Cathode Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

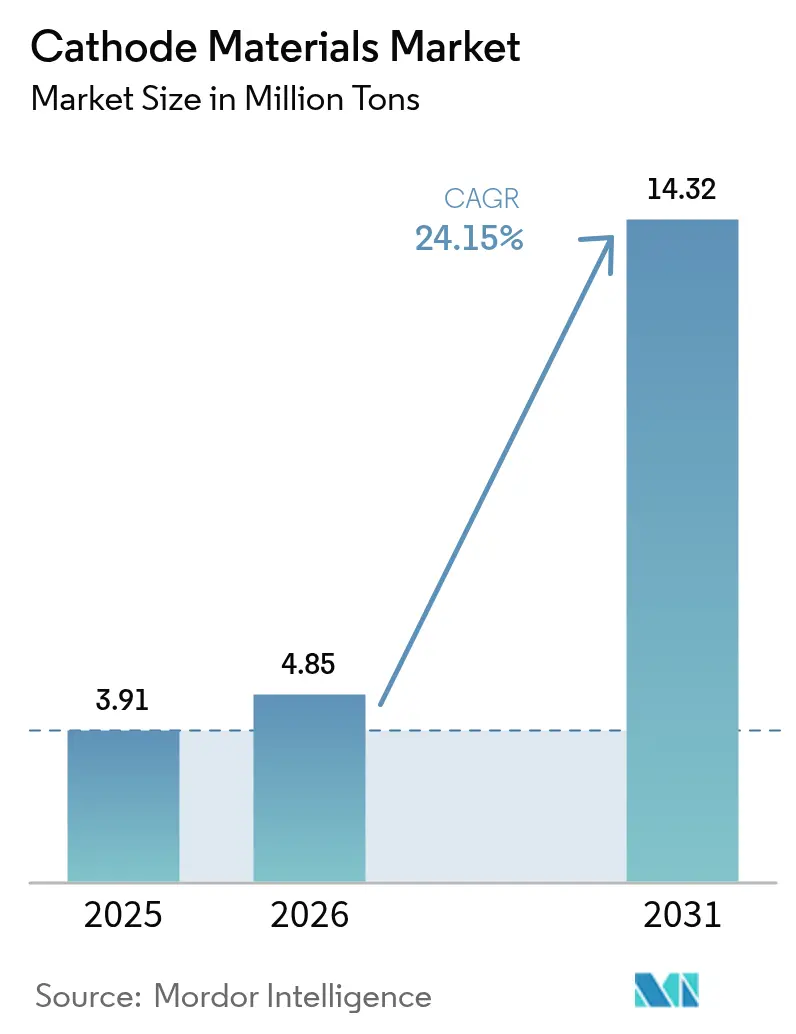

| Market Volume (2026) | 4.85 Million tons |

| Market Volume (2031) | 14.32 Million tons |

| Growth Rate (2026 - 2031) | 24.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cathode Materials Market Analysis by Mordor Intelligence

The Cathode Materials Market size was valued at 3.91 Million tons in 2025 and is estimated to grow from 4.85 Million tons in 2026 to reach 14.32 Million tons by 2031, at a CAGR of 24.15% during the forecast period (2026-2031). Automakers are prioritizing bill-of-material savings over energy density, prompting a pivot toward lithium iron phosphate (LFP) cells, while simultaneous gains in stationary storage and two-wheeler electrification create overlapping demand streams. Precursor joint ventures such as POSCO FUTURE M–GM and Ecopro BM–BMW expose how feedstock security now eclipses scale alone as a competitive lever. Regionally, Asia-Pacific will maintain its dominance as Indonesia’s downstream-nickel mandates and Vietnam’s assembly incentives accelerate local tonnage, whereas North American growth hinges on Inflation Reduction Act production credits. Emerging sodium-ion and LMFP chemistries broaden the cathode materials market addressable base, ensuring that lower-cost formulations complement premium NMC and NCA offerings.

Key Report Takeaways

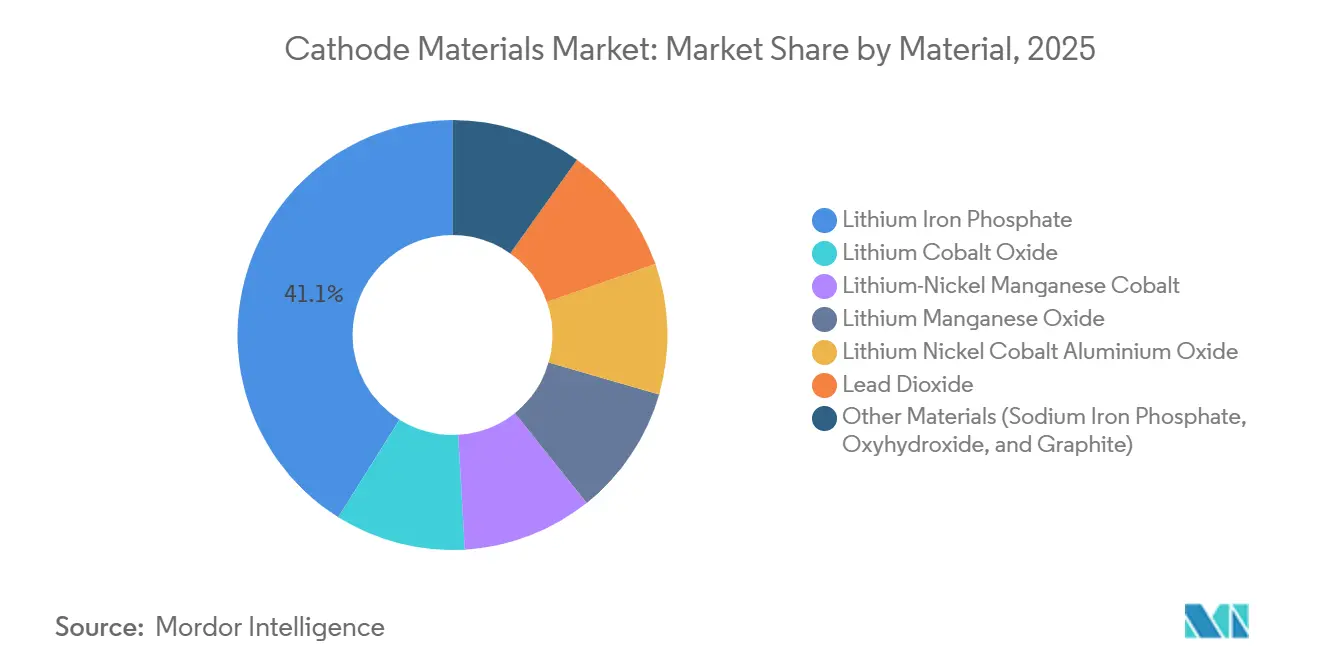

- By material, lithium iron phosphate led with 41.10% of cathode materials market share in 2025 and is forecast to post the quickest 24.97% CAGR through 2031.

- By battery type, lithium-ion accounted for 88.20% of demand in 2025 and is advancing at a 25.62% CAGR through 2031.

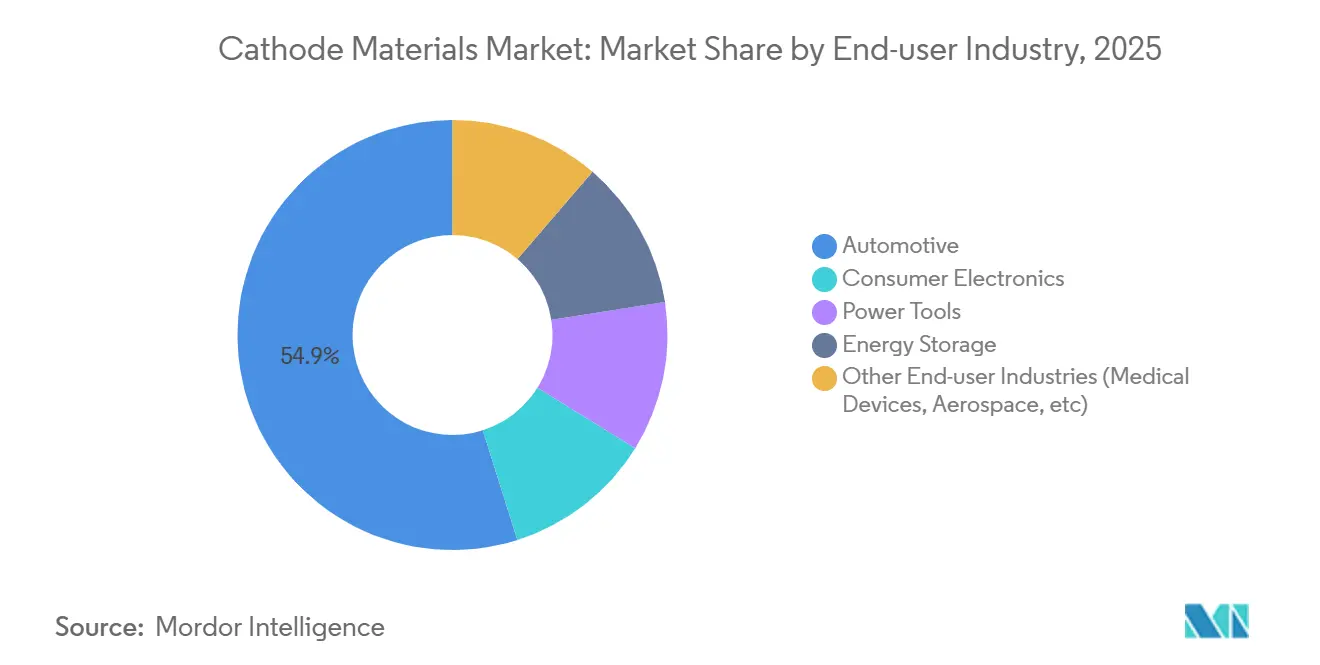

- By end-user industry, automotive held 54.90% volume share in 2025 and is advancing at a 25.18% CAGR through 2031.

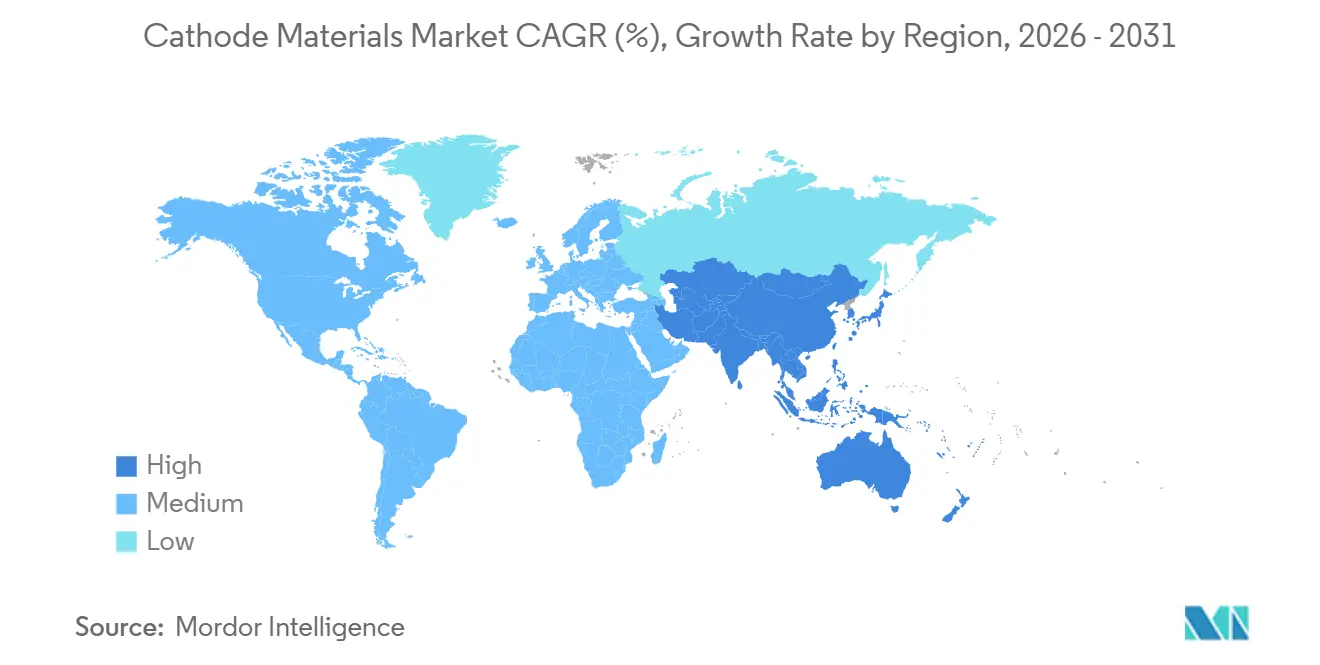

- By geography, Asia-Pacific captured 79.10% of 2025 tonnage and is set to expand at a 26.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cathode Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV Production Volumes | +6.8% | Global, with concentration in China, EU, and North America | Medium term (2-4 years) |

| Government Incentives and Emissions Regulations | +4.3% | North America, EU, China, India | Short term (≤ 2 years) |

| Battery-Pack Cost Decline from Scale Learning | +3.6% | Global, led by Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Localization of Cathode Supply Chains in US and EU | +2.9% | North America, EU | Medium term (2-4 years) |

| Sodium-Ion and LMFP Commercialization Expanding Demand | +2.4% | APAC core, spill-over to emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging EV Production Volumes

Global electric-vehicle output climbed to 13.8 million units in 2025 and is predicted to exceed 22 million by 2028, a trajectory that lifts cathode demand because every 60 kWh pack embeds 8–12 kg of active material. BYD plans to double 2024 volumes by manufacturing 4 million plug-ins in 2026, underscoring scale expansion across Asia. The switch to larger-format cells such as CATL’s Qilin increases cathode loading per vehicle by thickening electrode coatings. Fleet electrification adds another layer, illustrated by UPS ordering 10,000 LFP-powered delivery vans in 2025. Commercial-vehicle duty cycles favor LFP longevity, providing counter-cyclical stability for the cathode materials market.

Government Incentives and Emissions Regulations

Section 45X of the U.S. Inflation Reduction Act grants USD 10 per kilowatt-hour for domestic cells and USD 45 for modules, triggering 18 U.S. gigafactory announcements totaling 550 GWh of capacity[1]U.S. Department of Energy, “Inflation Reduction Act Fact Sheet,” energy.gov . In Europe, the Battery Regulation mandates carbon-footprint declarations by 2027 and tightens thresholds by 2030, advantaging cathode plants tied to renewable power such as Umicore’s Nysa site, which sources 80% wind energy. China extended new-energy vehicle purchase-tax exemptions to 2027, sustaining demand in the world’s largest EV arena. India’s USD 2.4 billion Production-Linked Incentive for advanced cells lures Reliance Industries and Rajesh Exports, positioning South Asia as a new pole of cathode consumption.

Battery-Pack Cost Decline from Scale Learning

Average lithium-ion pack prices declined to USD 115/kWh in 2024, driven partly by lower cathode costs that account for up to 40% of a cell’s bill of materials. BASF’s 42,000 t/yr CAM plant in Germany leverages continuous co-precipitation to shave 18% off per-kilogram expense. Logistics efficiencies such as Sumitomo Metal Mining’s dedicated nickel-sulfate carriers cut freight outlays by 12% and cascade through bids on long-term contracts. Once total-cost-of-ownership parity is reached—forecast for Europe in 2027—cathode volumes must triple to satisfy mass-market adoption, expanding the cathode materials market footprint.

Localization of Cathode Supply Chains in US and EU

The U.S. Department of Energy awarded USD 3.5 billion to 25 battery-material projects, including Ascend Elements’ hydro-to-cathode recycling hub in Kentucky and Redwood Materials’ Nevada foil complex. Northvolt’s Ett plant in Sweden sources 60% of its NMC cathode from an adjacent BASF facility, shortening lead times from 12 weeks to 3 weeks. Europe aims for 550 GWh of cell capacity by 2030, translating to 1.1 million tons of cathode demand—eight times current regional output. South Korea classified cathodes as a national strategic technology, unlocking tax credits that pushed POSCO FUTURE M to green-light a 100,000 t/yr plant in Gwangyang.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Concentration in China | -1.9% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Solid-State Batteries Lower Cathode Mass/kWh | -1.4% | Japan, North America, select EU markets | Long term (≥ 4 years) |

| Processing Hurdles for High-Mn Chemistries | -1.2% | Global manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Concentration in China

China refined 78% of global lithium hydroxide and 93% of manganese sulfate in 2024, exposing Western automakers to delivery risk when domestic suppliers reprioritize local needs[2]U.S. Geological Survey, “Critical Minerals Outlook 2024,” usgs.gov . Ford postponed its F-150 Lightning extended-range launch by four months in 2024 after a Chinese precursor partner diverted shipments during a lithium shortage. U.S. defense assessments warn that a Taiwan Strait conflict could choke cathode flows, while European players like Volkswagen’s PowerCo rely on China for 82% of NMC precursor. Building a 20 kt/yr precursor plant costs USD 150 million and 30 months, which slows diversification. Compliance with the Uyghur Forced Labor Prevention Act obliges automakers to trace multi-tier suppliers, adding administrative overhead.

Solid-State Batteries Lower Cathode Mass/kWh

QuantumScape’s ceramic-electrolyte cell tolerates 4.5 V operation and trims cathode mass by 28% per kWh, potentially curbing future tonnage if adoption accelerates. Toyota’s prototype delivers 1,200 km of range using only 1.4 kg of cathode per kWh, compared with today’s 2 kg baseline. Even if solid-state captures 15% of EV sales by 2032, cathode demand would fall against a liquid-electrolyte scenario. Manufacturing scale is nascent: Solid Power produced only 15 MWh in 2024, and interfacial resistance remains triple target levels. High capital outlays—USD 800 million for 1 GWh/year—further slow mainstream penetration, but the technology sets a ceiling on long-run cathode materials market volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: LFP Gains Scale, NMC Retains Premium Position

Lithium iron phosphate accounted for 41.10% of 2025 volume and is anticipated to expand at 24.97% through 2031, reflecting Tesla and BYD adoptions that eliminated cobalt and nickel from mass-market models. BYD’s Blade pack narrowed the energy-density gap with NMC 622 to 15%, supporting broader acceptance. Premium brands still specify high-nickel NMC: BMW’s Neue Klasse uses NMC 811 at 285 Wh/kg, positioning the chemistry where 500-km range is non-negotiable. Lithium-nickel-cobalt-aluminum holds niche but profitable ground in long-range packs, although sliding cobalt prices erode its margin advantage. Lead dioxide continues in starter batteries yet will cede share as 12-V lithium replacements scale. Sodium iron phosphate’s slice will rise as sodium-ion cars launch in price-sensitive Asian markets, broadening the cathode materials market canvas.

By Battery Type: Lithium-Ion Dominance, Sodium-Ion Acceleration

Lithium-ion represented 88.20% of cathode demand in 2025 and are growing at 25.62% CAGR as grid storage layers onto automotive deployments. Tesla installed 3.9 GWh of Megapacks in 2024, underpinning LFP’s role in long-duration storage. Lead-acid retained a moderate share for SLI and telecom but faces a mild-hybrid transition to lithium variants. Sodium-ion demand is growing as CATL’s 160 Wh/kg cells find homes in city cars and data-center UPS. Flow batteries occupy a niche share but remain essential for 8+-hour storage, aligning with long-duration mandates in California. This diversification keeps the cathode materials market resilient against single-technology disruption.

By End-user Industry: Automotive Transformation Drives Growth

Automotive consumed 54.90% of tonnage in 2025 and will grow at 25.18% as Euro 7 effectively bans diesel passenger cars and U.S. CAFE rules tighten. GM’s zero-emission pledge implies 1.2 million tons of annual cathode at full scale, reinforcing automaker pull-through. Energy-storage is also advancing as utilities deploy batteries to firm renewables and arbitrage peak-off-peak spreads. Consumer electronics keeps a moderate share on larger smartphone batteries, while power tools and specialty medical segments round out demand. These diversified outlets insulate the cathode materials market from any single-sector slowdown.

Geography Analysis

Asia-Pacific commanded 79.10% of the market share in 2025 and is on a 26.34% CAGR trajectory to 2031, reflecting deep integration across mining, processing, and cell manufacturing. China anchors this ecosystem through cost advantages and proprietary process expertise, enabling sustained innovation velocity. South Korea and Japan provide complementary high-precision manufacturing and advanced material formulations, reinforcing regional dominance. Indonesia’s USD 15 billion in smelting investment and Vietnam’s decade-long tax holidays ensure Southeast Asia doubles as both precursor and assembly hub, reinforcing the cathode materials market’s eastward gravity.

North America demand is also growing on the back of Section 45X credits that de-risk domestic plants. The United States production is supported by BASF Ohio and Albemarle Kings Mountain, with Canadian capacity tripling once POSCO FUTURE M and Talon Metals commission assets. Mexico’s USD 2 billion influx from Ganfeng and Tianqi creates a near-shoring corridor that meets USMCA thresholds. These moves shrink delivery times and diversify the cathode materials market supply chain beyond Asia.

Europe is also rising as the European Battery Alliance bankrolls local output. Germany’s production in 2024 climbed with BASF Schwarzheide and Umicore Nysa, while the U.K. rebooted via Tata Chemicals’ 40,000 t/yr LFP project to serve JLR. South America’s lithium-rich Chile and Argentina export hydroxide feeding 22,000 tons of cathode precursor, and Morocco’s Bou-Azzer mine supplies cobalt sulfate to European sites. Middle-East and Africa hold lower share but own strategic raw materials that could reposition them as precursor exporters. Collectively, geographic diversification sustains the cathode materials market against regional shocks.

Regulatory Landscape

Cathode-material supply chains are being shaped by due diligence, traceability, and content requirements that extend upstream into cobalt, natural graphite, lithium, and nickel. In the European Union, the Batteries Regulation (Regulation (EU) 2023/1542) and its amendment via Regulation (EU) 2025/1561 tighten due-diligence expectations for economic operators involved in sourcing, processing, and trading these inputs, increasing compliance burdens for cathode and precursor cathode active material (pCAM) producers that sell into the EU.

In the United States, cathode material producers are managing both product stewardship and localization-linked incentive rules. The EPA issued a standardized assessment and a March 13, 2026 policy memorandum for Mixed Metal Oxide (MMO) cathode active materials under TSCA Section 5, pushing for more consistent lifecycle hazard evaluation and risk-management expectations for MMO-based cathodes. Separately, the IRA clean vehicle credit rules raise the 2026 battery component threshold to 70% North American manufacturing/assembly value, while allowing taxpayers to use the prior critical-minerals value-add approach through the end of 2026, which reinforces a near-term focus on auditable sourcing and regional content documentation for cathode and precursor inputs.

Value Chain Analysis

The cathode materials value chain runs from raw mineral extraction (lithium, nickel, cobalt, manganese, iron, phosphate) through chemical refining into battery-grade salts (for example, lithium hydroxide/carbonate and metal sulfates), then into precursor cathode active materials (pCAM) and final cathode active materials (CAM). It continues with electrode manufacturing, cell assembly, and pack integration for automotive and stationary storage. A key chokepoint sits in midstream conversion and purification steps, particularly lithium conversion between carbonate and hydroxide that is critical for high-nickel chemistries, and the co-precipitation and calcination stages that determine CAM consistency, yield, and impurity control.

Competitive positioning increasingly depends on controlling pCAM-CAM linkages, qualifying materials with OEMs and cell makers, and building redundancy outside China for both LFP and nickel-based supply. The market shows strong midstream concentration in China, which is pushing North American and European players toward vertically integrated projects and long-term offtake structures that connect refiners, CAM producers, and automakers. Recycling is also taking on a larger feedstock role in the chain, with black mass and recovered metal fractions feeding back into pCAM/CAM production to support cost, carbon footprint, and supply-security goals.

Competitive Landscape

The cathode materials market shows moderate concentration: CATL, LG Chem, POSCO FUTURE M, Umicore, and BASF together held about 52% capacity in 2025, leaving room for mid-tier challengers. Competitive strategy has shifted from volume to vertical integration, typified by CATL’s 10-year LFP license-plus-supply deal with Ford that locks in 120,000 t/yr. LG Chem’s stake in Liontown, plus downstream hydroxide and CAM expansions, captures value across every step. Recycling emerges as a cost-advantaged wedge; Redwood Materials recovers 95% of critical metals and re-sells precursor 20% below virgin benchmarks, enabling cell makers to meet low-carbon requirements while preserving margins.

Technology differentiation is equally important. BASF’s cobalt-free NMC with aluminum-titanium dopants, Ecopro BM’s radial-grain single-crystal NMC, and Mitra Chem’s iron-manganese-phosphate pilots illustrate the sprint toward cobalt elimination, high-voltage tolerance, and cost efficiency. Standards such as forthcoming IEC 62660-3 purity specifications will raise compliance costs and potentially disqualify non-aligned suppliers. Overall, incumbents protect share through feedstock security and R&D velocity, while startups exploit chemistry white space to penetrate the cathode materials market.

Cathode Materials Industry Leaders

BASF

LG Chem

Umicore

POSCO FUTURE M

Contemporary Amperex Technology Co., Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary whitespace is non-Chinese LFP cathode supply aligned with localization incentives and OEM qualification needs, as LFP expands in entry-level EVs and stationary energy storage where bill-of-material savings and cobalt-free sourcing are prioritized. 2026 project activity highlights the build-out: L&F completed construction of an LFP cathode plant in Daegu, South Korea (60,000 tons/year capacity cited), and EnergyX with Wildcat Discovery Technologies announced a USD 230 million LFP cathode manufacturing facility in Hooks, Texas. These investments point to opportunity for CAM suppliers that can deliver consistent LFP performance at scale while meeting regional content and traceability requirements.

Another opportunity set is Europe and India-focused supply-chain reinforcement driven by policy tools that encourage local component manufacturing and industrial ramp-up. The European Commission created the Battery Booster Facility via Decision (EU) 2026/1283 to support scale-up across the battery value chain, and a joint venture between XTC New Energy and Orano (Neomat CAM) announced a final investment decision to build a CAM plant in Dunkirk, France. In India, the government proposed an incentive scheme (around Rs 12,000 crore) targeting local manufacturing of battery components including cathode active materials, which creates room for new domestic CAM capacity and technology transfer partnerships that pair precursor availability, process know-how, and downstream demand visibility.

Recent Industry Developments

- April 2026: TSR Group and BASF agreed to cooperate on recycling of electric vehicle batteries in Europe, spanning dismantling and discharging end-of-life batteries and processing spent batteries into black mass. BASF linked the initiative to its Schwarzheide site, where it operates battery recycling for black mass production, and outlined added work on metal fractions and logistics. The collaboration strengthens recycled feedstock availability for battery-material production in Europe and supports cathode supply resilience as traceability and circularity requirements tighten.

- September 2025: BASF Battery Materials renewed a long-term cathode active materials supply agreement linked to its Schwarzheide CAM plant. BASF positioned Schwarzheide as a fully automated large-scale CAM production site in Europe, supporting customer qualification and delivery continuity. The renewal reinforces contracted offtake for European CAM capacity at a time when regional buyers are emphasizing localized and auditable supply chains.

- March 2025: Umicore announced separate precursor cathode active materials (pCAM) supply agreements with CNGR and Eco&Dream (E&D) to support EV battery customer contracts in North America and Asia. Securing pCAM inputs across multiple suppliers addresses a key bottleneck feeding CAM production and reduces procurement concentration risk. The agreements also reflect the growing role of upstream contracting in enabling cathode material scale-up alongside OEM and cell-maker demand commitments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers cathode materials used to manufacture rechargeable batteries, where demand is tracked by battery production needs across key end uses. Sizing is expressed in physical volume so shifts in chemistry mix can be captured without being distorted by metal price swings.

Scope exclusions: Standalone mining, upstream refining of base metals, and complete battery pack manufacturing are excluded unless directly tied to cathode material output.

Segmentation Overview

- By Material

- Lithium Iron Phosphate

- Lithium Cobalt Oxide

- Lithium-Nickel Manganese Cobalt

- Lithium Manganese Oxide

- Lithium Nickel Cobalt Aluminium Oxide

- Lead Dioxide

- Other Materials (Sodium Iron Phosphate, Oxyhydroxide, and Graphite)

- By Battery Type

- Lithium-Ion

- Lead-Acid

- Sodium-ion

- Flow batteries

- By End-user Industry

- Automotive

- Consumer Electronics

- Power Tools

- Energy Storage

- Other End-user Industries (Medical Devices, Aerospace, etc)

- By Geography

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Indonesia

- Vietnam

- Thailand

- Malaysia

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Turkey

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the demand pool and supply footprint using public statistics and technical references. Sources reviewed include International Energy Agency (IEA) battery and EV datasets, USGS mineral summaries, UN Comtrade trade flows for relevant chemicals and intermediates, World Bank macro indicators, and peer reviewed battery materials journals that track chemistry trends and performance tradeoffs.

We also use company annual reports, investor presentations, and plant announcements to understand capacity additions, commissioning timing, and debottlenecking activity. Where needed, paid subscriptions for company financials and intelligence, import export shipment level data, and patent databases were used to cross check production claims and technology direction. These examples are not exhaustive, and many other public sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to stress test the desk assumptions on chemistry mix, utilization, and near term supply constraints, and then to confirm what buyers and producers see as realistic run rate changes. Inputs were taken from cathode material producers, precursor suppliers, battery manufacturers, and downstream OEM and integrator stakeholders across APAC, EMEA, and the Americas to close gaps in publicly reported volumes.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 44% |

| Mid tier: 51% | Functional/Unit leaders: 32% | EMEA: 33% |

| Smaller Players: 16% | Managers: 54% | Americas: 23% |

Market-Sizing & Forecasting

The core model uses a top-down build where battery production and cell demand signals are converted into cathode material requirements using chemistry shares and intensity factors (tons per GWh), and then adjusted for typical scrap and yield loss. To keep the outcome grounded, we corroborate totals with selective bottom-up approximations such as sampled producer capacity roll ups, utilization ranges, and indicative output per line, followed by ASP sanity checks only as a reasonability layer.

Key inputs used include regional battery cell manufacturing capacity additions, EV and energy storage deployment rates, cathode chemistry mix shifts (LFP versus NMC and other blends), typical cathode loading levels by chemistry, and changes in local policy support that pull forward manufacturing in specific countries. Forecasting is done through scenario analysis supported by simple time-series smoothing on the main drivers, and then the output is reviewed with interview feedback so short term spikes and commissioning delays are not overstated. Where a player level volume is not directly disclosed, gaps are handled through capacity based ranges that are narrowed using trade flows and plant ramp profiles.

Data Validation & Update Cycle

Validation is done by checking the modeled tonnage against independent signals such as battery production statistics, cathode precursor trade movements, and announced commissioning milestones, and then investigating any large variance before final sign off. Our team runs anomaly checks on chemistry mix shares, regional splits, and year over year step changes, and a second analyst review is completed to confirm that assumptions are consistent across sections.

Reports are refreshed annually, and interim updates are triggered when there are material events like large plant delays, major policy changes, or step changes in EV demand. Prior to delivery, a final pass is completed so the latest public releases and any follow up needed to resolve conflicts are reflected in the numbers.

Mordor Intelligence's Cathode Material Market Size Versus Other Published Estimates

It is normal to see different market size numbers for cathode materials because some publishers size in USD value while others track physical output, and the results move in different ways when metal prices and chemistry mix change. Differences also come from what is counted as cathode material output versus upstream precursors, and whether near term commissioning delays are built into the base year.

Key gaps usually show up in the unit of measure, the treatment of scrap and yield loss, and how quickly LFP and high nickel blends are assumed to shift across regions. Some estimates also apply a single global price curve and then convert currencies using annual average rates, which can widen the spread when there are sharp raw material price moves.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.91 M (2025) | |

| Global Consultancy A | USD 27.83 B (2023) | Reported as revenue in USD, which can inflate the apparent market size during high nickel and cobalt price periods, and it may also group broader battery value chain items beyond cathode output. |

| Industry Publisher B | USD 52.21 B (2026) | Uses a later base year with aggressive ramp assumptions for new capacity and typically applies value and volume conversions that depend heavily on assumed ASP by chemistry and region. |

The table indicates that the largest spread comes from mixing value based sizing with volume based sizing, along with different timing assumptions around plant ramp ups. By keeping the estimate in tons and applying explicit loss factors before any price checks are used, the demand pool stays tied to battery output signals, which is the modeling choice applied in Mordor Intelligence.

Key Questions Answered in the Report

What CAGR is projected for global cathode demand between 2026 and 2031?

The cathode materials market is forecast to grow at a 24.15% CAGR over 2026-2031, and reach 14.32 million tons by 2031 growing from 4.85 million tons in 2026.

Which chemistry will lead volume growth through 2031?

Lithium iron phosphate is set to expand at 24.97% CAGR, the quickest among all material types.

How will regional supply diversify beyond Asia?

North America and Europe are adding more than 500 GWh of cell capacity backed by Section 45X and EU Battery Regulation incentives, underpinning new cathode plants in the United States, Canada, Sweden, and Poland.

How concentrated is supplier power today?

The top five producers hold about 52% of global capacity, reflecting moderate concentration and leaving room for mid-tier and recycling-based entrants.

Page last updated on: