Peru Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

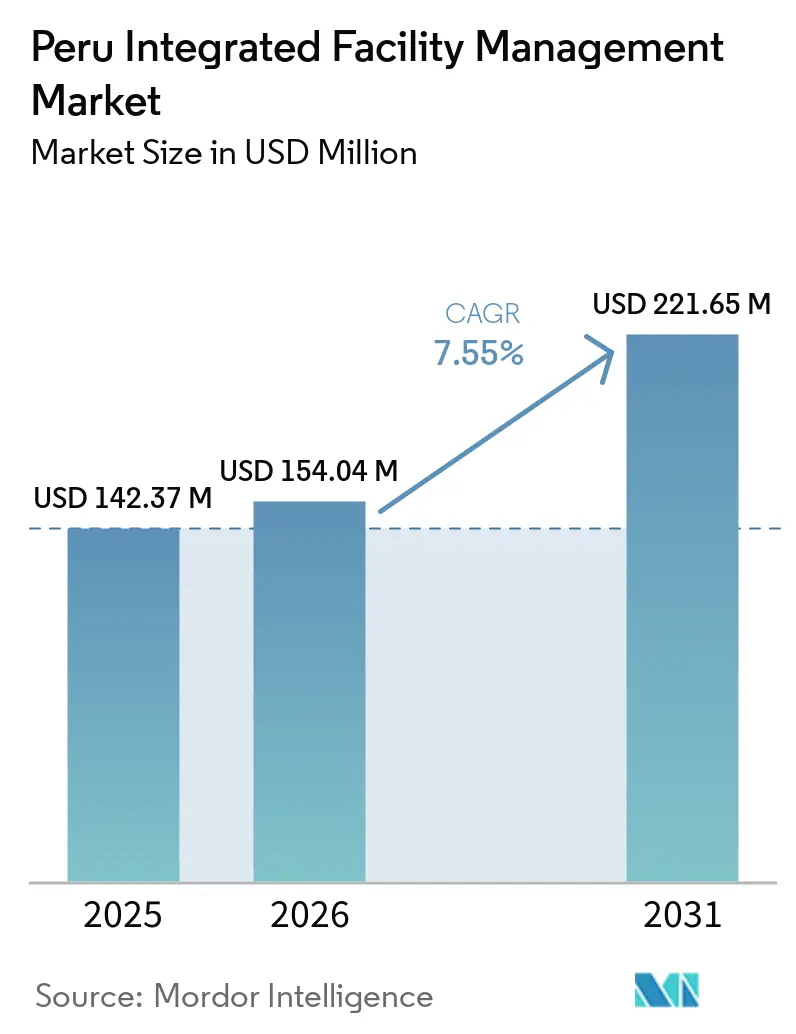

| Base Year Market Size (2025) | USD 142.37 Million |

| Market Size (2026) | USD 154.04 Million |

| Market Size (2031) | USD 221.65 Million |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

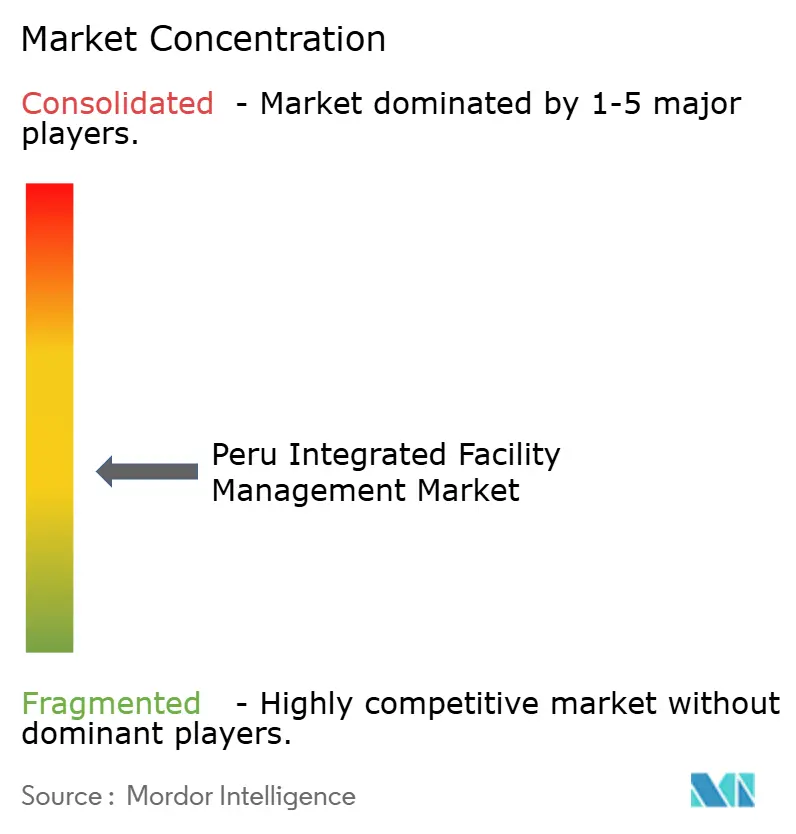

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peru Integrated Facility Management Market Analysis by Mordor Intelligence

The Peru integrated facility management market size is projected to expand from USD 142.37 million in 2025 and USD 154.04 million in 2026 to USD 221.65 million by 2031, registering a CAGR of 7.55% between 2026 to 2031. The Peru integrated facility management (IFM) market is shaped by two demand centers that reinforce each other, large urban assets in Lima and remote industrial operations tied to mining and energy. Peru’s large mining base gives the market a durable service layer that is less exposed to office cycles alone, because camps, plants, logistics points, and support infrastructure require continuous bundled services. Urban development in Lima and secondary cities is also raising the number of commercial, healthcare, and institutional buildings that need outsourced maintenance, cleaning, security, and compliance support. Building quality is becoming more important as owners compete on uptime, efficiency, tenant experience, and sustainability performance rather than on space additions alone. Competition remains moderately fragmented, and providers that combine technical depth, remote-site execution, and workforce training are better placed to capture longer-tenor contracts as the Peru IFM market matures.

Key Report Takeaways

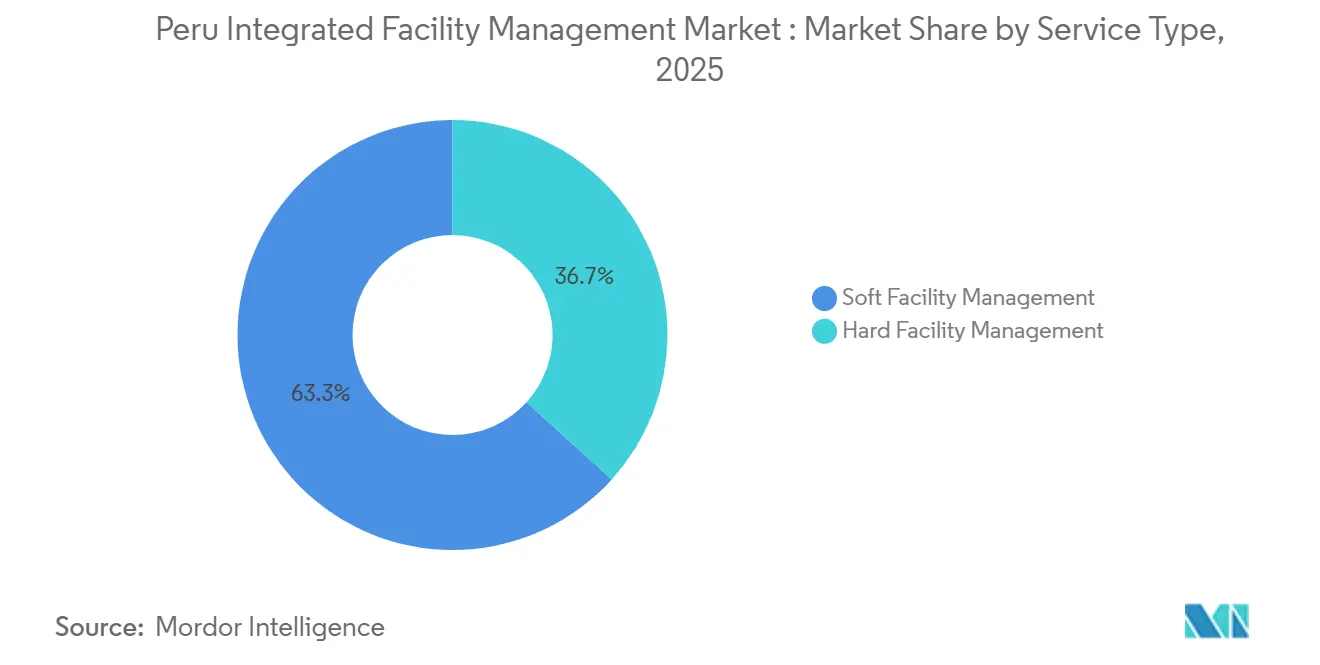

- By service type, soft facility management led with 63.27% of the Peru integrated facility management market size in 2025, while hard facility management is forecast to expand at an 8.01% CAGR through 2031.

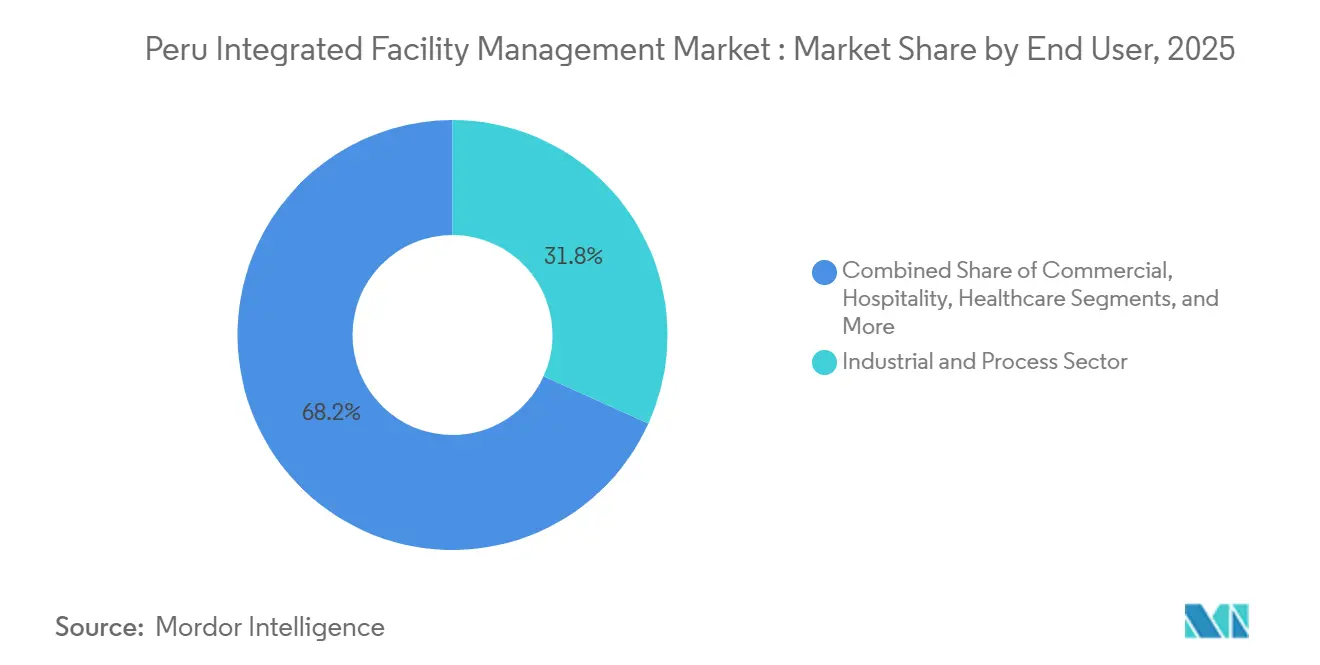

- By end-user, Industrial & Process Sector held 31.76% share of the Peru integrated facility management (IFM) market share in 2025, while Commercial recorded the highest projected CAGR at 8.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Peru Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth Of Mining And Energy Projects Requiring FM | +2.3% | Southern macro-region, including Apurímac, Arequipa, and Cajamarca, with spillover to northern departments | Long term (≥ 4 years) |

| Accelerating Urbanization Of Peru's Cities And Infrastructure | +1.8% | Lima Norte, Lima Este, Callao, and secondary cities such as Arequipa, Trujillo, and Chiclayo | Medium term (2-4 years) |

| Expansion Of Office Space And Real Estate Across Lima | +1.4% | Lima, including San Isidro, Miraflores, Surco, and San Borja, with early gains in Ate and Surquillo | Short term (≤ 2 years) |

| Energy Demand And Energy Efficiency In Buildings | +1.1% | National, with early gains in Lima and major mining hubs | Medium term (2-4 years) |

| Post-Pandemic Focus On Indoor Air Quality | +0.7% | Lima metropolitan area and healthcare facilities nationally | Short term (≤ 2 years) |

| Integration Of Smart Building And IoT Platforms In New Developments | +0.5% | Lima prime office districts and new mining camp infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of Mining and Energy Projects Requiring Integrated FM

Peru’s 2025 mining investment portfolio included 67 construction projects worth USD 64.071 billion, up by USD 9.515 billion from the prior portfolio and spread across 19 departments, which keeps a wide pipeline of site-based support needs active across the forecast period.[1]Ministerio de Energía y Minas, “Cartera de Proyectos de Inversión Minera 2025,” Ministerio de Energía y Minas, gob.pe The government also stated in 2025 that it aimed to secure more than USD 8.5 billion in new mining investments for 2025 and 2026, which supports near-term contract formation around camps, utilities, security, and site maintenance before full production begins. Remote mining and energy sites require bundled services such as catering, camp management, laundry, security, maintenance, and waste handling, and those services are operational requirements rather than discretionary spending items. That operating model gives the Peru IFM market a steadier revenue base than a purely office-led market, because remote industrial contracts are usually broader in scope and more difficult to replace with in-house teams. It also raises the value of vendors that can meet health, safety, environmental, and asset-reliability expectations at isolated sites where service failure can interrupt production. As more mines move from investment planning into construction and commissioning, the Peru IFM market should continue to tilt toward longer-tenor industrial accounts with higher service intensity.

Accelerating Urbanization of Peru's Cities and Infrastructure

The Metropolitan planning framework for Lima Norte projected the sub-region’s population at 3.6 million by 2034 and set out a more intensive pattern of logistics, commercial, and institutional development that will require organized building services and asset upkeep. The same planning direction points to a larger built environment in northern Lima, where denser urban use creates recurring demand for cleaning, security, reception, technical maintenance, and waste management across mixed-use facilities. Lima’s employed population rose 3.0% in 2025 to 5.62 million, and the services sector alone added 92,200 jobs, which means more daily occupancy across offices, public buildings, retail corridors, and transport-linked facilities.[2]Instituto Nacional de Estadística e Informática, “Población Ocupada En Lima Metropolitana Creció 3,0% En El 2025,” Instituto Nacional de Estadística e Informática, gob.pe The opening of new airport and logistics capacity strengthens this pattern, because urban growth now extends beyond central office districts into broader service and distribution nodes that need professional operations support. For the Peru integrated facility management market, this means demand is broadening across more building types instead of staying concentrated in a narrow set of premium office assets. As urban assets become denser and more technically demanding, outsourced integrated contracts become easier to justify on cost control, uptime, and service consistency.

Expansion of Office Space and Real Estate Across Lima

Lima’s office market improved through 2025, and JLL’s market reporting showed stronger absorption and a tighter supply environment, which supports a more favorable backdrop for outsourced building services in prime assets. The International Finance Corporation invested USD 40 million in Fibra Prime in December 2025 to support its 2025 and 2026 expansion plan focused on sustainable Class A office acquisitions in Peru.[3]International Finance Corporation, “IFC Invests USD 40 Million In Fibra Prime To Boost The Development Of Peru’s Real Estate Market,” International Finance Corporation, ifc.org That transaction matters for the Peru integrated facility management market because institutional owners tend to link property value more closely with energy performance, maintenance standards, tenant retention, and measurable service outcomes. When the new supply pipeline stays constrained, landlords compete more through building quality and workplace experience than through new square footage alone, and that shifts FM from a support expense toward an asset-protection function. This is one reason the Peru IFM market is drawing more interest in contracts that combine soft services, technical upkeep, and sustainability reporting within one operating model. Owners that want higher occupancy and stronger rent resilience are more likely to prefer professional service platforms over fragmented vendor management.

Energy Demand and Energy Efficiency in Buildings

Peru strengthened the regulatory basis for more efficient buildings when the Ministry of Housing approved the Technical Code of Sustainable Construction in 2024, bringing energy, water, and environmental quality into a clearer compliance framework. The Ministry of Housing also issued Resolution No. 139-2025-VIVIENDA, which modified the glazing standard for buildings and expanded mandatory structural, thermal, acoustic, and fire requirements. These rule changes increase the operational importance of inspections, HVAC optimization, commissioning, retrofits, and performance tracking, all of which support recurring technical work for integrated providers. IFC’s investment in Fibra Prime also included technical advisory under the GRIP program to support a building decarbonization strategy, showing that large institutional owners are treating energy outcomes as a practical operating priority rather than a branding exercise. For the Peru integrated facility management (IFM) market, this supports a gradual move toward contracts tied not only to service delivery but also to measurable asset performance and compliance readiness. Providers with engineering capacity and reporting discipline should therefore be in a stronger position than firms that focus only on labor-based services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Qualified FM Personnel And Technical Workforce | -0.8% | National, most acute in Lima, Arequipa, and remote mining regions | Medium term (2-4 years) |

| Regulatory Compliance Barriers And Permitting Complexity | -0.4% | National, with elevated impact in mining and public-sector healthcare facilities | Long term (≥ 4 years) |

| Water And Macroeconomic Conditions Impacting Private Sector Investment Cycles | -0.2% | Mining-dependent departments such as Cajamarca and Apurímac | Medium term (2-4 years) |

| Limited Awareness Of Total Integrated Contract Value And Pricing Structures | -0.2% | National, particularly among SME clients and public institutions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Qualified FM Personnel and Technical Workforce

The Federal Reserve Bank of Richmond found that Peru’s labor market tends toward generalist hiring because of high worker reallocation, which creates a poor fit for technical FM roles that require specific certifications and repeatable site processes. The same research noted an average vacancy duration of 9.1 days, which signals fast hiring activity but does not imply that employers are filling specialist roles with equally qualified candidates. In the Peru integrated facility management market, that gap matters most in Hard FM, where MEP maintenance, fire protection, and energy-management tasks depend on certified technical staff rather than interchangeable labor pools. APEFAM has been working since 2019 to build the profession through ISO 41001:2018 alignment, training programs, and sector recognition, which shows that the skills shortfall is real enough to require organized industry action. The issue is likely to become more visible as hospitals, airports, mines, and higher-grade offices all seek more technical service coverage at the same time. Providers that build internal academies or secure exclusive training partnerships should therefore gain a practical advantage in service quality, staffing stability, and bid credibility.

Regulatory Compliance Barriers and Permitting Complexity

Large public healthcare projects in Peru are expanding, but they also raise the operational burden on FM providers because these facilities include extensive auxiliary systems, technical areas, and support functions that must meet strict public-sector requirements. ANIN’s La Caleta Hospital project in Chimbote included more than 56,000 sqm, 394 beds, 11 operating rooms, and full support units such as laundry, maintenance workshops, and cold chain facilities, which illustrates the complexity of new institutional assets entering the pipeline.[4]Autoridad Nacional de Infraestructura, “ANIN Inicia Construcción Del Nuevo Hospital La Caleta Para Fortalecer Los Servicios De Salud En Chimbote,” Autoridad Nacional de Infraestructura, gob.pe Housing regulations are also tightening, and the 2025 update to the glazing standard widened the compliance scope around structural, thermal, acoustic, and fire performance in buildings. Mining-linked facilities sit in an equally demanding environment because projects are large, remote, and closely tied to formal investment, safety, and environmental processes. This combination lengthens mobilization, documentation, and onboarding for integrated contracts, which tends to favor firms with local compliance depth over smaller operators with limited back-office capacity. As a result, compliance is not only a cost issue in the Peru integrated facility management (IFM) market, but also a scaling barrier that shapes which firms can move from single-site work into multi-asset portfolios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Outpacing Soft Facility Management On Technical Intensity

Soft FM held 63.27% of the Peru integrated facility management market share in 2025, which shows that cleaning, security, catering, and front-of-house services still form the main revenue base for providers operating in the country. These services gained commercial adoption earlier because they require less specialized capital equipment, can be mobilized faster, and are easier for buyers to outsource in stages. Security has become especially important in industrial accounts, and Securitas Peru stated in 2025 that it allocated 20% of its investment portfolio to the mining and energy sector. Catering also remains central to remote-site operations, with the USDA reporting that Peru’s food service segment grew 26% by July 2025, supported by mining, construction, and institutional demand. As Lima’s workplace stock expands and institutional assets formalize operations, additional soft services such as shuttle coordination, reception support, and document handling are also becoming more relevant to bundled contracts.

Hard FM is projected to grow at an 8.01% CAGR through 2031, making it the most dynamic part of the Peru IFM market size over the forecast period. The reason is straightforward, newer mines, higher-specification hospitals, and better-grade offices all need reliable MEP maintenance, fire systems management, asset lifecycle planning, and performance monitoring instead of reactive repair alone. The 2025 update to Peru’s glazing standard widened the technical scope around thermal, acoustic, and fire compliance, which should raise commissioning and ongoing maintenance needs in new and upgraded buildings. IFC’s decarbonization support for Fibra Prime also points to a broader move toward performance-led operations, where owners expect documented energy and building-efficiency outcomes from service partners. In that context, the Peru integrated facility management industry is likely to reward firms with in-house engineering depth more than firms that rely only on labor-intensive soft service models.

By End-User: Industrial Leads While Commercial Demand Builds

Industrial and Process Sector accounted for 31.76% share of the Peru integrated facility management market share in 2025, reflecting Peru’s strong dependence on mining and resource-linked operations as a base for integrated services demand. The mining project portfolio reached USD 64.071 billion in 2025 across 67 projects, and that pipeline creates recurring needs for camps, power support, maintenance, catering, laundry, transport coordination, and security at isolated work sites. Newrest stated that it operates in more than 80 mining and oil and gas operations in Peru, which shows how remote-site specialists have already built scale around industrial accounts. The government’s 2025 push to secure more than USD 8.5 billion in additional mining investment for 2025 and 2026 further supports future contract creation in regions where professional providers are still building coverage. This industrial base gives the Peru IFM market a structural layer of demand that is less sensitive to short office leasing cycles and more tied to long-duration operating assets.

Commercial is projected to expand at an 8.18% CAGR through 2031, making it the fastest-growing end-user segment in the Peru integrated facility management market. IFC’s USD 40 million investment in Fibra Prime supports sustainable Class A office acquisitions and a decarbonization roadmap, which should raise the service expectations attached to professional office buildings in Lima. Healthcare is also becoming a larger contributor, because Peru’s hospital modernization drive includes major projects such as Sergio Bernales and La Caleta that require laundry, sterilization support, technical maintenance, waste handling, and compliance management over long operating lives. Hospitality and institutional demand add another layer, with the USDA reporting 29 new hotels under construction and USD 650 million in private investment, which expands the base for outsourced housekeeping, maintenance, catering, and guest-support functions. Together, these shifts show that the Peru integrated facility management industry is no longer driven only by heavy industry, because formal commercial and public assets are steadily widening the service mix.

Geography Analysis

Lima remains the core geography for the Peru integrated facility management market because it concentrates the country’s largest stock of Class A offices, institutional buildings, healthcare assets, and corporate service activity. IFC’s December 2025 investment in Fibra Prime confirmed that Lima is still the main center for institutional office expansion and sustainability-linked real estate management. The city’s employed population increased 3.0% in 2025 to 5.62 million people, and the services sector added 92,200 jobs, which points to heavier daily use of commercial and public facilities. New hospital projects, airport-linked activity, and urban expansion across Lima Norte are increasing the number of facilities that need structured operations support from commissioning into routine service delivery.

Southern Peru is the most important non-Lima zone for Hard FM and remote-site services, because Apurímac, Arequipa, and Cajamarca together accounted for 45.5% of Peru’s total mining investment portfolio in 2025. Major projects such as Tía María, Ferrobamba Replacement, and Corani extend the industrial pipeline into 2027 and 2028, which supports future demand for camps, maintenance infrastructure, utilities support, and perimeter security. This makes the southern corridor especially important for providers that can mobilize technical teams to isolated sites and maintain consistent service levels under demanding operating conditions. Northern Peru is building a different kind of demand base around logistics and industrial expansion, with Lima Norte planning tied to larger trade and transport flows. That mix favors integrated vendors that can support warehousing, transport facilities, processing spaces, and related support buildings under one service platform.

Secondary cities remain smaller contributors, but they are becoming more relevant to the Peru integrated facility management market as newer healthcare and transport assets move closer to operation. The Antonio Lorena Hospital in Cusco reached 54% completion in May 2025, showing that complex institutional assets are no longer limited to the capital. ACCIONA’s April 2026 contract to construct the new Chinchero-Cuzco airport control tower adds another long-cycle asset in the south that will later require operations, maintenance, and safety-related support services. As these projects move from construction into commissioning and everyday use, providers looking beyond Lima should find more room to build local scale in healthcare, aviation, and public infrastructure support.

Competitive Landscape

The Peru integrated facility management market is moderately fragmented, with global groups holding many visible accounts while local specialists remain important in municipal, institutional, and remote-site delivery. Compass Group, ACCIONA, Cushman and Wakefield, JLL, Securitas, and Newrest operate beside local service firms that compete on staffing agility, geographic reach, and contract customization. ACCIONA has operated in Peru since 1998, and its April 2026 airport control tower contract in Chinchero shows how infrastructure relationships can create longer-term openings in operations and maintenance services. The company’s broader engineering profile gives it an advantage in complex assets where owners want one provider with construction understanding, technical systems familiarity, and lifecycle support capability. This is one of the reasons the Peru integrated facility management (IFM) market still allows scale players to defend premium accounts even though no single operator dominates the country.

Cushman and Wakefield explicitly offer integrated facilities management and smart building solutions in Peru, which reflects the growing role of data-led operations in higher-grade commercial properties. JLL’s Lima market reporting also supports the case for engineering-led building management as office conditions tighten and owners focus more on property performance. Newrest strengthened its regional position in 2025 by becoming a Platinum Associate of APEFAM and by announcing an agreement to acquire Compass Group’s operations in Chile, Colombia, and Mexico. That move suggests that the middle layer of the Peru integrated facility management market is becoming more competitive as regional operators seek both scale and professional credentialing. Local providers continue to matter because they can price more flexibly, respond faster, and deploy teams into secondary cities or mining corridors where large firms may still depend on partnership networks.

Technology is becoming a clearer separator across the Peru IFM market, especially in high-risk industrial and event-security environments where visibility and response speed matter. Securitas Peru secured its third consecutive contract for Perumin 37 in 2025 and deployed more than 100 professionals supported by real-time video surveillance and drones for perimeter monitoring. APEFAM’s push around ISO 41001:2018 is also helping buyers compare providers on a more formal basis, which should gradually raise expectations around documented processes and performance controls. The result is a competitive field where global firms bring technical breadth and financing strength, while local firms and specialized operators can still win share through compliance discipline, site execution, and familiarity with Peru’s operating conditions.

Peru Integrated Facility Management Industry Leaders

CBRE Group, Inc.

Sodexo S.A.

ISS A/S

Compass Group PLC

Prosegur

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ACCIONA secured a USD 48 million contract to construct the control tower for the new Chinchero-Cuzco International Airport in Peru, covering seven structural levels, technical rooms, and full electromechanical and fire suppression systems, extending ACCIONA's Peruvian infrastructure-to-FM pipeline further into the tourism and aviation segment.

- April 2026: The government of Peru signed contracts for the modernization of the Manuel Nuñez Butrón Regional Hospital in Puno with an investment of nearly PEN 1.2 billion (USD 353 million), under a government-to-government agreement with France, targeting 296 beds and seven operating rooms, a facility that will generate long-term healthcare FM contracting demand in southern Peru.

- December 2025: The IFC invested USD 40 million in Fibra Prime, Peru's first and largest REIT, to support its 2025-2026 expansion plan focused on sustainable Class A office acquisitions, with technical advisory to develop a building decarbonization strategy, a transaction that will raise FM sustainability performance expectations across Lima's institutional real estate segment.

- November 2025: The Autoridad Nacional de Infraestructura initiated construction of the new La Caleta Hospital in Chimbote, covering over 56,000 sqm across 394 hospitalization beds, 11 operating rooms, and full auxiliary service units, including laundry, maintenance workshops, and cold chain, awarded to the Consorcio Sinohydro Corporation Limited Sucursal del Perú.

Peru Integrated Facility Management Market Report Scope

The Peru Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the size outlook for Peru integrated facility management through 2031?

The Peru integrated facility management market was valued at USD 142.37 million in 2025, stood at USD 154.04 million in 2026, and is projected to reach USD 221.65 million by 2031 at a 7.55% CAGR.

Which service category is largest in Peru?

Soft facility management led the revenue mix with 63.27% share in 2025, supported by strong demand for cleaning, security, catering, and workplace support across commercial and industrial sites.

Which service category is growing fastest in Peru?

Hard facility management is expected to expand at an 8.01% CAGR through 2031, helped by demand for MEP maintenance, fire systems, compliance work, and asset performance support in mines, hospitals, and better-grade offices.

Which end-user segment has the strongest current position?

Industrial and Manufacturing/Energy held 31.76% share in 2025, reflecting Peru's large mining base and the non-discretionary service needs of remote operational sites.

What is the main challenge for providers operating in Peru?

The biggest near-term constraint is the shortage of qualified technical FM personnel, because generalist hiring patterns make it harder for staff certified roles in Hard FM, healthcare, and remote industrial operations.

Page last updated on: