Cold-Rolled Steel Coil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

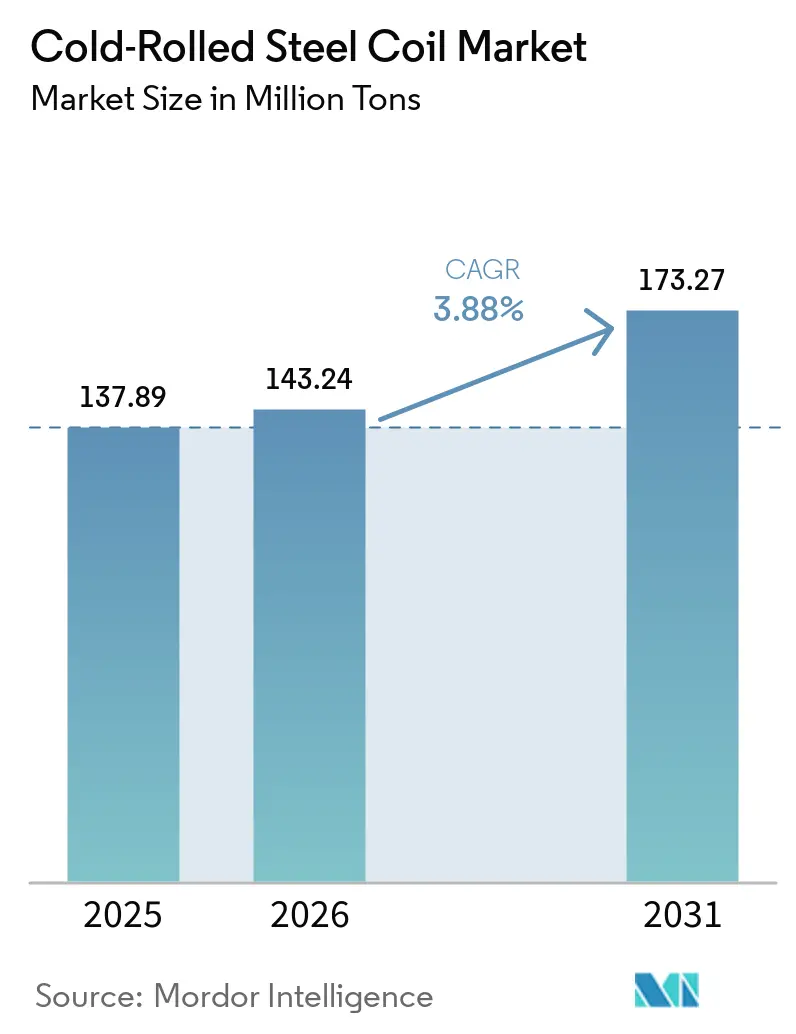

| Market Volume (2026) | 143.24 Million tons |

| Market Volume (2031) | 173.27 Million tons |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

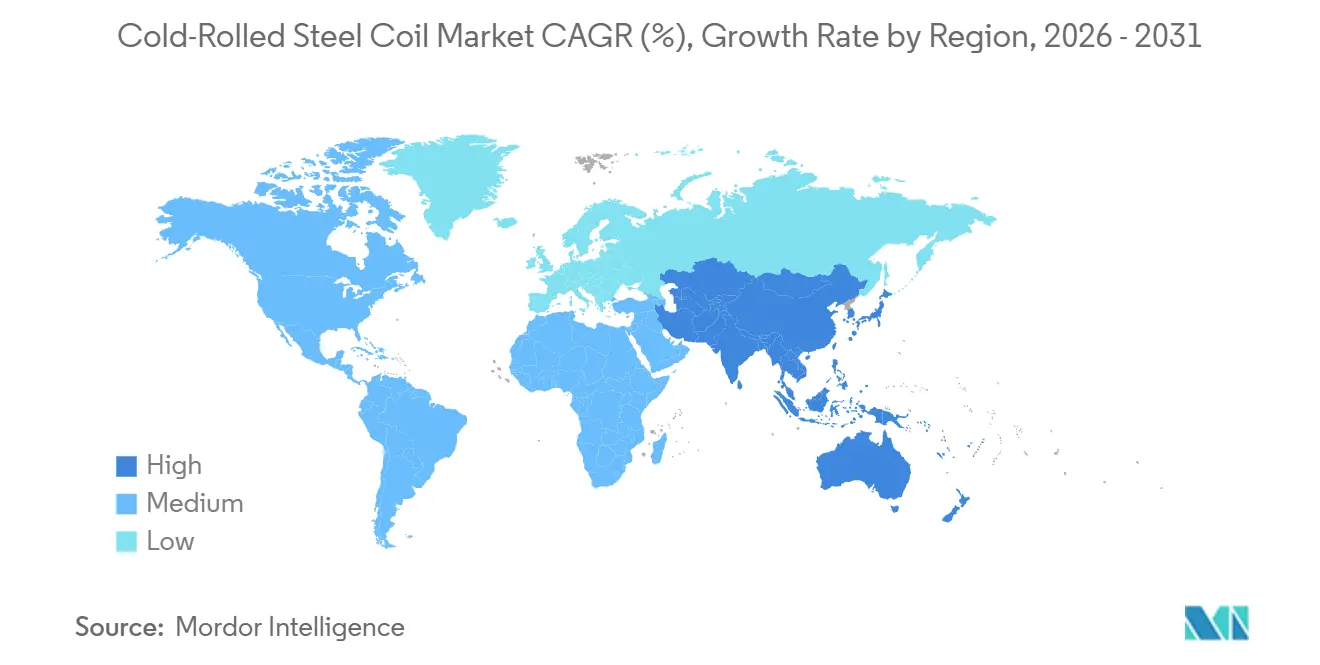

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cold-Rolled Steel Coil Market Analysis by Mordor Intelligence

The Cold-Rolled Steel Coil Market size is expected to increase from 137.89 Million tons in 2025 to 143.24 Million tons in 2026 and reach 173.27 Million tons by 2031, growing at a CAGR of 3.88% over 2026-2031. Automotive electrification pushes advanced high-strength steel (AHSS) into battery enclosures and crash structures, lifting value per vehicle even where unit output plateaus. Data-center construction in North America and Europe absorbs cold-formed framing faster than traditional commercial buildings, while modular housing encourages thin-gauge galvanized coil in seismic zones. Asia-Pacific commands 59.94% of volume and will keep outpacing global growth as India commissions more than USD 10 billion of new capacity and Southeast Asian automakers localize sourcing. Premiums of USD 150-200 per ton for AHSS over commodity low-carbon coil entice integrated mills to upgrade annealing and coating lines, even as electric-arc-furnace (EAF) producers expand commodity supply.

Key Report Takeaways

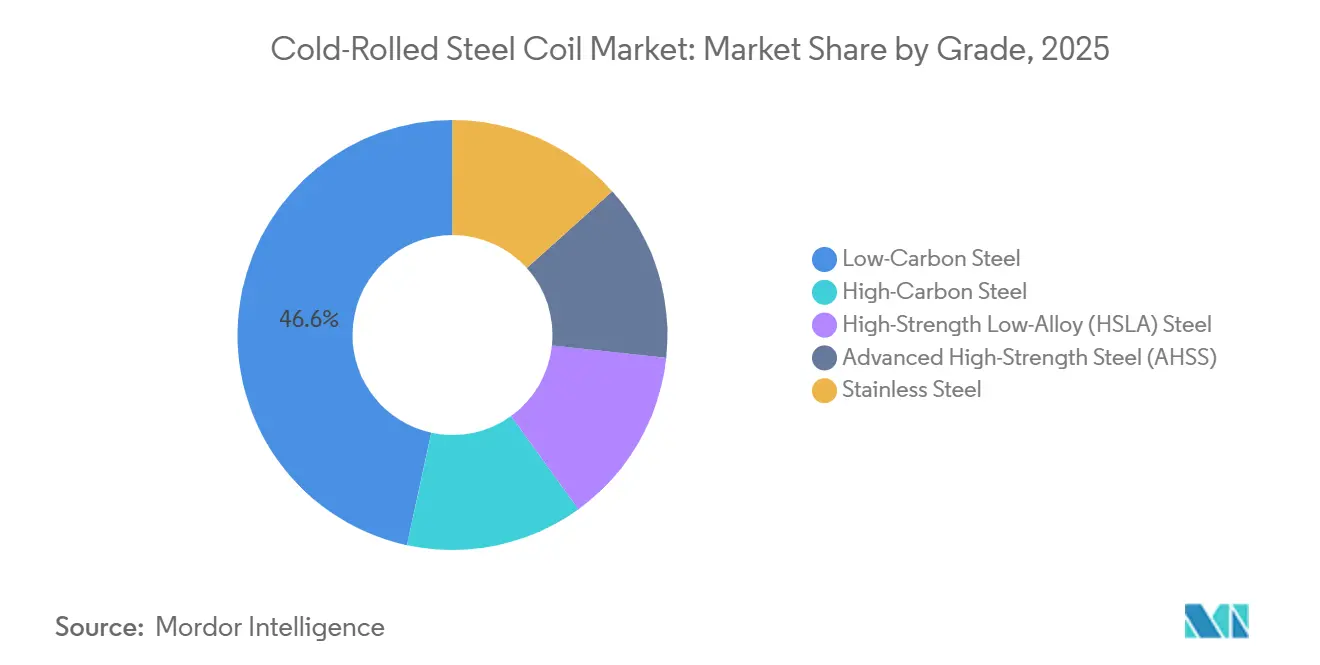

- By grade, low-carbon steel led with 46.61% of the cold-rolled steel coil market share in 2025, while advanced high-strength steel (AHSS) is forecast to grow at a 4.55% CAGR through 2031.

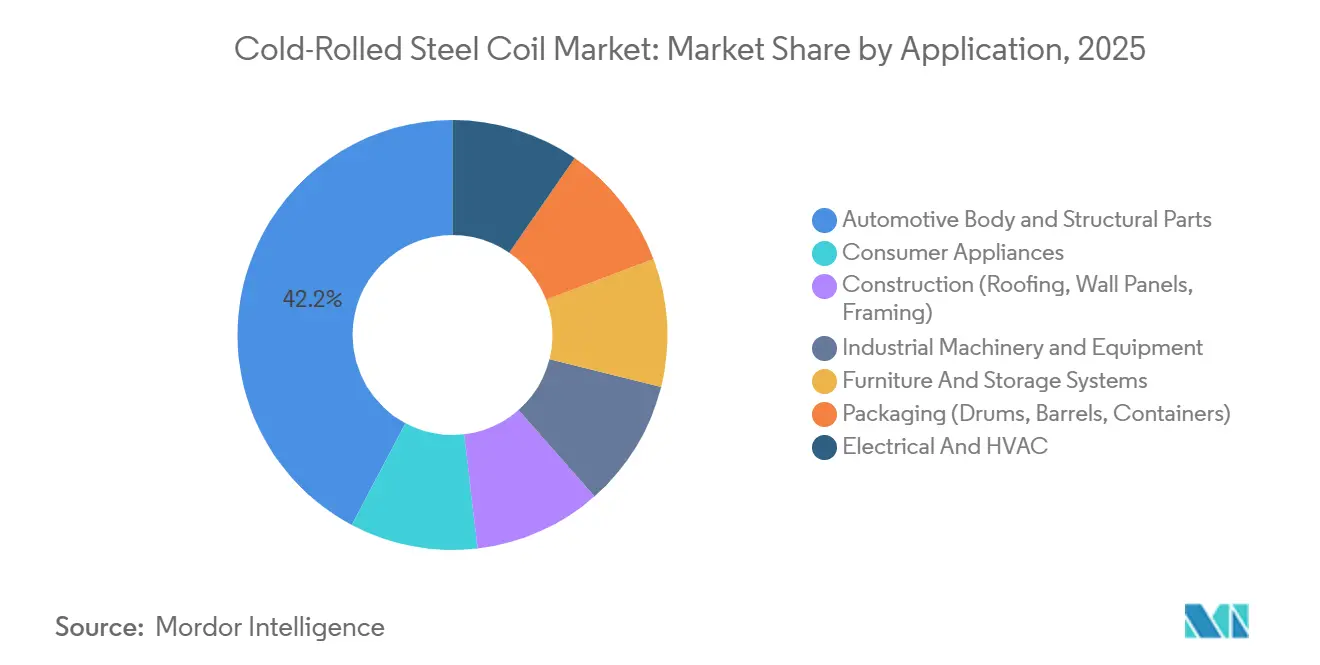

- By application, automotive body and structural parts accounted for 42.23% of the cold-rolled steel coil market size in 2025, and consumer appliances are advancing at 4.11% CAGR to 2031.

- By geography, Asia-Pacific commanded 59.94% of the cold-rolled steel coil market size in 2025 and is projected to expand at 4.36% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cold-Rolled Steel Coil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand from Automotive and Appliance Industries | +1.2% | Global, with concentration in APAC (China, India, ASEAN) and North America | Medium term (2-4 years) |

| Increasing Use in Construction and Infrastructure Projects | +0.9% | North America, Europe, GCC Middle East | Medium term (2-4 years) |

| High-Strength and Surface-Finish Advantages over Hot-Rolled Steel | +0.6% | Global, particularly automotive and appliance segments | Long term (≥ 4 years) |

| Manufacturing Expansion in Emerging Economies | +1.0% | India, Southeast Asia (Vietnam, Indonesia, Thailand), Mexico, Brazil | Long term (≥ 4 years) |

| Cold-Formed Steel Framing in Modular and Data-Center Builds | +0.5% | North America, Europe, select APAC metro regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand From Automotive And Appliance Industries

Battery-electric-vehicle output reached 14 million units in 2025, each platform consuming 15%-20% more AHSS than its internal-combustion predecessor to offset battery mass and meet crash requirements[1]WorldAutoSteel, “AHSS Applications in Electric Vehicles,” worldautosteel.org. SSAB launched EV-optimized AHSS in 2025 with tensile strengths beyond 1,500 MPa, allowing automakers to trim gauge thickness 10%–15% while holding structural integrity. Refrigerator and washing-machine makers in China and India shifted to 0.4-0.5 mm pre-painted coil from traditional 0.6-0.7 mm, reducing material costs up to 12% and cutting energy-label penalties. These twin pulls sustain the cold-rolled steel coil market even where vehicle assembly flattens in mature economies. Mills with tight-tolerance rolling and advanced coating are best placed to capture expanding margins, whereas commodity producers face intensified import competition.

Increasing Use In Construction And Infrastructure Projects

North American building codes adopted cold-formed steel framing for multi-story and seismic applications in 2024-2025, widening addressable demand beyond single-family housing[2]FRAMECAD, “Cold-Formed Steel Framing Code Updates,” framecad.com. Data-center construction in Virginia, Texas, and Ireland alone consumed roughly 1.2 million tons of coil in 2025 for framing, HVAC ducting, and cable trays. GCC countries registered an increase in steel-demand growth in 2025, channeling cold-rolled products into solar-farm roofing and desalination cladding. Modular building in Europe and North America adds 300,000-400,000 tons annually but stays price sensitive, exposing suppliers to substitution if steel premiums exceed 20% of framing cost. Regulatory alignment and labor shortages continue to favor cold-formed solutions, supporting the cold-rolled steel coil market trajectory in non-automotive sectors.

High-Strength And Surface-Finish Advantages Over Hot-Rolled Steel

Automotive outer panels demand surface roughness below 1.5 µm and thickness variation within ±0.02 mm, thresholds achievable only by cold-reduction plus temper rolling. Appliance makers rely on deep-draw capabilities for washing-machine drums and refrigerator liners, where hot-rolled sheet would crack. Electrical-steel producers cold-roll grain-oriented grades to align crystal structure, cutting transformer core loss. Cleveland-Cliffs invested USD 195 million in 2025 to lift GOES capacity by 100,000 tons, targeting grid-modernization projects. These performance moats allow cold-rolled coil to command 25%-35% premiums over hot-rolled sheet, anchoring the profitability of the cold-rolled steel coil market despite raw-material volatility.

Manufacturing Expansion In Emerging Economies

India added 3.5 million tons of cold-rolling capacity in 2024-2025 via Tata Steel, JSW Steel, and AM/NS India, positioning domestic mills to replace imports into Europe and North America. Ternium’s USD 400 million complex in Pesquería, Mexico, inserted 1.5 million tons of automotive-grade supply inside USMCA trade walls. Vietnam crossed 8 million tons of capacity in 2025, exporting to ASEAN construction and automotive customers at costs 10%-15% below Northeast Asian peers. Such build-outs keep the cold-rolled steel coil market globally balanced but heighten regional price swings whenever auto output misses forecasts or trade barriers tighten.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Raw-Material (Iron-Ore and Scrap) Prices | -0.8% | Global, with acute impact on mills without long-term ore contracts | Short term (≤ 2 years) |

| Energy-Intensive Processing and Carbon Dioxide Regulations | -0.6% | Europe (EU CBAM), China (dual-control policies), North America (state-level carbon pricing) | Medium term (2-4 years) |

| Aluminium and Composites Substitution in Lightweighting | -0.4% | North America and Europe automotive, aerospace adjacencies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices

Iron ore traded between USD 90 and USD 130 per ton in 2025, while U.S. scrap ranged from USD 300 to USD 450 per ton, squeezing margins by 200-300 basis points for producers lacking captive resources. Integrated mills such as Tata Steel or Cleveland-Cliffs cushioned swings through internal transfer pricing, whereas merchant mills faced spot-market exposure. EAF operators benefited during scrap troughs but lost cost edge when scrap rose USD 100 above pig-iron parity. This asymmetry will persist into 2027, complicating price negotiations in the cold-rolled steel coil market.

Energy-Intensive Processing And Carbon Regulations

Cold-rolling plus annealing consumes up to 550 kWh per ton, rendering electricity price and carbon levies decisive to profitability. The EU Carbon Border Adjustment Mechanism added EUR 50-80 (USD 54-87) per ton on imports exceeding 1.8 tons CO₂ per ton of steel from January 2026. Chinese dual-control targets curtailed output in high-intensity provinces during peak demand in 2025. Mills' signing of renewable power-purchase agreements locks in electricity 20%-30% above spot, yet secures green-steel premiums from automakers. Plants delaying decarbonization face exclusion from premium contracts, tempering growth in the cold-rolled steel coil market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: AHSS Gains Share As Automakers Pursue Crash Performance And Weight Reduction

Low-carbon steel controlled 46.61% of 2025 volume in the cold-rolled steel coil market, yet Advanced High-Strength Steel (AHSS) is forecast to grow at 4.55% to 2031 as OEMs replace conventional grades to meet fleet-average emission targets.

Stainless cold-rolled coil remains a niche but lucrative slice, especially for food equipment and chemical processing, where Outokumpu and SSAB supply low-carbon variants meeting EU ecodesign norms at 40%-60% margin uplifts. High-carbon and HSLA steels trail overall growth as electrification reduces drivetrain steel content. Mills are unable to produce AHSS or specialty stainless risk margin compression within the cold-rolled steel coil market.

By Application: Automotive Dominates Volume, Consumer Appliances Lead Growth

Automotive body and structural parts used 42.23% of 2025 tonnage, reflecting the sector’s historical dependence on cold-rolled sheet for body-in-white and closures. However, the cold-rolled steel coil market size tied to consumer appliances is projected to grow at a 4.11% CAGR during the forecast period (2026-2031), paced by Indian and Chinese white-goods factories shifting to thinner gauges.

Construction, including roofing, wall panels, and framing, will maintain steady but slower growth as aluminum, fiber-cement, and engineered timber compete in coastal and high-humidity settings. Electrical and HVAC applications enjoy structural tailwinds from grid-modernization, with Cleveland-Cliffs boosting GOES output by 100,000 tons to serve transformer demand. The changing mix nudges mills toward coating and slitting capabilities that suit appliance and electrical sectors, diversifying revenue streams in the cold-rolled steel coil market.

Geography Analysis

Asia-Pacific commanded 59.94% of 2025 volume, expanding at 4.36% through 2031 on the back of Indian and Southeast Asian capacity additions and Chinese appliance exports. India alone commissioned 3.5 million tons of new capacity across Tata Steel, JSW Steel, AM/NS India, and Shyam Metalics during 2024-2025 to satisfy domestic demand and EU-bound exports. Vietnam reached 8 million tons capacity in 2025 with delivered costs 10%-15% under Northeast Asian mills.

North America’s cold-rolled steel coil market’s growth is propelled by EAF investments such as Nucor’s 3-million-ton West Virginia mill and Hyundai Steel’s USD 5.8 billion U.S. greenfield EAF announced in March 2026. Mexico’s 1.5 million-ton Pesquería complex positions the country as a regional hub under USMCA rules.

Europe faces slower growth given stagnant auto output and high energy costs, yet CBAM incentives are triggering capacity reshoring to Poland, Spain, and Italy. South America’s growth is led by Brazilian and Argentine automotive recovery, while the Middle East and Africa will advance on Saudi and UAE infrastructure pipelines, including EMSTEEL’s AED 625 million expansion targeting GCC HVAC and construction buyers.

Competitive Landscape

The cold-rolled steel coil market is moderately fragmented. Technology upgrades focus on AI-enabled gauge control, hydrogen annealing to slash carbon intensity, and inline coating to shorten cycle times. Producers hitting thickness tolerances tighter than ±0.015 mm (millimeter) and surface roughness under 1.2 µm (micrometer) secure automotive contracts, while laggards compete on price within construction and packaging.

Cold-Rolled Steel Coil Industry Leaders

ArcelorMittal

Nippon Steel Corporation

POSCO

Tata Steel

China Baowu Steel Group Corporation Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nippon Steel acquired U.S. Steel for USD 14.9 billion, strengthening its production capabilities and market position in North America's cold-rolled steel coil segment. The acquisition established Nippon Steel as a significant player in the global steel market.

- November 2024: JSW Steel and POSCO invested USD 7.73 billion in a new steel plant in Odisha, India, to increase the production of hot and cold-rolled steel coil. The plant's initial capacity of 5 million tons per year will expand to 18 million tons within three years. The investment responds to India's growing steel demand, driven by economic growth and infrastructure development.

Global Cold-Rolled Steel Coil Market Report Scope

Cold-rolled steel coil is a high-precision, superior-surface finish material produced by processing hot-rolled coils at room temperature, increasing strength and hardness. It typically features tighter dimensional tolerances, improved flatness, and a polished finish suitable for plating, essential for automotive, appliance, and furniture manufacturing.

The cold-rolled steel coil market is segmented by grade, application, and geography. By grade, the market is segmented into low-carbon steel, high-carbon steel, high-strength low-alloy (HSLA) steel, advanced high-strength steel (AHSS), and stainless steel. By application, the market is segmented into automotive body and structural parts, consumer appliances, construction (roofing, wall panels, and framing), industrial machinery and equipment, furniture and storage systems, packaging (drums, barrels, and containers), and electrical and HVAC. The report also covers the market size and forecasts for cold-rolled steel coil in 17 countries across major regions. The market sizes and forecasts are provided in terms of volume (tons).

| Low-Carbon Steel |

| High-Carbon Steel |

| High-Strength Low-Alloy (HSLA) Steel |

| Advanced High-Strength Steel (AHSS) |

| Stainless Steel |

| Automotive Body and Structural Parts |

| Consumer Appliances |

| Construction (Roofing, Wall Panels, Framing) |

| Industrial Machinery and Equipment |

| Furniture And Storage Systems |

| Packaging (Drums, Barrels, Containers) |

| Electrical And HVAC |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Low-Carbon Steel | |

| High-Carbon Steel | ||

| High-Strength Low-Alloy (HSLA) Steel | ||

| Advanced High-Strength Steel (AHSS) | ||

| Stainless Steel | ||

| By Application | Automotive Body and Structural Parts | |

| Consumer Appliances | ||

| Construction (Roofing, Wall Panels, Framing) | ||

| Industrial Machinery and Equipment | ||

| Furniture And Storage Systems | ||

| Packaging (Drums, Barrels, Containers) | ||

| Electrical And HVAC | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What was the cold-rolled steel coil market size in 2025 and how fast is it growing?

The Cold-Rolled Steel Coil Market size is expected to increase from 137.89 Million tons in 2025 to 143.24 Million tons in 2026 and reach 173.27 Million tons by 2031, growing at a CAGR of 3.88% over 2026-2031.

Which region leads global demand?

Asia-Pacific held 59.94% of 2025 volume and will keep expanding fastest through capacity additions in India and Southeast Asia.

Why is AHSS gaining share in coil consumption?

Automakers adopt AHSS to cut vehicle weight while meeting crash standards, driving a 4.55% CAGR for the forecast period (2026-2031) for AHSS through 2031.

What investments are reshaping North American supply?

Nucor’s new West Virginia sheet mill and Hyundai Steel’s planned USD 5.8 billion U.S. EAF plant will add 4.5 million tons of automotive-grade capacity by 2030.

Page last updated on: