Metal Replacement Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

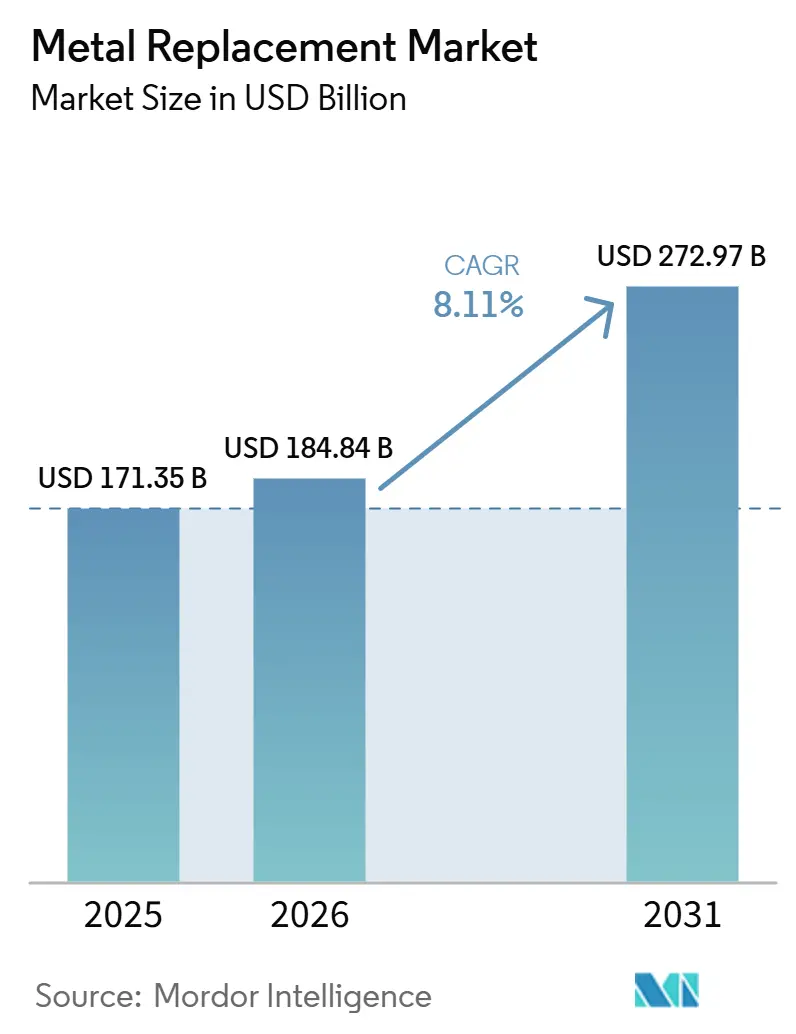

| Market Size (2026) | USD 184.84 Billion |

| Market Size (2031) | USD 272.97 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Replacement Market Analysis by Mordor Intelligence

The Metal Replacement Market size is projected to be USD 171.35 billion in 2025, USD 184.84 billion in 2026, and reach USD 272.97 billion by 2031, growing at a CAGR of 8.11% from 2026 to 2031. Lower vehicle-emission limits, accelerated electric-vehicle (EV) adoption, and airline efforts to reduce fuel consumption are intensifying the demand for lighter, corrosion-resistant alternatives to steel and aluminum. Engineering plastics currently dominate in terms of volume, but rapid capacity expansions in carbon- and glass-fiber composites are narrowing their cost gap and enabling broader adoption in mid-tier passenger vehicles and next-generation aircraft. Regulatory authorities in the European Union, the United States, and China are implementing vehicle weight targets that necessitate material substitutions, while topology-optimization software is significantly reducing design cycles, allowing engineers to validate polymer solutions early in the development process. Additionally, petrochemical producers in the Middle-East are establishing fully integrated composite parks, offering 15–20% cost savings and attracting global Tier-1 suppliers into joint ventures.

Key Report Takeaways

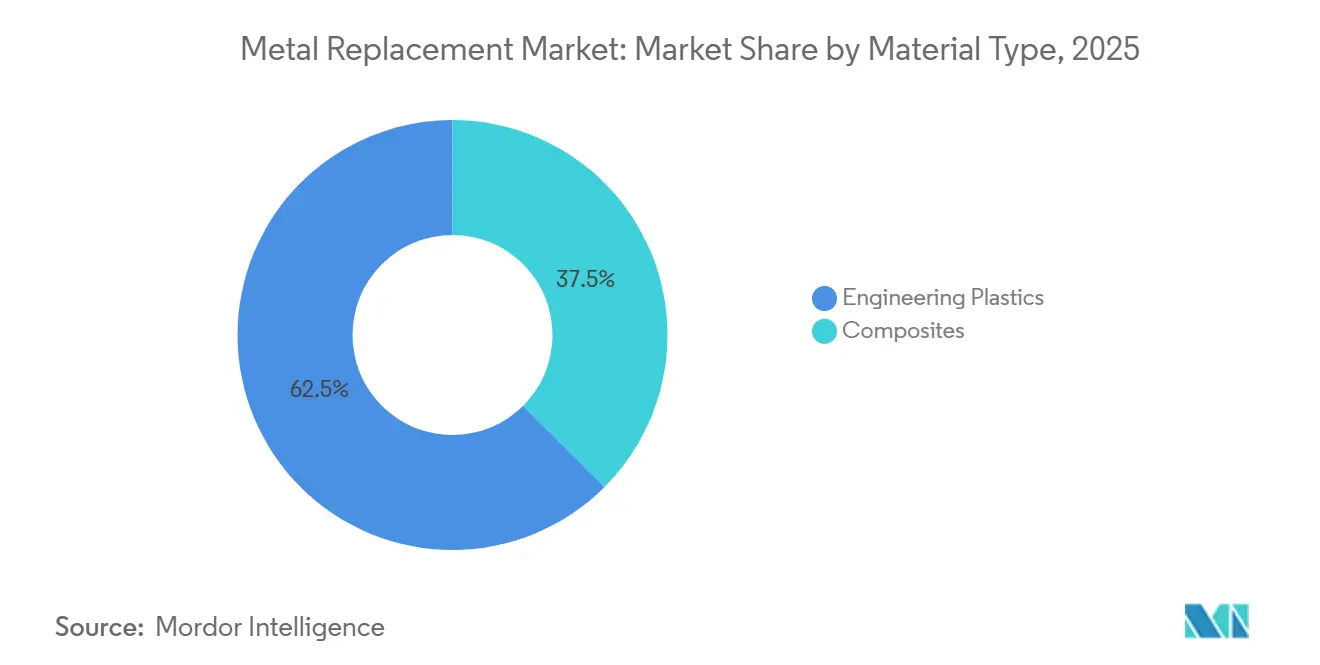

- By material type, engineering plastics led with 62.50% of the metal replacement market share in 2025, whereas composites are poised to register the fastest 9.10% CAGR through 2031.

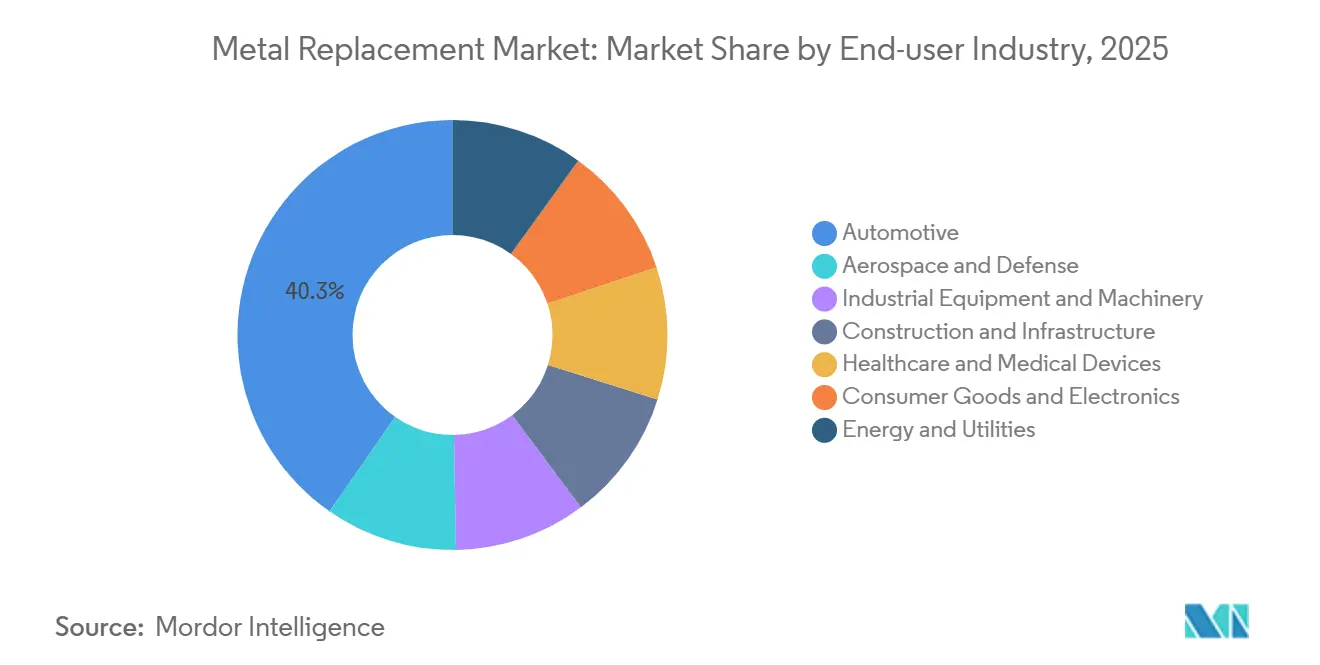

- By end-user industry, automotive retained 40.30% of the metal replacement market share in 2025, yet healthcare and medical devices represent the fastest-growing segment at a projected 9.12% CAGR through 2031.

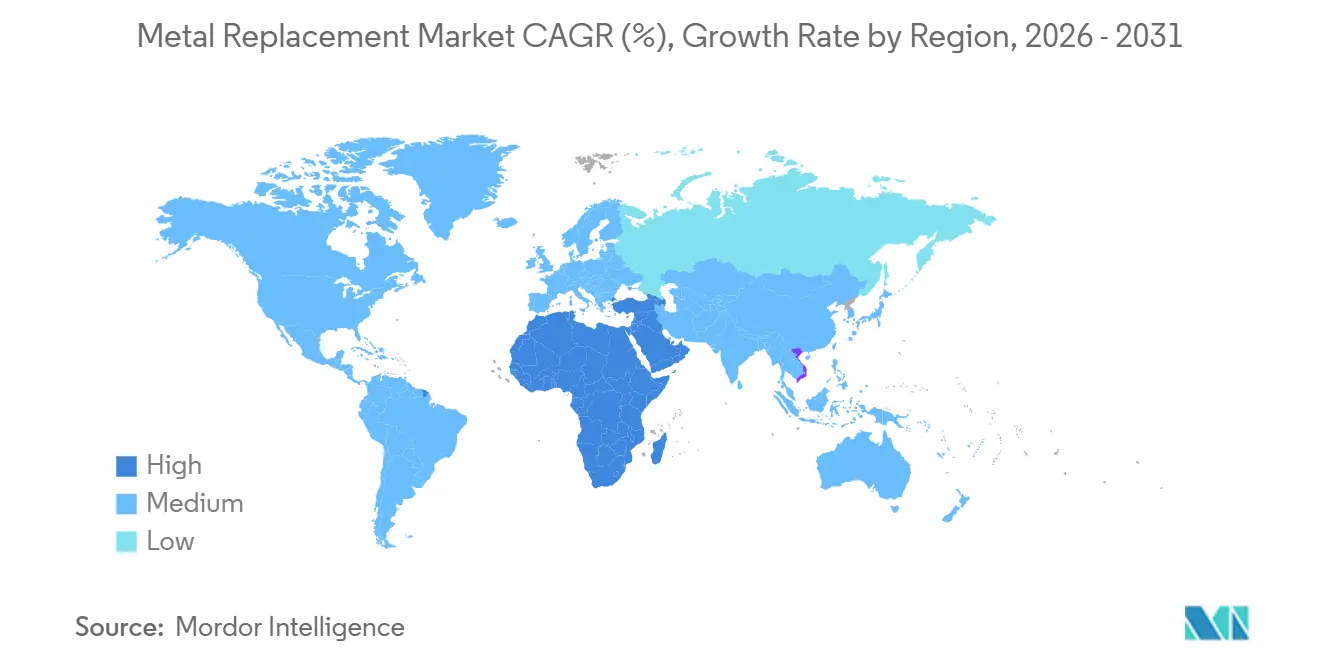

- By geography, Asia-Pacific generated 47.30% of the metal replacement market share in 2025, while the Middle-East and Africa are forecast to advance at the strongest 9.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Metal Replacement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in automotive and aerospace lightweighting trends | +2.1% | Global, with concentration in North America, Europe, and China | Medium term (2-4 years) |

| Increasing adoption of engineering plastics and composites | +1.8% | Global, led by Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Rapid expansion of electric-vehicle component manufacturing | +1.6% | China, Europe, North America; spillover to India and ASEAN | Short term (≤ 2 years) |

| Regulatory push for transportation lightweighting | +1.3% | Europe (EU CO₂ standards), North America (CAFE), China (NEV credits) | Medium term (2-4 years) |

| AI-driven topology optimization enhancing polymer part design | +0.9% | North America and Europe early adopters; Asia-Pacific scale deployment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in Automotive and Aerospace Lightweighting Trends

Battery-electric vehicles need to reduce 200–300 kg of chassis weight to offset the mass of lithium-ion batteries, leading automakers to replace underbody steel with glass-fiber polypropylene shields and carbon-fiber-reinforced thermoplastic battery enclosures that meet crash-worthiness standards while improving energy efficiency. Airbus validated a fully recyclable thermoplastic fuselage panel in 2025, which reduces manufacturing energy consumption by 40% compared to thermosets and allows for localized repairs, potentially lowering airline maintenance costs by 15–20% over a 25-year lifespan. Global wind-turbine capacity additions reached 117 GW in 2024, with composite blades now accounting for over 90% of rotor mass and reducing offshore foundation steel requirements by up to 40%. Hybrid carbon-glass designs approved by Sandia National Laboratories demonstrated a 44.7% increase in tensile strength, enabling rotor diameters to expand from 150 m to 180 m without proportional mass increases[1]Sandia National Laboratories, “Hybrid Carbon-Glass Blade Tests,” sandia.gov. Thermoplastic blades prototyped by Akelite in 2025 achieved an additional 7.3% weight reduction and full recyclability once standards are established.

Increasing Adoption of Engineering Plastics and Composites

Bio-based polyamide 11 captured 12% of the automotive under-hood market in 2025 after Arkema increased Rilsan PA11 production by 20% to meet EV cooling-line demand. Polyphenylene sulfide now holds 8% of the industrial pump housing market due to its acid resistance, which eliminates downtime previously costing operators USD 50,000–100,000 per incident. PEEK implants, despite being priced at a 15% premium over polycarbonate, have reduced spinal-fusion revision rates by 30%, saving USD 8,000–12,000 per patient. Carbon-fiber-reinforced PEEK screws demonstrated 25% greater pull-out strength than titanium in cadaveric tests, earning three new U.S. FDA clearances in 2025. Polyplastics’ cellulose-fiber-blended PLASTRON LFT, launched in 2025, reduced the product carbon footprint by 30% while maintaining the impact strength required by global OEMs.

Rapid Expansion of Electric-Vehicle Component Manufacturing

Battery enclosures contribute 15–20 kg of mass per EV, with carbon-fiber-reinforced polyamide achieving 40% weight savings while meeting IP67 ingress and 1.5-m drop standards under UN ECE R100. Tesla’s cell-to-pack structure integrates the housing as a stressed member, requiring composite laminates capable of absorbing 30 kJ per kg of crash energy. Intumescent polyphenylene sulfide barriers delay thermal-runaway propagation by up to 8 minutes, helping five EV models achieve 5-star Euro NCAP ratings in 2025. China’s MIIT issued guidelines in 2025 mandating 8% recycled carbon fiber in all new-energy vehicles by 2028. Mitsui Chemicals’ 10,500 tons per year long-glass-fiber polypropylene plant in Jiangsu province addresses cost-sensitive applications such as battery trays.

Regulatory Push for Transportation Lightweighting

The European Union will tighten passenger car fleet limits to 49.5 g CO₂/km by 2030, with non-compliance penalties of EUR 95 per excess gram, potentially exceeding EUR 800 million annually unless 100–150 kg of metal is replaced. NHTSA’s 2027–2032 CAFE standards require U.S. light-duty fleets to achieve an average of 58 mpg equivalent, prompting Detroit automakers to adopt glass-fiber polyamide door inners. ICAO’s global aviation carbon scheme incentivizes airlines to retrofit wide-body interiors with 500–700 kg of carbon-fiber panels, reducing fuel consumption by 1.5–2.0%. China’s NEV credit system doubled credits in 2025 for 500-km-range vehicles, achievable only through aggressive lightweighting that combines aluminum frames with composite body panels[2]Ministry of Industry and Information Technology of China, “Draft NEV Recycled-Carbon-Fiber Guideline,” miit.gov.cn. ACI 440.11-22, published in 2024, became the first U.S. code to approve glass-fiber-reinforced polymer rebar for structural concrete applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced polymers and composites | -1.4% | Global, most acute in price-sensitive Asia-Pacific and South America markets | Medium term (2-4 years) |

| Performance limits in high-stress/high-temperature uses | -0.8% | Global, particularly in aerospace, industrial equipment, and energy sectors | Long term (≥ 4 years) |

| Recycling and end-of-life challenges for multi-material parts | -0.6% | Europe and North America regulatory pressure; Asia-Pacific infrastructure gaps | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Polymers and Composites

PEEK was priced at USD 60–80 per kg in 2025, eight to twelve times the cost of aluminum die-cast alloys, limiting its use in cost-sensitive applications such as appliances. Aerospace-grade carbon-fiber prepreg reached USD 150 per kg after a 12% increase in polyacrylonitrile feedstock prices, delaying composite adoption in secondary aircraft parts. Polyphenylene sulfide compounding requires USD 8–12 million twin-screw extruders, restricting supply to fewer than 20 global specialists. Flax and hemp composites reduce reinforcement costs by 30–40%, but their 8% moisture absorption causes dimensional drift, excluding them from precision applications like door modules. Recycled carbon fiber, priced at USD 15–25 per kg, has 20–30% lower tensile strength, limiting its use to non-structural products such as laptop shells.

Performance Limits in High-Stress/High-Temperature Uses

Engineering plastics have a maximum continuous-service temperature of 310 °C for PEEK, far below the 600 °C required for turbine hot sections, which still rely on nickel super-alloys. Glass-fiber composites creep under loads exceeding 40% of their tensile strength, making them unsuitable for heavy-duty crane gears where steel handles 70–80% loading without deformation. Thermal cycling between −40 °C and +80 °C over 50,000 cycles can cause micro-cracks in carbon-fiber laminates, leading Boeing to revert to aluminum wing-root fittings in certain programs. Outdoor UV exposure reduces the flexural strength of uncoated polymer matrices by 15–25% after 5,000 hours, with protective coatings adding USD 5–10 per m² and complicating recycling. Thermoplastic composites lose 40–50% of their impact resistance at −30 °C, preventing their use in Arctic oil pipelines where low-temperature steel remains ductile.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Composites Gain on Cost-Performance Convergence

Engineering plastics accounted for 62.50% of the projected 2025 revenue, driven by the dominance of polyamide in under-hood components and the strength of polycarbonate in electronics housings. Composites are anticipated to grow at a 9.10% CAGR through 2031, as Asian carbon-fiber production reduces the cost gap to USD 20–25 per kg. The susceptibility of polycarbonate to hydrolysis is encouraging 5G antenna manufacturers to shift toward polyphenylene sulfide. ABS remains a cost-effective option for appliance shells at USD 3 per kg, but its 80 °C softening point limits its use to non-thermal applications. High-performance materials like PEEK, PEI, and PPS continue to reinforce their niche roles in medical and aerospace applications.

Glass-fiber-reinforced plastics, priced at USD 1.50–2.00 per kg, are widely used in automotive underbody shields and turbine housings. Carbon-fiber-reinforced systems remain essential for aerospace skins and premium EV body structures, despite their higher fiber cost of USD 25–40 per kg. Natural-fiber composites are primarily utilized in European door panels, valued for their lower embedded carbon. Toray has expanded French carbon-fiber production, while Hexcel’s rapid-cure prepreg reduces autoclave cycles to two hours, helping thermosets maintain competitiveness against thermoplastics.

By End-user Industry: Healthcare Outpaces Automotive in Growth

The automotive industry is projected to dominate with 40.30% of 2025 revenue, driven by the adoption of EV battery trays, underbody panels, and adhesives replacing metal parts. However, the healthcare and medical devices industry is expected to grow at the fastest rate, with a 9.12% CAGR through 2031. Orthopedic implant manufacturers are transitioning from titanium to radiolucent PEEK, which has reduced spinal fusion revision rates by 25–30% and is expected to expand the metal replacement market size for implants to an estimated USD 520 million in 2025. Aerospace and defense demand is supported by the FAA's approval of the first thermoplastic composite fuselage panel in 2024, which reduced lay-up time by 80%.

In industrial machinery, polymer gears in robotics are reducing plant noise by 10 dB and eliminating lubrication costs of USD 10,000 annually. Construction applications are advancing due to ACI 440.11-22, which removed regulatory barriers for GFRP rebar. Energy installations are supported by wind-turbine growth, requiring 15–20 tons of composites per MW.

Geography Analysis

Asia-Pacific is expected to contribute 47.30% of 2025 revenue, driven by China’s 6–8 Mt engineering plastics capacity and Japan’s leadership in carbon-fiber precursor production. China hosts Mitsui Chemicals’ long-glass-fiber polypropylene plant for EV battery trays, while Japan’s Toray, Teijin, and Mitsubishi Chemical strengthen their aerospace-grade feedstock specialization. India is attracting new polymer investments as manufacturers diversify from China, and South Korea is piloting carbon-fiber recycling lines to meet China’s 2028 mandate for 8% recycled fiber. ASEAN nations are gaining market share due to tariff concessions under RCEP and labor costs 30–40% lower than coastal China.

In North America, aerospace composites, Detroit's lightweighting initiatives, and wind-energy installations are supported by the U.S. Inflation Reduction Act’s 30% manufacturing tax credit. BASF has increased polyisobutylene output by 60% at Ludwigshafen to meet EV battery-seal demand, while Canada’s hydropower resources have attracted a 3,000-ton PAN-fiber plant with a 40% lower carbon footprint compared to coal-powered Chinese facilities. Mexico benefits from USMCA content rules favoring near-shoring of compounded resins.

Europe faces challenges from high energy costs but benefits from stringent 2030 CO₂ targets, driving steel-to-polymer substitutions averaging 100 kg per passenger car. The Syensqo and Arkema HAICoPAS consortium secured EASA approval for a PEKK/carbon-fiber fuselage panel, reducing lay-up time from 8 hours to 45 minutes and enabling closed-loop repair pathways. The UK emphasizes recycling, with Hexcel and Lavoisier converting aerospace scrap into Carbonium reclaimed fabric at 40% lower cost than virgin materials. Nordic builders are adopting flax-fiber panels with half the embodied carbon of glass fiber. The Middle-East and Africa are forecast to achieve the highest CAGR of 9.07%, supported by Saudi Aramco and Syensqo's USD 30 billion investment in a vertically integrated compositing park.

Competitive Landscape

The top five suppliers include BASF, DuPont, SABIC, Toray, and Celanese. The metal replacement market is moderately concentrated. Chemical companies are streamlining the value chain by acquiring converters. Syensqo's Saudi joint venture integrates resin, fiber, and tape-laying processes, targeting 15–20% cost savings. Arkema's bio-based Rilsan PA11 holds 12% of under-hood applications, offering insulation from petroleum price volatility. Hexcel's AI-optimized lattice brackets, co-developed with automakers, deliver 30–50% mass savings, outperforming traditional metal stampers without requiring significant retooling investments.

Additive manufacturing companies like Caracol and CEAD are disrupting the market by feeding carbon-fiber pellets at 30–50 kg per hour, significantly reducing raw material costs compared to filament printers and enabling the production of one-piece boat hulls up to 10 meters long. Patent filings in thermoplastic composites increased by 40% year-over-year in 2024–2025, led by Hexcel, Arkema, and Toray, reflecting a shift toward faster-curing, fully recyclable matrices. SABIC has allocated USD 3.5–4.0 billion for specialty polymer expansions focused on EV thermal management and 5G devices, where liquid-crystal polymers command a 30% premium. Certification processes remain anchored in ISO 527 and ASTM D3039 standards, with suppliers investing USD 5–10 million annually in accredited labs to expedite aerospace and automotive approvals.

Metal Replacement Industry Leaders

SABIC

BASF

DuPont

Celanese Corporation

TORAY INDUSTRIES INC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: BASF introduced a portfolio of polyamide (PA) and polyphthalamide (PPA) blends for advanced metal replacement in structural parts. These blends offer superior and consistent mechanical properties compared to PA66. Ultramid T7000 exceeds PA66 in stiffness and strength, both in dry and humid conditions, with reduced water absorption ensuring excellent dimensional stability.

- October 2024: SABIC advanced metal replacement in transportation and medical devices with innovative materials. Their LNP ELCRES FST copolymer resins for train interiors provide design flexibility, weight reduction, recyclability, and compliance with fire safety standards. SABIC also showcased 3D-printed rail parts using LNP THERMOCOMP compounds for faster replacements.

Global Metal Replacement Market Report Scope

Metal replacement involves substituting traditional metal components with high-performance polymers, composites, or ceramics to enhance efficiency, reduce weight, and lower production costs. In contemporary manufacturing, this process typically requires re-engineering parts to utilize the unique properties of advanced materials, such as corrosion resistance and self-lubrication, rather than a direct "one-to-one" replacement.

The Metal Replacement Market is segmented into material type, end-user industry, and geography. By material type, the market is segmented into engineering plastics (polyamide (PA), polycarbonate (PC), acrylonitrile-butadiene-styrene (ABS), polyethylene terephthalate (PET), polyphenylene sulfide (PPS), and high-performance polymers (PEEK, PEI, etc.), and composites (glass fibre-reinforced plastics (GFRP), carbon fibre-reinforced plastics (CFRP), and natural-fibre composites). By end-user industry, the market is segmented into automotive, aerospace and defense, industrial equipment and machinery, construction and infrastructure, healthcare and medical devices, consumer goods and electronics, and energy and utilities. The report also covers the market size and forecasts for metal replacement in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Engineering Plastics | Polyamide (PA) |

| Polycarbonate (PC) | |

| Acrylonitrile-Butadiene-Styrene (ABS) | |

| Polyethylene Terephthalate (PET) | |

| Polyphenylene Sulfide (PPS) | |

| High-Performance Polymers (PEEK, PEI, etc.) | |

| Composites | Glass Fibre-Reinforced Plastics (GFRP) |

| Carbon Fibre-Reinforced Plastics (CFRP) | |

| Natural-Fibre Composites |

| Automotive |

| Aerospace and Defense |

| Industrial Equipment and Machinery |

| Construction and Infrastructure |

| Healthcare and Medical Devices |

| Consumer Goods and Electronics |

| Energy and Utilities |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Engineering Plastics | Polyamide (PA) |

| Polycarbonate (PC) | ||

| Acrylonitrile-Butadiene-Styrene (ABS) | ||

| Polyethylene Terephthalate (PET) | ||

| Polyphenylene Sulfide (PPS) | ||

| High-Performance Polymers (PEEK, PEI, etc.) | ||

| Composites | Glass Fibre-Reinforced Plastics (GFRP) | |

| Carbon Fibre-Reinforced Plastics (CFRP) | ||

| Natural-Fibre Composites | ||

| By End-user Industry | Automotive | |

| Aerospace and Defense | ||

| Industrial Equipment and Machinery | ||

| Construction and Infrastructure | ||

| Healthcare and Medical Devices | ||

| Consumer Goods and Electronics | ||

| Energy and Utilities | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the metal replacement market?

The metal replacement market size reached USD 184.84 billion in 2026 and is projected to hit USD 272.97 billion by 2031.

Which material type leads revenues today?

Engineering plastics hold 62.50% of 2025 revenue, led by polyamide and polycarbonate applications.

Which end-user industry will expand fastest through 2031?

Healthcare and medical devices are forecast to post the strongest 9.12% CAGR through 2031 as PEEK implants replace titanium and stainless steel.

Which region is expected to grow the quickest through 2031?

The Middle-East and Africa are set to advance at a 9.07% CAGR through 2031 as Saudi and UAE investments create vertically integrated composite hubs.

Page last updated on: