Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2026) | USD 134.32 Billion |

| Market Size (2031) | USD 161.43 Billion |

| Growth Rate (2026 - 2031) | 3.75% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Facility Management Market Analysis by Mordor Intelligence

The South America facility management market reached USD 134.32 billion in 2026 and is projected to advance to USD 161.43 billion by 2031, reflecting a 3.75% CAGR over the forecast period. Adoption of outsourced service delivery, extension of IoT-enabled building platforms, and regulatory pressure for formal labour contracts are converging to push organizations toward predictive, data-driven maintenance models. Brazil’s Sustainable Taxonomy now obliges listed enterprises to disclose climate-related risks, prompting landlords and industrial operators to embed energy-efficiency metrics in FM contracts, while Argentina’s deregulation wave has opened its market to multinational providers despite currency volatility. Hard services continue to dominate revenue because asset-intensive sectors such as mining and manufacturing depend on mechanical, electrical, and plumbing uptime, yet soft services are expanding faster as e-commerce logistics hubs and hospitality chains ramp up 24/7 operations. Competitive intensity is rising as global integrators deploy digital platforms, forcing smaller regional firms to modernize or risk displacement.

Key Report Takeaways

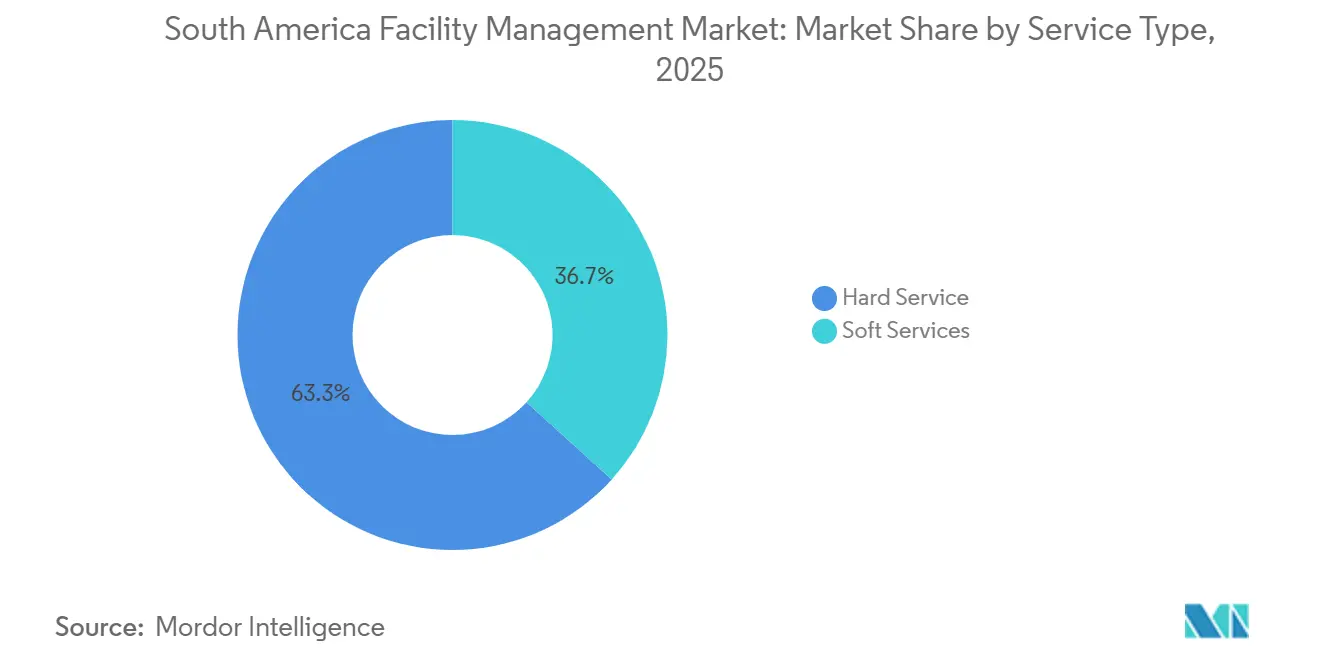

- By service type, hard services led with a 63.27% revenue share in 2025; soft services are projected to expand at a 4.01% CAGR through 2031.

- By delivery model, in-house delivery held 56.91% of the South America facility management market size in 2025, while outsourced models are forecast to grow at a 3.89% CAGR through 2031.

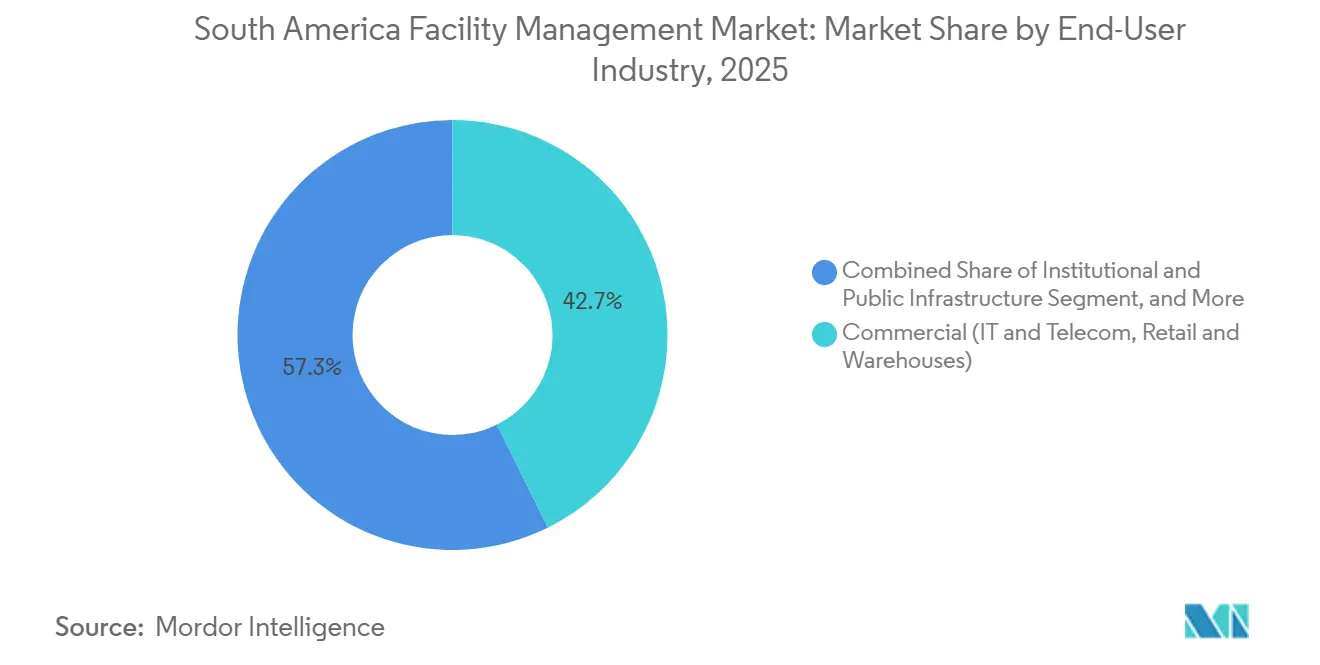

- By end-user industry, commercial facilities contributed 42.68% of revenue in 2025, whereas institutional and public infrastructure segments are expected to post the highest CAGR at 4.26% to 2031.

- By country, Brazil accounted for 40.19% of the South America facility management market share in 2025, and the Rest of South America cluster is poised to expand at a 4.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing Momentum | +0.90% | Brazil, Argentina, Chile strongest in São Paulo, Buenos Aires, Santiago metro areas | Medium term (2-4 years) |

| Technology Integration Across FM Workflows | +0.70% | Brazil (São Paulo, Rio de Janeiro), Chile (Santiago), Colombia (Bogotá) | Long term (≥4 years) |

| ESG-Aligned Facilities and Net-Zero Mandates | +0.60% | Brazil (federal and state mandates), Chile (renewable-energy commitments), Colombia | Medium term (2-4 years) |

| Demand for Integrated FM Contracts | +0.50% | Brazil, Argentina, Rest of South America, concentrated in commercial and institutional segments | Medium term (2-4 years) |

| Expansion of Edge and Micro-Data-Center Footprints | +0.40% | Brazil (São Paulo, Rio de Janeiro), Chile (Santiago), Colombia (Bogotá, Medellín) | Long term (≥4 years) |

| Nearshoring-Driven Industrial Facility Build-out | +0.50% | Brazil (automotive corridor in Minas Gerais, São Paulo), Argentina (Córdoba), Chile (Antofagasta mining region) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Outsourcing Momentum

Companies across South America are accelerating the shift from in-house teams to third-party facility managers to convert fixed payrolls into variable costs and access specialist skills in energy management, fire safety, and digital work-order systems. GPS Group reported that net revenue climbed 56% year-over-year to BRL 4.113 billion (USD 750 million) in Q3 2024 after winning thousands of new outsourced contracts.[1]GPS Group, “3Q 2024 Earnings Release,” gpsgroup.com.br Brazil’s updated labour code has tightened penalties for misclassifying workers, encouraging enterprises to formalize service relationships with FM suppliers that hold ISO 9001 certifications.[2]Presidência da República, “Decreto 12 705 de 2025, Taxonomia Sustentável,” planalto.gov.br Argentina’s deregulation package lowered wage floors and simplified dismissals, making outsourced delivery attractive even amid peso volatility. Mid-sized firms lacking procurement scale are therefore migrating to bundled service agreements that transfer compliance risk and introduce outcome-based pricing. The result is a consistent pipeline of multi-year FM tenders across manufacturing and logistics corridors.

Technology Integration Across FM Workflows

IoT sensors, computerized maintenance-management systems, and building-information modelling are redefining service delivery by enabling predictive maintenance that cuts downtime and extends asset life. ISS noted that 21 contract extensions in Q3 2025 included nine scope expansions tied to digital dashboards that combine work orders, energy use, and indoor-air-quality metrics, driving 4.9% organic growth and a 94% retention rate.[3]ISS A/S, “Q3 2025 Trading Update,” issworld.com Johnson Controls’ OpenBlue platform deployed in São Paulo and Santiago optimizes HVAC run-times via machine learning, reducing energy spend 15-20% while keeping comfort within ASHRAE Standard 55 thresholds.[4]Johnson Controls, “OpenBlue Case Studies,” johnsoncontrols.com Brazil’s metrology institute updated calibration guidelines in 2024 so that IoT endpoints meet traceability norms required for ISO 50001 audits. Despite these advances, a JLL survey showed technology adoption among South American FM users still trails the global average by roughly 10 percentage points due to capital constraints and limited Portuguese and Spanish vendor support. This technology gap gives multinational providers a clear advantage when bidding for large integrated contracts.

ESG-Aligned Facilities and Net-Zero Mandates

Climate-risk disclosure rules are forcing landlords and industrial operators to quantify and reduce Scope 1-3 emissions, creating demand for FM partners with robust sustainability toolkits. Brazil’s securities regulator has mandated IFRS S1 and S2 reports from fiscal 2026, compelling companies to track the carbon footprint of every building they own. FM contracts now bundle energy audits, LED retrofits, solar-panel installation, and refrigerant monitoring under performance-linked service-level agreements. Itaú Unibanco achieved ISO 14001 certification at its headquarters by installing 34 MWp of rooftop solar and diverting 98% of waste from landfills, demonstrating how FM partners can deliver measurable ESG outcomes. Chile’s energy strategy offers tax credits to commercial buildings that reach LEED Gold certification, further boosting demand for sustainability-focused FM expertise.

Demand for Integrated FM Contracts

Enterprises are consolidating fragmented service lines such as cleaning, security, catering, and HVAC under single, integrated agreements that tie payments to quantifiable outcomes. Cushman & Wakefield’s December 2025 extension with BHP covers 1.46 million square feet across 12 countries and links compensation to energy consumption per square meter, tenant-satisfaction indices, and compliance incidents. ISS reported that six new large accounts secured in H1 2025 featured integrated scopes, underpinning a 4.1% organic growth rate. Public bodies are following suit: the World Bank’s 2024 request for information for its Brasília campus required bidders to hold ISO 9001, ISO 14001, and ISO 45001 certifications and to provide consolidated governance structures. Integrated contracts reduce vendor-management overhead and align provider incentives with client business objectives, making them the fastest-growing service model across the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic Volatility and Currency Swings | -0.80% | Argentina (peso depreciation), Brazil (real fluctuations), regional exposure to commodity cycles | Short term (≤2 years) |

| Fragmented Regulatory Landscape Across Countries | -0.50% | Brazil (27 state-level fire codes), Argentina (provincial labor rules), Chile (municipal building permits) | Medium term (2-4 years) |

| Low Technology Adoption among Smaller FM Providers | -0.30% | Brazil (interior states), Argentina (provinces outside Buenos Aires), Paraguay, Bolivia | Long term (≥4 years) |

| High Informality within Facilities Services Labor Market | -0.40% | Brazil, Argentina, Peru, concentrated in cleaning, security, and residential services | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic Volatility and Currency Swings

Elevated inflation and sharp exchange-rate shifts compress contract margins and discourage long-term capital commitments. Argentina’s inflation hit 117% in 2024, forcing FM suppliers to renegotiate prices quarterly and index wages to consumer-price indices, while the peso’s slide from 350 to over 1,000 per USD strained firms with dollar-denominated debt. Brazil’s central bank lifted its policy rate to 14.75% in May 2025 to rein in services inflation, raising borrowing costs for FM companies financing equipment purchases. Commodity-price swings add to the uncertainty because national budgets tied to copper, iron ore, and soy exports influence public-sector FM spending. Such volatility forces providers to embed aggressive escalation clauses or adopt hedging strategies that can deter price-sensitive clients.

Fragmented Regulatory Landscape Across Countries

Divergent building codes, labour statutes, and environmental rules inflate compliance costs and impede scale efficiencies. Brazil’s 27 states maintain separate fire-safety standards, meaning FM technicians must train on multiple inspection protocols when servicing clients across state lines. Argentina’s provinces differ on overtime pay and union-bargaining frameworks, complicating national workforce planning. In Chile, municipal building-permit timelines range from 30 days in Santiago to six months in smaller communes, delaying facility handovers and the start of FM contracts. These discrepancies hamper the roll-out of standardized service models and increase back-office overhead for multinational operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Revenue Dominated by Asset-Intensive Hard Services

Hard services captured 63.27% of 2025 revenue as capital-heavy sectors such as mining, energy, and pharmaceuticals depend on continuous MEP uptime to avoid production losses and regulatory penalties. Within this slice of the South America facility management market, demand is buoyed by Chilean copper mines that require round-the-clock HVAC and compressed-air systems, and by Brazilian cleanrooms that must pass stringent GMP audits. Soft services, while smaller, are pacing future growth at a 4.01% CAGR as e-commerce hubs add cleaning, security, and catering shifts to serve 24/7 warehouse operations. Fire-safety services have risen in profile since the Kiss nightclub tragedy prompted stricter alarm and egress rules, though enforcement varies by municipality.

Soft services also benefit from hospitality’s rebound, with Brazilian hotel occupancy and revenue per available room nearing pre-pandemic peaks in 2025. However, persistent informality 69% of Brazilian residential-services workers lack formal contracts limits service quality and increases turnover. Cleaning and catering providers that offer structured training and certification are gaining share as clients demand higher hygiene standards. Overall, the South America facility management market size attached to soft services is therefore expanding faster than the hard-service base, yet the latter remains indispensable for regulatory compliance and asset preservation.

By Offering Type: Outsourcing Builds Momentum and Integrated Models Lead

In-house delivery still represented 56.91% of 2025 spending, reflecting the legacy preference of large industrial conglomerates and public hospitals for direct labour control. Vale, for example, maintains proprietary facility teams at its mining complexes to synchronize maintenance windows with production cycles. Nevertheless, outsourced models are forecast to rise at a 3.89% CAGR as clients convert fixed costs into variable fees and shift compliance risk to ISO-certified providers. Single-service contracts remain common among SMEs, but they elevate administrative overhead and obscure accountability when service gaps overlap.

Bundled contracts that group two or more services under one agreement offer a transitional step, while integrated FM contracts forecast as the fastest growing subsegment at roughly 4.2% embed strategic responsibility with a single supplier. Cushman & Wakefield’s BHP deal and ISS’s surge in key-account extensions illustrate how integrated scopes improve retention and lift margins. The South America facility management industry, therefore, sees integrated delivery gaining Favor among multinationals and public entities alike, aided by Brazil’s Federal Law 14,133/2021, which rewards performance-based contracting. As a result, the South America facility management market size derived from outsourced integrated arrangements is set to climb steadily through the decade.

By End-User Industry: Commercial Stock Leads, Institutional Growth Accelerates

Commercial assets offices, retail, warehouses, and data centers held 42.68% of 2025 revenue because they combine high occupancy densities with tenant-experience imperatives. São Paulo’s Class A warehouse vacancy of 7.7% in Q3 2025, the tightest since 2013, has pushed asking rents toward BRL 40 per square meter and intensified demand for dock-leveller maintenance, refrigeration checks, and around-the-clock cleaning. Data-center colocation facilities require uptime guarantees that meet Uptime Institute Tier III or IV standards, calling for FM specialists versed in N+1 redundancy and precision cooling.

Institutional and public infrastructure sites, government campuses, universities, and transport terminals are projected to expand at a 4.26% CAGR, the fastest among end-users, buoyed by PPP concessions such as São Paulo’s Campos Elísios urban-renewal project. Hospitals are outsourcing non-clinical functions to meet strict infection-control standards, while hotel chains capitalize on tourism’s rebound to restore pre-pandemic staffing levels. Consequently, the South America facility management market share of institutional users will rise even as the commercial segment maintains the largest absolute footprint.

Geography Analysis

Brazil commanded 40.19% of the market in 2025, supported by the continent’s largest building inventory and business hub concentrations in São Paulo and Rio de Janeiro. Net absorption in São Paulo’s office sector was 18% higher year-to-date versus 2024, and logistics hubs around Guarulhos and Cajamar recorded premium rents, underpinning demand for both hard and soft services. Resolution 193 obliges listed firms to adopt IFRS sustainability disclosures from 2026, further embedding ESG metrics into FM contracts. However, a fragmented state-level fire-code regime elevates compliance complexity and favours providers with broad regulatory expertise.

Argentina held an estimated 18% share in 2025 despite 117% inflation the prior year. President Milei’s deregulation removed sectoral price caps and simplified labour codes, facilitating market entry for multinational FM providers. Buenos Aires concentrates roughly 60% of national demand, while Córdoba’s automotive hub is upgrading production lines after the elimination of import quotas. Yet currency swings remain a headwind because most FM input costs are indexed to the U.S. dollar.

The Rest of South America segment Chile, Colombia, Peru, and smaller economies posted the fastest forecast growth at 4.07%. Chile’s 70% renewable-electricity target by 2030 offers tax incentives for LEED-Gold properties that hire green-focused FM firms. Google, AWS, and Oracle have all expanded data-center footprints in Chile and Brazil, catalysing specialized FM demand for precision cooling and fire suppression. Colombia’s net-zero roadmap requires a 30% cut in building energy intensity by 2030, creating openings for LED retrofit and building-automation projects. Peru’s mining camps sustain a steady need for catering and remote-site logistics, though social unrest can delay new projects.

Competitive Landscape

The South America facility management market is moderately fragmented, with the top ten providers controlling roughly 35-40% of revenue. Global integrators ISS, Sodexo, CBRE, Cushman & Wakefield, JLL compete on standardized processes, digital transparency, and multi-country coverage, often winning key-account contracts that bundle hard and soft services. GPS Group leads the regional specialist cohort after its 2024 acquisition of GRSA, lifting trailing-twelve-month revenue to BRL 16.96 billion and staffing to 187,000 employees. Niche firms such as Leadec Brazil and Brasanitas thrive in industrial and healthcare verticals where sector-specific certifications are mandatory.

Technology is the prime differentiator. ISS reports that digital work-order platforms raise retention to 94%, and Johnson Controls’ OpenBlue suite trims client energy use by up to 20%. Smaller local firms reliant on spreadsheets struggle to meet service-level guarantees, giving multinationals a performance edge. White-space opportunities persist in mid-tier cities where industrial parks lack integrated coverage, in hospitals migrating from in-house to outsourced FM, and in micro-data-center sites that require specialized cooling and security protocols.

Price pressure remains elevated because clients negotiate aggressive escalation clauses to offset inflation and currency volatility. Nonetheless, providers capable of combining predictive maintenance with ESG reporting and robust labour-compliance processes command premium margins. Consolidation is likely as regional specialists seek scale to fund technology upgrades and to match the cross-border reach of global rivals.

South America Facility Management Industry Leaders

Sodexo SA

ISS A/S

CBRE Group Inc.

Cushman & Wakefield plc

Brasanitas Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Cushman & Wakefield extended a global contract with BHP covering 1.46 million ft² across 12 countries, integrating hard and soft services under outcome-based KPIs for energy, tenant satisfaction, and compliance incidents.

- October 2025: ISS secured a new key-account contract valued above DKK 100 million annually, driving 4.9% organic growth and lifting retention to 94%.

- July 2025: ISS won a North American integrated FM deal exceeding DKK 100 million per year, highlighting scalability of its global digital platform.

- May 2025: Brazil’s central bank lifted the Selic rate to 14.75%, raising labour and equipment financing costs for FM suppliers.

South America Facility Management Market Report Scope

The South America Facility Management Market Report is Segmented by Service Type (Hard Services, Soft Services), Offering Type (In-house, Outsourced), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-user Industries), and Geography (Brazil, Argentina, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-User Industry

| Commercial (IT and Telecom, Retail and Warehouses) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

By Country

| Brazil |

| Argentina |

| Rest of South America |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-User Industry | Commercial (IT and Telecom, Retail and Warehouses) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Country | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the South America facility management market by 2031?

The market is expected to reach USD 161.43 billion by 2031, expanding at a 3.75% CAGR.

Which service category currently holds the largest revenue share?

Hard services, including MEP and HVAC maintenance, accounted for 63.27% of 2025 revenue.

Why are integrated FM contracts gaining popularity?

Integrated agreements reduce vendor-management overhead, tie payments to performance outcomes, and align with regulations that favor bundled service delivery.

How does ESG regulation influence facility management demand?

Mandated climate-risk disclosures and renewable-energy targets push building owners to hire FM partners that can track and reduce Scope 1-3 emissions.

Which country is forecast to grow fastest within the region?

The Rest of South America cluster Chile, Colombia, Peru, and neighboring markets is projected to post a 4.07% CAGR through 2031.

What technological capabilities differentiate leading FM providers?

Digital work-order platforms, IoT-enabled predictive maintenance, and real-time energy dashboards help providers cut downtime, lower costs, and meet ESG targets.

Page last updated on: