Morocco Cybersecurity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

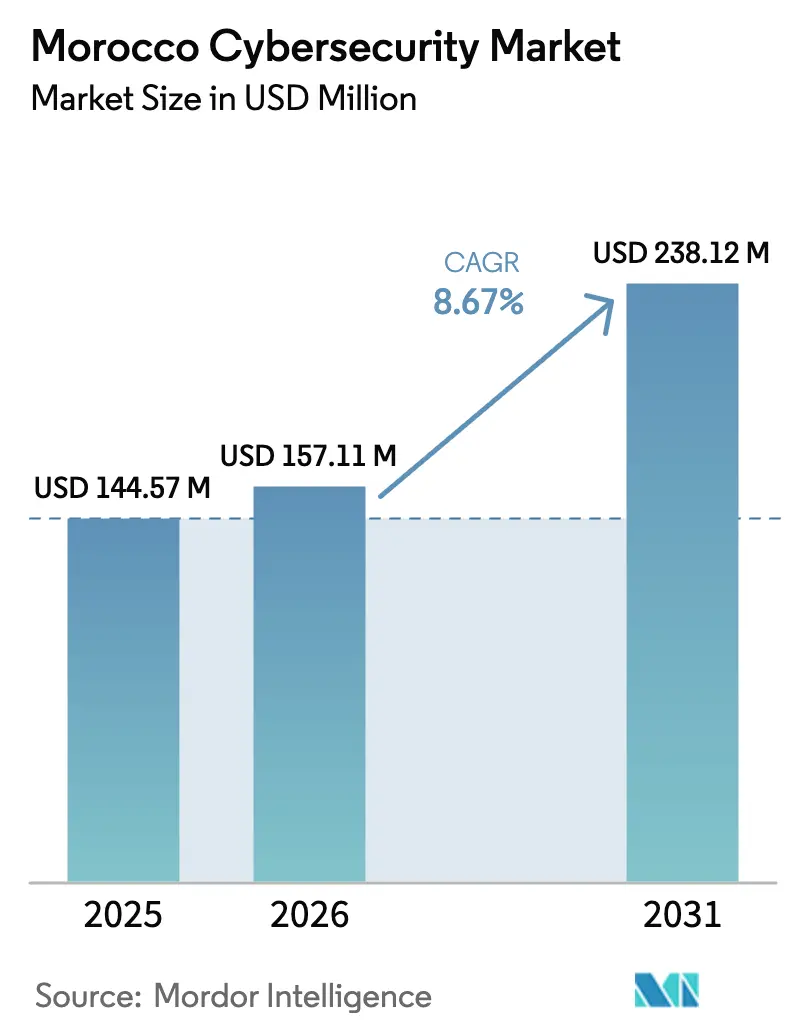

| Base Year Market Size (2025) | USD 144.57 Million |

| Market Size (2026) | USD 157.11 Million |

| Market Size (2031) | USD 238.12 Million |

| Growth Rate (2026 - 2031) | 8.67% CAGR |

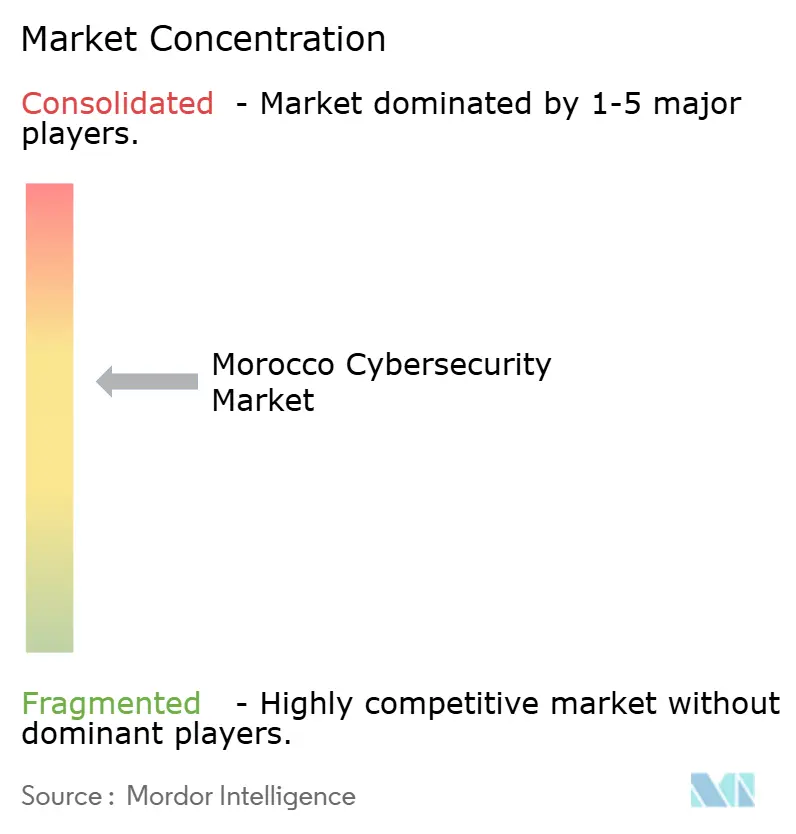

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Cybersecurity Market Analysis by Mordor Intelligence

The Morocco cybersecurity market size was valued at USD 144.57 million in 2025 and estimated to grow from USD 157.11 million in 2026 to reach USD 238.12 million by 2031, at a CAGR of 8.67% during the forecast period (2026-2031). The current growth reflects the country’s ambition to position itself as a pan-African digital hub through the government’s Digital Morocco 2030 program, a multi-year initiative prioritizing secure connectivity, hybrid-cloud adoption, and critical-infrastructure protection. Morocco’s early move to a national cloud-first policy, coupled with the roll-out of local hyperscale cloud regions, is expanding procurement options while sustaining demand for secure Infrastructure-as-a-Service and managed detection platforms. Heightened threat visibility in the wake of the April 2025 CNSS breach has pushed authentication upgrades, endpoint hardening, and 24/7 monitoring onto executive agendas across public and private sectors. Structural challenges—chiefly a shortage of Arabic- and French-speaking cyber talent and license-cost exposure to the USD—continue to shape vendor selection, strengthen the case for managed security services, and open opportunities for local skills-development programs.

Key Report Takeaways

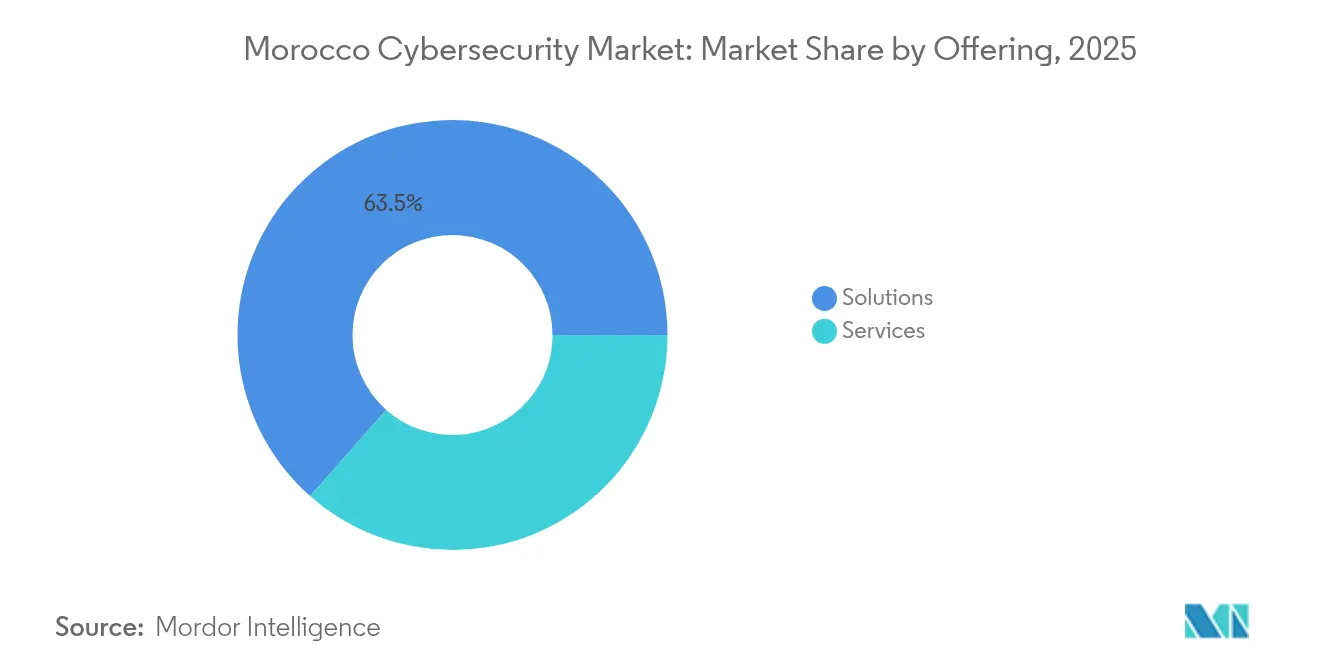

- By offering, solutions led with 63.48% revenue share in 2025, whereas managed security services are projected to expand at a 15.23% CAGR through 2031.

- By deployment mode, on-premise installations held 54.86% of the Morocco cybersecurity market share in 2025; cloud-based deployments are forecast to post the fastest CAGR at 17.42% through 2031.

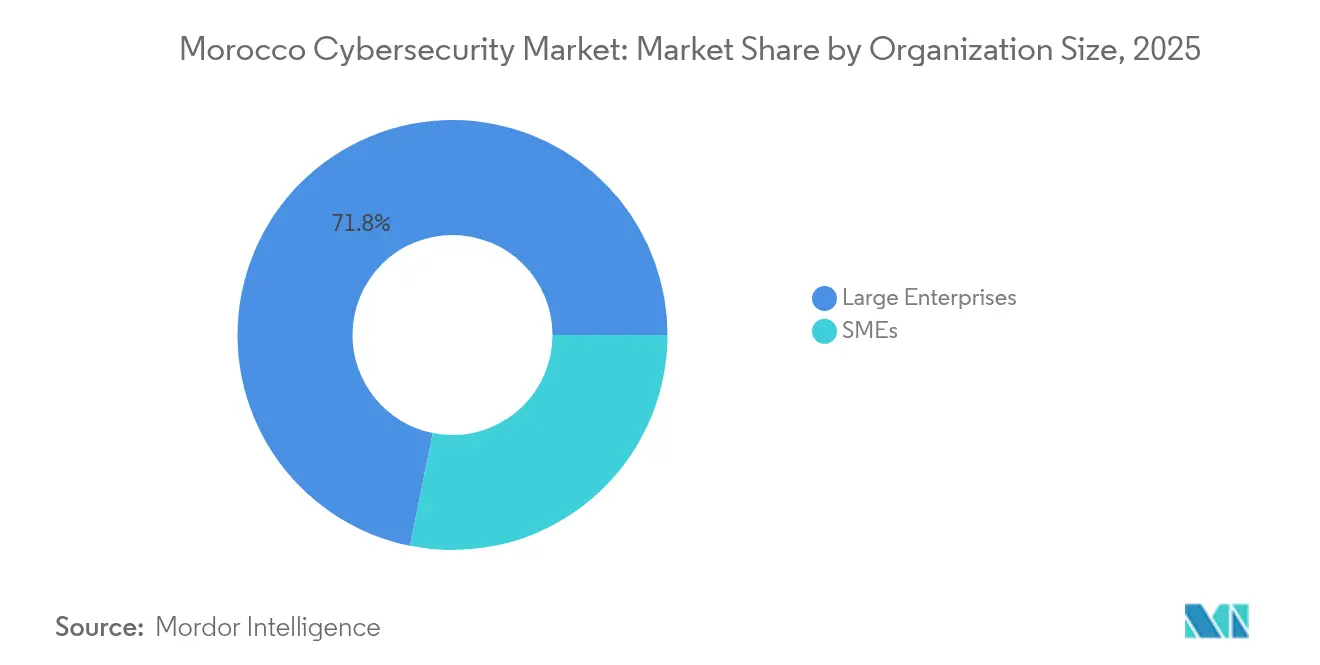

- By organization size, large enterprises accounted for 71.83% share of the Morocco cybersecurity market size in 2025, while SMEs are poised to grow at a 15.67% CAGR to 2031.

- By end-user vertical, banking, financial services, and insurance held 25.10% revenue share in 2025; healthcare is set to grow the quickest at 16.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Morocco Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Phishing-as-a-Service (PhaaS) Networks Targeting Moroccan Banks | +1.8% | National, concentrated in Casablanca and Rabat financial districts | Short term (≤ 2 years) |

| Accelerated Digital Identity Projects under Morocco Digital 2030 | +2.1% | National, with pilot programs in major urban centers | Medium term (2-4 years) |

| Surge in Cyber-Insurance Uptake by Casablanca-based Exporters | +0.9% | Regional, focused on Casablanca export hub | Medium term (2-4 years) |

| Government Cloud-First Policy Spurring Secure IaaS Demand | +1.6% | National, prioritizing government agencies and SOEs | Long term (≥ 4 years) |

| Tanger-Med Port's 5G Roll-out Creating New OT-Security Spend | +0.7% | Regional, Tangier-Tetouan-Al Hoceima region | Short term (≤ 2 years) |

| FIFA 2030 Bid Driving Critical-Infrastructure Hardening Budgets | +1.2% | National, with focus on host cities and transport corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Phishing-as-a-Service Networks Targeting Moroccan Banks

The April 2025 CNSS compromise underscored the geopolitical threat landscape after an Algerian actor weaponized a zero-day in widely deployed database middleware. Financial institutions responded by accelerating roll-outs of multi-factor authentication, encrypted database gateways, and outsourced 24/7 monitoring to contain similar attack chains. Spending on managed detection and response platforms is therefore projected to keep outpacing overall Morocco cybersecurity market growth as banks align controls with central-bank supervisory guidelines.

Accelerated Digital-Identity Projects under Digital Morocco 2030

Digital Morocco 2030 targets issuance of secure digital IDs to every citizen and aims to create 240,000 tech jobs by 2030. Pilots in Casablanca, Rabat, and Marrakech demonstrate that identity-and-access-management platforms, cloud key-management services, and compliance monitoring tools will anchor enterprise security architectures over the forecast period. Sustained procurement is expected from ministries rolling out hybrid architectures that balance on-premise confidentiality demands with agile cloud analytics.

Government Cloud-First Policy Spurring Secure IaaS Demand

The Directorate-General of Information Systems Security (DGSSI) requires government workloads rated Très Sensible to remain onshore[1]DGSSI, “Strategie Nationale de Cybersécurité,” dgssi.gov.ma. Oracle’s twin public-cloud regions, which opened in 2024, now meet that residency mandate and allow ministries to replace capex-intensive data centers with pay-as-you-go secure IaaS. This shift directly feeds next-generation firewall, secure-access-service-edge, and automated compliance tooling spend.

FIFA 2030 Bid Driving Critical-Infrastructure Hardening Budgets

The 2025–2029 capex pipeline tied to the World Cup includes upgrades for the Casablanca-Rabat high-speed rail corridor, Tanger-Med port terminals, and multiple power substations. Industrial-control-system security, OT network segmentation, and incident-response retainer contracts are therefore forecast to post double-digit growth, supporting the long-run trajectory of the Morocco cybersecurity market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortfall of Arabic/French-Speaking Cyber Talent Raising MSSP Prices | -1.4% | National, acute in Casablanca and Rabat tech hubs | Long term (≥ 4 years) |

| Fragmented Legacy SOCs among State-Owned Enterprises | -0.8% | National, concentrated in government agencies and SOEs | Medium term (2-4 years) |

| Low Cyber-Insurance Penetration outside BFSI Slowing Risk-Transfer Spend | -0.6% | National, particularly affecting SME segments | Medium term (2-4 years) |

| Budget Volatility Tied to Dirham Depreciation vs. USD-priced Licenses | -0.9% | National, affecting all sectors with international procurement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortfall of Arabic/French-Speaking Cyber Talent Raising MSSP Prices

Local service providers report vacancy rates above 25% for tier-two analysts. The result is upward fee pressure that narrows the cost gap between in-house operations and outsourcing. While universities expanded cyber curricula in 2025, day-one-ready practitioners remain scarce, delaying in-market delivery capacity and tempering the CAGR of the Morocco cybersecurity market.

Fragmented Legacy SOCs among State-Owned Enterprises

Multiple ministries still operate siloed security tools that lack event-correlation or automated response. The CNSS incident exposed those integration gaps despite prior audit spending. Harmonizing architectures around shared playbooks and XDR platforms is now a budget priority, yet procurement cycles across SOEs remain lengthy, muting near-term tailwinds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Dominance Amid Services Acceleration

Solutions retained 63.48% revenue in 2025, underscoring the preference across finance, government, and utilities for appliance-centric protection led by network firewalls, endpoint suites, and identity-governance platforms. This foundation secured immediate risk-reduction after the CNSS breach and continues to anchor refresh budgets. At the same time, managed security services are expanding at a 15.23% CAGR as organizations pursue 24/7 coverage and advanced threat hunting that internal teams cannot staff.

Professional-service spend tracks platform deployments, covering red-team exercises, configuration audits, and migration support. Cloud workload-protection, application-security testing, and data-loss-prevention platforms are the fastest-growing sub-categories as ministries roll out micro-service architectures under the cloud-first directive. The Morocco cybersecurity market therefore shows a two-speed pattern: hardware refresh cycles stabilize overall revenue, while annuity-based service contracts drive incremental growth.

By Deployment Mode: Cloud Transformation Accelerating

On-premises estates still account for 54.86% of market revenue in 2025, reflecting decades of data-sovereignty rules and the early dominance of appliance-based designs. However, cloud deployments are outpacing all other segments at an 17.42% CAGR through 2031 on the back of Oracle, Huawei Cloud, and AWS local zone expansions. The Morocco cybersecurity market size related to cloud security controls is forecast to reach USD 84.6 million by 2031, illustrating rapid wallet shift toward secure IaaS and SaaS.

Hybrid models dominate among tier-one banks and telecom operators that must retain core-ledger data on-premises while leveraging cloud analytics for fraud detection. Consequently, secure access-service-edge, cloud access security brokers, and workload-encryption gateways are moving from proof of concept to production across Casablanca’s data center corridor.

By Organization Size: SME Cybersecurity Democratization

Large enterprises held 71.83% spending in 2025 owing to deeper budgets, internal compliance teams, and exposure to region-wide attacks. Their spending direction sets vendor roadmaps, particularly for privileged-access-management and secure-software-development-lifecycle tooling. Yet SMEs are scaling fastest at 15.67% CAGR, closing essential gaps with subscription-based endpoint detection and response suites and cloud-native secure email gateways.

SME traction is further propelled by subsidized training schemes under Digital Morocco 2030 and the availability of Arabic dashboards that lower language barriers. Several domestic integrators now bundle cyber-insurance with monitoring, providing smaller exporters a one-invoice path to compliance, thereby enlarging the addressable Morocco cybersecurity market.

By End-User Vertical: Healthcare Emerges as Growth Leader

The BFSI sector contributed 25.10% of 2025 spend as banks prioritized SWIFT security controls and real-time fraud analytics. Moving forward, hospitals and e-health platforms will deliver the highest CAGR of 16.74% as electronic-medical-record roll-outs converge with new regulations on patient-data confidentiality. The Morocco cybersecurity market size for healthcare is projected to grow from USD 12.45 million in 2026 to USD 26.9 million in 2031.

Energy and utilities sustain above-average growth through mandatory IEC 62443 compliance for substations feeding Tanger-Med and the 850 MW Noor solar complex. Meanwhile, manufacturing adoption is guided by Industry 4.0 pilots in the Casablanca-Settat region that require OT-specific intrusion detection and secure remote-maintenance channels.

Geography Analysis

Casablanca and Rabat together generate nearly 59.70% of the Morocco cybersecurity market thanks to the concentration of headquarters, data centers, and regulatory bodies. Both cities benefit from carrier-neutral facilities that host banking core systems and SaaS aggregators, keeping cybersecurity budgets high and distributed across identity, network, and data-protection layers. Tangier’s port district is the fastest-expanding regional pocket, boosted by IT/OT convergence projects attached to the Tanger-Med port’s 5G network and the Dakhla Atlantic Port build-out.

Outside these hubs, national programs are seeding regional centers of excellence. The Ministry of Digital Transition funds Cyber-Ready zones in Fez-Meknes and Souss-Massa that pair fibre roll-outs with shared security operations workspaces for local SMEs. This decentralization diversifies end-user demand, lifting baseline adoption of cloud-delivered secure web gateways and MFA tokens.

Internationally, Morocco’s Tier-1 ranking in the 2024 ITU Global Cybersecurity Index underpins cross-border service exports. Managed SOCs in Casablanca now monitor French-speaking administrations across West Africa, expanding the revenue pool for domestic providers and aligning local best practices to international frameworks such as ISO 27035.

Competitive Landscape

Global vendors IBM, Cisco, Microsoft, and Palo Alto Networks leverage direct enterprise frameworks to maintain share in next-gen firewall, SIEM, and XDR categories. Oracle’s sovereign-cloud regions provide a platform edge in database and identity-security workloads, especially across ministries bound by DGSSI data-classification rules.

Regional specialists DATAPROTECT and Orange Cyberdefense differentiate on French-language SOC services and regulatory advisory, capturing contracts with telecom operators, energy utilities, and public enterprises[3]Orange Cyberdefense, “Orange Cyberdefense and Palo Alto Networks Strengthen MDR Partnership,” orangecyberdefense.com . Rising Moroccan startup Defendis emphasizes AI-driven anomaly detection tailored for Arabic interfaces, reflecting a trend toward home-grown intellectual property.

Strategic alliances shape competitive outcomes: Orange Cyberdefense and Palo Alto Networks jointly integrated Cortex XSIAM to trim mean-time-to-contain figures by 80% for local banks; IBM and Thales co-deliver quantum-safe encryption proof-of-concepts to public agencies; and Oracle collaborates with the National Ports Authority on secure data-lake architecture designed for maritime logistics analytics[2].Thales Group, “Thales Opens Cybersecurity Operations Center in Morocco,” thalesgroup.com

Morocco Cybersecurity Industry Leaders

DATAPROTECT

Orange Cyberdefense

IBM Corporation

Atos SE (Morocco)

Trend Micro Incorporated.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: An Algerian threat actor exploited a zero-day in legacy middleware to breach the National Social Security Fund, exposing data of nearly 2 million citizens and prompting a government-wide review of identity-encryption controls.

- April 2025: CNSS awarded DATAPROTECT and Modcod a combined MAD 4.8 million for security auditing and intrusion-prevention projects ahead of broader SOC modernization.

- February 2025: Orange Cyberdefense deepened its partnership with Palo Alto Networks, embedding Cortex XSIAM in its Casablanca SOC to shorten detection-to-response intervals.

- May 2024: Oracle inaugurated two Moroccan public-cloud regions offering in-country data residency, accelerating public-sector adoption of secure IaaS and PaaS services.

Morocco Cybersecurity Market Report Scope

The Moroccan cybersecurity market is defined based on the revenues generated from the solutions and services used in various end-user industries worldwide. The analysis is based on the market insights captured through secondary research and primaries. The market also covers the major factors impacting its growth in terms of drivers and restraints.

The Morocco cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Solutions | |

| Services | Professional Services |

| Managed Services |

| On-Premise |

| Cloud |

| SMEs |

| Large Enterprises |

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail |

| Energy and Utilities |

| Manufacturing |

| Others |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Solutions | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By Organization Size | SMEs | |

| Large Enterprises | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

Key Questions Answered in the Report

What is the current value of the Morocco cybersecurity market?

The Morocco cybersecurity market size is USD 157.11 million in 2026.

The Morocco cybersecurity market size is USD 157.11 million in 2026.

The market is projected to register a 8.67% CAGR and reach USD 238.12 million by 2031.

Which segment is expanding the quickest?

Managed security services are forecast to post the highest CAGR at 15.23% through 2031.

Why is healthcare emerging as a high-growth vertical?

Electronic medical record roll-outs, telemedicine adoption, and stricter patient-data rules are driving a 16.74% CAGR for healthcare cybersecurity spending.

Page last updated on: