Philippines Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

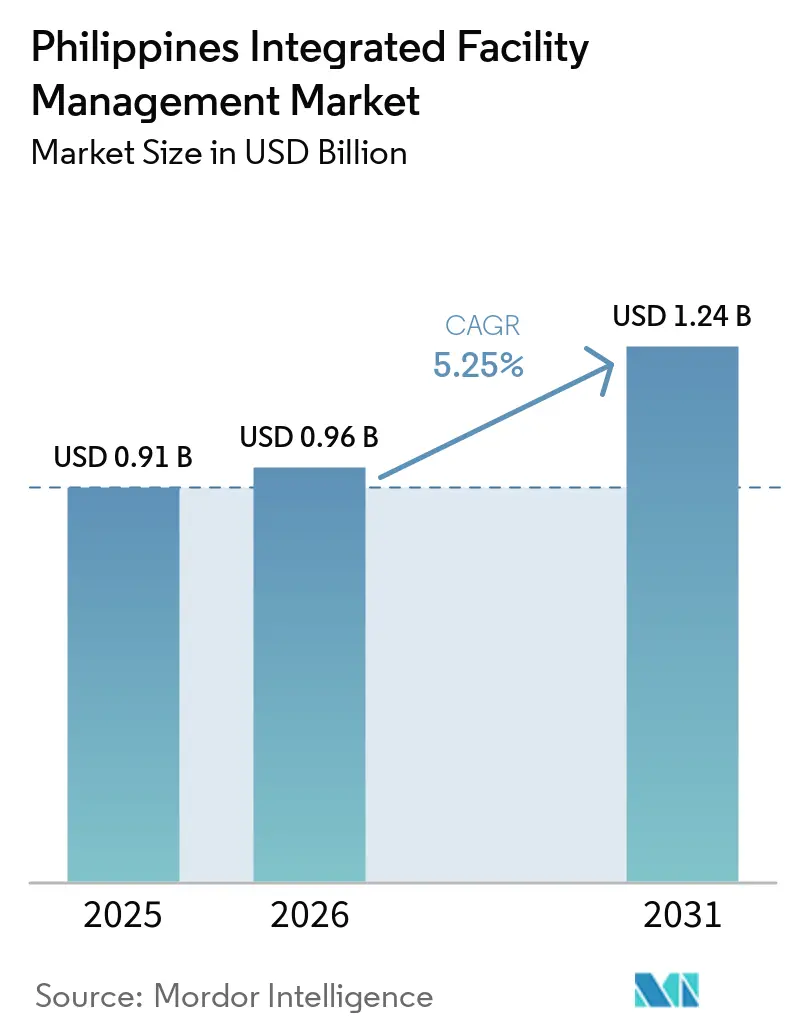

| Base Year Market Size (2025) | USD 0.91 Billion |

| Market Size (2026) | USD 0.96 Billion |

| Market Size (2031) | USD 1.24 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

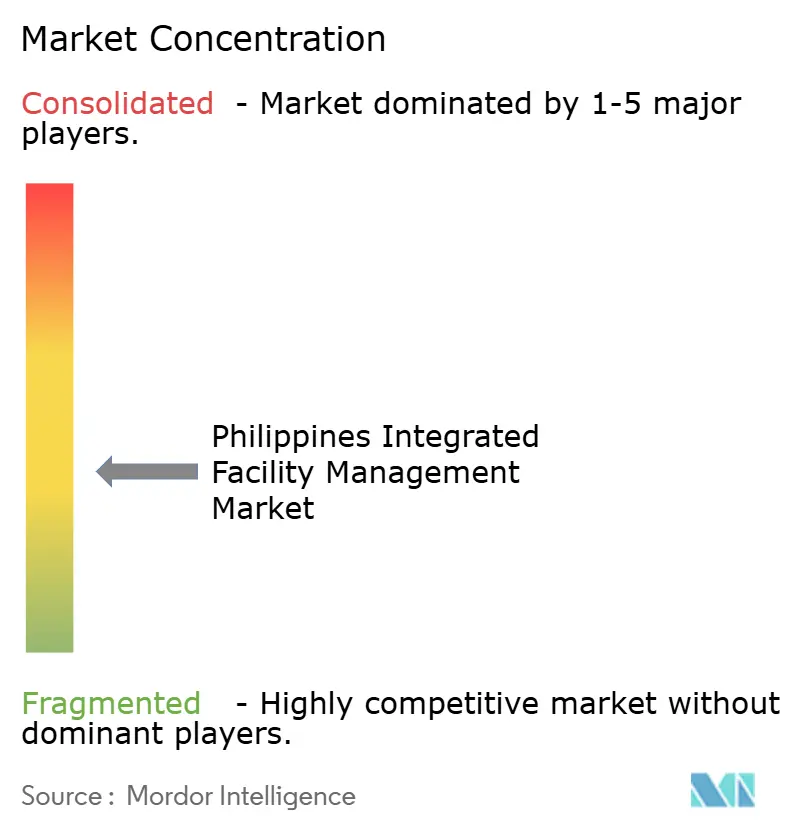

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Integrated Facility Management Market Analysis by Mordor Intelligence

The Philippines Integrated Facility Management Market size is projected to be USD 0.91 billion in 2025, USD 0.96 billion in 2026, and reach USD 1.24 billion by 2031, growing at a CAGR of 5.25% from 2026 to 2031.

The forward path remains tied to a larger base of operating assets, as transport projects, commercial buildings, hospitals, industrial facilities, and data centers all require longer-term service coverage after commissioning. The Philippines integrated facility management market also stands out in Southeast Asia because BPO demand keeps soft services prominent, while newer technical assets are starting to increase the share of engineering-led contracts. The government’s Build Better More program, with PHP 1.5 trillion (USD 25.9 billion) in 2026 spending, reinforced the medium-term pipeline, as these assets will require structured operations and maintenance support throughout their lifecycles. Office recovery in Metro Manila, hospital capacity additions across several regions, and the push to scale national data center capacity widened the addressable contract base across both routine and specialized services. Near-term execution still depends on labour availability and energy-cost stability because hard FM delivery becomes more difficult to scale when MEP talent is scarce and power prices fluctuate sharply in Luzon and parts of the Visayas.

Key Report Takeaways

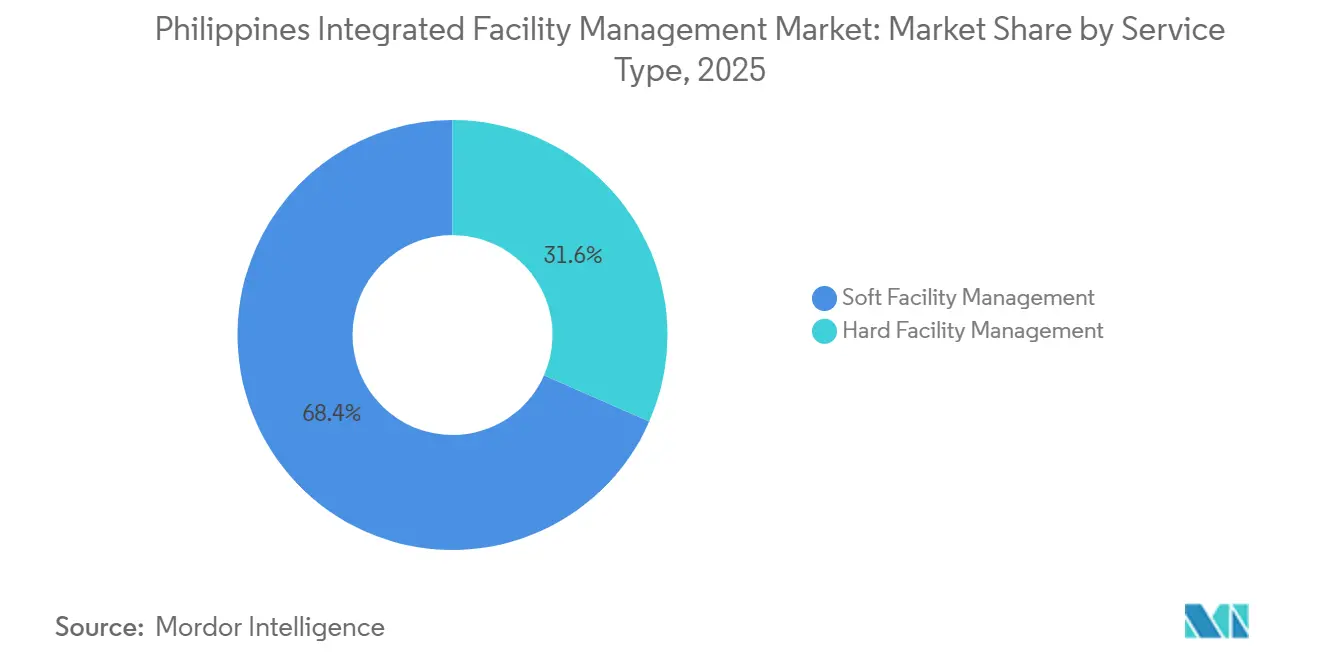

- By service type, soft integrated facility management market held a 68.41% in the Philippines integrated facility management market share, in 2025, while hard integrated facility management recorded the highest projected CAGR at 6.07% through 2031.

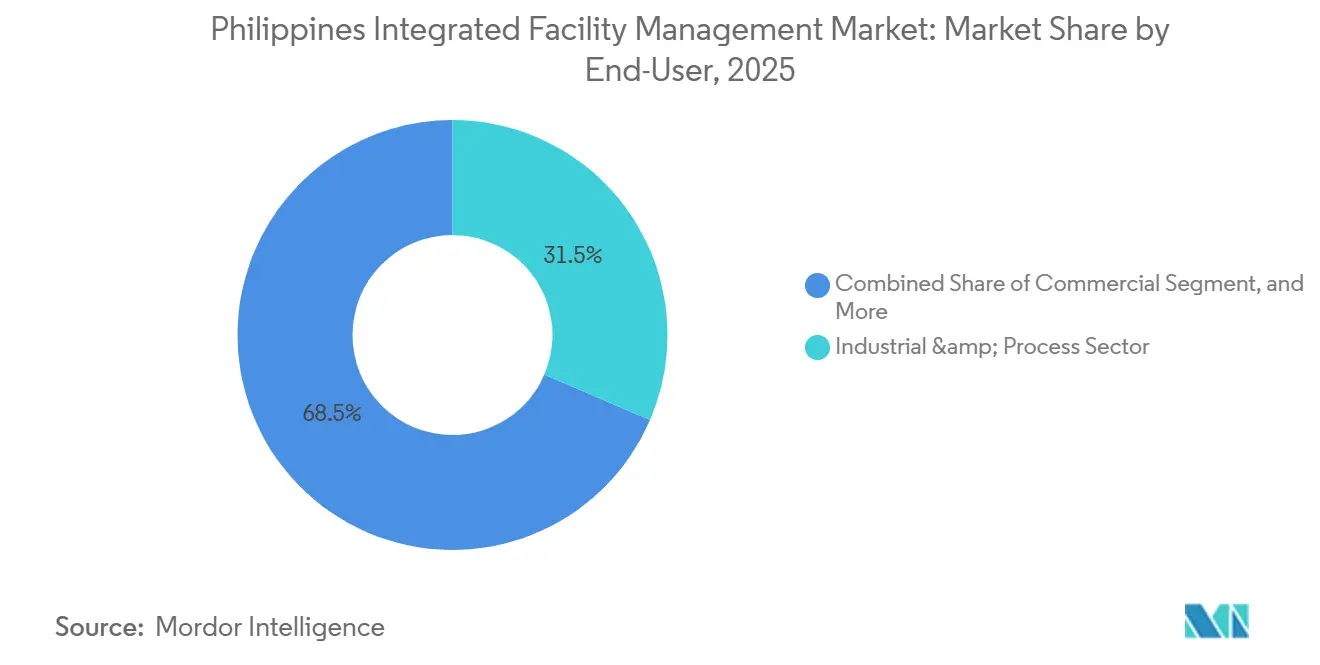

- By end-user industry, the industrial and process sector integrated facility management market held a 31.47% in the Philippines integrated facility management market share in 2025, while commercial end-users recorded the highest projected CAGR at 5.91% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Build Better More Infrastructure Pipeline Expansion | +1.8% | Philippines-wide, concentrated in NCR, Central Luzon, and Visayas corridors | Short term (≤ 2 years) |

| Outsourcing Trend Among BPO and Commercial Offices | +1.3% | NCR, Cebu, Davao, and emerging provincial centers | Medium term (2-4 years) |

| Healthcare Facility Build-outs and Modernization | +0.9% | Philippines-wide, including Western Visayas, Bicol, and Mindanao | Medium term (2-4 years) |

| Smart-Building and IoT-Enabled FM Adoption | +0.7% | NCR commercial districts and PEZA economic zones | Long term (≥ 4 years) |

| Mandatory ESG and Green-Building Certifications | +0.5% | NCR, Cebu, Metro Davao, and PEZA-registered estates nationwide | Long term (≥ 4 years) |

| Hyperscale Data-Center Capacity Growth | +0.4% | NCR, Cavite, and New Clark City | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Build Better More Infrastructure Pipeline Expansion

The Philippines integrated facility management market is drawing support from the government’s broader infrastructure build-out because new rail, terminal, and utility assets create recurring service demand after construction ends. The PPP pipeline expanded materially by January 2026, and the project base now covers a larger set of assets that move into operating and maintenance phases over time.[1]Public-Private Partnership Center, “PPP Project Pipeline and Active Projects,” PPP Center In May 2026, the administration also unveiled a PHP 3.16 trillion (USD 54.6 billion) project pipeline, across 252 projects, with railway development taking the largest value share in that list. That matters because concessionaires usually focus on transport delivery and asset operation rather than building large in-house FM teams across every location. Providers that can combine technical maintenance, asset management, cleaning, and security are better positioned to win bundled work as these facilities come online. Procurement activity is therefore likely to deepen between 2027 and 2030, when today’s construction pipeline converts into a broader installed base of operating public assets.

Outsourcing Trend Among BPO and Commercial Offices

The Philippines integrated facility management market continues to benefit from the outsourcing practices of the office sector, especially where large occupiers prefer predictable service standards across multi-floor or campus-style sites. Metro Manila office transactions reached 847,000 sqm in 2025, and that recovery was supported by IT-BPM demand and faster expansion from Global Capability Centers. Provincial expansion also widened the contract map beyond Cebu and Davao, as operators added capacity in cities such as Bacolod and across other established delivery locations. This matters because BPO requirements are no longer limited to basic occupancy support, since healthcare information management, AI operations, and software development environments require better thermal control, more dependable power support, and cleaner indoor air. Those changes raise the FM specification of both existing and newly leased sites, which strengthens the case for integrated service contracts instead of separate single-service vendors. The demand base still carries some exposure to U.S. policy risk because North America remains the main origin of IT-BPM investment, so providers are increasingly testing revenue plans against slower client expansion scenarios.

Healthcare Facility Build-outs and Modernization

The Philippines integrated facility management market is also gaining from hospital expansion because new healthcare buildings require a tighter service model from the day they begin operations. Public and private projects both advanced during this period, including the Region 1 Medical Center expansion to 1,500 beds, the Las Piñas General Hospital building addition, and the Eastern Visayas Medical Center cancer center project. St. Luke’s Medical Center also proceeded with its PHP 18 billion Aseana hospital project, equivalent to USD 310.9 million, while Subic General Hospital remained on track for completion in 2026. Healthcare demand matters more than its current share suggests because these sites need cleaning, infection control, waste handling, security, engineering support, and life-safety compliance at a higher operating standard than ordinary offices. Public procurement has also tended to separate healthcare FM by service line, which opens opportunities for vendors that can compete through compliance capability and formal tender management. Providers with documented health, safety, and operating systems hold an advantage in this part of the market because hospital buyers place greater weight on auditability and procedural discipline.

Smart-Building and IoT-Enabled FM Adoption

The Philippines integrated facility management market is gradually moving toward a more data-led service model, especially in Grade A buildings and PEZA-linked assets where efficiency reporting is becoming increasingly important. The Energy Efficiency and Conservation Act requires designated establishments to complete energy audits and file annual compliance reports, and penalties can reach PHP 1 million (USD 17,271), for non-compliance. In 2026, energy IoT platforms were already being used in Philippine commercial and industrial buildings to automate meter reading, trigger anomaly alerts, and improve consumption analysis. This changes client expectations because monitoring tools are increasingly treated as part of normal service delivery rather than optional upgrades sold outside the base contract. The shift is also visible in provider strategy, as facility management is being combined with demand-side energy optimization for industrial and commercial clients. Over time, performance data itself becomes commercially important because providers that can interpret building data are more likely to retain client relationships and defend pricing against lower-specification competitors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-Labor Shortage and Wage Inflation | -1.3% | Philippines-wide, most acute in Taguig, Makati, and Cebu IT Park | Short term (≤ 2 years) |

| Energy-Cost Volatility in the Grid | -1.0% | Luzon, with intermittent supply risk in the Visayas | Short term (≤ 2 years) |

| Fragmented Supplier Base and Price Competition | -0.7% | Philippines-wide, especially in mid-market and provincial locations | Medium term (2-4 years) |

| Compliance Burden from Energy Efficiency and Conservation Act Audits | -0.6% | Designated establishments in NCR, Cebu, and Metro Davao | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortage and Wage Inflation

The Philippines integrated facility management market still faces a labour bottleneck, and the most acute shortage exists in licensed MEP engineers and senior technical supervisors. The problem is more severe in major business districts, where specialist roles can remain open for extended periods and experienced engineering staff command significant pay premiums over standard market benchmarks. Overseas demand worsens the shortage because Gulf employers continue to offer materially higher pay for comparable engineering and construction management roles. That outflow reduces the pool of experienced professionals available for technically demanding contracts in hospitals, industrial plants, and data centers. It also limits how quickly domestic providers can move beyond soft services into more complex hard FM scopes. At the same time, wage pressure weakens margins on fixed-price contracts, which is why providers are pushing for annual escalation clauses, even though some public-sector buyers remain resistant.

Energy-Cost Volatility in the Grid

The Philippines integrated facility management market is also exposed to energy-price swings because electricity remains a major controllable cost in hard FM delivery. In the April 2026 billing cycle, the Luzon wholesale electricity spot market price rose 52.5% to PHP 4.10 per kWh (USD 0.07 per kWh), after supply tightening, planned outages, and LNG disruptions affected the system.[2]Independent Electricity Market Operator of the Philippines, “Grid Conditions and Spot Market Pricing,” IEMOP The Energy Regulatory Commission then suspended WESM operations after warning that unmitigated prices could reach PHP 9 per kWh (USD 0.16 per kWh). These movements matter most for data centers, hospitals, and industrial plants, where uptime requirements make it more difficult to reduce load or defer maintenance. Providers that lock in renewable supply or establish better procurement structures are more protected from spot-market volatility than firms that simply pass through cost increases. The Visayas remains more vulnerable during forced outages because thinner reserve margins can still push prices into the PHP 6 to PHP 7 per kWh (USD 0.10 to USD 0.12 per kWh) range.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft FM Leads Revenue While Hard FM Gains from Technical Assets

Soft integrated facility management (FM) held 68.41% of the Philippines integrated facility management (IFM) market share in 2025, while Hard FM is projected to expand at a 6.07% CAGR through 2031. That revenue mix reflected the buyer base of the Philippines IFM industry, where office occupiers, hospitality sites, and retail-led facilities still account for a large share of active contracts. Cleaning, office support, and security remained the core revenue generators because they are required at high frequency and across a wide installed base of commercial premises. These services also offered providers repeat contract volumes and steadier cash flow than highly cyclical project-linked work. Catering remained more concentrated in industrial plants, hospitals, and very large BPO campuses where on-site food provision supports workforce welfare and operating continuity.

Hard FM is growing faster because new asset classes carry higher technical obligations in MEP, HVAC, fire safety, and planned maintenance. Data centers, railway systems, and hospital facilities are increasing the engineering intensity of the Philippines IFM market and pushing buyers toward preventive maintenance and asset management models. Within the hard FM stack, asset management and MEP and HVAC services hold the strongest revenue concentration because downtime in industrial, transport, and healthcare sites has direct operating consequences. Fire and life-safety services remain smaller in revenue terms, but they maintain a reliable demand floor because compliance is mandatory across public and private buildings. Other hard FM scopes, including civil maintenance and façade work, are expanding with the built environment, but they remain less differentiated than technical building systems work. PCAB Quadruple A classification and formal quality, environmental, and safety credentials continue to matter for large utility and government accounts, which keeps the top end of the service category more selective.[3]MIESCOR, “Company Certifications and Contractor Classification,” MIESCOR

By End-User Industry: Industrial and Process Holds the Largest Base, While Commercial Expands Fastest

The Industrial and Process Sector held 31.47% of the Philippines IFM market share in 2025, making it the largest end-user group by current revenue. This position was supported by manufacturing concentration in Calabarzon, Central Luzon, Northern Mindanao, and Metro Cebu, where multi-shift production keeps facilities operating for longer hours throughout the year. Electronics, automotive, food processing, and pharmaceutical plants require a more controlled service model, and buyers increasingly expect environmental monitoring, calibrated maintenance, and documentation-ready compliance support inside operating facilities. Central Luzon also has the strongest industrial supply pipeline, with 870 hectares of new space expected between 2026 and 2028, which expands the addressable base outside Metro Manila. PEZA compliance further strengthens outsourced demand because building, fire, and environmental standards must be maintained in a disciplined manner for accredited estates and export-oriented facilities.

Commercial end-users are projected to grow at a 5.91% CAGR through 2031, making them the fastest-growing part of the Philippines IFM industry. This group includes BFSI, IT and telecom, retail, and warehousing occupiers, and its momentum is tied to office absorption, asset recovery, and more complex tenant needs in prime locations. Metro Manila vacancy improved between late 2025 and early 2026, and office transactions in the first quarter still showed a healthy base of demand despite elevated supply. Hospitality users also continue to add volume, although their FM budgets remain more sensitive to occupancy shifts and labour planning than industrial contracts. Institutional and public infrastructure accounts will grow as PPP-delivered assets move into operation, while healthcare demand should accelerate as new hospital projects add both bed capacity and technical complexity. Other end-user groups, including residential complexes, sports venues, entertainment sites, and leisure assets, remain underpenetrated by integrated providers and therefore represent a broader medium-term opportunity once service models are adapted to smaller and more distributed locations.

Geography Analysis

Metro Manila remains the clearest demand center because the Philippines IFM market is still anchored by office campuses, mixed-use estates, hospitals, and data centers concentrated in NCR. Office transactions in Metro Manila reached 847,000 sqm in 2025, and another 193,000 sqm was recorded in the first quarter of 2026, which shows that occupier activity remained meaningful even in a high-supply environment. Fort Bonifacio, Makati, and Ortigas continue to shape buying patterns because they host many large occupiers that prefer outsourced cleaning, security, reception, engineering, and workplace coordination under formal service-level agreements. The same geography also carries a disproportionate share of the country’s premium-grade assets, which makes NCR the first market where digital monitoring, energy optimization, and integrated contracts become baseline requirements. Data-center expansion in Quezon City and Cavite adds another layer of technical demand around power redundancy, cooling systems, and round-the-clock engineering support.

Central Luzon and nearby Southern Luzon are becoming more important because industrial estate expansion is widening the Philippines integrated facility management market beyond its traditional office-heavy base. Manufacturing clusters in Calabarzon and Central Luzon create demand that is more engineering-led and less exposed to office occupancy cycles. The 870-hectare industrial pipeline expected in Central Luzon between 2026 and 2028 suggests that future contract growth will increasingly come from production halls, logistics assets, warehouses, and utility-intensive facilities. New Clark City also matters because it sits within the geography linked to hyperscale and transport-related infrastructure growth. These areas tend to favour providers that can handle uptime-sensitive maintenance, environmental compliance, and multi-site operations across dispersed estate locations.

The Visayas and Mindanao are gaining importance through healthcare, provincial BPO expansion, and selected commercial projects, even though provider capability remains thinner than in NCR. Cebu and Davao remain the strongest regional demand nodes, while Iloilo and Bacolod offer room for expansion as occupiers and service buyers become more distributed. Public hospital investments in Western Visayas, Bicol, and other regional areas are important because they create healthcare FM needs outside the main metropolitan core. The regional picture is less uniform, however, because the Visayas still faces intermittent supply constraints and thinner reserve margins, which can increase operating risk for technical FM delivery. Over time, regional demand should become more balanced, but the near-term map still favours NCR for large commercial contracts and Central Luzon and Calabarzon for industrial and infrastructure-led growth.

Competitive Landscape

The Philippines integrated facility management market is moderately fragmented. OCS Group, Sodexo, CBRE GWS, and JLL compete through scale, multi-country service systems, and stronger access to multinational procurement programs. Domestic names such as Servicio Filipino and MIESCOR remain relevant because local licensing, government familiarity, and operating relationships still matter in many contracts. The market is fragmented at the mid-market level, with more than 20 active providers operating across integrated and single-service models. This mix creates moderate consolidation at the top end, but it still leaves a long tail of smaller firms competing on price, location coverage, and service flexibility.

Technology and compliance are becoming clearer points of differentiation in the Philippines integrated facility management market. Global players are using IoT monitoring, predictive maintenance tools, and energy dashboards to support account renewal and strengthen cross-sell opportunities within existing client portfolios. Domestic providers can still compete when they hold strong credentials, and MIESCOR’s PCAB Quadruple A status, together with ISO 9001, ISO 14001, and ISO 45001 certifications, gives it a defensible position in utility and government-linked work. White space remains strongest in provincial mid-tier cities and in data-center FM, where cooling expertise, redundancy planning, and uptime discipline are still beyond the practical scope of many local vendors. As multinational buyers continue to consolidate vendors under single integrated service-level agreements, single-service specialists will find it increasingly difficult to protect market share in larger accounts.

Strategic moves by leading companies show how the competitive landscape is shifting in the Philippines' integrated facility management market. OCS strengthened its position after the integration of Atalian’s Asia operations, which increased delivery scale and standardized service protocols across its Philippine footprint. Servicio Filipino’s April 2026 IFM win in Bonifacio Global Center showed that domestic firms can still enter multinational-grade sites when they compete on responsiveness and relationship depth. The OCS Philippines partnership with CEMS also showed that energy optimization is moving closer to the center of the FM value proposition, especially for industrial and commercial clients. Taken together, these moves suggest that future winners will be firms that combine scale, compliance, technical depth, and data capability without losing local execution discipline.

Philippines Integrated Facility Management Industry Leaders

CBRE Group, Inc.

Jones Lang LaSalle Incorporated

Cushman & Wakefield plc

ISS A/S

Sodexo S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Marcos administration unveiled a PHP 3.16 trillion (USD 54.6 billion) infrastructure pipeline of 252 projects, with railway development accounting for 62% of total value. The pipeline's scale of O&M contracting embedded across transit, terminal, and port facilities is expected to drive significant new IFM procurement through 2028 and beyond.

- April 2026: STT GDC Philippines announced the expansion of its Fairview 1 data center to a total of 32 MW, with a second 32 MW phase under design for completion by late 2026 or early 2027. The company operates seven data centers across Metro Manila, Cavite, and Davao, all running on 100% renewable energy, and signed a 10-year renewable energy supply agreement with MPower.

- April 2026: Artelia Philippines articulated a strategic shift toward energy transition advisory and sustainable asset retrofit services, aligned with the Department of Energy’s 50% renewable energy target by 2050. The firm confirmed a decade-long engineering engagement with Shell plc spanning more than 500 Philippine sites, having logged 10 million safe man-hours between 2019 and 2025.

- April 2026: Servicio Filipino Inc. launched IFM operations at Bonifacio Global Center for a global sporting goods brand, deploying an integrated team covering housekeeping, reception, messenger services, and facility coordination, with the contract structured as a platform for expansion across the client’s broader Philippines portfolio.

Philippines Integrated Facility Management Market Report Scope

Philippines Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-user Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is driving growth in the Philippines integrated facility management space through 2031?

Growth is being supported by infrastructure delivery, office outsourcing, hospital expansion, and data-center development. The market is projected to rise from USD 0.96 billion in 2026 to USD 1.24 billion by 2031 at a 5.3% CAGR.

Which service category currently generates the most revenue?

Soft FM remains the largest service category, with a 68.41% share in 2025. Its scale reflects the large base of office, retail, hospitality, and BPO contracts that require frequent recurring support.

Why is Hard FM growing faster than Soft FM in the Philippines?

Hard FM is forecast to expand at a 6.07% CAGR because newer assets such as hospitals, rail systems, and data centers require planned maintenance, engineering support, and stricter life-safety compliance.

Which end-user group contributes the largest revenue base?

The Industrial and Process Sector led with a 31.47% share in 2025. Manufacturing clusters in Calabarzon, Central Luzon, Northern Mindanao, and Metro Cebu support continuous demand for technical upkeep and compliance-led services.

Which customer group is expected to grow the fastest?

Commercial end-users are projected to grow at a 5.91% CAGR through 2031. Office recovery, warehousing activity, IT and telecom demand, and higher workplace specifications are supporting this expansion.

What are the main risks for providers operating in this space?

The main risks are shortages of MEP and facility-management talent, along with energy-cost volatility. These pressures affect contract margins, technical capacity, and service delivery in power-sensitive assets such as hospitals and data centers.

Page last updated on: