Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.34 Billion |

| Market Size (2026) | USD 4.44 Billion |

| Market Size (2031) | USD 4.97 Billion |

| Growth Rate (2026 - 2031) | 2.27% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Facility Management Market Analysis by Mordor Intelligence

The Chile facility management market size in 2026 is estimated at USD 4.44 billion, growing from 2025 value of USD 4.34 billion with 2031 projections showing USD 4.97 billion, growing at 2.27% CAGR over 2026-2031. This moderate pace reflects a maturing competitive landscape where post-pandemic workplace re-openings, a stronger regulatory push for energy efficiency, and rapid digital-infrastructure buildouts are reshaping service demand patterns. Large-scale cloud investments such as Amazon’s USD 4 billion regional cloud hub commitment have begun to elevate expectations for 24/7 critical‐environment support, while Chile’s Energy Efficiency Law is steering spending toward retro-commissioning and smart-building upgrades. Mining and renewable-energy CAPEX pipelines continue to broaden the opportunity set for providers able to work in remote, high-risk locations. At the same time, peso volatility and a nationwide shortage of certified HVAC and fire-safety technicians are compressing margins and accelerating the shift toward integrated contracts that spread risk across a broader service bundle. Together, these forces keep the Chile facility management market competitive yet primed for consolidation as global incumbents double down on high-growth verticals.[1]Ministerio de Energía, “Ley de Eficiencia Energética,” minenergia.cl

Key Report Takeaways

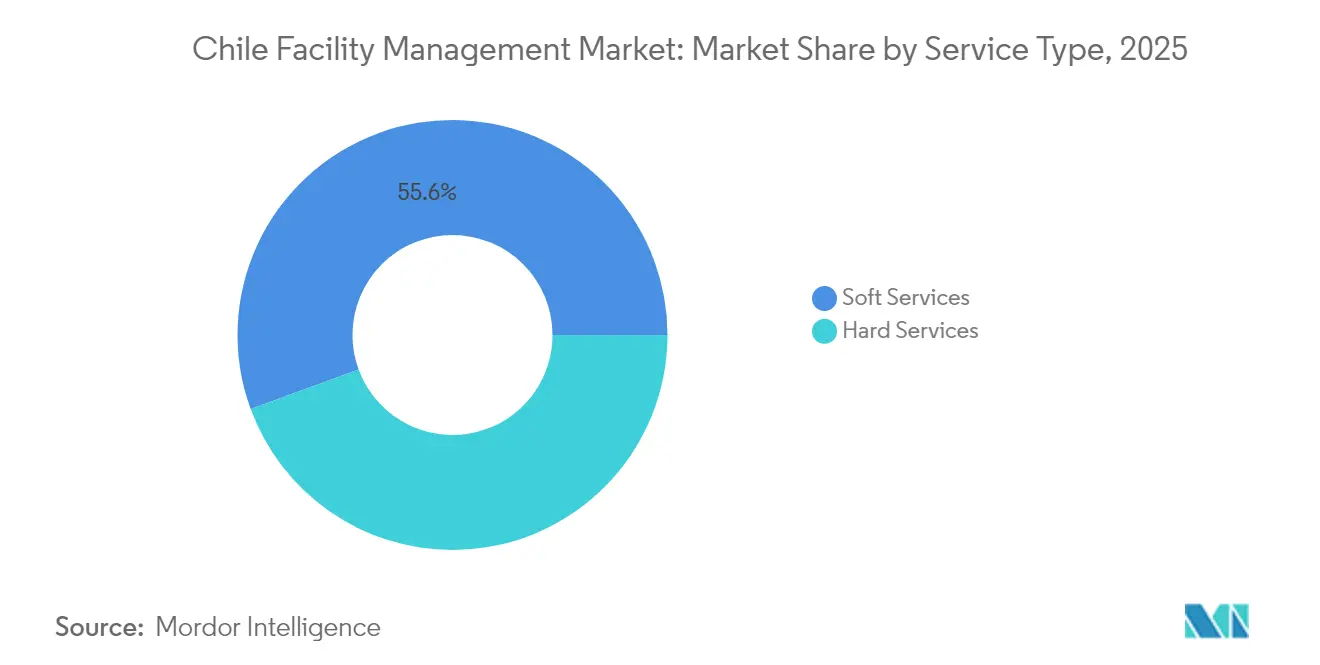

- Soft services held 55.60% of the 2025 Chile facility management market share, while integrated facility management is projected to expand at a 6.45% CAGR through 2031.

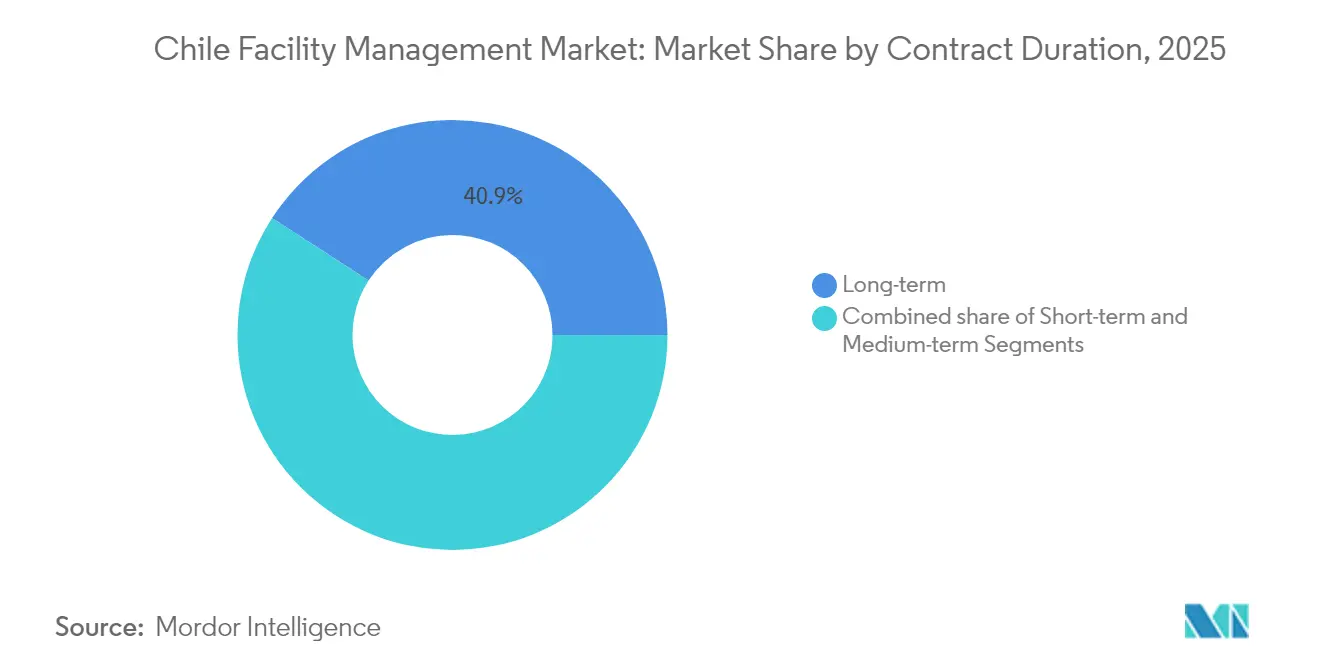

- Long-term agreements (longer than three years) captured 40.85% share of overall contract value in 2025; however, short-term contracts are advancing at a 5.63% CAGR as clients pursue flexibility.

- In-house delivery retained 63.75% share in 2025, yet outsourced integrated models represent the fastest-growing delivery mode with a 6.45% CAGR to 2031.

- The commercial segment led with 38.10% revenue share in 2025, whereas healthcare facilities are on track to post a 6.52% CAGR on the back of Chile’s active hospital construction program.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Grade-A office occupancy rates post-pandemic recovery | +0.80% | Santiago Metropolitan Region, with spillover to Valparaíso | Short term (≤ 2 years) |

| Corporate cost-optimisation pushing outsourcing penetration | +0.60% | National, with early gains in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Growth of mining and energy CAPEX boosting industrial FM demand | +0.70% | Northern Chile (Antofagasta, Tarapacá, Atacama) | Long term (≥ 4 years) |

| Mandatory energy-efficiency audits in public buildings drive retro-commissioning contracts | +0.40% | National, concentrated in Santiago and regional capitals | Medium term (2-4 years) |

| Expansion of Santiago data-centre footprint triggering 24/7 critical-environment FM demand | +0.50% | Santiago Metropolitan Region | Short term (≤ 2 years) |

| Modular prefabricated hospitals in remote north require integrated FM logistics support | +0.30% | Northern Chile (Antofagasta, Tarapacá, Atacama) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Grade-A Office Occupancy Rates Post-Pandemic Recovery

Santiago’s Grade-A vacancy dropped below pre-2020 levels as multinationals reconsolidated hub operations, creating a sustained premium for high-service office towers. FM providers that integrate wellness-focused soft services with IoT-enabled hard services are winning long-term deals because tenants now view workplace experience as a productivity lever rather than a cost line. Stable 2.5% GDP growth projected for 2025 underpins renewed leasing momentum, and foreign direct investment inflows reinforce the city’s role as a regional hub for headquarters locations. However, occupancy gains are concentrated in the Sanhattan submarket, leaving Grade-B assets exposed to downsizing and, therefore, to shorter FM commitments. The uneven rebound prompts service companies to carefully segment their offerings between high-touch financial tenants and price-sensitive secondary assets. Robust demand in Grade-A stock nonetheless sets a clear floor under revenue forecasts for the Chile facility management market.[2]International Energy Agency, “Energy Policy Review: Chile 2024,” iea.org

Corporate Cost-Optimization Pushing Outsourcing Penetration

National surveys show 57% of Chilean firms anticipate higher profits in 2025, yet the same companies cite cost control as a top strategic priority, triggering a more decisive pivot from in-house maintenance teams to third-party experts. Mid-market enterprises that historically managed cleaning and security internally are migrating to bundled or integrated solutions to access specialist talent and regulatory knowledge. As contracts migrate, providers are pressured to prove value through digital KPIs and transparent SLAs, reducing tolerance for fragmented vendor lists. The new outsourcing wave is also diluting hybrid models, creating a clearer split between full in-house control and fully outsourced end-to-end delivery. Transitional friction remains, particularly during knowledge transfer phases, but successful pilots in the banking and telecom sectors are acting as proof points that accelerate adoption in manufacturing, retail, and logistics.

Growth of Mining and Energy CAPEX Boosting Industrial FM Demand

The Ministry of Mining tracks USD 65.71 billion in committed projects through 2032, mainly copper and lithium expansions, each requiring resilient FM programs able to operate in desert climates and comply with strict environmental permits.[3]Ministerio de Energía, “Ley de Eficiencia Energética,” minenergia.cl Facility managers are therefore embedding remote monitoring, predictive maintenance, and modular accommodation services into their standard industrial offer. Renewable-power targets 80% clean electricity by 2030, adding solar, wind, and storage assets to the FM footprint, broadening the portfolio beyond traditional concentrators and smelters. Demand concentration in Antofagasta and Tarapacá intensifies technician shortages, driving up wages and increasing entry barriers for smaller local firms. While project timelines remain sensitive to community consultations, every construction mobilization still triggers interim FM contracts, creating a steady revenue pipeline even before mines reach steady state.

Mandatory Energy-Efficiency Audits in Public Buildings Drive Retro-Commissioning Contracts

Chile’s Energy Efficiency Law obliges large consumers to install certified energy-management systems and to cut intensity by 10% by 2030, a mandate expected to save USD 15.2 billion in cumulative energy costs. Public buildings must complete systematic audits, and the new National Registry of Energy Evaluators formalises the qualification path for service providers. Facility managers able to pair HVAC optimisation with compliant reporting tools are booking multi-year retro-commissioning contracts that blend engineering and advisory work. In private portfolios, executives increasingly align audit projects with ESG disclosures, positioning efficiency upgrades as both cost and reputation levers. Bottlenecks arise from the limited pool of certified evaluators and from retrofitting challenges in pre-2000 properties, yet early movers are locking in advantageous fee structures before market capacity tightens further.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delays and budget cuts in Chile's national infrastructure pipeline | -0.40% | National, with concentrated impact in Santiago and regional capitals | Medium term (2-4 years) |

| Escalating labour-safety compliance costs and liability premiums | -0.30% | National, with higher impact in industrial regions | Short term (≤ 2 years) |

| Acute skilled-technician shortage in HVAC and fire-safety systems | -0.50% | National, with severe impact in Northern Chile mining regions | Long term (≥ 4 years) |

| Peso volatility inflates imported spare-part costs for high-tech FM equipment | -0.20% | National, with higher impact on technology-intensive facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute Skilled-Technician Shortage in HVAC and Fire-Safety Systems

Chile’s 8.4% unemployment rate masks a persistent mismatch between available labour and certified technical roles, especially in HVAC, fire detection, and clean-room maintenance. Retirement-age demographics mirror global patterns: more than half of HVAC specialists are older than 45, reducing the incoming talent pipeline. Mining sites in Atacama require technicians able to operate at high altitude and in saline conditions, intensifying recruitment costs. The scarcity forces providers to over-time existing teams, elevating risk of burnout and wage inflation. To mitigate, larger integrators are co-funding vocational programmes with regional universities, but the talent gap is unlikely to close before 2028, constraining the Chile facility management market in its highest-margin service lines.

Peso Volatility Inflates Imported Spare-Part Costs for High-Tech FM Equipment

Chile’s peso has traded within a 20% range against the United States dollar since 2023, complicating budgeting for data-centre UPS components, MRI chillers, and specialised fire suppression gas cylinders. Many long-term FM contracts are denominated in Unidad de Fomento (UF) to hedge inflation; however, spare-part purchases settle in real-time USD, creating a spread that erodes margins. Providers have responded by adding currency adjustment clauses and hedging through forward contracts; however, such instruments can increase transaction complexity and hinder competitiveness in public tenders. Large global incumbents can spread exposure across multi-country procurement portfolios, whereas local specialists face tougher cost pass-through negotiations, keeping pressure on consolidation trajectories within the Chile facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft Services Dominate as Integration Gains Traction

Soft services accounted for 55.60% of 2025 revenue, underscoring a client preference for outsourced cleaning, security, and front-of-house functions that sustain day-to-day business continuity. Within Santiago’s financial district, multi-tenant towers now bundle concierge desks, interior landscaping, and wellness protocols into single invoices, raising ticket values and increasing retention. Hard services, including MEP, HVAC, and fire-safety maintenance, remain indispensable but contribute a smaller share because clients frequently defer heavy-equipment overhauls amid economic uncertainty. Integrated facility management, which merges both categories under unified governance, is projected to outpace all other service formats at a 6.45% CAGR, confirming its role as the prime growth engine of the Chile facility management market. The Energy Efficiency Law further lifts demand for predictive HVAC upgrades and sensor-based fault detection, bridging the gap between classic soft and hard scopes.

Predictive analytics and IoT retrofits allow providers to guarantee uptime, justifying premium pricing and longer contract tenures. As a result, mixed hard-and-soft packages are gaining traction among hospitals and data centres that cannot tolerate downtime. Other hard FM services and niche soft functions such as specialised cleaning for sterile environments are expanding more slowly but still benefit from rising compliance complexity. By reshaping offer design around scalability and outcome-based KPIs, leading vendors are repositioning themselves from mere maintenance suppliers to strategic partners, an evolution that keeps the Chile facility management industry relevant to C-suite agendas.

By Service-Delivery Mode: Outsourcing Accelerates, Yet In-House Remains Predominant

In-house teams delivered 63.75% of total 2025 spend, mirroring a longstanding corporate culture of direct head-count control. Nonetheless, the current cost-optimisation cycle is shifting sentiment. Integrated outsourcing is expected to grow at 6.45% CAGR, grabbing share in mining, healthcare, and data-centre environments where technical depth, safety accreditation, and 24/7 coverage are critical. Bundled and single-service contracts fill the transitional gap for organisations experimenting with selective outsourcing while retaining a core supervisory crew.

Even conservative public-sector entities are piloting third-party solutions for energy monitoring and waste management to comply with national sustainability targets. As more contracts migrate, providers able to prove seamless onboarding, workforce transfer, and KPI transparency will consolidate gains, reinforcing the Chile facility management market as a platform play rather than a labour arbitrage business. Resistance persists, especially among unions wary of job security, but clear demonstrations of lifecycle savings and audit compliance continue to weaken the in-house preference over time.

By Contract Duration: Stability Favoured, Flexibility Rising

Long-term agreements longer than three years commanded 40.85% share in 2025, particularly in heavy-industry and healthcare portfolios were asset complexity merits capital-intensive mobilisation. Such duration grants FM operators the runway to deploy digital twins, robotics, and specialised training, raising switching costs in the client’s eyes. However, volatile economic conditions and rapid technological change have fuelled a parallel rise in sub-one-year contracts, which are advancing at 5.63% CAGR. Short-cycle deals dominate in Grade-B offices and co-working spaces where landlords watch occupancy trends before locking in multiyear service levels.

Medium-term frameworks between one and three years serve as a compromise, giving both parties flexibility to renegotiate scope as buildings adopt new environmental or safety regulations. Providers therefore maintain modular service catalogues that scale with client demands without breaking contractual continuity, an approach that reinforces the resilient revenue outlook for the Chile facility management market.

By End-User Industry: Commercial Leads, Healthcare Accelerates

Commercial real estate, including corporate offices, retail venues, and logistics hubs, generated 38.10% of 2025 revenue, leveraged by Santiago’s role as the financial and digital centre of Chile. Yet, healthcare facilities represent the fastest-growing vertical, with a 6.52% CAGR, thanks to 25 hospitals under construction, including the USD 177 million Rengo and Pichilemu projects. Industrial and process plants in the mining and energy sectors also account for a sizable slice, demanding mission-critical maintenance, remote camp operations, and stringent safety compliance.

Hospitality, still recovering from tourism swings, depends heavily on soft-service quality to differentiate guest experience, whereas institutional and public buildings adopt integrated FM to meet budget constraints while satisfying energy-audit mandates. Converging hygiene expectations mean commercial towers are increasingly requesting hospital-grade cleaning, while industrial sites are mirroring office environments in offering knowledge-worker amenities. Such cross-pollination further integrates service lines and sustains the expansion of the Chile facility management market.

Geography Analysis

The Chile facility management market in 2024 accounted for 45% of the national GDP and nearly 6 million residents. The Sanhattan financial area alone supports dense Grade-A towers that require round-the-clock engineering, security, and tenant-experience services. Data-centre investments are accelerating. AWS secured environmental approval for a USD 205 million facility, and Equinix earmarked USD 130 million for its new Santiago campus, each underpinning multi-year critical-environment FM contracts. Stringent air-quality regulations and concerns about traffic congestion simultaneously boost demand for smart-building automation to curb emissions and enhance occupant comfort.

Northern Chile, specifically Antofagasta, Tarapacá, and Atacama, is delivering the fastest regional expansion for the Chilean facility management market. USD 65.71 billion in mining CAPEX, plus emerging green-hydrogen and ammonia plants, widens the industrial FM footprint well beyond traditional copper assets. Harsh desert climates, altitude, and remoteness require robust logistics, on-site accommodations, and specialized safety protocols, which increase service premiums. Technician shortages are acute, prompting providers to rotate crews from Santiago or rely on international specialists, which drives up costs and also creates barriers to entry.

Central regions such as Valparaíso and O’Higgins benefit from port logistics, vineyards, and an expanding warehouse cluster that supports Chile’s export economy. Southern provinces Biobío, Los Lagos, and Araucanía round out the addressable market with forestry, agro-industry, and growing adventure-tourism infrastructure. Seismic risk and weather volatility push public entities to elevate business-continuity benchmarks, thereby parking new opportunities for holistic FM solutions. These combined dynamics keep the Chile facility management market resilient nationwide even as growth vectors differ sharply by locality.

Competitive Landscape

The competitive field is moderately fragmented, yet consolidation momentum is building as capital-intensive integrated projects favour well-capitalised multinationals. ISS Chile reported 5.8% organic growth worldwide in Q2 2024, leveraging its global scale and digital interface to capture bundled contracts in banking and retail. Sodexo and Aramark both leverage their cross-border procurement reach to mitigate import cost volatility, thereby enhancing value propositions for price-sensitive public entities.

Compass Group’s exit from Chile opens white-space share for incumbents, especially in food services attached to integrated FM packages. Local specialists, such as Grupo EULEN and Mancorp, compete on geographic intimacy and bespoke service depth, but rising compliance costs and technology requirements may erode their margins unless they forge alliances or accept acquisition overtures.

Technology startups offering cloud-based work-order platforms challenge legacy operators on cost transparency and real-time reporting, pushing the entire Chile facility management market toward data-driven decision-making. Strategic partnerships, M and A, and co-innovation with prop-tech providers therefore headline boardroom agendas as companies seek durable differentiation.

Chile Facility Management Industry Leaders

ISS Chile S.A.

Sodexo Servicios de Gestión Chile SpA

Compass Group Chile Ltda.

Aramark Servicios y Aseo Chile SpA

Grupo EULEN Chile S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Amazon announced a USD 4 billion regional cloud-infrastructure plan that will include multiple availability zones and elevate demand for mission-critical FM services.

- March 2025: The Ministry of Energy launched the “Parque Solar Comunitario” scheme, encouraging municipalities to host community solar farms and opening a new municipal-scale FM segment.

- December 2024: The Ministry of Science and Technology unveiled a USD 2.5 billion National Data Centers Plan, positioning Chile as a Latin American digital hub and intensifying need for specialised FM.

- November 2024: Compass Group confirmed its strategic withdrawal from Chile, highlighting sector-wide consolidation pressures.

Chile Facility Management Market Report Scope

Facility management confines multiple disciplines to ensure buildings' functionality, comfort, safety, and efficiency by integrating people, place, process, and technology. While hard services include physical and structural services, such as fire alarm system lifts, among other services, soft services include cleaning, landscaping, security, and similar human-sourced services, providing a solution to end-user industries.

The Chile Facility Management Market is Segmented by Facility Management Type (In-house FM Service and Outsourced FM Service (Single FM, Bundled FM, and Integrated FM)), Offering Type (Hard FM and Soft FM), and End User (Commercial, Institutional, Public/ Infrastructure, and Industrial). The report offers the market size in value terms in USD for all the abovementioned segments.

The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study also tracks the revenue accrued from various facility management types used in various end-user industries across Chile. In addition, the study provides the Chilean facility management market trends, along with key vendor profiles. The study further analyses the overall impact of COVID-19 on the ecosystem.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Service-Delivery Mode

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By Contract Duration

| Short-term (Less than 1 yr) |

| Medium-term (1-3 yrs) |

| Long-term (More than 3 yrs) |

By End-User Industry

| Commercial (IT, Retail, Warehouses) |

| Hospitality (Hotels, Restaurants) |

| Institutional and Public Infrastructure |

| Healthcare (Public and Private) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-users (Multi-housing, Entertainment, Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Service-Delivery Mode | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By Contract Duration | Short-term (Less than 1 yr) | |

| Medium-term (1-3 yrs) | ||

| Long-term (More than 3 yrs) | ||

| By End-User Industry | Commercial (IT, Retail, Warehouses) | |

| Hospitality (Hotels, Restaurants) | ||

| Institutional and Public Infrastructure | ||

| Healthcare (Public and Private) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-users (Multi-housing, Entertainment, Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Chile facility management market?

The Chile facility management market size is valued at USD 4.44 billion in 2026.

How fast is the Chile facility management market expected to grow?

It is projected to expand at a 2.27% CAGR, reaching USD 4.97 billion by 2031.

Which service type dominates spending?

Soft services hold the largest share at 55.60% of 2025 revenue, driven by cleaning, security, and front-of-house needs.

Why is healthcare the fastest-growing end-user segment?

Chile’s hospital construction program, including the Rengo and Pichilemu projects, is fueling a 6.52% CAGR in healthcare FM demand.

How is peso volatility affecting providers?

Exchange-rate swings inflate imported spare-part costs, prompting currency hedging and price-adjustment clauses in FM contracts.

Page last updated on: