Metal Coil Lamination Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

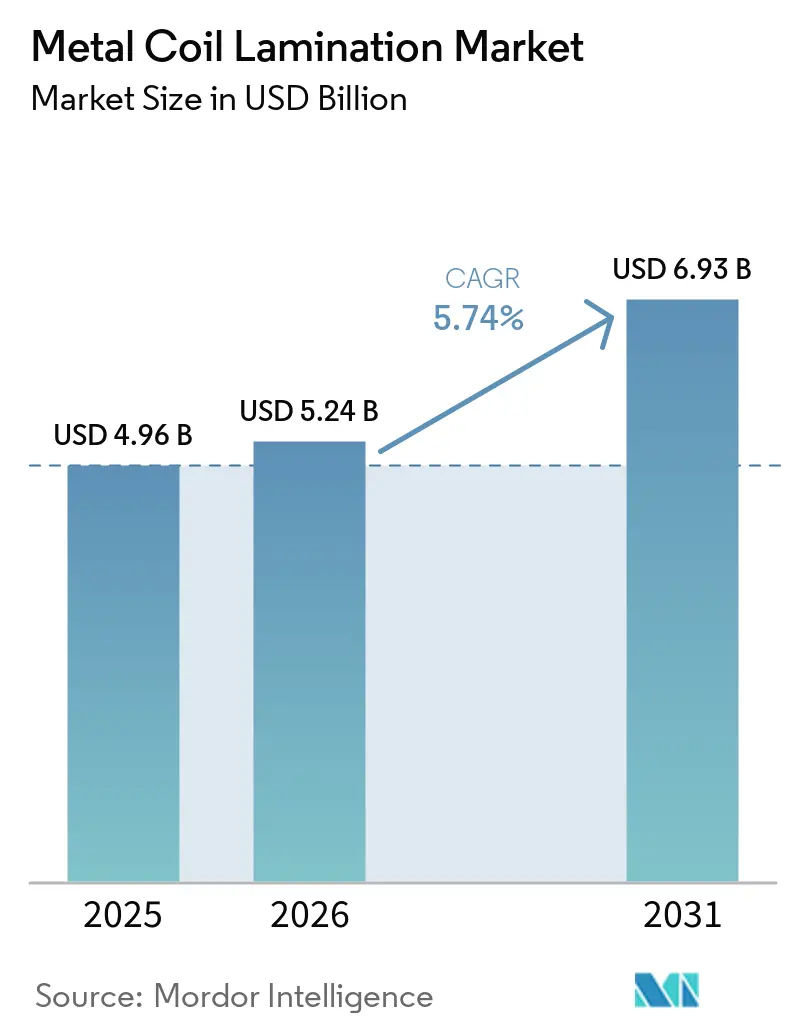

| Market Size (2026) | USD 5.24 Billion |

| Market Size (2031) | USD 6.93 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

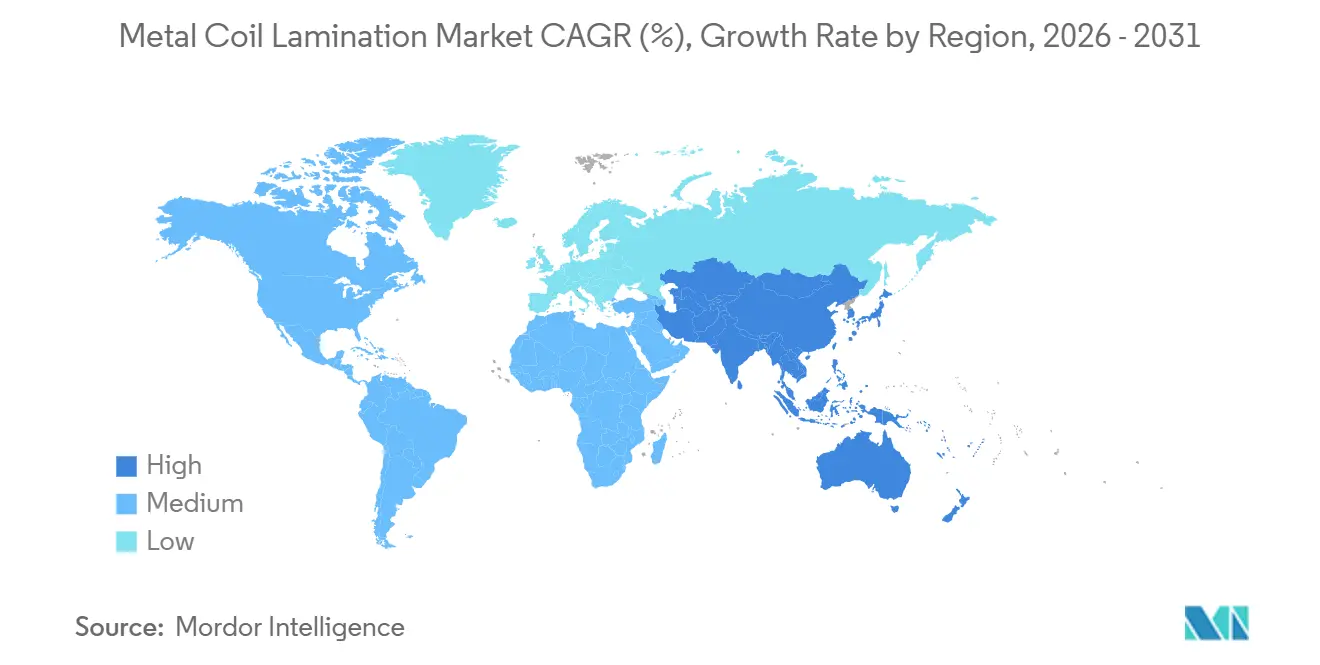

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Coil Lamination Market Analysis by Mordor Intelligence

The Metal Coil Lamination Market size is expected to increase from USD 4.96 billion in 2025 to USD 5.24 billion in 2026 and reach USD 6.93 billion by 2031, growing at a CAGR of 5.74% over 2026-2031. Demand accelerates because factory-finished coils reduce project timelines, eliminate paint-booth emissions, and provide architects with pre-colored panels ready for installation. Regulations such as the EU Carbon Border Adjustment Mechanism incentivize low-energy curing processes, while the U.S. Environmental Protection Agency’s 2026 PFAS discharge limits encourage converters to adopt fluoropolymer-free chemistries. Integrated producers are focusing on captive coating lines to ensure substrate quality, while independent laminators excel in fulfilling orders requiring quick pattern changes or antimicrobial films. Aluminum is gaining market share as automakers work to reduce vehicle weight to comply with the European Union’s 2027 fleet CO₂ limits. UV curing is also gaining popularity due to its ability to reduce energy consumption by 50% to 70% compared to thermal ovens. Overall, the metal coil lamination market demonstrates a balance of volume growth in the Asia-Pacific region and margin growth in premium automotive and smart-surface applications.

Key Report Takeaways

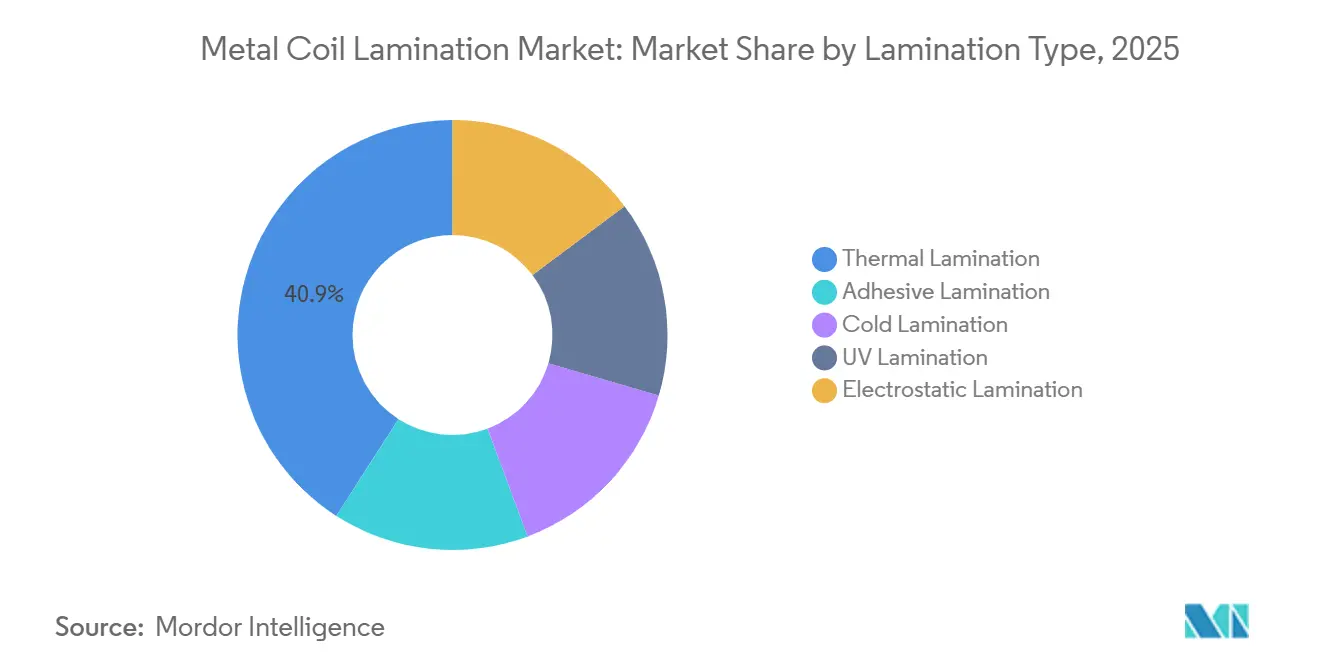

- By lamination type, thermal lamination led with 40.91% of the metal coil lamination market share in 2025, while UV lamination is advancing at a 6.35% CAGR through 2031.

- By substrate metal, steel coils commanded 63.78% of the metal coil lamination market share in 2025; aluminum coils are projected to grow at a 6.89% CAGR through 2031.

- By laminate material, polyethylene terephthalate (PET) films held 51.25% of the metal coil lamination market share in 2025, whereas other laminate materials (acrylics, fluoropolymers) are set to expand at a 7.21% CAGR through 2031.

- By application, architectural panels and cladding 33.88% of the metal coil lamination market share in 2025, while automotive panels and trim are forecast to rise at a 7.43% CAGR through 2031.

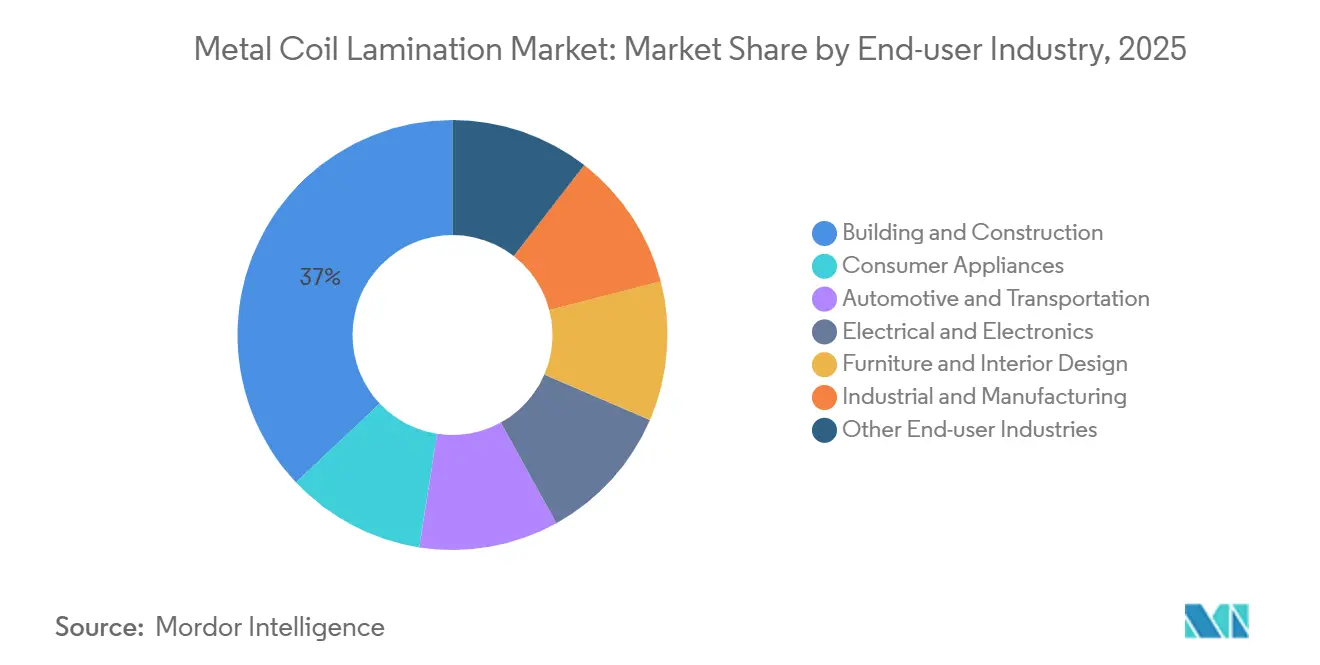

- By end-user industry, building and construction accounted for 37.03% of the metal coil lamination market share in 2025, while automotive and transportation will advance at a 7.31% CAGR through 2031.

- By geography, Asia-Pacific held 42.83% of the metal coil lamination market share in 2025 and is forecast to advance at a 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Metal Coil Lamination Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for pre-coated metal in construction and appliances | +1.2% | Global, with APAC core and spillover to Middle-East | Medium term (2–4 years) |

| Increasing adoption in automotive lightweighting and interiors | +1.5% | North America, Europe, APAC (China, Japan, South Korea) | Long term (≥4 years) |

| Enhanced corrosion resistance and aesthetic appeal | +0.8% | Global, coastal, and high-humidity regions | Medium term (2–4 years) |

| Shift toward high-performance and decorative laminates | +0.7% | Europe, North America, and premium segments in APAC | Medium term (2–4 years) |

| Energy-efficient building materials adoption | +0.9% | Europe (CBAM zones), North America (LEED markets), select APAC cities | Long term (≥4 years) |

| Integration of antimicrobial and smart-surface laminates | +0.6% | Global, with early adoption in healthcare and food-service construction | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Pre-Coated Metal in Construction and Appliances

Factory coating eliminates the need for on-site painting, reducing labor exposure to solvents and shortening construction schedules. AM/NS India expanded its color-coated steel capacity to 1 million tons per year in 2026, targeting roofing applications in second-tier cities where spray booths are less common. Appliance manufacturers prefer laminated coils for their consistent color quality; Vietnamese supplier Systeel Vina provides VCM and PCM to regional LG and Samsung plants tariff-free under ASEAN agreements. In regions where labor costs rise faster than automation expenses, factory lamination becomes more economically viable. New appliance-grade lines now offer features such as fingerprint resistance and deep-draw formability, which traditional paint cannot achieve. These factors collectively drive unit demand and improve margins in the metal coil lamination market.

Increasing Adoption in Automotive Lightweighting and Interiors

Automakers are increasingly adopting pre-laminated aluminum to meet CO₂ targets without investing in new paint facilities. AMAG supplies aluminum body sheets, while Alutrim’s decorative films reduce interior weight by up to 12% while maintaining Class-A surface quality. Material Sciences Corporation’s Smart Steel combines polymer film with high-strength steel, enabling thinner gauges to meet crash standards. Regulations such as California’s Advanced Clean Cars II further drive adoption, and Tier 1 suppliers report 15%–20% energy savings in assembly processes when paint ovens are eliminated.

Enhanced Corrosion Resistance and Aesthetic Appeal

Polymer films protect substrates from salt spray, moisture, and UV exposure. Tata Steel’s Colorcoat HPS200 Ultra, launched in 2025, offers 25-year coastal warranties, exceeding the durability of typical painted steel by a decade. SSAB’s GreenCoat uses bio-based resins, earning BREEAM credits for low lifecycle carbon emissions. Nippon Steel’s Viewcoat creates textured finishes that replicate stone or wood, allowing architects to combine durability with design flexibility. These innovations support premium pricing and help maintain margins in the metal coil lamination market.

Shift Toward High-Performance and Decorative Laminates

Specifiers are increasingly demanding laminates that offer scratch resistance, thermal stability, and visually appealing patterns. ThyssenKrupp Steel’s Pladur Aesthetic, introduced in 2024, features a high-gloss finish that eliminates the energy costs associated with curing powder coats. Arkema’s waterborne PVDF-acrylic hybrids maintain VOC levels below 100 g/L while preserving gloss. Gravure printing technology enables the reproduction of intricate wood grain patterns for furniture, opening new opportunities for market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in metal and polymer feedstock prices | -0.9% | Global, with an acute impact in import-dependent regions | Short term (≤2 years) |

| Environmental scrutiny over VOC and PFAS emissions | -0.6% | North America, Europe (REACH, EPA zones) | Medium term (2–4 years) |

| Competition from powder-coated/painted metal | -0.5% | Global, price-sensitive construction and industrial segments | Medium term (2–4 years) |

| Complex recycling of multi-layer laminate scrap | -0.4% | Europe (EPR mandates), select North American states | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in Metal and Polymer Feedstock Prices

Steel, aluminum, and resin costs remain vulnerable to energy market fluctuations. For instance, polyethylene terephthalate resin prices surged in 2025, impacting converters without price-pass clauses in their contracts. Aluminum smelters, which consume approximately 15 MWh per ton, are particularly affected by power price spikes, which influence coil pricing. Additionally, supply disruptions of critical minerals for specialty alloys increase lead-time risks, complicating inventory and cash flow management in the industry.

Environmental Scrutiny Over VOC and PFAS Emissions

The EPA’s 2026 rule on PFAS discharge limits requires U.S. coil coaters to retrofit water treatment systems or adopt alternative chemistries[1]EPA, “PFAS Discharge Rule for Metal Finishing,” epa.gov. European REACH regulations are tightening restrictions on plasticizers and flame retardants, extending OEM requalification cycles by up to two years. In California, proposed air-district guidance includes fenceline monitoring for scrap processors handling laminated offcuts, necessitating capital expenditures for enclosures and air controls. Smaller converters, lacking dedicated environmental engineering resources, face disproportionate costs, which slow capacity expansion and moderate growth in the metal coil lamination market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lamination Type: UV Lamination Gains on Energy Economics

In 2025, thermal lamination continued to lead with 40.91% of the metal coil lamination market share. However, UV lamination is anticipated to grow at the fastest rate, with a 6.35% CAGR through 2031, due to its instant curing capabilities and significant energy cost reductions. The adoption of UV lamination is accelerating, particularly in regions where the EU CBAM increases the cost of natural gas ovens. Electrostatic, cold, and adhesive methods remain niche, catering to electronics, signage, and multilayer shields requiring specialized bonding. OEMs report a three- to five-year payback period for UV upgrades, factoring in energy savings and avoided carbon penalties. IST METZ and Koenig & Bauer dominate the equipment supply market, benefiting from service revenues tied to lamp replacement schedules. Over time, UV technology's higher throughput is expected to erode the market share of thermal ovens, although legacy systems may persist in regions with energy subsidies.

Converters using UV to bake acrylic or fluoropolymer films avoid substrate warpage, a critical requirement for 0.5 mm automotive body sheets. Cold lamination remains relevant for temporary protection films, though its line speeds are limited by adhesive flash-off time. Adhesive lamination thrives in applications requiring multilayer barriers, such as high-voltage transformers, where polyimide, aramid, and PET are used. As regulatory energy surcharges increase, UV technology is emerging as the preferred choice for new capacity in the metal coil lamination market.

By Substrate Metal: Aluminum Coils Capture Lightweighting Premium

Steel coils held 63.78% of the metal coil lamination market share in 2025, primarily due to their cost-effectiveness and magnetic properties. However, aluminum coils are expected to grow at a CAGR of 6.89% through 2031, driven by the need to reduce vehicle weight and comply with 2027 fleet CO₂ limits. Novelis has committed USD 4.1 billion to its Bay Minette rolling mill, which has a capacity of 600,000 tons per year and offers pre-laminated autobody sheets. Copper remains a premium but niche substrate for electrical insulation, offering higher margins due to its dielectric properties. Zinc and nickel alloys are used in chemical processing applications where galvanic resistance justifies their higher costs.

Integrated steel producers like POSCO sold over 7 million tons of coated steel in 2025[2]POSCO, “2025 Coated Steel Production Statistics,” posco.com. However, their dominance is challenged as buyers increasingly consider the total cost of ownership, including embedded carbon. Aluminum's recyclability and weight reduction benefits are shifting buyer preferences, despite its higher price. The metal coil lamination market is evolving into a competition between steel's cost advantage and aluminum's regulatory and lightweighting benefits.

By Laminate Material: Other Laminate Materials (Acrylics, Fluoropolymers) Surge on PFAS Bans

Polyethylene terephthalate (PET) films accounted for 51.25% of the metal coil lamination market share in 2025 due to their cost-effectiveness and balanced properties. However, regulatory changes are driving demand for alternative laminate materials, such as acrylics and fluoropolymers, which are expected to grow at a CAGR of 7.21% through 2031. By 2031, the market size for acrylic and hybrid fluoropolymers could reach USD 1.46 billion, as specifiers increasingly demand VOC levels below 100 g/L. Products like Cortec’s 27% biobased EcoLine 3860 demonstrate that renewable materials can perform well under accelerated weathering conditions without significant cost increases. Waterborne PVDF-acrylic hybrids from Arkema offer a drop-in solution for legacy coil lines, retaining gloss while reducing solvent use.

PVC remains dominant in furniture laminates due to its fire-code compliance and embossing capabilities, although plasticizer migration issues necessitate reformulation. BOPP and CPP films are gaining traction in thin-panel applications due to their weight-saving properties. Paper-based laminates remain a niche option for circular-economy packaging but indicate potential future diversification. Overall, regulatory pressures and ESG targets are reshaping the material landscape in the metal coil lamination market.

By Application: Automotive Panels and Trim Outpace Traditional Architectural Panels and Cladding

Architectural panels and cladding led the market with a 33.88% share in 2025. However, automotive panels and trim are expected to grow at a CAGR of 7.43% through 2031. Automakers benefit from energy savings of up to 20% by eliminating paint ovens, as laminated coils arrive ready for stamping without VOC emissions. Building codes continue to support cladding demand, particularly in Asia, where urbanization drives the need for durable facades.

Household appliances maintain steady demand, as refrigerators and washing machines require consistent color finishes. Furniture and interior décor applications favor pre-laminated metal for its hygiene and flame resistance advantages over wood veneer. Electrical cabinets require conductive backside coatings for grounding. While these niches ensure the continued relevance of pre-coated metal, the automotive sector remains the primary growth driver for the metal coil lamination market.

By End-user Industry: Automotive Leads Growth Amid Emissions Mandates

The building and construction industry held 37.03% of the market share in 2025. However, the automotive and transportation industry is projected to grow at a CAGR of 7.31% through 2031, driven by emissions regulations in Europe and California that link credit penalties to CO₂ output. OEMs are increasingly adopting laminated aluminum and advanced steel solutions. Consumer appliances continue to rely on laminated coils to avoid batch paint variation and meet VOC compliance requirements. The electrical and electronics industries demand specialty copper laminates for their dielectric properties, which command premium margins.

Segments such as furniture, healthcare, and industrial storage use laminates for fire safety and corrosion protection. Although these segments represent smaller revenues, they offer robust margins due to their performance-driven requirements. Overall, regulatory timelines for emissions and waste are pushing the metal coil lamination industry toward transportation and high-specification equipment over the next five years.

Geography Analysis

Asia-Pacific accounted for 42.83% of the metal coil lamination market share in 2025 and is expected to grow at a CAGR of 7.18% through 2031. Investments such as Shanxi Jianlong’s USD 1.4 billion Jiaozuo line, which offers 30-year PVDF warranties, are supporting housing booms in tier-2 Chinese cities. Japanese and Korean producers are focusing on CO₂ reductions, with Nippon Steel’s Viewcoat achieving 30% lower emissions per ton. India’s AM/NS plant, with a capacity of 1 million tons per year, targets roofing applications where on-site spray booths are unavailable.

North America is growing from a smaller base, led by Novelis’s Bay Minette aluminum coil mill and USMCA regulations that localize automotive sourcing. EPA PFAS limits are driving investments in water treatment, raising entry barriers for new players. Mexico is emerging as a hub for appliance exports, while Canada’s green-building initiatives encourage the use of low-VOC coated steel.

Europe, while mature, is advancing sustainability initiatives. CBAM imposes carbon costs on imports, encouraging buyers to choose domestic UV-cured coils. SSAB’s GreenCoat is gaining traction with bio-based resin systems. Southern Europe favors cost-effective galvanized sheets, while Germany and Nordic countries prefer premium laminates with documented life cycle assessments.

The Middle-East and Africa, along with South America, contribute smaller shares but show selective growth. Saudi Arabia’s Vision 2030 projects require corrosion-resistant cladding for coastal resorts. Brazil’s construction cycle supports demand for coated roofing, while Argentina uses laminated aluminum in export vehicles. These regions highlight how infrastructure and resource investments sustain incremental growth in the metal coil lamination market.

Competitive Landscape

The market is moderately concentrated, with key players such as ArcelorMittal, Hindalco Industries Ltd. (Novelis), POSCO, Nippon Steel, and Tata Steel integrating substrate rolling with captive coating operations. These companies capture end-to-end margins and offer bundled pricing. Independent specialists like Material Sciences Corporation, LIENCHY, and Laminators Incorporated compete by offering quick-change production lines, antimicrobial films, or conductive coatings for electronics. Specialty chemical companies such as Arkema and Cortec provide PFAS-free and biobased resins, enabling converters to meet regulatory requirements without compromising durability.

Technological advancements are a key differentiator. UV curing systems from IST METZ and Koenig & Bauer operate at speeds exceeding 400 m/min, reducing energy consumption and attracting automotive orders. Novelis has filed patents for high-recycled-content aluminum with pre-applied films, aligning with circular economy goals. ThyssenKrupp’s Pladur Aesthetic replaces powder-coated appliances by matching gloss uniformity while eliminating oven loads. While price competition is intense in commodity roofing, high-performance niches reward companies that demonstrate ESG advantages and offer rapid prototyping. Overall, companies that combine substrate control with low-carbon or functional coatings maintain strong competitive positions in the metal coil lamination market.

Metal Coil Lamination Industry Leaders

POSCO

Tata Steel

ArcelorMittal

NIPPON STEEL CORPORATION

Hindalco Industries Ltd. (Novelis)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NIPPON STEEL CORPORATION completed its USD 14.9 billion acquisition of US Steel, which strengthened its position in electrical steel production. This development influenced the metal coil lamination market by ensuring a steady supply of high-quality electrical steel for EV motors and transformer laminations.

- May 2025: Tata Steel inaugurated the Phase II expansion of its Kalinganagar plant in Odisha, India, which increased its crude steel production capacity from 3 million tonnes per annum (MTPA) to 8 MTPA. This expansion is expected to support the growing demand in the metal coil lamination market by ensuring a steady supply of high-quality steel.

Global Metal Coil Lamination Market Report Scope

Metal coil lamination is a continuous industrial process in which thin layers of materials, such as plastic films or metal foils, are bonded to metal coils, typically aluminum, steel, or copper, to improve their performance and appearance. This process is typically carried out on a continuous production line using heat, pressure, or adhesives to produce a durable composite material.

The Metal Coil Lamination Market is segmented into lamination type, substrate metal, laminate material, application, end-user industry, and geography. By lamination type, the market is segmented into thermal lamination, adhesive lamination, cold lamination, UV lamination, and electrostatic lamination. By substrate metal, the market is segmented into steel coils, aluminum coils, copper coils, and other substrate metals (zinc, nickel alloys). By laminate material, the market is segmented into polyethylene terephthalate (PET) films, polyvinyl chloride (PVC) films, biaxially oriented polypropylene (BOPP) films, paper-based laminates, and other laminate materials (acrylics, fluoropolymers). By application, the market is segmented into architectural panels and cladding, household appliances, furniture and interior décor, electrical cabinets and equipment, automotive panels and trim, industrial storage and racks, and other applications (signage, consumer). By end-user industry, the market is segmented into building and construction, consumer appliances, automotive and transportation, electrical and electronics, furniture and interior design, industrial and manufacturing, and other end-user industries. The report also covers the market size and forecasts for metal coil lamination in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Thermal Lamination |

| Adhesive Lamination |

| Cold Lamination |

| UV Lamination |

| Electrostatic Lamination |

| Steel Coils |

| Aluminum Coils |

| Copper Coils |

| Other Substrate Metals (Zinc, Nickel Alloys) |

| Polyethylene Terephthalate (PET) Films |

| Polyvinyl Chloride (PVC) Films |

| Biaxially Oriented Polypropylene (BOPP Films) |

| Paper-Based Laminates |

| Other Laminate Materials (Acrylics, Fluoropolymers) |

| Architectural Panels and Cladding |

| Household Appliances |

| Furniture and Interior Décor |

| Electrical Cabinets and Equipment |

| Automotive Panels and Trim |

| Industrial Storage and Racks |

| Other Applications (Signage, Consumer) |

| Building and Construction |

| Consumer Appliances |

| Automotive and Transportation |

| Electrical and Electronics |

| Furniture and Interior Design |

| Industrial and Manufacturing |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Lamination Type | Thermal Lamination | |

| Adhesive Lamination | ||

| Cold Lamination | ||

| UV Lamination | ||

| Electrostatic Lamination | ||

| By Substrate Metal | Steel Coils | |

| Aluminum Coils | ||

| Copper Coils | ||

| Other Substrate Metals (Zinc, Nickel Alloys) | ||

| By Laminate Material | Polyethylene Terephthalate (PET) Films | |

| Polyvinyl Chloride (PVC) Films | ||

| Biaxially Oriented Polypropylene (BOPP Films) | ||

| Paper-Based Laminates | ||

| Other Laminate Materials (Acrylics, Fluoropolymers) | ||

| By Application | Architectural Panels and Cladding | |

| Household Appliances | ||

| Furniture and Interior Décor | ||

| Electrical Cabinets and Equipment | ||

| Automotive Panels and Trim | ||

| Industrial Storage and Racks | ||

| Other Applications (Signage, Consumer) | ||

| By End-user Industry | Building and Construction | |

| Consumer Appliances | ||

| Automotive and Transportation | ||

| Electrical and Electronics | ||

| Furniture and Interior Design | ||

| Industrial and Manufacturing | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the metal coil lamination market?

The metal coil lamination market stands at USD 5.24 billion in 2026 and is projected to reach USD 6.93 billion by 2031.

Which lamination type is growing fastest through 2031?

UV lamination leads with a 6.35% CAGR through 2031 because it cuts energy use by up to 70% and avoids carbon levies tied to thermal ovens.

Why are aluminum coils gaining share in metal lamination?

Automakers seek vehicle lightweighting to meet 2027 CO₂ limits, so aluminum coils, although pricier, offer major mass reduction and recyclability advantages.

What material shift is driven by PFAS regulations?

Buyers are replacing traditional PVDF with PFAS-free acrylic and hybrid fluoropolymer films that still deliver weatherability but avoid 2026 discharge limits.

Page last updated on: