Metal Foam Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

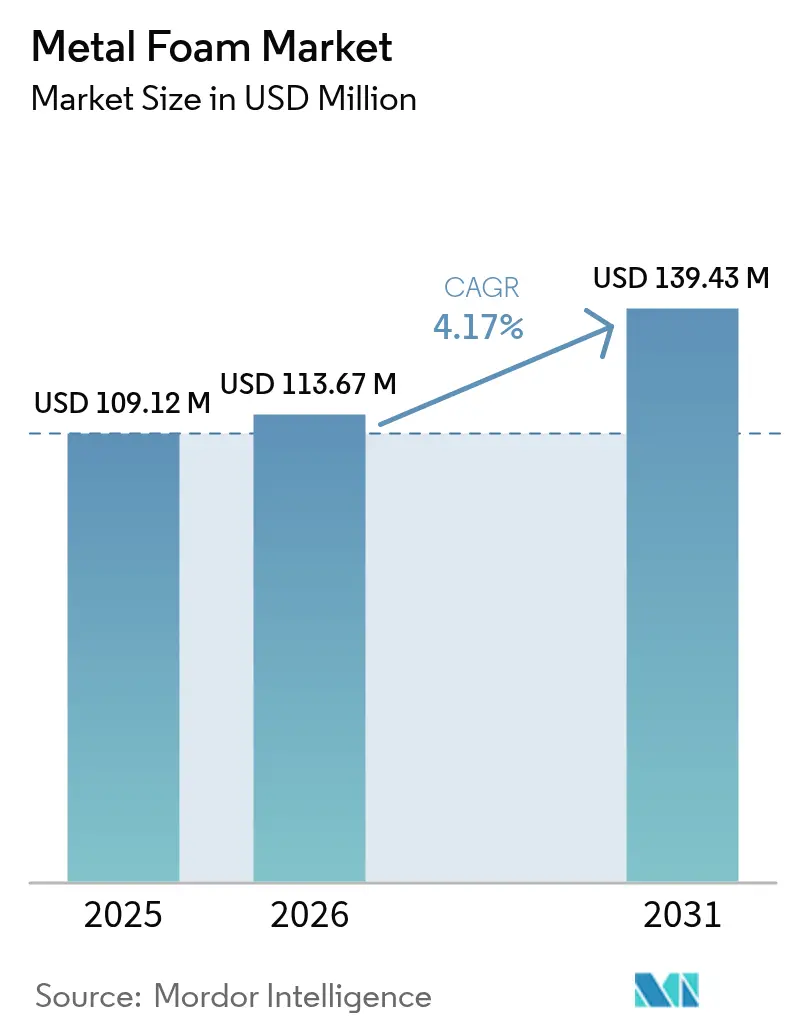

| Market Size (2026) | USD 113.67 Million |

| Market Size (2031) | USD 139.43 Million |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Foam Market Analysis by Mordor Intelligence

The Metal Foam Market size was valued at USD 109.12 million in 2025 and estimated to grow from USD 113.67 million in 2026 to reach USD 139.43 million by 2031, at a CAGR of 4.17% during the forecast period (2026-2031). Steady demand from automotive lightweighting, aerospace energy absorption, and battery-pack thermal management underpins this expansion, while emerging use cases in data-center cooling and hydrogen fuel cells broaden the addressable base for suppliers. Open-cell foams dominate thermal management solutions because the interconnected porosity boosts convective heat transfer, whereas closed-cell foams continue to underpin crash-energy absorbers and buoyancy components. Regionally, Asia-Pacific anchors the metal foam market owing to its dense automotive and electronics supply chains and its rapid scale-up of secondary aluminum smelting capacity. Manufacturers are shifting toward powder-metallurgy routes for cost-effective volume production, yet additive manufacturing is gaining ground as 3-D printers enable intricate lattices tuned to application-specific porosity, strength, and weight targets.

Key Report Takeaways

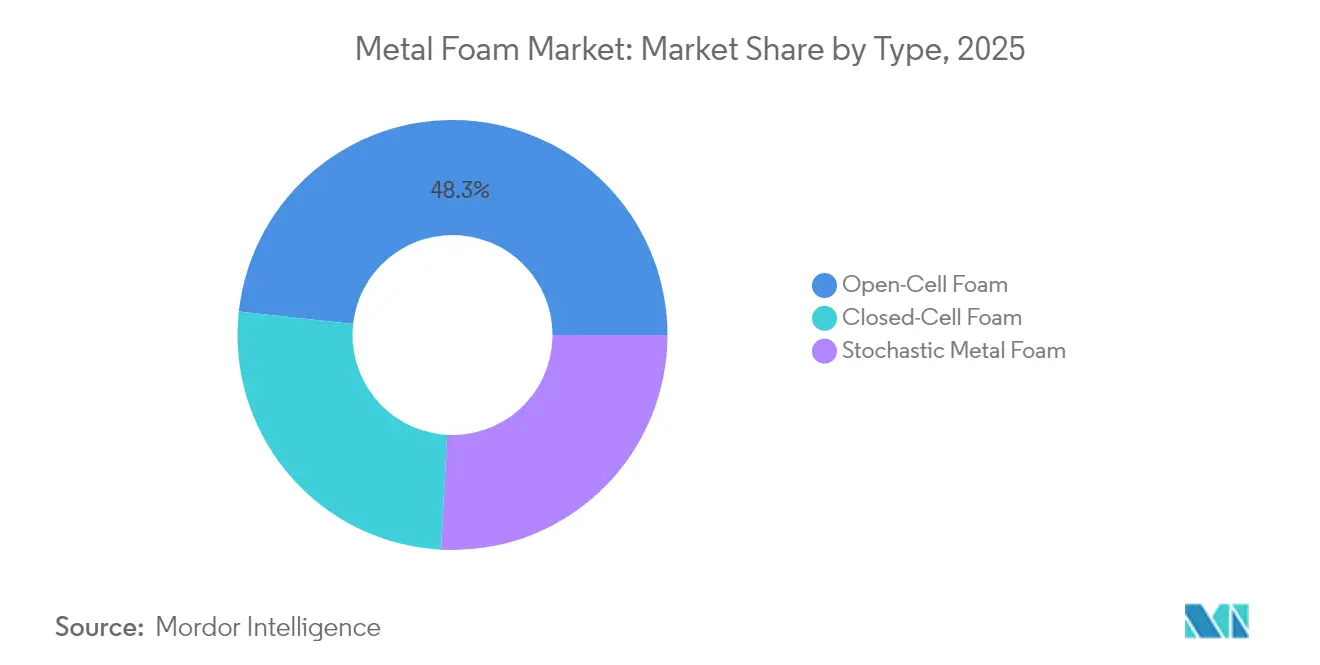

- By type, open-cell foam commanded 48.25% of the metal foam market share in 2025; the same segment is projected to expand at a 4.92% CAGR through 2031.

- By material, aluminium led with 56.55% share of the metal foam market size in 2025, and it retains the fastest forecast growth at 4.97% CAGR.

- By manufacturing process, powder metallurgy held 54.80% revenue share in 2025, while additive manufacturing records the highest projected CAGR at 4.74% through 2031.

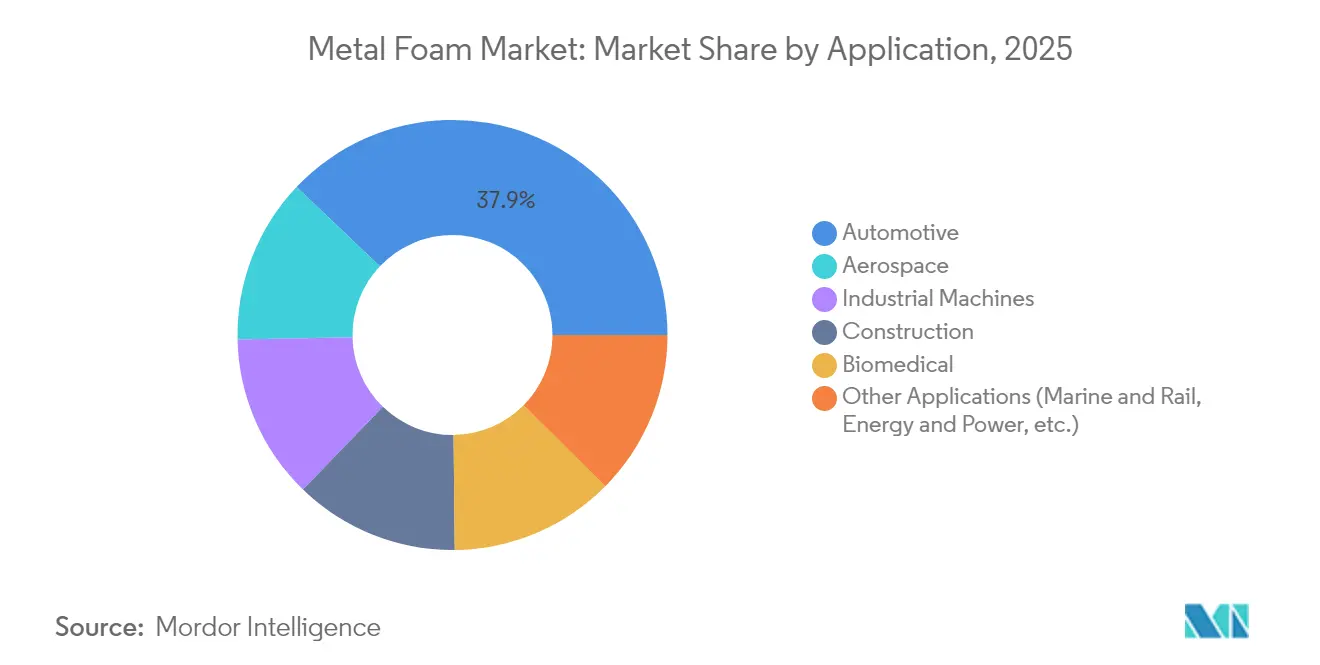

- By application, automotive accounted for a 37.92% share of the metal foam market size in 2025; other applications, notably hydrogen fuel cells and biomedical implants, are advancing at a 5.07% CAGR to 2031.

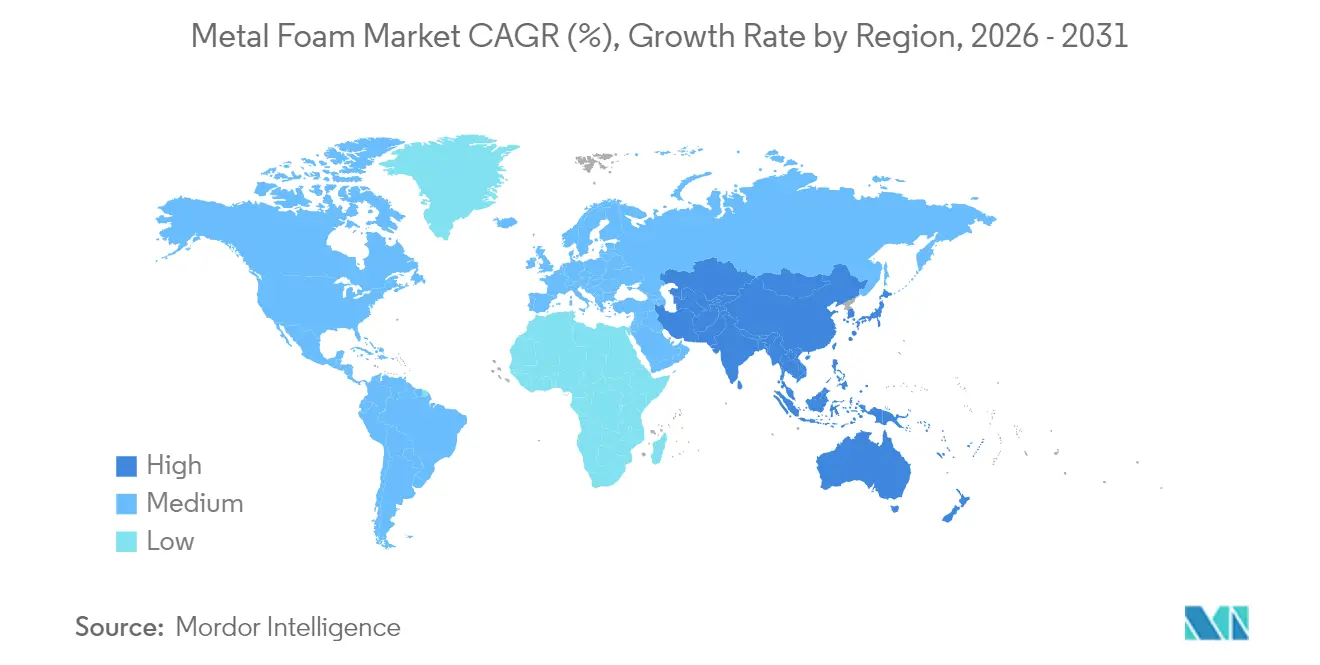

- By geography, Asia-Pacific dominated with 44.10% metal foam market share in 2025 and is forecast to post a 5.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metal Foam Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging lightweighting demand in EV and ICE passenger vehicles | +1.2% | Global, with APAC and North America leading adoption | Medium term (2-4 years) |

| Intensifying aerospace focus on crash and fire-safety energy absorbers | +0.8% | North America and EU, with spillover to APAC | Long term (≥ 4 years) |

| Rapid adoption of metal-foam heat spreaders in battery thermal packs | +1.0% | APAC core, spill-over to North America and EU | Short term (≤ 2 years) |

| Novel hydrogen-fuel-cell heat-exchanger designs using nickel foams | +0.5% | EU and North America, early adoption in Japan | Long term (≥ 4 years) |

| Custom 3-D printed bio-implant foams accelerating orthopaedic uptake | +0.4% | North America and EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Lightweighting Demand in EV and ICE Passenger Vehicles

Global automakers continue to remove vehicle mass in pursuit of range extension and fuel-economy compliance, and cellular metals have become integral to this strategy. Tesla integrates aluminium foam ribs inside Model Y battery enclosures, trimming weight while bolstering side-impact resistance[1]U.S. Department of Energy, “Chapter 05 – Materials Technology,” energy.gov. The European Union’s CO₂ fleet-average rules and China’s dual-credit system likewise push manufacturers toward lighter architectures that the metal foam market can satisfy. Supply-chain familiarity with aluminium alloys eases qualification, enabling faster model-year adoption cycles. In parallel, steelmakers are experimenting with composite steel-foam laminates for bumper beams, widening material options beyond aluminium. As automakers electrify entry-level nameplates, material substitution moves downstream, enlarging the total available market for open-cell and closed-cell foams.

Intensifying Aerospace Focus on Crash and Fire-Safety Energy Absorbers

Regulators now require cabin and cargo structures that withstand longer-duration pool-fire scenarios, and composite metal foams outperform stainless-steel panels by maintaining protected-side temperatures below 379 °C after 100 minutes at 825 °C. Aircraft makers therefore specify cellular aluminum and titanium inserts for vulnerable belly skins and landing-gear fairings. Military rotor-craft programs prioritize ballistic-limit enhancement without payload penalties, driving niche demand for steel-foam armor. Additive platforms let suppliers print topology-optimized lattice cores into sandwich panels, compressing part counts and maintenance time. Because qualifying new materials in aviation is capital-intensive, early entrants gain durable order visibility, reinforcing revenue resilience in the metal foam market.

Rapid Adoption of Metal-Foam Heat Spreaders in Battery Thermal Packs

Open-cell copper and aluminium foams impregnated with phase-change materials cool cylindrical and pouch cells, curbing thermal runaway. Laboratory studies show a 14% mean temperature drop at air flows of 2 m s-1 compared with solid-plate heat sinks. Asia-Pacific gigafactories have begun inserting foam bricks between module rows, a design that decouples aging cells and simplifies over-temperature detection. Data-center operators mirror this approach, positioning nickel foams behind high-power CPUs to dissipate hotspots. Combined, these deployments make thermal management the fastest-scaling use case inside the metal foam market during the next two years.

Novel Hydrogen-Fuel-Cell Heat-Exchanger Designs Using Nickel Foams

To improve proton exchange membrane durability at elevated current densities, European automakers now trial nickel-foam heat exchangers that display polarization voltages around 10 mV at 40 mA cm-2, far below conventional plates. The porous skeleton retains mechanical integrity in acidic environments while providing a high surface area for humidification. Infrastructure build-out in France and Germany, supported by public-private hydrogen hubs, creates early commercial demand for nickel foams. Downstream, petrochemical sites evaluate nickel-foam recuperators for high-temperature steam reforming, potentially opening an industrial channel for suppliers once transport volumes scale.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High investment required for scalable melt-foaming and post-machining | -1.1% | Global, particularly affecting SMEs in emerging markets | Medium term (2-4 years) |

| Limited industrial-grade volume availability outside aluminium | -0.7% | Global, with acute shortages in specialized applications | Short term (≤ 2 years) |

| Recycling complexity of multi-phase composite metal foams | -0.3% | EU and North America, driven by circular economy regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Investment Required for Scalable Melt-Foaming and Post-Machining

Industrial melt-foaming furnaces rely on controlled gas injection, precise temperature staging, and rapid quenching, a capital stack that can exceed USD 4 million for a mid-size line[2]U.S. Department of Homeland Security, “Threat of Limited U.S. Access to Critical Raw Materials,” dhs.gov. Small and mid-size enterprises find such outlays prohibitive, curbing supplier diversity in the metal foam industry. Post-process CNC trimming and surface sealing add incremental cost layers because the cellular lattice is prone to burrs and requires tight tolerances in aerospace fixtures. Although additive manufacturing bypasses some tooling expenses, laser-powder-bed systems carry their own high CAPEX and maintain strict powder-conditioning protocols. Government grants in North America and tax credits in the EU soften the burden, but financing gaps persist in emerging markets where local banks label advanced materials as high-risk.

Recycling Complexity of Multi-Phase Composite Metal Foams

Composite foams that combine aluminium matrices with ceramic or polymer fillers outperform monolithic alternatives yet create end-of-life disassembly challenges. Mechanical shredding contaminates melt streams with incombustibles, contravening EU recycling thresholds under the Circular Economy Action. Pyro-metallurgical routes can recover metal fractions, but energy intensity erodes cost savings. As automakers commit to closed-loop supply chains, recyclability premiums may favor single-phase foams unless better separation processes emerge. In North America, research and development consortia explore chemical leaching of binders to improve circularity, but commercial readiness remains several years away, tempering broader deployment in high-volume consumer products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Open-Cell Dominance Driven by Thermal Applications

Open-cell foams held 48.25% of the metal foam market share in 2025, reflecting widespread demand for high-surface-area cores in battery packs, heat exchangers, and data-center cold plates. Their porosity enables convective flows that dissipate hot spots, a capability that closed-cell foams lack. The open-cell segment is expected to register a 4.92% CAGR to 2031, reinforcing its leadership in the metal foam market. Research from the World Academy of Science, Engineering and Technology confirms that coupling ultrasound with open-cell structures can raise overall heat-transfer coefficients by up to 38%, strengthening the application case.

Closed-cell foams maintain relevance where buoyancy, infiltration resistance, and compressive crash performance dominate. Aeronautical bulkheads and offshore buoyancy modules rely on gas-tight cells to prevent flooding. Suppliers now offer hybrid laminates that marry an open-cell core with a closed-cell skin, balancing thermal, mechanical, and impermeability performance within a single panel.

By Material: Aluminium Leadership Faces Emerging Competition

At 56.55% share in 2025, aluminium anchors most mobility and aerospace deployments thanks to a favorable strength-to-weight ratio and ready recyclability. The aluminium slice of the metal foam market size is set to expand at 4.97% CAGR through 2031, supported by aircraft cabin retrofits and EV chassis redesigns that displace stamped sheet. Ultrahigh-strength aluminium alloys infused with transition metals extend fatigue life, unlocking higher-load zones such as battery-enclosure crumple zones.

Copper foams serve thermal spreaders in electronics where conductivity trumps mass penalties, while nickel foams excel in hydrogen fuel cells and high-temperature process lines. Magnesium and steel variants address marine and blast-armor applications, respectively. Material substitution dynamics hinge on alloy price spreads; as aluminium tightens, OEMs may adopt copper-foam inserts despite cost for mission-critical cooling. Specialty suppliers therefore diversify powder portfolios to hedge commodity risk and preserve order continuity.

By Manufacturing Process: Powder Metallurgy Leads Despite Additive Manufacturing Growth

Powder-metallurgy (PM) routes captured 54.80% of 2025 revenue, leveraging decades-old sintering expertise transposed from conventional powder metallurgy into cellular formats. PM tooling amortizes quickly on high-volume parts such as automotive energy absorbers, delivering favorable unit economics. Topology-optimized hips and cranial plates benefit from lattice gradients unattainable through molds, illustrating how 3-D printing extends the practical design space within the metal foam market.

Melt-foaming remains important for large billets where PM porosity control proves difficult, such as buoyant ship fenders. Chemical vapor deposition and electro-deposition target ultra-thin wall thicknesses needed in micro-channel heat sinks for satellite avionics. Hybrid processes now fuse PM cores with laser-printed skins in a single production cell, compressing lead times for prototype runs. This convergence recapitalizes legacy facilities by embedding digital controls atop established furnaces and presses.

By Application: Automotive Dominance Challenged by Emerging Sectors

Automotive applications represented 37.92% of the metal foam market size in 2025, led by bumper beams, battery cradles, and NVH dampers that exploit cellular energy absorption. Global EV penetration fuels incremental demand for both aluminium and copper foams, yet internal-combustion vehicle light-weighting continues, preserving a broad customer base.

Other applications, grouping hydrogen fuel cells, marine coolers, biomedical implants, and data-center spreaders, deliver the fastest growth at 5.07% CAGR to 2031. The surge is partly regulatory: Europe’s Fit-for-55 package favors hydrogen trucks, and hospitals worldwide install porous titanium knee spacers that slash revision surgeries. Aerospace, although smaller by volume, maintains premium margins because certification processes protect incumbents. Industrial machinery users install copper foams inside high-duty servo-drive housings to tame thermal gradients, reinforcing a diversified demand profile that insulates the metal foam market from single-sector swings.

Geography Analysis

Asia-Pacific accounted for 44.10% of global revenue in 2025. Expansion of gigafactories across Guangdong, coupled with Japan’s precision-machined lattice cores for satellite thrusters, underpins a 5.03% regional CAGR to 2031. ASEAN economies, notably Vietnam and Thailand, attract the reshoring of electronics assembly, creating fresh pull for open-cell copper foams in server racks. South Korean conglomerates invest in nickel-foam capacity aimed at hydrogen trucks, leveraging government subsidies to amortize electro-forming lines.

North America is buoyed by federal funding for nuclear-energy heat exchangers and defense armor programs. Advanced Materials Manufacturing secured USD 3.1 million in grants to scale nickel-based composite foams for reactor modules. Mexico’s automotive corridor in Coahuila specifies aluminium foams for lightweight frames, ensuring continental demand diversity. Canada’s CYMAT Technologies won a 21,000-unit order for SmartMetal cylinders for the French armed forces, illustrating how regional firms export niche expertise to global clients.

Europe emphasizes sustainability and high-end engineering. German suppliers integrate foam cores into carbon-fiber sandwich panels for luxury EV cradles, aligning with the EU Carbon Border Adjustment Mechanism that favors low-emissions inputs. French hydrogen clusters pilot nickel-foam heat sinks, while Italian biomedical startups 3-D print tantalum lattices for hip implants. Newly industrializing economies in South America and the Middle East adopt aluminium foams for modular building façades and desalination equipment, contributing incremental yet rising volumes to the metal foam market.

Value Chain Analysis

Upstream, the value chain starts with base metals (aluminium, nickel, copper) and alloying inputs that feed either melt-based routes or powder-based routes. Process consumables such as blowing or foaming agents and stabilizers, along with powders and binders for powder metallurgy (PM) and additive manufacturing, influence achievable pore size distribution and repeatability. Equipment and know-how are a major gate in the chain, including controlled-atmosphere sintering and pressing for PM, gas-injection and quenching systems for melt foaming, and surface-finishing and joining steps (machining, sealing, brazing, bonding) needed to integrate foams into battery packs, sandwich panels, and energy absorbers.

Midstream, foam producers convert metals into open-cell and closed-cell forms through PM, melt foaming, electro-deposition, and other specialty methods, then supply semi-finished cores, billets, sheets, or near-net-shape parts. Downstream value capture sits with tier suppliers and integrators that embed foams into assemblies, including automotive crash structures and battery enclosures, aerospace fire and crash protection inserts, and hydrogen and thermal-management components, with OEM qualification and field validation as the next step. Common bottlenecks include qualification lead times, consistency in high-strain-rate performance data across suppliers, and scaling beyond aluminium into industrial-grade volumes for nickel and copper foams, which increases dependence on localized PM capacity, finishing capability, and repeatable characterization to support multi-industry adoption.

Competitive Landscape

The metal foam market features moderate fragmentation anchored by midsize specialists rather than vertically integrated conglomerates. CYMAT Technologies leverages proprietary gas-injection foaming to supply defence, architectural, and rail customers, capturing repeat orders such as the French SmartMetal cylinder program. Competitive intensity is application-dependent: automotive value chains present cost pressure, favoring large PM houses that achieve scale economies, whereas biomedical devices tolerate higher unit costs in favor of customisation, benefiting nimble printers. Patent filings focus on alloy composition and pore-gradient control, serving as critical barriers against fast followers.

Metal Foam Industry Leaders

Alantum

Aluinvent

CYMAT Technologies Ltd.

ERG Aerospace

Havel metal foam GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Thermal management remains a practical whitespace for metal foams across battery packs, electronics, and emerging high-heat-flux structures, supported by the shift toward open-cell architectures that improve convective heat transfer. Aerospace-facing R&D is also expanding the design envelope for foam-filled sandwich concepts aimed at combining load-bearing capacity and heat dissipation, which aligns with use cases cited in technical literature for corrugated-core and sandwich structures. For suppliers, these pathways translate into demand for application-tuned porosity and stable mechanical performance that can pass customer qualification requirements.

Process and materials innovation further widens openings where sustainability, repeatability, and high-temperature endurance are constraints. In May 2026, Helmholtz-Zentrum Hereon reported magnesium foam produced using ground oyster shell powder as a non-toxic blowing agent, reinforcing a circular-economy compliant route that can broaden material options beyond aluminium in lightweighting programs. Research attention on additive manufacturing of aluminium foams, including work published in March 2026 on H2-infused shielding gas approaches, also points to efforts to reduce tooling barriers and enable complex geometries for low-to-mid volume programs. High-temperature durability evidence for composite metal foams, including reported multi-hundred-thousand to million-cycle testing at elevated temperatures in academic reporting, supports industrial and aerospace niches where conventional lightweight cores struggle to hold performance, creating room for premium offerings centered on reliability as much as density reduction.

Recent Industry Developments

- May 2026: Helmholtz-Zentrum Hereon researchers reported producing magnesium foam using ground oyster shell powder as a sustainable, non-toxic blowing agent. The work signals a pathway to lower-toxicity, circular-economy aligned foam manufacturing, which can help widen material options beyond aluminium for lightweighting programs.

- September 2025: CYMAT Technologies Ltd. entered into a partnership agreement with a global automotive Tier 1 manufacturer to design and manufacture energy-absorbing components. The agreement positions CYMAT closer to OEM supply chains where validated tier-led integration and standardized component platforms accelerate adoption of stabilized aluminium foam in vehicle structures.

- August 2024: CYMAT Technologies received its first commercial order for 21,000 SmartMetal stabilised-aluminium-foam cylinders for non-lethal defence munitions for the French Armed Forces. The order underlined defense as a repeatable volume channel for aluminium foam producers and helped anchor production scale-up through program-driven demand.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenue earned from selling metal foam materials (open-cell, closed-cell, and similar porous metal structures) that are supplied as sheets, blocks, panels, or formed parts for industrial and commercial use.

Scope exclusions: We exclude finished end products where metal foam is only a minor internal component and cannot be valued separately at the material or formed-part level.

Segmentation Overview

- By Type

- Open-Cell Foam

- Closed-Cell Foam

- Stochastic Metal Foam

- By Material

- Aluminum

- Copper

- Nickel

- Other Materials (Magnesium, Steel, Alloys)

- By Manufacturing Process

- Powder Metallurgy Route

- Melt Foaming Route

- Additive Manufacturing / 3-D Printing

- Other Manufacturing Processes (CVD and Electro-Deposition, etc.)

- By Application

- Automotive

- Aerospace

- Industrial Machines

- Construction

- Biomedical

- Other Applications (Marine and Rail, Energy and Power, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

To ground the model, we built a clear picture of where metal foam demand comes from and how it moves across regions. Public sources were used to track signals such as lightweighting activity, industrial production trends, and downstream manufacturing health, which then guide our assumptions for adoption and pricing.

Illustrative sources include government statistics portals such as the US Census Bureau and Eurostat, trade and macro datasets such as UN Comtrade, standards and technical bodies such as ASTM and ISO, and research literature indexed in public science databases. We also reviewed company filings, investor presentations, association websites, and reputable press coverage to validate capacity additions, application trends, and technology shifts such as additive manufacturing. Where needed, paid subscriptions were used for company financials and intelligence, shipment-level trade views, and patent database checks to confirm timing of new material routes and product focus. These examples are not exhaustive, and other public and internal references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions and fill gaps that are rarely stated in public sources, such as typical conversion from foam output to saleable forms and how application mix shifts pricing. We spoke with a mix of manufacturers, distributors, and downstream users across major regions so that adoption rates, procurement patterns, and near-term demand softness or acceleration could be reflected in the final numbers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | APAC: 44% |

| Mid tier: 54% | Functional/Unit leaders: 40% | EMEA: 29% |

| Smaller Players: 18% | Managers: 48% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where production and trade data, together with end-use demand pools, are used to reconstruct how much metal foam is consumed in each region and application. For metal foam, key inputs include the share of open-cell versus closed-cell usage, manufacturing route mix (powder metallurgy, melt foaming, additive manufacturing), downstream indicators tied to automotive and aerospace build activity, and industrial machine and construction output trends that influence project-led purchasing.

Those totals were then checked using selective bottom-up approximations, mainly by sampling supplier revenue ranges, mapping typical price bands by material (such as aluminum, copper, and nickel foams), and using volume proxies where interviews clarified conversion yields and scrap rates. When a bottom-up check had gaps, the missing portion was handled through conservative ranges anchored to capacity and channel availability shared by interviewees, then narrowed through regional consistency checks.

For forecasting, scenario analysis was used so that adoption timing could be adjusted around practical triggers, including lightweighting programs, battery and thermal management demand, and the pace of new production routes scaling to repeatable quality. Assumptions were kept consistent across regions and then tuned using expert views on price progression and realistic qualification cycles for new applications.

Data Validation & Update Cycle

Validation is done through multiple passes so that the final outputs remain aligned with real market signals. We compare the model results against independent indicators such as regional industrial production, trade flow direction, and downstream build rates, and then investigate any sharp jumps that do not match known demand events.

If a variance is found, the assumptions that drive it are revisited, followed by a re-check of conversion factors, application shares, and currency timing used for regional rollups. Interview re-contacts are triggered when a major discrepancy appears between desk signals and what practitioners report on pricing or utilization. Reports are refreshed annually, and interim updates are made when material events occur, after which a final analyst pass is completed before delivery to reflect the latest available information.

Mordor Intelligence's Metal Foam Market Size Compared Against Other Published Estimates

Published market sizes for metal foam often do not line up because the scope is not identical, and the steps used to translate application demand into revenue can vary a lot. Differences usually come from what is counted as metal foam revenue, how open-cell and closed-cell products are treated, and how pricing is carried forward across the forecast period.

Some external estimates fold in a wider set of porous metal structures and include more finished products where metal foam is embedded and not priced separately. In Mordor Intelligence, revenue is counted only when metal foam is sold as a material or formed part, and adjacent finished assemblies are kept out even if they contain foam for energy absorption or thermal management.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 109.12 M (2025) | |

| Industry Publisher A | USD 108.59 M (2025) | Uses a similar base year value, but its scope appears to lean more on material splits and broader application narratives, which can shift what is treated as directly monetized metal foam versus foam-containing end products. |

| Industry Publisher B | USD 105.70 M (2025) | Applies a narrower 2025 value and then projects a faster long-term growth path, which can come from more aggressive adoption assumptions in automotive and construction and a different way of stepping up ASPs over time. |

The table shows that the 2025 values are close, and the spread is mainly explained by what gets counted as saleable metal foam revenue and how fast adoption and prices are assumed to rise. By tying the totals back to application demand signals, manufacturing route realities, and interview-validated pricing ranges, the estimate stays traceable to clear inputs and repeatable checks.

Key Questions Answered in the Report

What is the current value of the metal foam market?

The metal foam market size stood at USD 113.67 million in 2026 and is forecast to reach USD 139.43 million by 2031.

Which region holds the largest metal foam market share?

Asia-Pacific led with 44.10% revenue share in 2025, propelled by China’s expansive EV and secondary-aluminium ecosystems.

Which application segment dominates demand?

Automotive applications contributed 37.92% of 2025 value due to strict lightweighting and crash-safety mandates across electric and conventional vehicles.

How fast is additive manufacturing growing within the market?

Additive manufacturing is projected to post a 4.74% CAGR between 2026 and 2031, the fastest among production routes.

What is the primary restraint curbing faster adoption?

High capital investment for melt-foaming equipment and subsequent precision post-machining subtracts an estimated 1.1 percentage points from the overall CAGR forecast.

Page last updated on: