by substrate type, coating type, application, end-user industry, and geography. By substrate type, the market is segmented into cold-rolled steel (CR steel), galvanized steel, galvalume/aluzinc steel, and other substrate types. By coating type, the market is segmented into single-side PET film coating, double-side PET film coating, UV/matte/glossy PET film coatings, and antibacterial and functional PET films. By application, the market is segmented into home appliances, wall panels and roofing sheets, doors and partition panels, electrical cabinets and enclosures, shipping containers and industrial shelters, and other applications (elevators, cladding, and signage). By end-user industry, the market is segmented into construction and infrastructure, consumer appliances, industrial equipment, transportation and automotive, electrical and electronics, and other end-user industries (retail, furniture, and interior décor). The report also covers the market size and forecasts for PET film coated steel coil in 17 countries across major regions. The market sizes and forecasts are provided in value (USD).

| Cold-Rolled Steel (CR Steel) |

| Galvanized Steel |

| Galvalume/Aluzinc Steel |

| Other Substrate Types |

| Single-side PET Film Coating |

| Double-side PET Film Coating |

| UV/Matte/Glossy PET Film Coatings |

| Antibacterial and Functional PET Films |

| Home Appliances |

| Wall Panels and Roofing Sheets |

| Doors and Partition Panels |

| Electrical Cabinets and Enclosures |

| Shipping Containers and Industrial Shelters |

| Other Applications (Elevators, Cladding, and Signage) |

| Construction and Infrastructure |

| Consumer Appliances |

| Industrial Equipment |

| Transportation and Automotive |

| Electrical and Electronics |

| Other End-user Industries (Retail, Furniture, and Interior Décor) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Substrate Type | Cold-Rolled Steel (CR Steel) | |

| Galvanized Steel | ||

| Galvalume/Aluzinc Steel | ||

| Other Substrate Types | ||

| By Coating Type | Single-side PET Film Coating | |

| Double-side PET Film Coating | ||

| UV/Matte/Glossy PET Film Coatings | ||

| Antibacterial and Functional PET Films | ||

| By Application | Home Appliances | |

| Wall Panels and Roofing Sheets | ||

| Doors and Partition Panels | ||

| Electrical Cabinets and Enclosures | ||

| Shipping Containers and Industrial Shelters | ||

| Other Applications (Elevators, Cladding, and Signage) | ||

| By End-user Industry | Construction and Infrastructure | |

| Consumer Appliances | ||

| Industrial Equipment | ||

| Transportation and Automotive | ||

| Electrical and Electronics | ||

| Other End-user Industries (Retail, Furniture, and Interior Décor) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for PET-laminated coils be by 2031?

The PET film coated steel coil market is projected to reach USD 22.14 billion by 2031, growing at a 5.18% CAGR over 2026-2031.

Which application is expanding fastest?

Electrical cabinets and enclosures lead growth with a 6.23% CAGR during the forecast period (2026-2031) as data centers and renewable-energy inverters proliferate.

Why are PET laminates replacing PVC coatings?

PET avoids chlorine chemistry, meets tougher recycling targets, and delivers better scratch and color stability demanded by OEMs.

Which region offers the strongest growth outlook?

Asia-Pacific holds more than 52.26% revenue and will rise at 6.12% CAGR during the forecast period (2026-2031), supported by capacity additions in India and China.

Page last updated on: