Chile Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

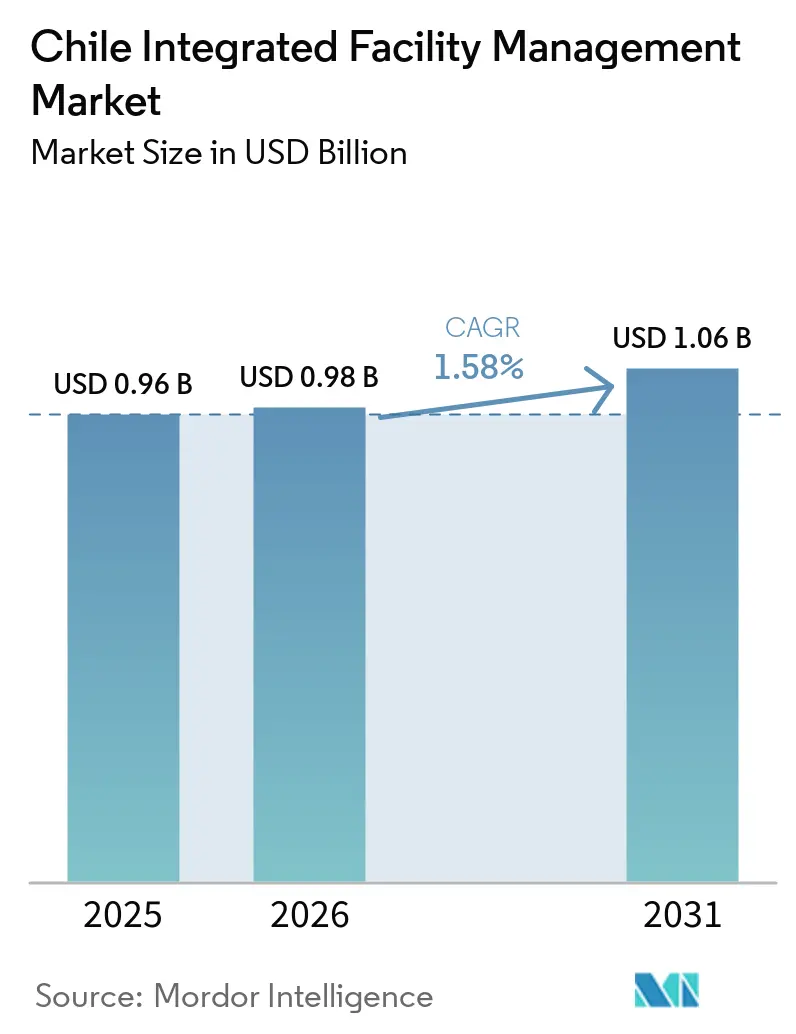

| Base Year Market Size (2025) | USD 0.96 Billion |

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.06 Billion |

| Growth Rate (2026 - 2031) | 1.58% CAGR |

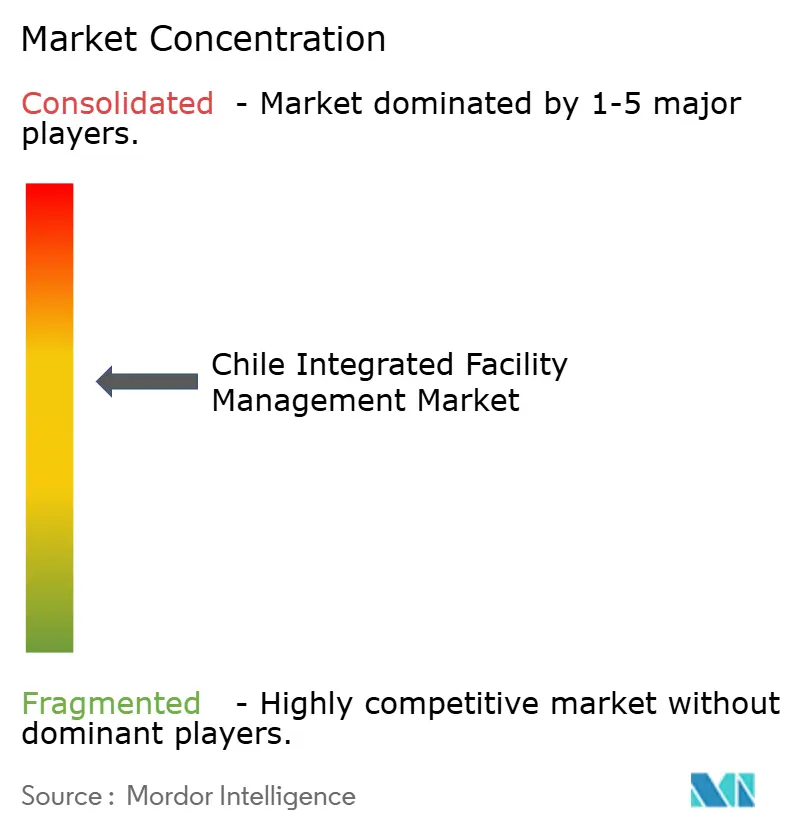

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Integrated Facility Management Market Analysis by Mordor Intelligence

The Chile integrated facility management market size was valued at USD 0.96 billion in 2025 and estimated to grow from USD 0.98 billion in 2026 to reach USD 1.06 billion by 2031, at a CAGR of 1.58% during the forecast period 2026-2031. This path reflects a broad move in the Chile integrated facility management (IFM) market from reactive, single-service buying toward longer and more coordinated contracts that cover both daily support and technical upkeep. Demand is being anchored by copper and lithium mining, digital infrastructure, healthcare assets, and corporate real estate, all of which require stable service delivery and committed capital spending. Buyers are also placing more weight on providers that can combine workforce scale with technical depth, because uptime, compliance, and audit readiness now matter as much as headline price. AI-enabled work order systems, IoT-based preventive maintenance, and cloud asset tracking are changing procurement standards, especially where clients expect real-time visibility across dispersed sites. Growth remains supported by outsourcing adoption, but technician shortages, exchange-rate pressure, inflation, and uneven municipal compliance create operating strain that favors larger and better-organized vendors.

Key Report Takeaways

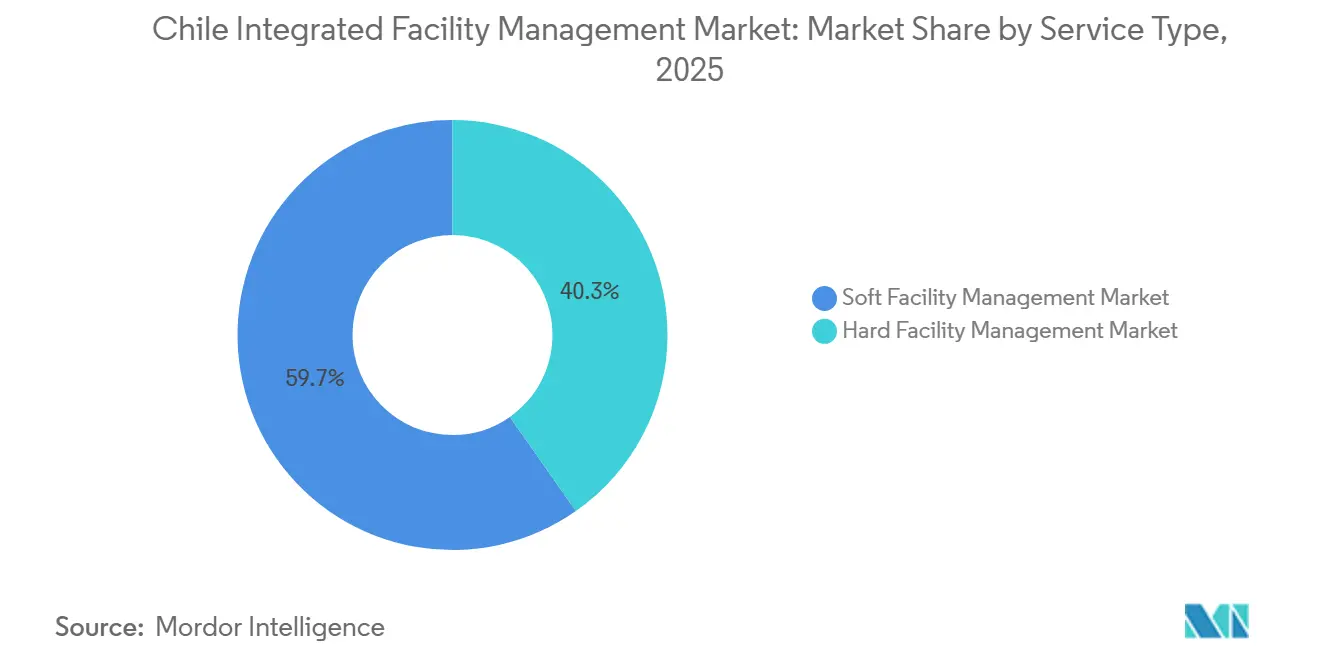

- By service type, Soft Facility Management (Soft FM) held 59.73% share of the Chile integrated facility management market in 2025, while Hard Facility Management (Hard FM) is forecast to expand at a 1.85% CAGR through 2031.

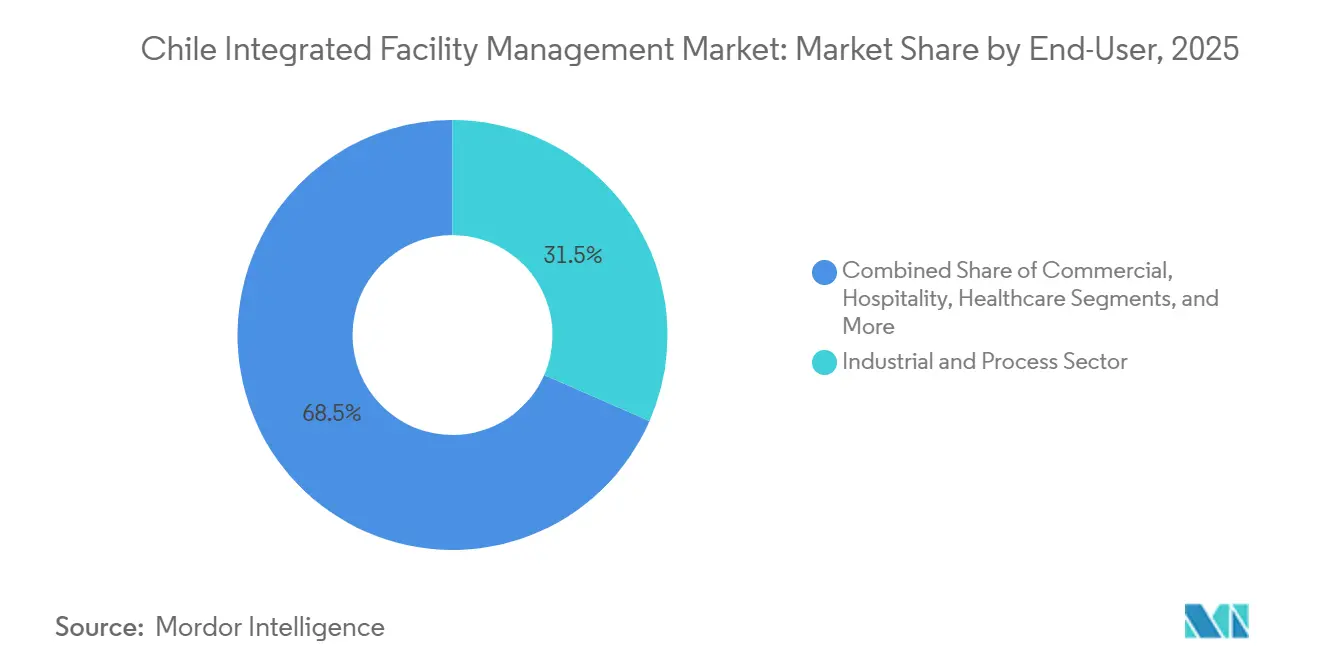

- By end user, the Industrial and Process Sector held 31.54% share of the Chile integrated facility management (IFM) market in 2025, while Commercial recorded the highest projected CAGR at 2.24% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Chile Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Growth Of Chile's Data Center Pipeline | +1.4% | National, with early gains in Santiago, Valparaíso | Short term (≤ 2 years) |

| Mining Sector's Shift Toward Integrated Outsourcing Models | +1.2% | Northern Chile, Antofagasta, Atacama, Tarapacá | Long term (≥ 4 years) |

| Government Push For Energy-Efficient Buildings | +0.9% | National, led by Metropolitan Region and major cities | Medium term (2-4 years) |

| Rising Outsourcing Penetration In Healthcare Facilities | +0.7% | National, with early gains in Santiago, Rancagua | Medium term (2-4 years) |

| Expansion Of Corporate Nearshoring Activity | +0.5% | National, with early gains in Santiago, Chillán, Valparaíso | Short term (≤ 2 years) |

| AI-Driven Predictive Maintenance Adoption In Public Infrastructure | +0.4% | National, with early gains in Valparaíso, Antofagasta | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Growth Of Chile's Data Center Pipeline

Robust growth in Chile's data center pipeline is creating a separate critical-environment service pool inside the Chile integrated facility management market, where uptime requirements are stricter and contract durations are longer. Amazon Web Services announced in May 2025 that it will invest more than USD 4 billion to launch an infrastructure region in Chile by the end of 2026.[1]Amazon.com, Inc., “Amazon to Invest More Than $4 Billion to Launch Infrastructure Region in Chile,” AWS Press Center, aboutamazon.com That scale of investment raises demand for continuous oversight of power systems, precision cooling, fire suppression, and physical access control across always-on facilities. In the Chile integrated facility management (IFM) market, this work naturally shifts revenue toward providers with specialized Hard FM capabilities, documented maintenance routines, and round-the-clock escalation protocols. Providers that can connect maintenance activity to data center infrastructure management systems are more likely to secure multi-year contracts that smaller generalist competitors will struggle to contest.

Mining Sector's Shift Toward Integrated Outsourcing Models

Mining continues to shape the Chile integrated facility management market because remote sites require dependable service models, tight liability control, and large workforces that can scale with maintenance cycles. Chile's mining sector accounted for 42% of the country's goods and services exports in 2025, which explains why mine operators remain the most influential buyers of integrated operational support. Techint Engineering and Construction signed a 5-year mechanical maintenance contract with Minera Centinela in 2024, deploying 138 base employees and scaling to 250 when campaigns intensify.[2]Techint Group, “Back to Mining Maintenance in Chile,” Techint Group, techint.com These contract structures show that clients increasingly prefer fewer counterparties that can combine maintenance execution, planning discipline, and workforce flexibility under one commercial framework. For the Chile integrated IFM market, that shift steadily favors providers that can manage site-wide operations rather than isolated service tasks.

Government Push For Energy-Efficient Buildings

Energy regulation is creating a compliance-led demand stream in the Chile integrated facility management market, especially where public assets and large buildings need continuous reporting and technical upgrades. Chile's Energy Efficiency Law requires energy labeling for new residential and commercial buildings and energy management systems for large energy consumers that represent more than one-third of national consumption. The compliance burden widened in January 2026 when municipalities entered the framework, bringing 6,150 public-sector properties and 10.48 million m² of managed space into mandatory reporting obligations. A 2024 public audit also found that 81.14% of 228 buildings lacked thermal wall insulation and 85.78% failed rooftop transmittance standards, which leaves a large retrofit queue for building-envelope, lighting, and HVAC work. For the Chile integrated facility management (IFM) market, these rules turn energy audits and upgrade programs into recurring service opportunities instead of one-time projects.

Rising Outsourcing Penetration in Healthcare Facilities

Healthcare outsourcing is strengthening the Chile integrated facility management market because hospital operators are buying compliance, reliability, and service accountability rather than just labor savings. At Hospital Clínico Félix Bulnes, the concession model covered 15 services, and the 2024 public account reported a chiller renewal, HEPA filter maintenance in 32 isolation rooms, and activation of a new CT scanner.[3]SCMS - Sociedad Concesionaria Metropolitana de Salud S.A., “Servicios Concesionados Mejoran la Calidad de la Salud Pública en el Hospital Clínico Félix Bulnes,” SCMS, scms.cl EULEN Group Chile positions its healthcare offering around ISO 13485:2016-aligned processes, clinical cleaning, and predictive maintenance for electromedical equipment.That pattern gives larger credentialed providers an advantage in procurement, because hospitals face strict operating conditions and cannot tolerate failures in HVAC, fire protection, or sanitation support. As more facilities enter concession or professionalized operating models, the Chile IFM market should see steadier demand from healthcare campuses that want one accountable service partner.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity Of Certified Skilled Technicians | -1.1% | National, acute in Antofagasta, Atacama, and Metropolitan Region | Long term (≥ 4 years) |

| Persistent Macroeconomic Volatility And FX Risk | -0.8% | National | Medium term (2-4 years) |

| Fragmented Regulatory Oversight Across Municipalities | -0.5% | National, acute in smaller municipalities outside Santiago | Medium term (2-4 years) |

| High Informality In Small-Scale FM Providers | -0.3% | National, higher in Southern and Northern regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity Of Certified Skilled Technicians

Technician scarcity remains a structural constraint on the Chile integrated facility management market because certified HVAC and fire-safety work cannot be substituted with general labor. Chile also starts from a weak digital skills base, with only 11.7% of adults proficient in problem-solving in technology-rich environments, against an OECD average of 32.3%. That gap matters because more contracts now require smart building tools, sensor-led diagnostics, and computerized maintenance planning in addition to field execution. Large multinational operators can partly close the gap through internal academies and recognized certifications, but smaller domestic firms often lack the margin room to invest at the same pace. In the Chile integrated facility management (IFM) market, the result is slower scaling in technical service lines and rising concentration of credentialed labor among the largest operators.

Persistent Macroeconomic Volatility and FX Risk

Macroeconomic volatility and foreign-exchange exposure continue to pressure the Chile IFM market because many contracts are billed in local currency while key technical inputs are imported. Banco Central de Chile reported that the peso-dollar parity crossed CLP 1,000 in January 2025, highlighting how quickly equipment and software costs can move for service providers. The central bank also kept the policy rate at 4.5% in December 2025 while acknowledging persistent inflation risks, even after inflation eased later in the year.[4]Banco Central de Chile, “Monetary Policy Report - March 2025 Presentation,” Banco Central de Chile, bcentral.cl OECD flagged U.S. tariff escalation as a downside risk to Chilean growth and copper export revenues, which matters because mining-linked demand still underpins a large part of outsourced facility services. Providers with more local sourcing and tighter contract indexation are better placed than equipment-heavy operators when currency swings compress already narrow margins in the Chile integrated facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM's Technical Complexity Drives Margin Expansion

Soft Facility Management (Soft FM) held 59.73% of the Chile integrated facility management market share in 2025, which kept it as the largest service type by revenue. Its scale reflects the daily need for cleaning, catering, office support, and related services across commercial, institutional, healthcare, and industrial sites where continuity matters more than technical complexity. Renewal cycles are frequent and buyer familiarity is high, so providers can retain volume, but price competition remains intense and margin expansion is harder than in specialized technical work. Aramark strengthened its catering logistics base in Chile when it opened a USD 10 million cook-and-chill facility in Lampa in November 2024, with capacity of 2,000 meals per hour at full production and national reach from Arica to Punta Arenas.

Within the Chile integrated facility management market size outlook, Hard Facility Management (Hard FM) is projected to advance at a 1.85% CAGR through 2031, making it the fastest-growing service type. The growth profile is tied to data centers, energy-efficiency retrofits, healthcare assets, and mining facilities that need dependable MEP, HVAC, fire systems, and asset management support. Large energy consumers must implement certified energy management systems and undergo recurring audits, which creates repeat demand for technical service bundles rather than isolated repairs. The January 2026 extension of the compliance framework to municipalities widened that opportunity by pulling thousands of public properties into formal reporting and upgrade cycles. That mix of regulation, uptime risk, and technical training needs is why Hard FM is becoming a more defensible part of the Chile integrated facility management industry than labor-led soft services.

By End User: Mining Anchors Volume, Commercial Cohort Accelerates Growth

Commercial is the fastest-growing end-user group in the Chile integrated facility management market size outlook, with a 2.24% CAGR during 2026-2031. Growth is tied to office absorption from nearshoring activity, rising demand from BFSI, IT and telecom, retail, and warehouse operators, and the concentration of data center investment in Santiago. SoftServe expanded its Chile presence in November 2025 with a new office in Chillán and a talent program aimed at more than 100 professionals in AI, software development, and cybersecurity, which signals wider corporate demand beyond the capital. In the Chile integrated facility management market, these occupiers often prefer bundled contracts because they want one provider managing daily services, compliance routines, and basic technical upkeep across multiple sites.

The Industrial and Process Sector held 31.54% of the Chile integrated facility management (IFM) market share in 2025, which kept mining-linked demand as the main volume anchor. Chile integrated facility management industry dynamics in this segment are shaped by remote operating conditions, safety obligations, and the need to control maintenance costs across plants, camps, logistics assets, and support infrastructure. Techint's 5-year contract with Minera Centinela showed how mine operators are turning to larger service partners that can deploy stable base teams and flex capacity during campaign periods. Institutional and public infrastructure demand remains steady, while healthcare is growing from a smaller base through concession-based outsourcing that ties service delivery to documented outcomes and compliance standards. Other end-user industries, including hospitality, entertainment, sports, and leisure, are improving with occupancy recovery, but they still contribute less revenue and remain more exposed to shifts in consumer and corporate sentiment.

Geography Analysis

Santiago Metropolitan Region remains the center of gravity for the Chile integrated facility management (IFM) market because it concentrates corporate offices, retail assets, public institutions, healthcare capacity, and the country's largest digital infrastructure pipeline. Amazon Web Services committed more than USD 4 billion in May 2025 to launch an infrastructure region in Chile by the end of 2026, reinforcing Santiago's role as the core location for critical-environment service demand. That concentration favors providers that can manage 24/7 uptime requirements, structured escalation, and detailed reporting across power, cooling, fire protection, and physical security. The region also sits at the center of energy-efficiency compliance activity, because much of the public building retrofit backlog and the largest administrative asset base are located in and around the capital.

Northern Chile is the second major demand anchor in the Chile integrated facility management market, led by Antofagasta, Atacama, and Tarapacá, where mining operations and related energy assets dominate service requirements. OECD identified mining as a central pillar of Chile's export economy, which explains why outsourced operations and maintenance contracts in the north have a direct influence on national facility services demand. Techint's return to mining maintenance at Minera Centinela illustrated how large industrial clients in Antofagasta want service partners that can handle workforce scale, mechanical maintenance, and remote site execution under a single framework. ISS Chile also presents integrated service capabilities in the local market, which supports the view that the northern corridor remains essential for providers with industrial and multi-site ambitions. Renewable power infrastructure in the Atacama zone adds adjacent demand, because operators need dependable maintenance for electrical systems and support assets that serve mining and grid-linked facilities.

Valparaíso, Biobío, Ñuble, and the southern regions represent a smaller but steadily developing part of the Chile integrated facility management market, where professional outsourcing is spreading from a lower base. SoftServe's expansion into Chillán showed that nearshoring-led business activity is beginning to support a broader commercial footprint outside Santiago. In Valparaíso, EFE Trenes de Chile launched an AI and IoT-based monitoring system for the Las Cucharas Bridge in May 2024, showing that public infrastructure owners in secondary regions are already testing predictive maintenance models. For national operators in the Chile IFM market, these regions offer a first-mover advantage because established service hubs and certification depth can be extended before local competitors build comparable capabilities.

Competitive Landscape

The Chile integrated facility management (IFM) market remains moderately fragmented, with multinational operators better placed for complex multi-service contracts and local firms retaining room in narrower or geography-specific mandates. The competitive gap is widest where clients want technical compliance, standardized reporting, and the ability to manage cleaning, catering, maintenance, and security through one accountable operating model. Newrest strengthened its commercial footprint in Santiago in 2024 through 2 facility management wins, one with Banco de Estado at its Santa Anita headquarters and another covering cleaning services across Bechtel's 3 offices. That kind of contract stacking matters in the Chile integrated facility management market because it gives providers scale in labor deployment, site supervision, and procurement that smaller rivals struggle to match.

Aramark remains one of the most influential operators in the Chile integrated facility management market, and its November 2024 investment in a USD 10 million food production facility in Lampa deepened its delivery capacity across mining, healthcare, and education accounts. The company also framed that site as part of a broader growth plan, which shows how leading vendors are using logistics infrastructure to make soft services harder for clients to unbundle. Regulatory scrutiny is also shaping competition, as Chile's Fiscalía Nacional Económica approved Sodexo's acquisition of Mediterránea de Catering in February 2026 only on the condition that Mediterránea's Chilean business be sold. That ruling limits straightforward horizontal consolidation and keeps space open for mid-tier challengers or specialized entrants that can win carved-out accounts. Several international and regional providers, including ISS Chile, EULEN, Sodexo, Newrest, Equans, and Confipetrol, therefore continue to coexist across different service scopes in the Chile IFM market.

Technology adoption is becoming the clearest separator in the Chile integrated facility management market because clients increasingly want proof of response times, asset visibility, and preventive action rather than labor presence alone. EGenya reports that its platform has helped Chilean facility management clients cut incident resolution times by 67% and personnel costs by 12%, which shows why digital tools are gaining commercial attention even in a labor-intensive market. Providers that can combine ISO-aligned operating discipline, predictive maintenance capability, and sector-specific know-how are better positioned for data centers, mining complexes, hospitals, and large public assets. As a result, the Chile IFM market is moving toward a structure where breadth still matters, but technical credibility and data-backed service assurance increasingly decide who wins the highest-value contracts.

Chile Integrated Facility Management Industry Leaders

Sodexo S.A.

ISS A/S

CBRE Group, Inc.

Compass Group PLC

G4S Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Chile's Fiscalía Nacional Económica, FNE, conditionally approved Sodexo S.A.'s acquisition of Mediterránea de Catering S.L., imposing the full divestiture of Mediterránea's Chilean operations as a precondition due to competition concerns in the institutional food and FM services market. The ruling signals active antitrust oversight of FM sector consolidation and may redirect Mediterránea's Chilean client base toward mid-tier operators.

- November 2025: SoftServe expanded its Chilean operations with a new office in Chillán, Ñuble Region, supported by CORFO funding, to serve U.S. and Canadian nearshoring clients. The investment, exceeding USD 100,000 in its talent acceleration program and targeting 100+ professionals in AI and software development, illustrates nearshoring demand beginning to migrate beyond Santiago into secondary Chilean cities.

- August 2025: SCMS published its 2024 public account for Hospital Clínico Félix Bulnes, reporting a chiller unit renewal, HEPA filter maintenance across 32 isolation rooms, and activation of a high-resolution CT scanner as outputs of its 15 concessioned FM services under the PPP model. The disclosure underscores how outcome-based reporting is becoming a performance accountability standard for outsourced healthcare FM in Chile.

- May 2025: Amazon Web Services announced an investment exceeding USD 4 billion to launch an infrastructure region in Chile by end of 2026, featuring 3 availability zones supporting cloud, AI, and machine-learning workloads. The project is expected to create sustained demand for 24/7 technical facility management across data center campuses and sets a precedent for hyperscale FM scope in the Chilean market.

Chile Integrated Facility Management Market Report Scope

The Chile Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-Users |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-Users | ||

Key Questions Answered in the Report

What is the current size and growth outlook for Chile facility management?

The market stood at USD 0.96 billion in 2025 and is forecast to reach USD 1.06 billion by 2031 at a 1.58% CAGR over 2026-2031.

Which service type leads revenue in Chile?

Soft FM led the market in 2025 with a 59.73% share, supported by recurring demand for cleaning, catering, and office-support services.

Why is Hard FM growing faster than Soft FM in Chile?

Hard FM is projected to grow at a 1.85% CAGR through 2031 because data centers, energy retrofits, healthcare assets, and mining sites need specialized technical maintenance.

Which end-user group is expanding the fastest?

Commercial is the fastest-growing end-user group, with a projected 2.24% CAGR through 2031, driven by nearshoring activity, office demand, and digital infrastructure investment.

Why does Santiago dominate demand for integrated services?

Santiago concentrates corporate offices, public institutions, retail assets, healthcare capacity, and the country's largest digital infrastructure pipeline, including new cloud investment.

What are the main factors limiting growth in Chile?

The biggest constraints are shortages of certified technicians, foreign-exchange volatility, inflation pressure on imported inputs, and uneven regulatory conditions across municipalities.

Page last updated on: