High-End Copper Foil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

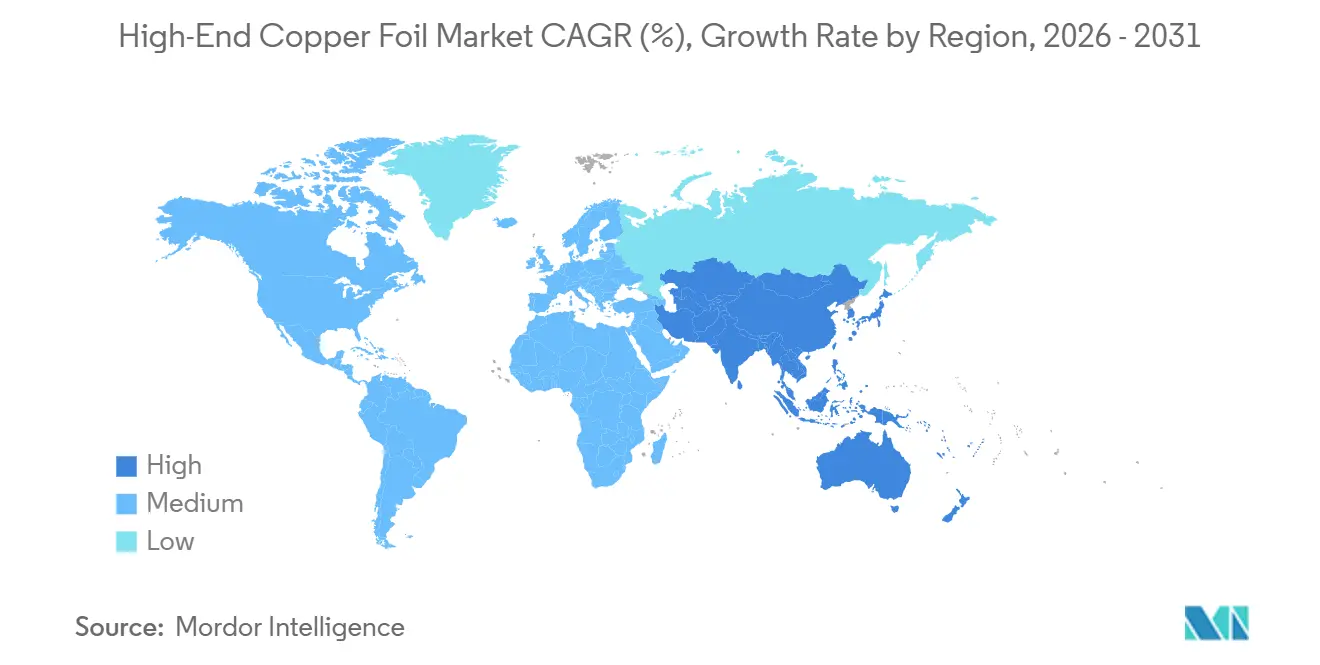

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

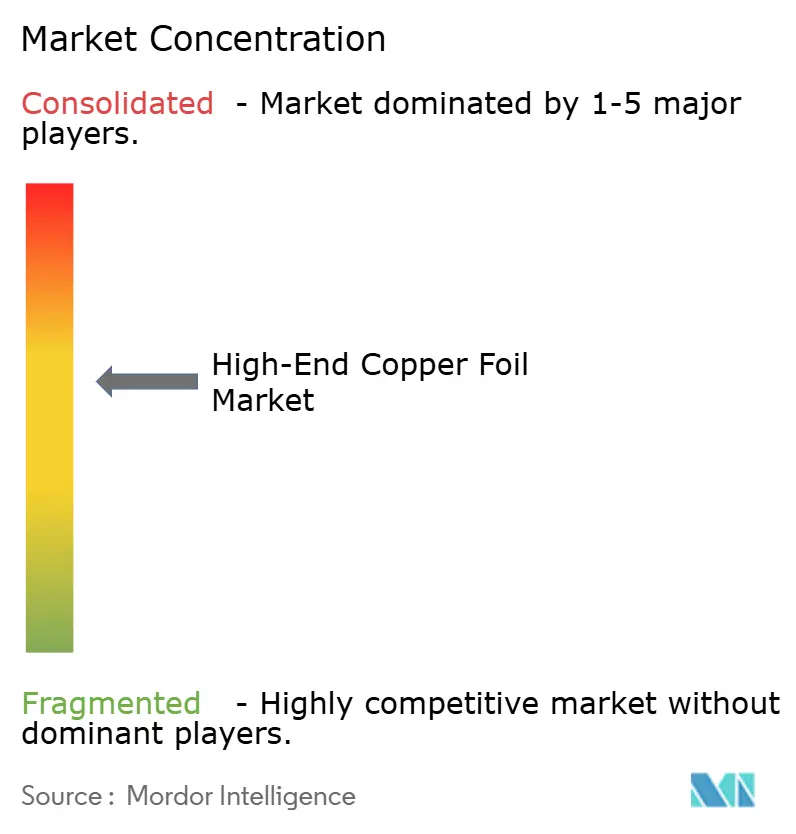

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-End Copper Foil Market Analysis by Mordor Intelligence

The High-End Copper Foil Market size is estimated at USD 1.16 billion in 2026, and is expected to reach USD 1.58 billion by 2031, at a CAGR of 6.38% during the forecast period (2026-2031). Firm demand for ultra-thin electrodeposited foils in lithium-ion batteries, alongside premium rolled foils for millimeter-wave printed-circuit boards (PCBs), is reshaping profit pools. Automakers are specifying 4 µm current collectors to unlock 5-11% energy-density gains, while data-center operators require ultra-low-profile surfaces to manage 30-300 GHz signal losses. China’s new GB safety standard, effective July 1, 2026, tightens purity and tensile-strength thresholds, compelling local mills to upgrade electrodeposition lines or exit. Finally, North American and European gigafactories are redirecting 15-20% of incremental battery-foil demand to regional suppliers to satisfy domestic-content rules, accelerating capacity announcements in Mexico, Poland, and Hungary.

Key Report Takeaways

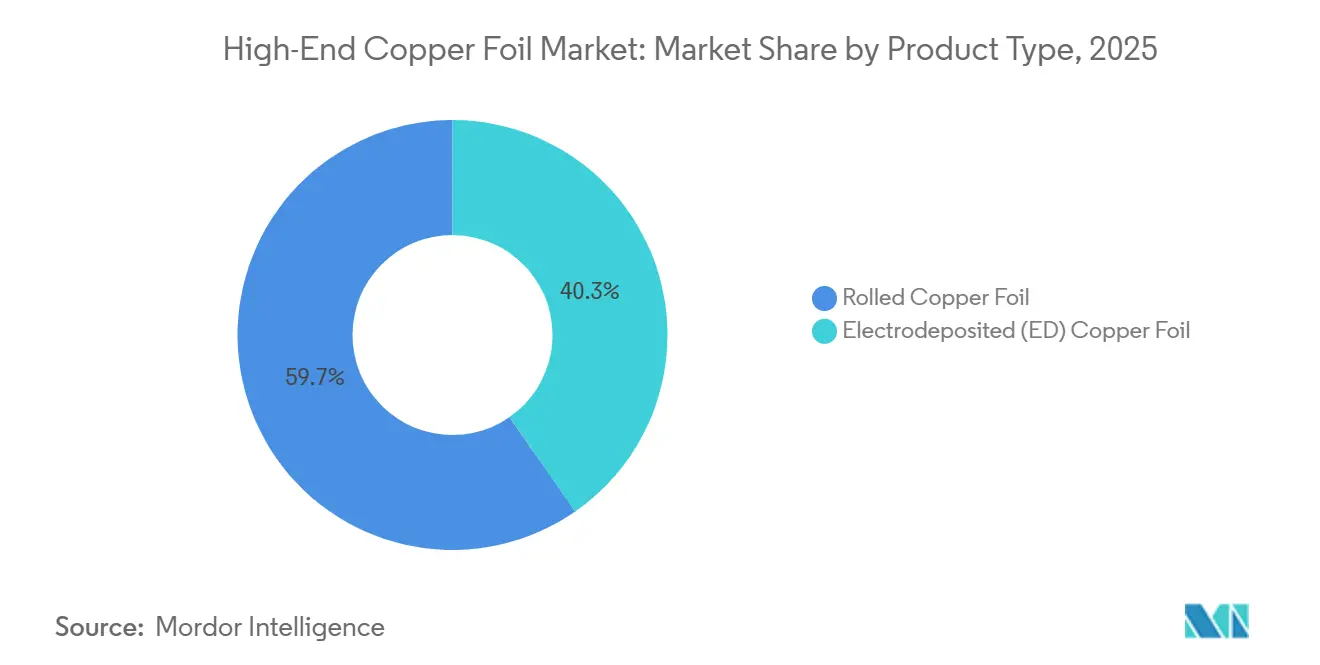

- By product type, rolled copper foil led with 59.67% of 2025 revenue, whereas electrodeposited foil is forecast to advance at an 8.44% CAGR through 2031.

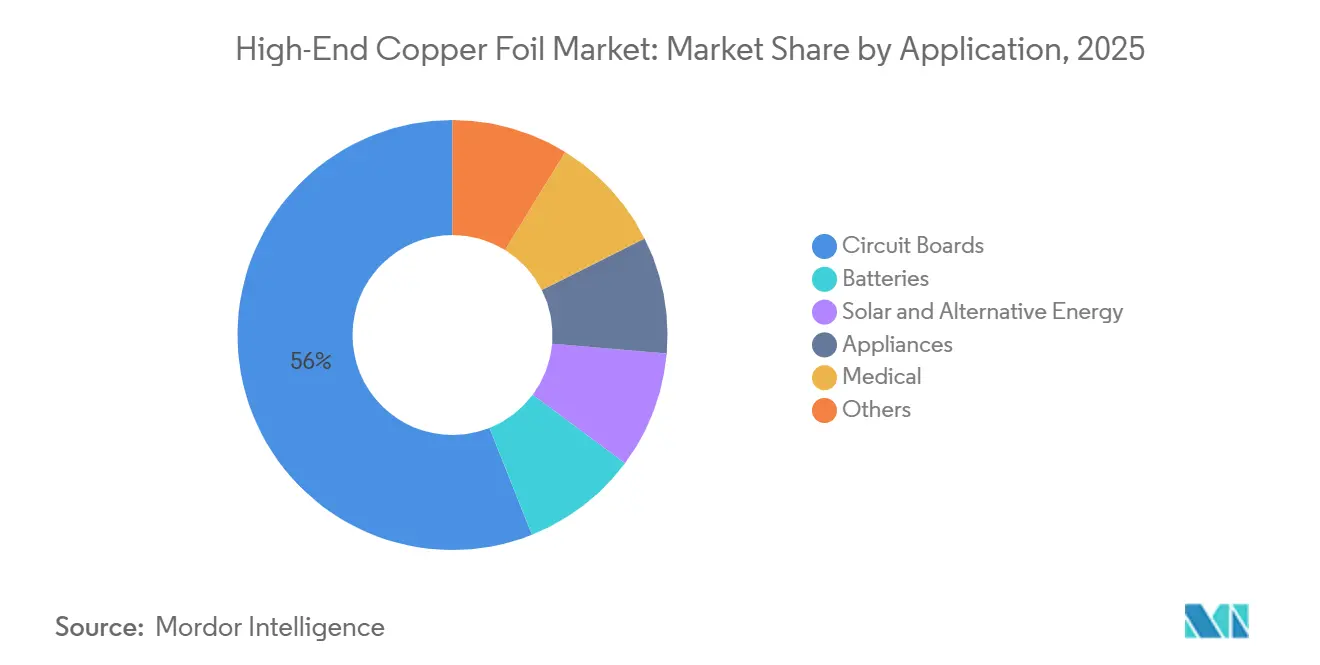

- By application, circuit boards captured 56.02% of 2025 revenue, while batteries record the fastest 14.18% CAGR to 2031.

- By geography, Asia-Pacific held 69.60% of 2025 value; the region exhibits the highest 6.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High-End Copper Foil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Battery Demand for Ultra-Thin High-Purity Foils | +2.1% | Global, with APAC core and spill-over to North America and EU | Medium term (2-4 years) |

| 5G / HPC Push for High-Frequency PCBs | +1.3% | North America, EU, Japan, South Korea | Short term (≤ 2 years) |

| Regional Gigafactory Localisation Wave (North America and European Union) | +1.6% | North America and EU, secondary impact in Mexico and Eastern Europe | Medium term (2-4 years) |

| Closed-Loop Battery-Grade Foil Recycling Initiatives | +0.7% | EU (regulatory-driven), North America (voluntary), emerging in China | Long term (≥ 4 years) |

| Tight Supply of HF PCB Substrates Drives Premium Foil Demand | +0.9% | Global, concentrated in North America, Japan, Taiwan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV Battery Demand for Ultra-Thin High-Purity Foils

Every 2 µm reduction in foil thickness lifts gravimetric energy density by 5-6%, spurring OEMs to adopt 6 µm and 4 µm anode collectors. China shipped 1,334 GWh of lithium batteries in 2025 and is on track for 1,622 GWh in 2026, but July 2026 purity mandates will push marginal mills out of the high-end copper foil market. Western gigafactories demand 99.99% purity and sub-1% elongation variance, tilting awards toward Japanese and Korean suppliers. The International Energy Agency warns of a 30% primary-copper shortfall by 2035, intensifying the importance of thin-foil yield management. Premium electrodeposited grades command USD 22-28 per kg versus USD 15-18 for standard 8 µm foils, rewarding mills that master sub-6 µm deposition.

5G / HPC Push for High-Frequency PCBs

Hyperscale data centers upgrading to 800G and 1.6T Ethernet require dielectric constants below 3.5, forcing laminate makers to use ultra-low-profile rolled foils with surface roughness under 0.4 µm. Rogers Corporation’s RO4000 laminate lead times lengthened from 16 to 26 weeks in 2025 because copper-foil supply was constrained. AI accelerator boards lose competitiveness when insertion loss exceeds 1 dB per inch, encouraging buyers to secure foil allocations a year in advance. IPC-6018D design rules now carve out rolled foil for mmWave boards, lifting spot premiums 15-20% above contracts. Integrated suppliers that own both rolling mills and laminate lines capture the value.

Regional Gigafactory Localisation Wave

Samsung SDI and General Motors’ USD 3.5 billion U.S. plant, Volkswagen’s USD 20 billion Ontario project, and Northvolt’s EUR 902 million German facility epitomize the localization wave. Yet North America operated only 18,000 tpa of electrodeposited capacity in 2025, forcing airfreight imports from Asia at 12-15% logistics premiums. Korean and Japanese mills are responding with greenfield lines in Mexico, Poland, and Hungary, redirecting 15-20% of incremental battery-foil demand away from China. Domestic-content credits under the U.S. Inflation Reduction Act and the EU Critical Raw Materials Act underpin the shift.

Closed-Loop Battery-Grade Foil Recycling Initiatives

Redwood Materials reached 100 GWh of recycling capacity in 2025, recovering copper at 99.95% purity and lowering input costs 20-25% relative to virgin metal[1]Redwood Materials, “Closed-Loop Copper Recovery,” redwoodmaterials.com . The EU Battery Regulation mandates 12% recycled copper by 2031 and an 85% collection rate by 2028, driving gigafactories to co-locate scrap reclamation. Umicore and Ascend Elements have signed multi-year offtake deals that shorten copper loops to 30 days. China’s extended-producer-responsibility rules add further impetus, though enforcement varies by province.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper Price Volatility and Margin Squeeze | -1.4% | Global, with acute impact in China and India | Short term (≤ 2 years) |

| Chinese Over-Capacity-Led Price Wars in Li-Battery Foil | -0.9% | APAC core, spill-over to global commodity segments | Medium term (2-4 years) |

| Sodium-Ion Shift (Al Current Collectors) Cannibalises Copper | -0.6% | China, India, emerging in EU for stationary storage | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Copper Price Volatility and Margin Squeeze

London Metal Exchange spot rose to USD 11,200/t in October 2025, with Q2 2026 forecasts near USD 12,500/t, slashing foil-maker EBITDA by 2-3 percentage points because pass-through clauses lag 60-90 days. Smaller South Asian mills lacking hedge programs posted negative margins in Q3 2025 when premiums widened to USD 280/t. The IEA foresees a structural 30% copper supply deficit by 2035, preserving volatility. Producers are locking multi-year concentrate offtakes and investing in scrap recycling, but benefits accrue only after 18-36 months.

Chinese Over-Capacity-Led Price Wars in Li-Battery Foil

China built roughly 600,000 tpa of electrodeposited capacity by 2024, yet domestic demand consumed only 420,000-450,000 tpa, leaving idle capacity that drove spot prices for 8-10 µm grades down to USD 15-17/kg in 2025. Provincial subsidies have entrenched overinvestment, echoing past solar-panel gluts. Export surges to Southeast Asia and Europe triggered anti-dumping probes, but high-purity and ultra-thin niches remain insulated by stringent quality hurdles. Marginal Chinese mills may consolidate or shift to lower-cost regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rolled Foil Retains PCB Premium, Electrodeposited Scales in Batteries

Rolled copper accounted for 59.67% of 2025 value, supported by root-mean-square roughness near 0.35 µm and unrivaled mechanical strength that mitigates skin-effect losses on 30-300 GHz boards. Electrodeposited foil is projected to grow at 8.44% CAGR, driven by battery makers migrating toward 6 µm and 4 µm gauges that electrodeposition can deliver uniformly across 1,350 mm widths. Capital intensity runs above USD 100 million per multi-stage rolling mill, fostering an oligopoly among Japanese and European producers who can charge USD 28-35 / kg for ultra-smooth variants. Conversely, Chinese electrodeposition capacity surged to 600,000 tpa by 2024, sparking price wars in standard 8 µm grades.

Electrodeposited processes allow higher throughput and lower micro-crack risk below 5 µm thickness, an edge as the high-end copper foil market pivots to energy-dense cells. Meanwhile, 5G and AI boards drive pre-booking of rolled-foil allocations 12 months ahead, creating dual supply chains. Integrated rolled-foil mills are forward-integrating into laminates, while electrodeposited specialists co-locate near gigafactories to offer just-in-time delivery. These divergent models illustrate how the high-end copper foil market continues to bifurcate.

By Application: Circuit Boards Dominate Revenue, Batteries Deliver Growth

Circuit boards commanded 56.02% of revenue in 2025, reflecting entrenched demand in smartphones, automotive ADAS, and industrial controls. Batteries, however, register a 14.18% CAGR through 2031 as EV penetration rises and grid-scale storage accelerates. PCB demand is itself splitting: commodity rigid boards now specify thinner, lower-cost foils, while AI servers and 5G base stations require rolled foil priced at USD 28-35 / kg. Rogers Corporation’s RO4000 substrate backlog illustrates the strain, with lead times ballooning to 26 weeks.

Battery collectors are converging on 6 µm electrodeposited foil with 99.99% purity and ≥350 MPa tensile strength to deliver ≥2,000 cycles. Solar and alternative-energy end uses, such as CIGS thin-film and tandem perovskite modules, require oxidation-resistant foils that tolerate 150-180 °C reflow, creating a niche revenue stream. ISO 13485-qualified medical foils enjoy price insulation because qualification can run 24 months. Miscellaneous uses—RFID, EMI shielding, décor laminates—grow slowly but even out cyclicality, reinforcing the diversified but shifting profile of the high-end copper foil market.

Geography Analysis

Asia-Pacific generated 69.60% of 2025 revenue and is forecast at a 6.72% CAGR through 2031, bolstered by China’s large production share and South Korea’s sub-6 µm expertise. China’s July 2026 GB standard is forcing technical upgrades or exits, squeezing commodity producers but supporting premium price realization. South Korea’s SKC, Solus Advanced Materials, and LS MTRON are scaling capacity in Poland and Malaysia to serve EU and ASEAN gigafactories, while Japanese players prioritize quality in high-purity and rolled niches.

North America and Europe are pivoting toward localization. The high-end copper foil market size for North America is set to expand as the Inflation Reduction Act primes gigafactory investment. Yet only 18,000 tpa of regional electrodeposited capacity existed in 2025, necessitating imports at 12-15% cost premiums until greenfield lines in Mexico and Hungary come online. Europe’s Battery Regulation layers recycled-content mandates that favor co-located recycling, attracting investments from Redwood Materials and Umicore.

South America, the Middle East, and Africa remain import-dependent. Brazil buys about 10,000 t of copper foil yearly for consumer electronics, while Saudi Arabia’s Vision 2030 stimulates data-center builds that demand high-frequency laminates. South Africa’s mining base offers concentrates, but the region lacks foil fabrication, hinting at future semi-finished export models if Southern African battery clusters emerge.

Competitive Landscape

The high-end copper foil industry is moderately concentrated: the ten largest producers controlled roughly 57% of 2025 capacity. Rolled-foil supply is quasi-oligopolistic because only Japanese, European, and North American mills own precision rollers that achieve sub-0.4 µm roughness, whereas China’s 600,000 tpa electrodeposited segment is fragmented and price-competitive. Incumbents pursue three tactics. First, vertical integration into laminates to capture PCB substrate premiums. Second, co-location with gigafactories for just-in-time service and logistics savings. Third, backward integration into recycling to hedge copper volatility.

Patent filings for sub-6 µm electrodeposition and reverse-treatment chemistries climbed 22% in 2024-2025, led by Korean and Japanese applicants[2]World Intellectual Property Organization, “Copper-Foil Patent Trends 2025,” wipo.int. White-space opportunities include medical-grade flex circuits requiring ISO 13485 certification and photovoltaic interconnects for tandem perovskites that demand novel alloying for 150-180 °C stability. Regionally, SKC and Solus are adding 25,000 tpa in Poland, Furukawa Electric and Panasonic secured a five-year rolled-foil contract for 800G switches, and Redwood Materials teamed with Ford on a 50 GWh recycling joint venture. Sodium-ion batteries threaten 3-5% displacement as aluminum replaces copper, so incumbents are developing sub-3 µm foils for lithium-metal anodes in solid-state cells, reinforcing the dynamic nature of the high-end copper foil market.

High-End Copper Foil Industry Leaders

SKC

Nuode New Materials Co Ltd

Lotte Energy Materials

JX Advanced Metals Corporation

Mitsui Kinzoku Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Lotte Energy Material launched ‘HiSTEP,’ the first hybrid high-end product brand in South Korea’s copper foil industry. This launch marked a significant milestone in the country's copper foil sector.

- July 2024: Solus Advanced Materials commenced mass production of copper foil for next-generation AI accelerators developed by a major North American GPU company. This achievement marks the first time a Korean firm has secured product approval and initiated mass production of copper foil for AI accelerators.

Global High-End Copper Foil Market Report Scope

Copper of the highest purity, utilized in applications such as PCBs, Li-ion batteries, photovoltaic anodes, medical devices, home appliances, aerospace, and military equipment, is referred to as high-end copper. High-end copper foil is an ultra-thin, high-purity, and mechanically stable copper material essential for advanced electronics, including 5G, AI, batteries, flexible PCBs, providing excellent electrical conductivity, uniformity, and reliability.

The high-end copper foil market is segmented into product type, application, and geography. By product type, the market is segmented into rolled copper foil and electrodeposited (ED) copper foil. By application, the market is segmented into circuit boards, batteries, solar and alternative energy, appliances, medical, and others. The report also covers the market size and forecasts for the high-end copper in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Rolled Copper Foil |

| Electrodeposited (ED) Copper Foil |

| Circuit Boards |

| Batteries |

| Solar and Alternative Energy |

| Appliances |

| Medical |

| Others |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Rolled Copper Foil | |

| Electrodeposited (ED) Copper Foil | ||

| By Application | Circuit Boards | |

| Batteries | ||

| Solar and Alternative Energy | ||

| Appliances | ||

| Medical | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the high-end copper foil market in 2026?

The high-end copper foil market size stands at USD 1.16 billion in 2026 and is projected to reach USD 1.58 billion by 2031.

Which product type holds the largest share?

Rolled copper foil led with 59.67% of 2025 revenue due to its ultra-low-profile surface demanded by high-frequency PCBs.

What is the fastest-growing application through 2031?

Batteries grow at a 14.18% CAGR, supported by rising EV and energy-storage deployments.

Which region shows the highest growth rate?

Asia-Pacific is forecast to grow at 6.72% CAGR as localized gigafactories boost demand for domestic foil supply.

Page last updated on: