Peru Cybersecurity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

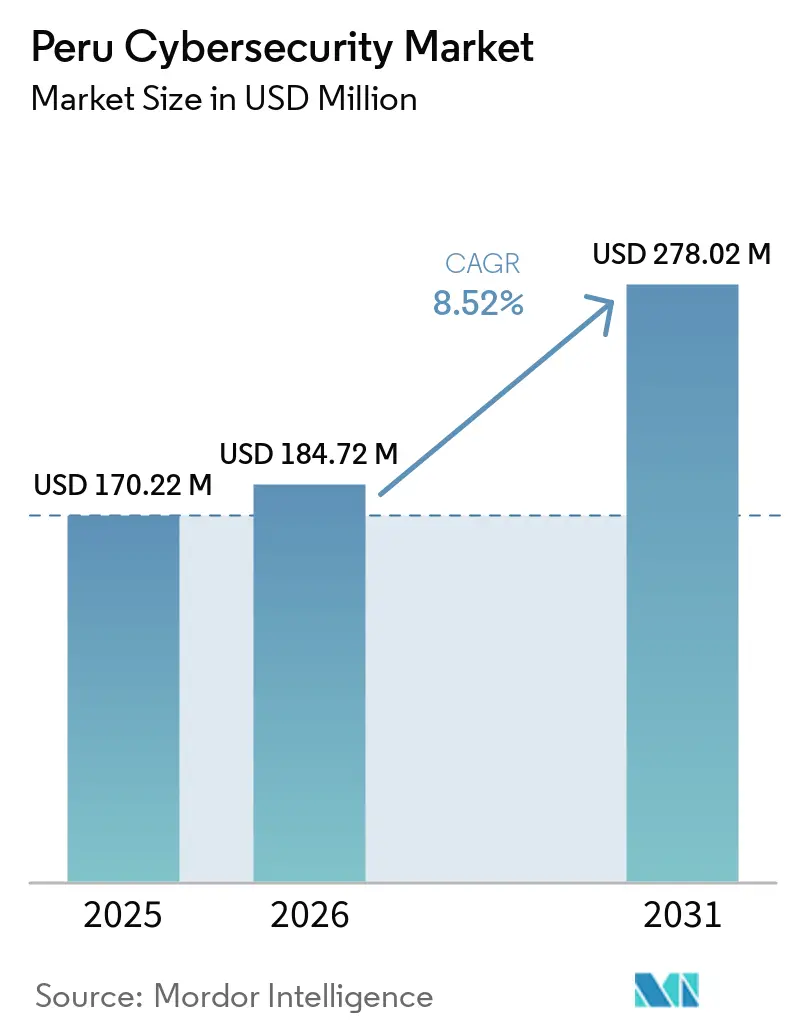

| Base Year Market Size (2025) | USD 170.22 Million |

| Market Size (2026) | USD 184.72 Million |

| Market Size (2031) | USD 278.02 Million |

| Growth Rate (2026 - 2031) | 8.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peru Cybersecurity Market Analysis by Mordor Intelligence

The Peru cybersecurity market size is projected to expand from USD 170.22 billion in 2025 and USD 184.72 billion in 2026 to USD 278.02 billion by 2031, registering a CAGR of 8.52% between 2026 to 2031. The Peru cybersecurity market is being lifted by a sharper threat environment, broader digitization across finance and public services, and a compliance cycle that is turning security from an optional spend line into a planned budget category. The Peru cybersecurity market is also benefiting from the way cloud migration, hybrid infrastructure, and outsourced security operations are now moving together rather than as separate technology decisions. Large institutions in Lima still account for much of the formal buying activity, but demand is spreading into mining corridors and provincial business centers as digital systems become more exposed. Competitive conditions remain moderate at the top end, with global platform vendors holding an advantage in breadth and integration, while regional specialists compete through local delivery, sector knowledge, and managed service models. The Peru cybersecurity market should also see more durable demand from payment modernization, public-sector digital trust programs, and gradual compliance deadlines that extend security buying into the later years of the forecast period.

Key Report Takeaways

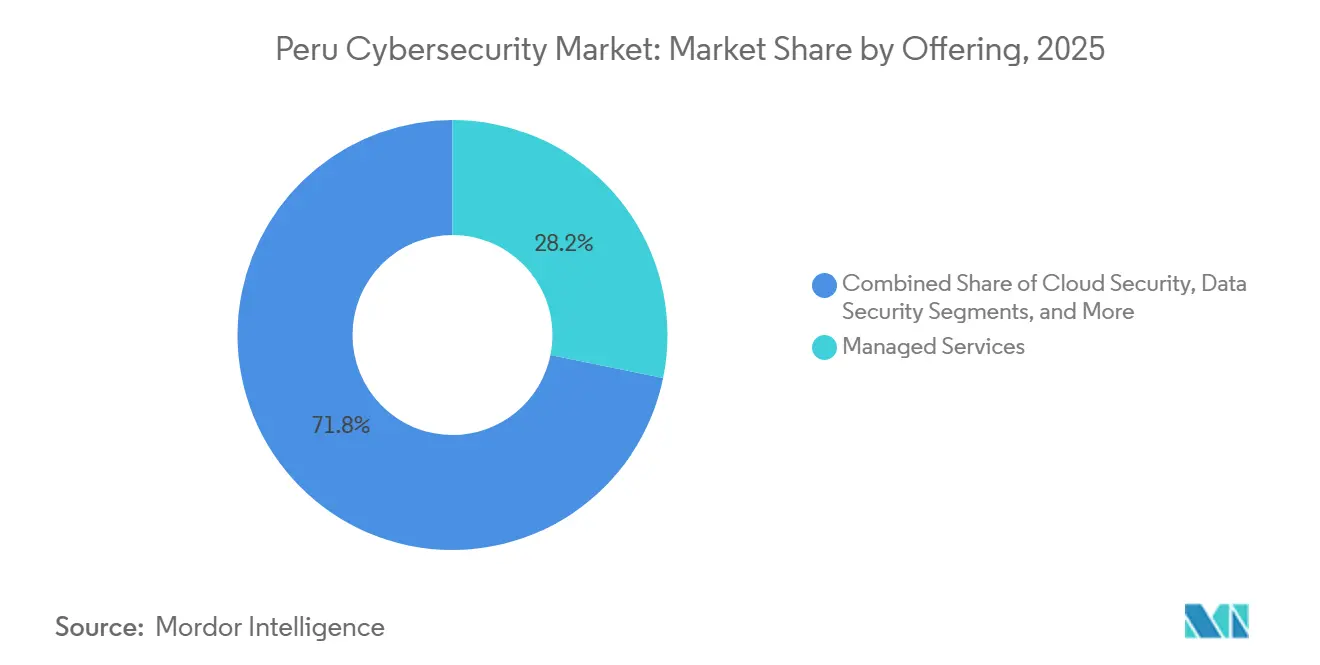

- By offering managed services held a 28.21% share of the Peru cybersecurity market in 2025, while cloud security is forecast to expand at a 13.71% CAGR through 2031.

- By deployment mode, cloud accounted for 62.36% of the Peru cybersecurity market size in 2025 and is also projected to grow at a 12.89% CAGR through 2031.

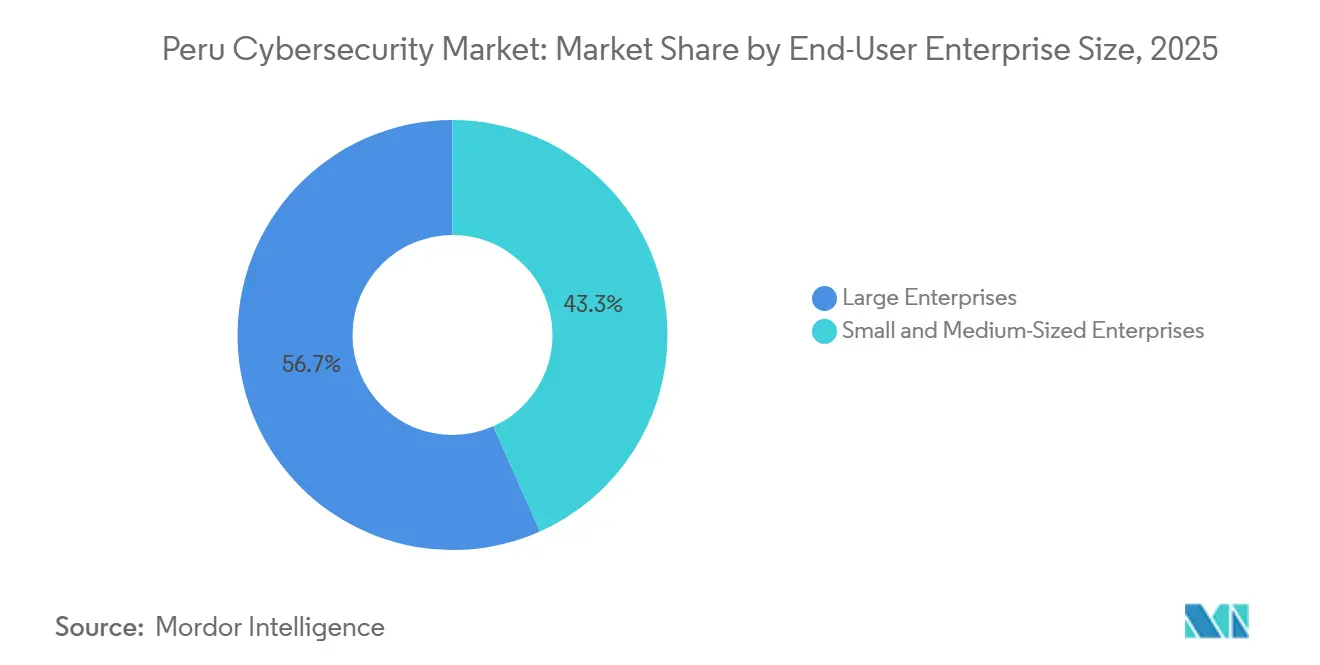

- By end-user enterprise size, large enterprises held 56.67% of the Peru cybersecurity market in 2025, while SMEs are forecast to advance at a 12.66% CAGR through 2031.

- By end user, BFSI captured 25.78% of the Peru cybersecurity market in 2025, while healthcare is projected to expand at a 12.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Peru Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Volume And Sophistication Of Cyberattacks | +2.8% | National, with peak exposure in Lima, Arequipa, and Piura | Short term (≤ 2 years) |

| Accelerated Digital Transformation In BFSI, Retail, And Government | +2.1% | National, with early gains in Lima financial and commercial districts | Medium term (2-4 years) |

| Tighter Data Protection And Digital Trust Compliance Requirements | +1.4% | National, financial and public-sector entities in Lima and regional capitals | Medium term (2-4 years) |

| Rapid Cloud And Managed Security Adoption | +1.2% | National, with cloud adoption concentrated in Lima and mining corridors | Medium term (2-4 years) |

| QR-Wallet Fraud And Real-Time Payment Abuse | +0.8% | Urban Peru, Lima Centro, La Libertad, and Ica are primary hotspots | Short term (≤ 2 years) |

| OT Security Investment In Mining And Energy Corridors | +0.6% | Andean mining zones, Junín, Apurímac, Moquegua, and Tacna | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Volume And Sophistication Of Cyberattacks

Peru recorded 1.7 billion cyberattack attempts in 2025, and more than 1 billion were active reconnaissance scans, which shows that attackers are spending more effort on mapping targets before execution. That pattern changes what buyers in the Peru cybersecurity market need, because broad perimeter defenses alone are less useful when adversaries are probing identities, workloads, and weak links over time.[1]Fortinet, “2026 Global Threat Landscape Report,” Fortinet, fortinet.com It also raises the value of continuous monitoring, log correlation, threat intelligence, and managed detection services that can spot abnormal behavior before a disruptive event develops. The Peru cybersecurity market is therefore seeing a clearer shift from one-time product purchasing toward ongoing visibility and response programs. National readiness efforts also show how persistent the threat climate has become, with Peru’s international cyberattack simulation expanding sharply in 2025 and the public digital security structure handling hundreds of alerts in 2026. As a result, the Peru cybersecurity market is increasingly shaped by demand for platforms and services that reduce response times, improve forensic depth, and strengthen resilience across both public and private networks.

Accelerated Digital Transformation In BFSI, Retail, And Government

Digitization in finance and public administration is widening the operational role of cybersecurity, rather than treating it as a separate technical layer. The Inter-American Development Bank approved a USD 65.8 million Banco de la Nación transformation program that directly included cybersecurity maturity alongside digital infrastructure and interoperability goals.[2]Inter-American Development Bank, “Banco de la Nación Digital Transformation Project (PE-L1286),” Inter-American Development Bank, iadb.org The financial system is also under closer supervision, with the IMF noting the breadth of regulated entities and the need for stronger sector coordination, governance, and incident response capabilities. Peru’s National Digital Transformation Policy placed digital trust among the country’s main strategic pillars, which means public entities are expected to embed security management, response planning, and governance into service delivery. The Peru cybersecurity market is also being supported by enterprise modernization programs such as Banco de Crédito del Perú’s hybrid cloud transformation with Kyndryl and Microsoft, where infrastructure change and security controls are being implemented within the same operating agenda. This keeps the Peru cybersecurity market closely tied to banking apps, state platforms, payment modernization, and retail digital channels that cannot scale safely without stronger protection layers.

Tighter Data Protection And Digital Trust Compliance Requirements

Peru’s data protection framework became more demanding after Supreme Decree 016-2024-JUS took effect on March 30, 2025, introducing 48-hour breach notification and stronger documentation expectations tied to recognized security standards.[3]Ministry of Justice and Human Rights, “Supreme Decree No. 016-2024-JUS: Supreme Decree That Approves the Regulation of Law No. 29733, Personal Data Protection Law,” El Peruano mirror, clinregs.niaid.nih.gov The decree also set a phased compliance path for data protection officer appointments, which spreads implementation pressure across large, medium, and smaller organizations over several years. That schedule matters for the Peru cybersecurity market because it supports repeat demand for advisory work, policy design, security assessments, integration, and audit preparation rather than a single short buying cycle. Peru also published the draft National Cybersecurity Strategy 2026-2028 with eight pillars that include critical infrastructure protection, public-sector implementation requirements, and stronger institutional coordination. The Peru cybersecurity market is therefore being supported by regulations that are becoming broader, more operational, and more measurable across agencies and regulated businesses. This makes security spending more durable because a growing part of the budget is now linked to legal accountability, governance readiness, and documented control maturity rather than discretionary upgrades.

Rapid Cloud And Managed Security Adoption

Cloud deployment already represented 62.36% of demand in 2025, while managed services led the offering mix with a 28.21% share, which shows how infrastructure change and outsourced defense are now reinforcing each other in the Peru cybersecurity market. Fortinet’s 2026 cloud security research found that 88% of companies operate in hybrid or multi-cloud environments, and nearly 70% identified tool sprawl and visibility gaps as major obstacles, which aligns with the complexity now appearing in Peru’s enterprise environments. That complexity favors MDR, SOC-as-a-Service, cloud posture management, and identity-centered controls because many local teams cannot run a full internal security operation across multiple environments. The Peru cybersecurity market is also benefiting from the fact that cloud-native tools can be deployed faster and priced more flexibly than many legacy on-premises systems. Large modernization programs in banking and mining are adding hybrid layers rather than replacing legacy estates in one step, so providers that can secure both sides of the architecture have a clear advantage. This is why the Peru cybersecurity market is moving toward unified platforms and recurring managed services instead of isolated point tools sold through one-time hardware transactions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Certified Cybersecurity Talent | -1.5% | National, most acute in provincial regions and SME-heavy sectors | Short term (≤ 2 years) |

| Budget Constraints Across SMEs | -1.0% | National, most pronounced outside Lima | Medium term (2-4 years) |

| Low Cyber Maturity Outside Lima | -0.6% | Provincial capitals, regional government entities, rural mining areas | Long term (≥ 4 years) |

| Public-Sector Procurement Volatility And Execution Delays | -0.4% | National, concentrated in central government ministries and state-owned enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Certified Cybersecurity Talent

The Peru cybersecurity market is still being held back by a shortage of qualified personnel who can run modern security programs, especially outside the largest institutions. Peru’s public digital governance data shows active capacity building, including 2,161 people trained in digital security in 2026, but the training pipeline remains smaller than the operational needs created by a more complex threat landscape. This gap affects the shape of demand as much as its speed, because organizations often postpone advanced projects when they cannot staff monitoring, response, governance, and compliance roles. It also pushes buyers toward outsourced models, which helps services revenue but limits the pace of fully internal security maturity. The Peru cybersecurity market therefore grows with a heavier dependence on MSSPs, vendor support, and external expertise than a more talent-rich environment would require. Until local education, certification, and retention improve at scale, workforce limits will continue to slow adoption in provincial institutions, smaller firms, and specialized operational environments.

Budget Constraints Across SMEs

SMEs remain one of the most difficult demand pools to convert into steady security spending, even though they face rising exposure and a growing compliance burden. ICEX noted that small companies may allocate up to 10% of IT budgets to cybersecurity, but those percentages still convert into small absolute budgets in much of the Peruvian business base.[4]ICEX España Exportación e Inversiones, “El Mercado de la Ciberseguridad en Perú,” ICEX España Exportación e Inversiones, icex.es That budget reality keeps many smaller organizations focused on baseline controls, while more advanced capabilities such as continuous monitoring, formal audits, and integrated response planning are delayed. The Peru cybersecurity market is trying to close that gap through subscription pricing, managed endpoint protection, and shared SOC models that reduce upfront cost barriers. Even so, adoption outside Lima often moves slowly because management teams still weigh security against near-term operating pressures and see it as a compliance expense before they see it as a business continuity safeguard. This means the Peru cybersecurity market continues to rely on simplified service bundles and lower-entry offerings if it wants to broaden penetration across the SME base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Managed Services Lead As Cloud Security Accelerates

Managed services held a 28.21% share of the Peru cybersecurity market in 2025, making them the largest offering category and reflecting a clear preference for recurring, externally supported protection models. This leadership says a great deal about the Peru cybersecurity market because many organizations want stronger defense outcomes without building a full 24-hour internal operation. Demand has been strongest in managed security operations, threat monitoring, and detection-focused services, where buyers need operational continuity more than additional standalone tools. The pattern also shows how the Peru cybersecurity industry is shifting away from isolated product sales and toward ongoing service delivery that bundles monitoring, incident handling, and platform management. In practical terms, this helps enterprises address talent shortages and gives regional providers a workable entry point against larger global vendors. It also broadens the buying base because managed services can be priced in ways that are easier for mid-sized firms to absorb than large upfront platform deployments.

Cloud security is the fastest-growing subsegment within solutions, with a 13.71% CAGR through 2031, which reflects the spread of hybrid workloads and the limits of older perimeter-first controls. Enterprises in the Peru cybersecurity market now need posture management, workload visibility, identity controls, and application protection that follow data and users across multiple environments rather than sitting only at the network edge. Network security, identity and access management, and endpoint security still act as the main spending anchors, because they remain essential to regulated institutions and broad enterprise estates. At the same time, consulting, risk assessment, and compliance services are gaining weight as the regulatory cycle pushes more organizations to document policies, assign responsibilities, and test controls. That creates a two-speed structure inside the Peru cybersecurity market, where core protection spending remains steady and governance-driven services rise alongside it. The Peru cybersecurity industry is therefore becoming more service-heavy without reducing the importance of integrated product platforms that support those services.

By Deployment Mode: Cloud Dominates As Hybrid Architectures Multiply

Cloud deployment accounted for 62.36% of the Peru cybersecurity market size in 2025, and it is also projected to expand at a 12.89% CAGR through 2031. That combination means the largest deployment model is also the fastest-moving one, which concentrates a significant share of future growth along the cloud axis. The Peru cybersecurity market is seeing this pattern because cloud controls are becoming easier to deploy, more adaptable to distributed work and digital channels, and more compatible with subscription pricing. Peru’s projected cloud services investment of USD 1.149 billion in 2026 also signals an environment where hyperscale infrastructure, hosted platforms, and remote operations will keep expanding the need for cloud-native security tools. Even where that infrastructure investment does not replace local systems immediately, it still changes how security policies, identities, and visibility layers must be managed. This is why cloud has become the anchor deployment model across much of the Peru cybersecurity market.

On-premises deployment still matters in heavily regulated and operationally complex settings, especially in financial institutions with data control demands and mining sites where connectivity conditions remain uneven. Hybrid environments are multiplying because enterprises are not replacing legacy estates in one move, and instead are connecting new cloud resources to existing core systems. That makes architecture more flexible, but it also adds policy fragmentation, visibility gaps, and exposure across identities, endpoints, applications, and operational technology. The Peru cybersecurity market is therefore rewarding vendors that can deliver consistent controls across cloud, on-premises, and mixed environments. Mining digitization adds another layer to this shift, as connected operations centers and remote management systems need protection across both plant-level systems and cloud-linked analytics platforms. As hybrid estates deepen, the Peru cybersecurity market is likely to keep favoring unified policy management and managed oversight rather than separate tools for each deployment domain.

By End-User Enterprise Size: Large Enterprises Lead While SMEs Accelerate

Large enterprises held 56.67% of demand by enterprise size in 2025, showing that the Peru cybersecurity market still draws most of its current spending from organizations with larger budgets, formal governance structures, and higher-value assets. These buyers usually have more mature procurement processes, stronger regulatory exposure, and a clearer ability to justify enterprise-grade platforms and services. They also tend to be concentrated in BFSI, telecommunications, major retail, and public institutions where digital services and reputational stakes are high. This keeps large organizations at the center of the Peru cybersecurity market, especially when purchases involve integrated architecture, managed response, and multiyear transformation programs. It also helps explain why much of the competitive activity still clusters in Lima and other major commercial hubs. In short, the current demand base remains led by institutions that can absorb complex implementations and longer security road maps.

SMEs, however, are forecast to grow at a 12.66% CAGR through 2031, making them the fastest-expanding enterprise-size group in the Peru cybersecurity market. Their growth is being supported by phased compliance requirements, growing exposure to digital fraud and ransomware, and the wider availability of subscription-based protection that lowers entry barriers. Many smaller firms are beginning their security journey with policy work, basic assessments, managed endpoint protection, and outsourced monitoring before they consider more advanced controls. That entry path matters because it widens the commercial reach of the Peru cybersecurity market without requiring SMEs to build internal teams that they often cannot afford. At the same time, the gap between large enterprise maturity and SME readiness is still wide, so growth in the smaller segment will likely stay service-led rather than infrastructure-led. This means the Peru cybersecurity market should continue to see SMEs as an expansion engine, while large enterprises remain the main source of present-day scale.

By End User: BFSI Commands Share As Healthcare Grows Fastest

BFSI held 25.78% of the Peru cybersecurity market share in 2025, confirming that finance remains the most important end-user vertical by current demand. This position reflects strong supervisory pressure, the central role of digital payments and banking channels, and the high sensitivity of customer data, transaction integrity, and service continuity. IMF work on Peru’s financial sector cybersecurity also pointed to the need for stronger coordination, governance, testing, and incident management, which reinforces why banks and related institutions remain core buyers. The Peru cybersecurity market also benefits from the fact that financial institutions often combine infrastructure modernization and security investment in the same program, which supports larger and more integrated contracts. That is visible in high-profile transformation work involving cloud, identity, resilience, and managed oversight. As long as regulation and digital payments keep deepening, BFSI will remain the anchor vertical within the Peru cybersecurity market.

Healthcare is the fastest-growing end-user segment, with a 12.36% CAGR through 2031, as electronic records, connected care systems, and digitally linked clinical workflows expand the number of vulnerable assets. This growth also reflects the wider global pattern in which healthcare environments carry high operational urgency and sensitive data, making them attractive targets for disruptive attacks. Government and defense remain important but unevenly developed, because national programs and formal implementation have advanced faster than operational maturity across all agencies. Peru reported that all ministries and regional governments had implemented an information security management system by April 2026, but the depth of implementation still varies by institution. Mining and energy are also moving upward as connected production systems, remote telemetry, and automated operations increase exposure across industrial environments. The Peru cybersecurity market is therefore broadening beyond finance, with healthcare, government, manufacturing, education, retail, and resource sectors all adding to the next wave of spending.

Geography Analysis

Lima and its metropolitan corridor dominated demand in the Peru cybersecurity market in 2025, even though the supplied material does not assign a precise geographic percentage split. The concentration is logical because Lima hosts the largest financial institutions, central government entities, major telecommunications operators, and many enterprise headquarters that account for the heaviest formal security spending. Public digital governance data also shows that the national security structure is coordinating a large institutional network, with 420 entities in the national CSIRT network and 313 digital security alerts handled in the first months of 2026. Those institutional capabilities support the concentration of response activity around the capital, where exposure, transaction density, and policy oversight are also the highest. The Peru cybersecurity market, therefore, still reflects a capital-centered demand pattern in which Lima sets adoption standards, vendor visibility, and early purchasing behavior.

The Andean mining and energy corridor forms a second geographic layer with a different risk profile and a distinct buying logic. Mines such as Quellaveco, Toquepala, Las Bambas, Antapaccay, and Minsur are deploying 5G, telemetry, autonomous systems, and AI-supported maintenance, which raises the need for IT and OT convergence security. This makes Junín, Apurímac, Moquegua, and Tacna especially relevant to the Peru cybersecurity market because connected industrial sites need protection that fits remote, continuous, and safety-sensitive operations. In these zones, ruggedized platforms, remote monitoring, identity control, and secure connectivity all become more important than standard office-centered security tools. The Peru cybersecurity market is also benefiting from the fact that mining digitization tends to be multiyear and capital-intensive, which supports longer security programs rather than one-off purchases.

A third geographic layer includes provincial capitals such as Arequipa, Trujillo, Piura, Chiclayo, and Cusco, where the Peru cybersecurity market is smaller today but increasingly important for future expansion. In these cities, demand is rising through digital government services, more online commerce, broader data protection duties, and gradual extension of enterprise security practices beyond Lima. Peru’s improved standing in the ITU Global Cybersecurity Index 2024, where it ranked 5th among South American and Caribbean economies and performed strongly on organizational and capacity-building pillars, suggests that institutional progress is becoming more visible across the country PCM. Even so, adoption in provincial locations still trails Lima because staffing, budgets, and implementation depth are less consistent. That leaves the Peru cybersecurity market with a clear regional opportunity, where future growth depends on turning compliance, training, and digital service expansion into stronger operational maturity outside the capital.

Competitive Landscape

The Peru cybersecurity market is moderately concentrated at the top and fragmented across the rest of the supplier base. The five largest vendors, Accenture, Microsoft, Broadcom, Fortinet, and Akamai, accounted for 41%-46% of the Peru cybersecurity market share in 2025, while the remaining demand was spread across regional integrators, local managed service providers, and specialist firms. This structure gives global vendors an advantage in platform breadth, threat intelligence depth, and the ability to bundle services across cloud, network, identity, and endpoint domains. At the same time, it leaves meaningful room for local and regional firms that compete through sector familiarity, geographic reach, and lower-cost managed delivery. The Peru cybersecurity market therefore does not behave like a winner-take-all field, even though the top tier still shapes much of the large-enterprise and public-sector agenda.

Strategic moves by leading companies show that the competitive focus is shifting toward integrated delivery rather than isolated products. Kyndryl’s recognition as 2025 Microsoft Peru Partner of the Year, linked to Banco de Crédito del Perú’s hybrid cloud implementation, highlights the appeal of programs that combine modernization, cloud operations, and cybersecurity within one transformation path. Fortinet’s official research and product direction also show how vendors are tying together cloud complexity, AI-supported security operations, and platform integration as core commercial themesT. The Peru cybersecurity market is rewarding these approaches because buyers increasingly prefer fewer vendors that can cover multiple layers of the environment. That preference raises switching costs and favors suppliers that can link architecture, managed services, and compliance support under one operating model.

White space is still substantial in provincial managed services, OT security, and SME-oriented compliance tooling. The Peru cybersecurity market remains underpenetrated outside the largest urban institutions, which creates room for focused providers that can serve mining corridors, regional capitals, and mid-market firms with simpler operating models. Public-sector implementation depth also varies widely, so vendors that can pair governance support with operational tooling have a stronger chance of expanding beyond the first tier of clients. Compliance-linked buying is becoming another differentiator, especially where customers want implementation partners that can translate legal requirements into working controls and documented assurance. This means the Peru cybersecurity market should continue to support both broad global platforms and more focused service specialists, rather than converging rapidly around a very small vendor set. Competitive success will likely depend less on product breadth alone and more on who can deliver reliable local execution, hybrid coverage, and measurable response outcomes.

Peru Cybersecurity Industry Leaders

Accenture plc

Microsoft Corporation

Broadcom Inc.

Fortinet, Inc.

Akamai Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Presidency of the Council of Ministers (PCM) conducted a workshop in collaboration with ICANN to strengthen the resilience of Peru's governmental IT systems and enhance institutional response capacity against cybercrime, part of ongoing capability-building under the Digital Government Law framework.

- February 2026: Minera Chinalco Peru brought its Integrated Operations Management Center (GIO) to full operation at the Toromocho copper mine in Junín, integrating advanced analytics, teleoperation, and cyber and physical security systems within a single command layer. Chinalco's 2026 capital plan includes USD 400 million in mining investment, with the GIO representing a flagship example of OT security embedded into large-scale digital mining infrastructure.

- January 2026: The Central Reserve Bank of Peru's (BCRP) Circular 0022-2025-BCRP took effect, establishing legally binding standards for payment system cybersecurity, periodic resilience testing, mandatory breach reporting, and doubled sanctions for non-compliance, including potential revocation of operating authorization for serious offenders. The circular formally extends cybersecurity oversight to payment service providers and open banking participants.

- November 2025: Kyndryl was recognized as 2025 Microsoft Peru Partner of the Year for the third consecutive year, with the Banco de Crédito del Perú hybrid cloud implementation cited as a regional benchmark for financial-sector digital transformation and cybersecurity integration.

Peru Cybersecurity Market Report Scope

The Peru Cybersecurity Market Report is Segmented by Offering (Solutions and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), End-User Enterprise Size (SMEs and Large Enterprises), End User (BFSI, Government and Defense, IT and Telecom, Mining and Energy, Retail and E-Commerce, Healthcare, Manufacturing, and Education), and Geography (Peru). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| Endpoint Security | |

| Security Information and Event Management | |

| Threat Intelligence and Analytics | |

| Other Solution Types | |

| Services | Consulting and Risk Assessment |

| Integration and Deployment | |

| Incident Response and Retainer Services | |

| Managed Detection and Response | |

| Managed Security Operations | |

| Compliance and Audit Services |

| Cloud |

| On-Premises |

| Hybrid |

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| BFSI |

| Government and Defense |

| IT and Telecom |

| Mining and Energy |

| Retail and E-Commerce |

| Healthcare |

| Manufacturing |

| Education |

| Other End-User Industries |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| Endpoint Security | ||

| Security Information and Event Management | ||

| Threat Intelligence and Analytics | ||

| Other Solution Types | ||

| Services | Consulting and Risk Assessment | |

| Integration and Deployment | ||

| Incident Response and Retainer Services | ||

| Managed Detection and Response | ||

| Managed Security Operations | ||

| Compliance and Audit Services | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By End-User Enterprise Size | Small and Medium-Sized Enterprises | |

| Large Enterprises | ||

| By End User | BFSI | |

| Government and Defense | ||

| IT and Telecom | ||

| Mining and Energy | ||

| Retail and E-Commerce | ||

| Healthcare | ||

| Manufacturing | ||

| Education | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current and forecast value of Peru cybersecurity demand?

The Peru cybersecurity market stood at USD 184.72 billion in 2026 and is forecast to reach USD 278.02 billion by 2031, rising at an 8.52% CAGR.

Which offering category leads spending in Peru?

Managed services led the offering mix with a 28.21% share in 2025, showing strong reliance on outsourced monitoring, response, and security operations.

Why is cloud security growing so quickly in Peru?

Cloud security is forecast to grow at a 13.71% CAGR through 2031 because hybrid and multi-cloud environments need stronger posture management, identity controls, and workload protection.

Which customer group is expanding fastest?

SMEs are the fastest-growing enterprise-size segment, with a 12.66% CAGR through 2031, supported by subscription-based services and rising compliance pressure.

Which end-user vertical currently spends the most on cybersecurity in Peru?

BFSI held 25.78% of demand in 2025 because financial institutions face the strongest regulatory pressure and some of the highest exposure to digital fraud and service disruption.

How concentrated is supplier competition in Peru?

Competition is moderate at the top, with the five largest vendors holding 41%-46% of 2025 share, while many regional integrators and specialists still serve the rest of the market.

Page last updated on: