Colombia Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

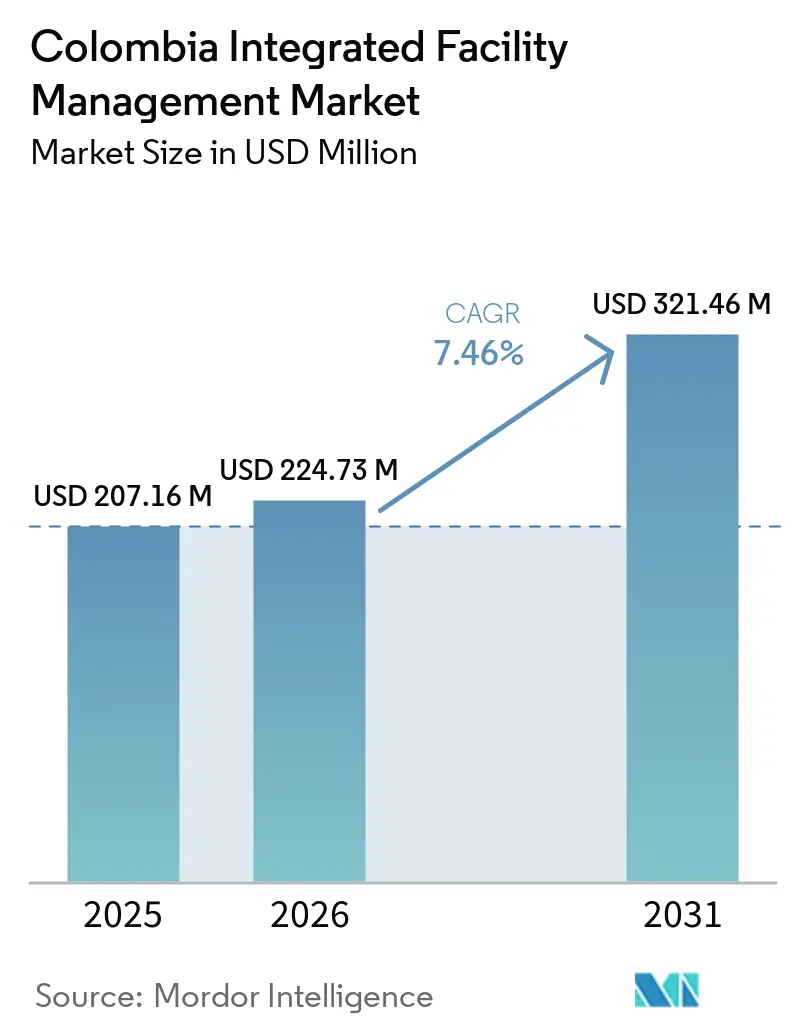

| Base Year Market Size (2025) | USD 207.16 Million |

| Market Size (2026) | USD 224.73 Million |

| Market Size (2031) | USD 321.46 Million |

| Growth Rate (2026 - 2031) | 7.46% CAGR |

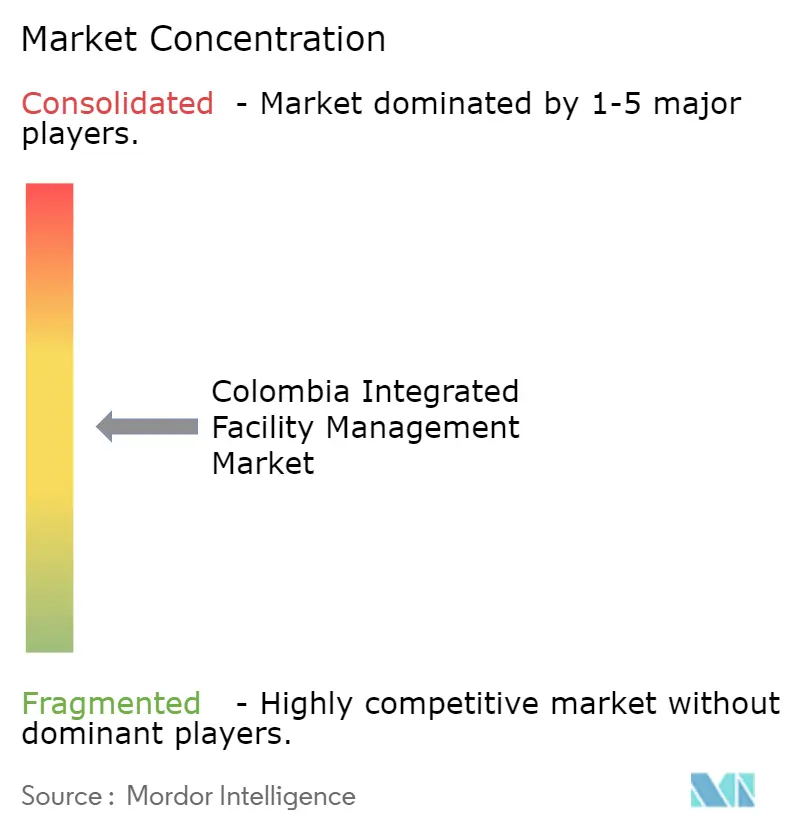

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Integrated Facility Management Market Analysis by Mordor Intelligence

The Colombia integrated facility management market size was valued at USD 207.16 million in 2025 and estimated to grow from USD 224.73 million in 2026 to reach USD 321.46 million by 2031, at a CAGR of 7.46% during the forecast period 2026-2031. This pace stayed well above Colombia's 2025 GDP growth of 2.6%, which reflects a clear shift in buyer behavior as facility management moved from a support cost into a more formal operating requirement. Regulatory pressure around energy and water efficiency, larger corporate real estate footprints, and stronger procurement discipline are all pushing organizations toward integrated service contracts with clearer accountability. The construction sector represented 4.3% of GDP and supported 1.55 million jobs in 2025, which means Colombia is adding to the stock of buildings and infrastructure that will require planned maintenance and workplace support over time. Colombia's role as a service and operations base is also creating more office campuses and managed workplaces that need auditable cleaning, maintenance, catering, and access control services. Competition is adjusting as contract volumes shift across providers after a major global operator exited, while labor informality and peso volatility still limit pricing power and national expansion in the less formal parts of the market.

Key Report Takeaways

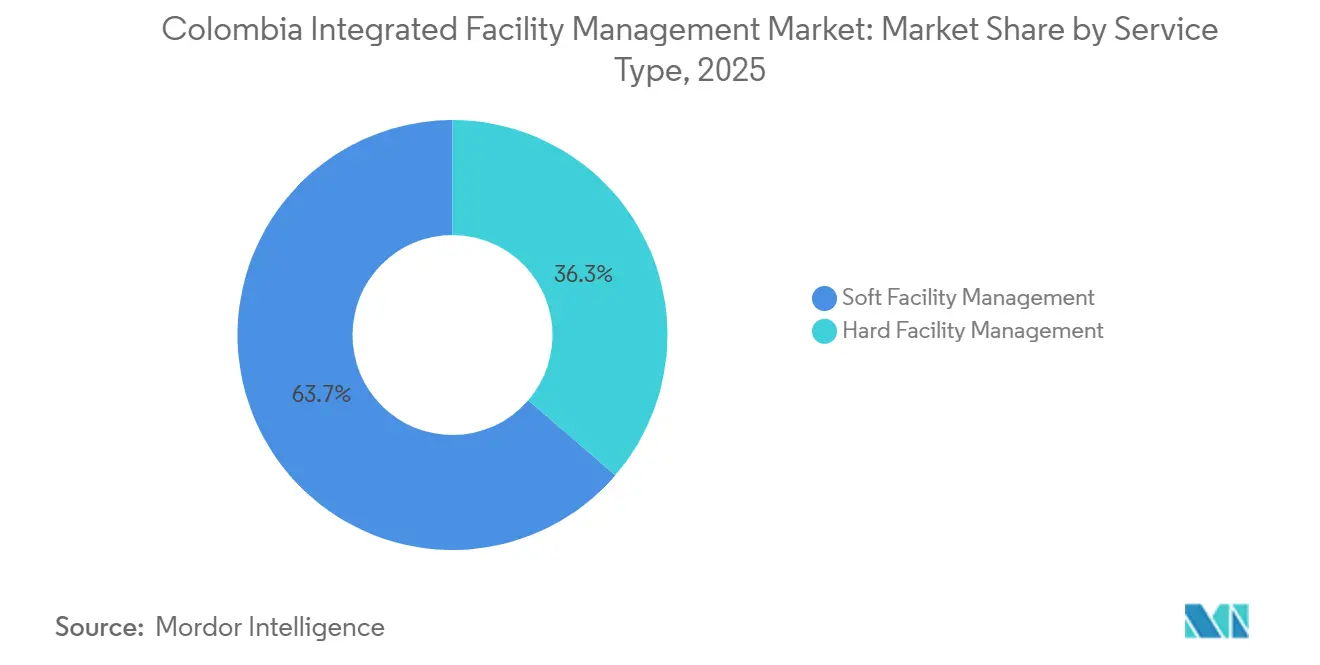

- By service type, Soft Facility Management (Soft FM) held 63.68% of the Colombia integrated facility management market share in 2025, while Hard Facility Management (Hard FM) is forecast to expand at an 8.01% CAGR during 2026-2031.

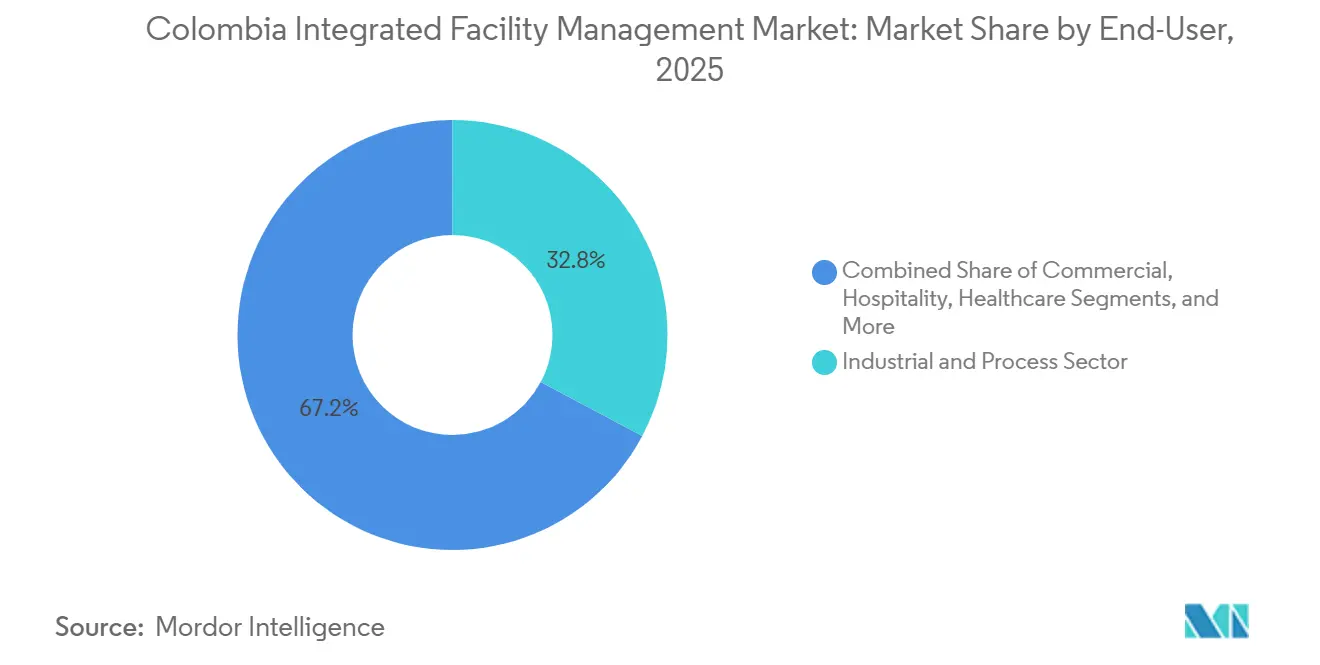

- By end-user, the industrial and process sector accounted for 32.79% of the Colombia integrated facility management (IFM) market size in 2025, while the commercial segment is projected to grow at an 8.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Colombia Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Emphasis of Companies Toward Outsourcing of Non-Core Functions | +2.2% | Global, concentrated in Bogotá, Medellín, and Barranquilla | Short term (≤ 2 years) |

| Increasing Corporate Investments in Urbanization and Real Estate | +1.8% | National, accelerated gains in Bogotá and Medellín | Medium term (2-4 years) |

| Increased Thrust for Energy Efficiency in Buildings | +1.2% | National, driven by Resolution 0194 and Law 2407 compliance mandates | Medium term (2-4 years) |

| Rise of Facility Standards Among Private Service Organizations | +0.8% | National, concentrated in industrial corridors and healthcare hubs | Short term (≤ 2 years) |

| Growing Urban Development Along Bogotá's Corridors | +0.5% | Bogotá D.C. and adjacent municipalities | Long term (≥ 4 years) |

| Maintaining Work-Life Balance Integration Between Business and Operations | +0.3% | Urban centers, BPO and tech campuses in Bogotá and Medellín | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Emphasis of Companies Toward Outsourcing of Non-Core Functions

Outsourcing of non-core functions is becoming a standard operating model in the formal parts of the Colombia integrated facility management (IFM) market, especially among occupiers that want consistent service delivery across several sites and clearer control over service quality. Large providers active in the country now market cleaning, maintenance, workplace support, and food services as a bundled operating solution, which indicates that many buyers prefer coordinated delivery instead of managing several specialist vendors on their own. This model is especially relevant for financial institutions, public agencies, and transport operators that need auditable service standards and regular reporting, which is consistent with the institutional client base highlighted by Elite Facility Management. Once buyers begin to combine compliance needs, uptime expectations, and occupant experience goals, contract scope usually widens from a single service into a broader integrated model that is harder for fragmented local vendors to match. Bogotá and Medellín benefit first because large formal office estates and more professional procurement teams are concentrated there, which supports higher-value and more specification-heavy contracts than those usually seen in smaller cities. In that setting, outsourcing is not only lifting volumes in the Colombia integrated facility management market, it is also raising average contract intensity where workplace complexity and accountability requirements are highest.

Increasing Corporate Investments in Urbanization and Real Estate

Growth in real estate and urban development is widening the physical asset base that feeds the Colombia integrated facility management market over time, because every new office, mixed-use asset, and managed property eventually moves into a recurring maintenance and service cycle. BBVA Research stated that the construction sector represented 4.3% of GDP and supported 1.55 million jobs in 2025, which underlines the scale of built assets entering operation across the country.[1]BBVA Research, “Colombia | Real Estate Outlook. 2025,” BBVA Research, bbvaresearch.com The same outlook projected 11.5% growth in new housing sales in 2026 and showed that renting households reached 7.3 million, ahead of the 7.1 million households that owned their homes, which shifts more property management responsibility toward organized landlords and managers. That tenure mix matters because professionally managed buildings are more likely to buy structured services for cleaning, common-area upkeep, utilities coordination, and preventive maintenance than assets managed through informal local arrangements. As these assets move from commissioning into stabilized operation, buyers usually adopt service schedules and performance standards that favor planned contracts instead of reactive work orders. This timing supports a forward pipeline for more technical and recurring work in the Colombia IFM market as new commercial and managed residential stock matures across the forecast period.

Increased Thrust for Energy Efficiency in Buildings

Energy and water efficiency rules are raising the technical threshold for service delivery in the Colombia integrated facility management market, because compliance is moving from a discretionary objective into a monitored obligation for both public and private buildings. In April 2025, the Ministry of Housing issued Resolution 0194 of 2025, which set mandatory minimum energy savings of 5%-20% and water savings of 15%-30% for new public and private buildings nationwide.[2]Presidencia de la República de Colombia, “Expiden Norma Que Impulsa la Construcción Sostenible y el Ahorro de Agua y Energía en Edificios Nuevos,” Presidencia de la República de Colombia, presidencia.gov.co Law 2407 of 2024 added a second compliance layer by requiring public entities to appoint dedicated energy managers, conduct energy planning, and report results annually to UPME, which gives energy management a formal place in day-to-day facilities operations. These rules favor FM operators that can manage metering, preventive maintenance, monitoring, and reporting through a technical service model instead of offering only labor-based support. The result is a wider gap between qualified integrated providers and informal competitors, because compliance-linked contracts require skills, documentation, and systems that the low end of the market usually does not carry. Over the next several years, this will keep pushing the Colombia integrated facility management (IFM) market toward contracts that combine maintenance delivery with measurable resource performance and documented compliance outputs.

Rise of Facility Standards Among Private Service Organizations

Facility standards across private organizations have stayed higher since the pandemic, and many clients now expect tighter hygiene routines, more structured waste handling, and more reliable preventive maintenance as part of normal site operations. Agilissa stated that integrated FM in healthcare settings reduces non-assistance operating costs by 18% and lowers healthcare-associated infection rates by more than 10%, which gives buyers a quantified basis for moving from narrow service contracts to broader operating models. That logic is spreading beyond hospitals because procurement teams increasingly want service partners that can connect operating quality to cost control, regulatory readiness, and user outcomes in one framework. Providers that can track incidents, work orders, space use, and supply consumption through digital tools are in a better position to defend contract value than firms that rely mostly on manual supervision and basic labor scheduling. The shift also supports longer contracts because performance data becomes more useful when service delivery is stable and measured over time instead of being reset across several short arrangements. In practical terms, the Colombia IFM market is rewarding providers that can express value in operating and financial terms, while price-only competitors are being pushed toward narrower and more commoditized scopes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of Informal Working Class Businesses and Industries | -1.5% | National, most acute in secondary cities and rural areas | Long term (≥ 4 years) |

| Currency Volatility Deterring Global FM Integrations | -0.9% | National, most acute for multinational FM operators with cross-border supply chains | Medium term (2-4 years) |

| Fragmented Market in Secondary Cities | -0.7% | Secondary cities, limited in Bogotá, Medellín, and Manizales | Long term (≥ 4 years) |

| Growing Adoption of CAFM Platforms Disrupting Traditional Integration | -0.5% | Urban, technology-forward FM clients in Bogotá and Medellín | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Informal Working Class Businesses and Industries

Labor informality remains the largest structural restraint on the Colombia integrated facility management market because it keeps a large share of cleaning, maintenance, and support services outside formal procurement and tax-compliant contract structures. The OECD reported that informal employment represented 55.4% of the national workforce in 2024, while rural informality reached 83.9%, which shows how deep the parallel service economy remains outside the largest urban centers. Banco de la República stated that non-wage labor costs exceeded 55% of base pay, which makes formal hiring difficult for many small businesses and sustains a low-cost informal provider base that formal FM operators cannot easily displace. UNDP also linked informality to the realities of micro and small businesses, which limits the pool of enterprises that are able to buy fully integrated and audited service contracts. This is most visible outside the major metros, where price discovery is distorted by unregistered providers and contract scope often stays narrow even when end-user needs are expanding. Until formalization broadens, national expansion in the Colombia IFM market will continue to look easier in strategy plans than in actual contract conversion on the ground.

Currency Volatility Deterring Global FM Integrations

Currency volatility complicates expansion plans in the Colombia integrated facility management market because many technical inputs, digital platforms, and specialized maintenance items still carry foreign currency exposure while client contracts often stay fixed for several years. When the Colombian peso weakens, imported HVAC components, software licenses, sensors, and specialist tools become more expensive, which puts pressure on operators that cannot reprice contracts quickly enough. Compass Group completed the sale of its operations in Chile, Colombia, and Mexico to Newrest Group in March 2025 for net disposal proceeds of approximately USD 166 million, which highlighted how regional portfolio decisions are influenced by capital returns and operating risk as much as by local contract volume.[3]Compass Group PLC, “Annual Report 2025,” Compass Group PLC, compass-group.com This cost mismatch tends to favor locally incorporated providers with Colombian peso cost bases, since they can protect daily margins more easily in labor-intensive delivery than firms that depend more heavily on imported systems or cross-border procurement. It also supports hybrid operating models in which international firms contribute systems and oversight while local partners handle a larger share of direct service execution. The result is slower full-stack integration by foreign players even when client demand for more sophisticated service models in the Colombia integrated facility management (IFM) market is moving in the opposite direction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Moves Faster as Soft FM Holds the Larger Base

Soft Facility Management (Soft FM) held 63.68% of the Colombia integrated facility management (IFM) market size in 2025, which made it the dominant service group because cleaning, catering, waste management, and office support are usually the first functions buyers move out of direct in-house control. This lead reflects buying behavior across the Colombia integrated facility management industry, where organizations often begin with essential labor-heavy services before they widen scope into more technical and compliance-driven work. Soft FM also benefits from its daily visibility to occupants, because site cleanliness, food services, and waste handling shape workplace experience in a way that clients can judge immediately. As a result, buyers often prefer to consolidate several soft services under one operator to reduce administrative friction and establish a clearer performance baseline across sites. Catering carries particular weight in large managed workplaces because food provision in office and campus settings often functions as part of staff retention and employee experience rather than a simple support cost.

Hard Facility Management (Hard FM) is forecast to grow at an 8.01% CAGR during 2026-2031, the fastest pace among service types in the Colombia integrated facility management market, because technical maintenance is becoming more closely tied to compliance, energy performance, and asset uptime. HVAC services, asset management, fire protection, and smart building support each address a different operating risk, which makes Hard FM more important as Colombia adds modern commercial and industrial assets with tighter performance expectations. Resolution 0194 of 2025 and Law 2407 of 2024 strengthen this shift because new buildings and public entities now face clearer requirements around energy savings, monitoring, and operating discipline. That gives technical providers a stronger position in the Colombia integrated facility management industry, since compliance-related maintenance is harder to replace with ad hoc local labor. The growth pattern therefore looks more like structural catch-up than a short cycle, because Hard FM is expanding from a smaller base but is attached to some of the most durable requirements in the Colombia IFM market.

By End-User: Industrial Demand Leads While Commercial Contracts Expand Faster

The industrial and process sector held 32.79% of the Colombia integrated facility management market share in 2025, which made it the largest end-user group because oil, gas, mining, and manufacturing sites need continuous support for uptime, industrial cleaning, HVAC reliability, and worker services. In these environments, the cost of unplanned stoppages is high, so buyers are more willing to pay for service models that combine maintenance discipline with measurable operating continuity. Sodexo Colombia's national service offer, which includes remote-site and facility support capabilities, reflects the scale and geographic spread that industrial clients often require from providers operating across different departments and site conditions. Industrial demand also tends to produce larger and more stable contract values because technical routines, safety requirements, and camp or site support functions are harder to separate into small local tasks. That is why this end-user group remains the demand anchor for the Colombia integrated facility management market even as faster growth is starting to come from more office-led and service-led environments.

The commercial segment is forecast to grow at an 8.28% CAGR during 2026-2031, which makes it the fastest-moving end-user group in the Colombia integrated facility management (IFM) market as more formal office, institutional, and mixed-use environments adopt standardized outsourced services. Elite Facility Management's client base includes Davivienda, BBVA, ICETEX, INVIMA, and Transmilenio, which shows that commercial procurement already spans financial services, public institutions, and transport-linked assets rather than a narrow office-only niche. Healthcare and hospitals add another layer of demand because service delivery in those sites requires tighter process control and supports higher-value integrated scopes when buyers are focused on hygiene, safety, and operational continuity. Infrastructure and public utilities still depend more heavily on public investment cycles, which makes their procurement rhythm less even than private commercial demand and more exposed to administrative timing. Other end-users, including education, retail, and government offices, remain less penetrated by integrated providers, which leaves room for the Colombia IFM market to widen as procurement practices become more formal across a broader base of occupiers.

Geography Analysis

Bogotá remains the central demand cluster for the Colombia integrated facility management market because it combines the deepest concentration of formal offices, public institutions, transport infrastructure, and premium real estate in the country. The city's contract profile is broad rather than narrow, since it spans conventional office cleaning and maintenance, institutional workplace services, and larger public-asset needs that require more formal procurement and reporting standards. Prosegur's January 2025 contract for Bogotá's El Campín Cultural and Sports Centre showed that the capital is also producing specialized facilities opportunities beyond normal office environments, including large-event security and operations support linked to major venue upgrades. BBVA Research projected 11.5% growth in new housing sales in 2026, and that broader increase in built assets should keep adding to the future service base for managed buildings in and around the main urban corridors. In practical terms, Bogotá is where the formal end of the Colombia integrated facility management market is most visible because buyer sophistication, compliance requirements, and site complexity all meet in the same geography.

Medellín forms the second major growth pole in the Colombia integrated facility management market because it combines a modern office base, business-services activity, and a formal corporate environment that is well suited to standardized contracts. The city fits service models that depend on documented delivery, workplace support, and digital reporting, which is why operators focused on institutional and office-led demand continue to treat it as a core urban node. Cali and other established urban centers extend that pattern, although at a smaller scale, because regional coverage still matters for clients that want consistent service standards across several sites instead of city-by-city vendor management. This leaves the largest cities with a clear advantage in the current market because formal demand is deeper there and contract execution is easier to scale through centralized management structures.

Secondary cities remain the hardest part of the market to formalize even though they offer the clearest long-term conversion opportunity for the Colombia integrated facility management market. High informality weakens contract depth outside the major metros and keeps many buyers in narrow single-service arrangements or locally arranged operating models that do not easily convert into integrated contracts. Even so, industrial corridors, hospitals, utilities, and transport assets still create pockets of formal demand that national providers can serve when buyers need standardized delivery across dispersed locations. Geographic expansion will therefore depend less on raw construction activity and more on the pace at which business formalization, compliance pressure, and professional procurement widen the addressable base outside the main urban centers,

Competitive Landscape

The Colombia integrated facility management market remains moderately fragmented, with global and regional operators competing against a wider set of local specialists that are strong in selected verticals, cities, or service lines. The most important recent competitive move was Compass Group's March 2025 divestiture of its operations in Chile, Colombia, and Mexico to Newrest Group for net disposal proceeds of approximately USD 166 million, which redistributed contract volume and altered the balance among established players. That shift created room for both multinational and domestic providers to pursue contracts that had previously sat with a global integrator, especially in accounts where continuity and transition management mattered as much as price. Sodexo Colombia remains one of the best-positioned large operators because it offers integrated facility management services across a national footprint and already addresses cleaning, technical support, and workplace needs through a bundled delivery model. Prosegur also shows how adjacent specialists are broadening their role in the Colombia integrated facility management market, since its El Campín project combined physical security deployment with iSOC-enabled real-time monitoring for a large public venue contract.

Local operators are closing the capability gap with larger international firms through technology and execution discipline rather than through scale alone. Elite Facility Management has built a digital suite around Elite Man, Elite WP, and Elite One, which supports maintenance control, space management, and incident or supply visibility for institutional clients that expect structured reporting. Corporativo Overall competes from a different position, using 37+ years of experience, 14,000+ collaborators, and 350+ active clients to support a local delivery model with cost structures rooted in Colombian pesos. These local strengths matter because many buyers in the Colombia integrated facility management market now want the discipline of integrated delivery but still need cost structures that can hold up in a volatile operating environment.

White space remains clearest in energy-compliance-led Hard FM, integrated healthcare FM, and formal commercial accounts outside the top urban clusters, because each of those areas requires either technical qualifications or more disciplined procurement than informal operators can usually provide. At the same time, CAFM and cloud-based management tools are giving some occupiers another option, since multi-vendor coordination can now be handled through software layers without always appointing a single integrated operator. That creates pressure on bundled economics, especially in formal office environments where buyers are confident enough to separate strategy, monitoring, and execution across different partners. Even with that pressure, the Colombia integrated facility management market still favors providers that can combine national reach, documented performance, and sector-specific know-how in contracts where compliance and continuity matter more than unit labor cost alone.

Colombia Integrated Facility Management Industry Leaders

ISS A/S

Sodexo S.A.

CBRE Group Inc.

Grupo EULEN Colombia

G4S PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Indigo Group acquired 100% of Central Parking System Colombia, becoming the largest parking and mobility operator in Colombia. The acquisition expanded INDIGO’s footprint to 209 parking facilities across 25 cities and strengthened its IFM-related urban mobility operations.

- December 2025: Turner & Townsend completed integration with CBRE, expanding project management, cost consulting, and digital infrastructure capabilities in Colombia. The combined entity positioned Colombia as a strategic hub for data center and infrastructure projects.

- July 2025: Hellmann established a fully owned Colombian subsidiary after acquiring perishables partner HPL Apollo. The expansion included integrated logistics, customs brokerage, and contract logistics services, strengthening facilities and supply-chain infrastructure management in Colombia.

- July 2025: Irritec acquired a majority stake in Agrifim Colombia and announced plans to modernize production facilities, add new manufacturing lines, and establish a technology transfer center. The move supports industrial facility expansion and operational infrastructure modernization.

Colombia Integrated Facility Management Market Report Scope

The Colombia Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End Users |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End Users | ||

Key Questions Answered in the Report

What is the current and forecast value of facility management in Colombia?

The Colombia integrated facility management market was valued at USD 207.16 million in 2025 and is forecast to reach USD 321.46 million by 2031, growing at a 7.46% CAGR during 2026-2031.

What is driving demand for integrated services in Colombia?

Demand is being supported by more outsourced non-core operations, a larger real estate base, and new energy-efficiency rules that are making building performance and compliance more important in day-to-day operations.

Which service type leads and which one is growing the fastest?

Soft FM led with 63.68% share in 2025 because cleaning, catering, and waste services are usually outsourced first. Hard FM is growing faster at an 8.01% CAGR as technical maintenance becomes more compliance-driven.

Which end-user group contributes the most demand?

The industrial and process sector led with 32.79% share in 2025 because oil, gas, mining, and manufacturing sites need uptime, industrial cleaning, and technical support through structured contracts.

Why is the commercial segment expanding faster than other end-users?

Commercial demand is forecast to grow at an 8.28% CAGR through 2031 as more offices, institutions, and mixed-use environments adopt standardized contracts with clearer reporting and broader service scope.

What is the biggest barrier to wider adoption across the country?

Labor informality is the main barrier, since 55.4% of the workforce was informal in 2024 and that keeps a large part of service delivery outside formal procurement channels, especially beyond the largest cities.

Page last updated on: