Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Base Year Market Size (2025) | USD 18.37 Billion |

| Market Size (2026) | USD 20.33 Billion |

| Market Size (2031) | USD 33.74 Billion |

| Growth Rate (2025 - 2030) | 10.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Cybersecurity Market Analysis by Mordor Intelligence

The South America cybersecurity market size was valued at USD 18.37 billion in 2025 and estimated to grow from USD 20.33 billion in 2026 to reach USD 33.74 billion by 2031, at a CAGR of 10.66% during the forecast period (2026-2031). A surge in ransomware-as-a-service kits, wider zero-trust adoption across regulated industries, and cloud migration by small and medium enterprises (SMEs) are pushing spending beyond basic firewalls toward integrated detection and response platforms. Brazil’s Resolution 538 has turned continuous monitoring from a best practice into a licensing condition for banks, causing a run on managed security operations center (SOC) capacity. Currency volatility, especially in Argentina, is steering buyers toward subscription pricing denominated in USD, while hyperscaler investments in São Paulo and Santiago reduce latency concerns for regulated workloads. As industrial firms expose operational technology (OT) networks for remote maintenance, demand is rising for protocol-aware threat analytics that traditional IT tools cannot deliver.

Key Report Takeaways

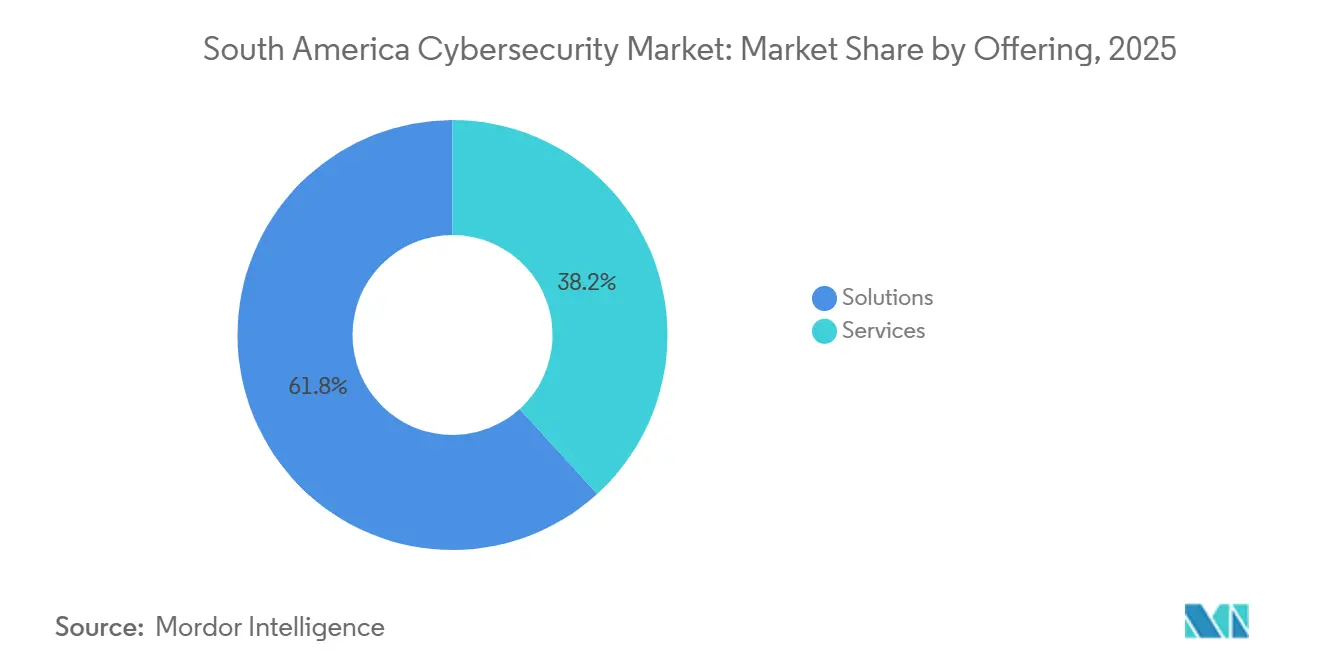

- Solutions led with 61.76% of South America cybersecurity market share in 2025; services are projected to expand at an 11.18% CAGR through 2031.

- On-premises deployments accounted for 53.43% of the South America cybersecurity market size in 2025, while cloud delivery is forecast to advance at an 11.24% CAGR between 2026-2031.

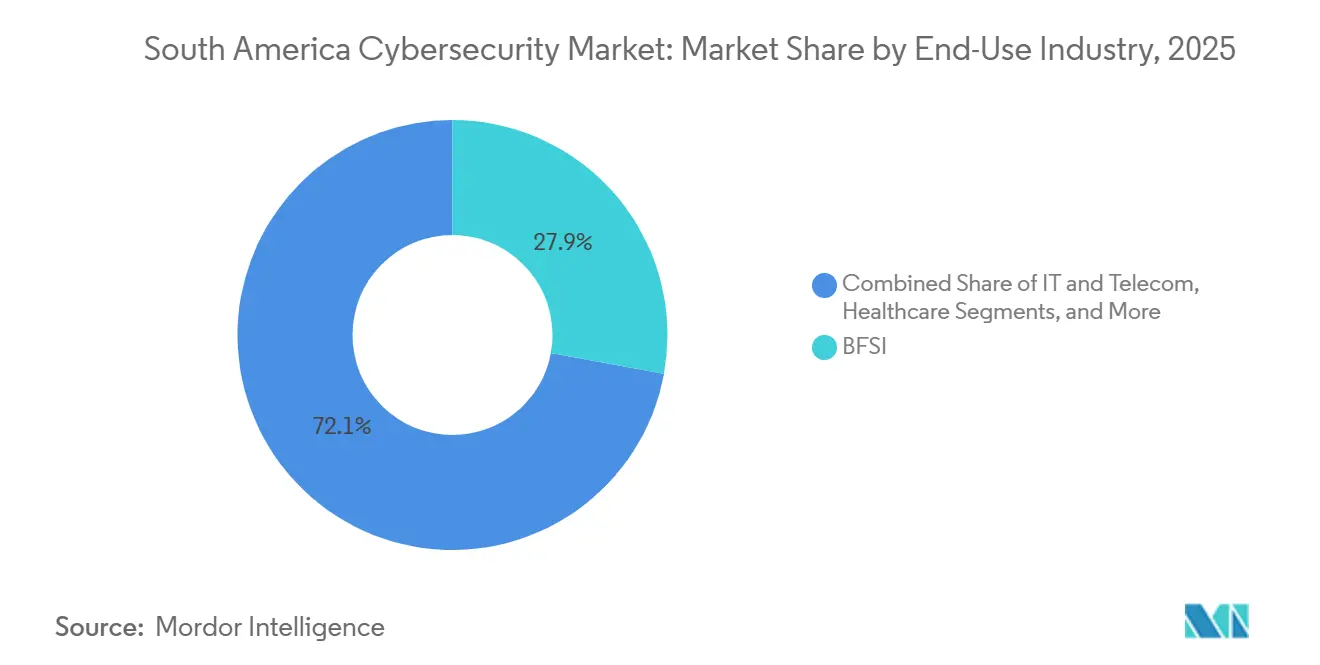

- The banking, financial services, and insurance segment commanded 27.88% revenue share in 2025, whereas healthcare is poised to post the fastest 12.23% CAGR up to 2031.

- Large enterprises held 58.61% share of 2025 spending, yet SMEs are tracking a 10.93% CAGR during 2026-2031 as cloud subscriptions lower entry barriers.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Ransomware-as-a-Service Ecosystem | +2.1% | Brazil, Argentina, Chile; spillover to Colombia and Peru | Short term (≤ 2 years) |

| Proliferation of Zero-Trust Adoption by Regulated Industries | +1.8% | Brazil (BFSI, healthcare), Chile (mining, utilities) | Medium term (2-4 years) |

| Accelerating Cloud Migration Among South American SMEs | +1.6% | Regional, with concentration in Brazil, Chile, Colombia | Medium term (2-4 years) |

| Government Cybersecurity Capacity-Building Programs in Brazil and Chile | +1.3% | National programs in Brazil and Chile; regional coordination through OAS/CICTE | Long term (≥ 4 years) |

| Telco-Led Security APIs Boosting Mobile Identity Protection | +1.1% | Brazil, Argentina, Chile; mobile-first markets | Medium term (2-4 years) |

| Industrial OT Security Demand from Converging IT-OT Networks | +1.4% | Brazil (manufacturing, energy), Chile (mining), Argentina (agriculture) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Ransomware-as-a-Service Ecosystem

Affiliate programs selling ready-made encryption payloads have cut the skill threshold for attackers, shifting South America cybersecurity market spending toward endpoint detection, immutable backup, and incident response retainers. Dragos logged 147 ransomware incidents against regional industrial control systems during the first three quarters of 2025, a 34% year-over-year increase, with Brazil accounting for 62% of cases. Healthcare institutions running Windows Server 2012 were hit hardest, forcing provincial governments to authorize cryptocurrency payments despite budget constraints. Double-extortion tactics stealing data before encryption nudged enterprises to elevate data loss prevention and forensics. Boards now request tabletop exercises that assume perimeter compromise, prompting uptake of managed detection and response services with one-hour containment service-level agreements. As payouts inflate, insurers tighten underwriting, raising premiums and amplifying return-on-investment narratives for proactive security tooling.

Proliferation of Zero-Trust Adoption by Regulated Industries

Zero-trust frameworks moved from concept to compliance obligation once Brazil’s Resolution 538 mandated continuous authentication and micro-segmentation for banks in December 2025.[1]Central Bank of Brazil, “Resolution 538: Cybersecurity Requirements for Financial Institutions,” BCB.GOV.BR Chile’s copper producers replicated the approach after ransomware halted supervisory control and data acquisition systems, costing millions in lost output. Identity platforms that score device posture and geolocation before granting access are replacing static credential checks. Implementation starts with asset inventory and ends with east-west traffic monitoring, a path that most firms outsource to managed security providers due to scarce in-house architects. Vendors offering policy templates mapped to Brazil’s LGPD and Chile’s Framework Law shorten audits and encourage cross-sell into cloud workload protection.

Accelerating Cloud Migration Among South American SMEs

Eighty-three percent of organizations now run hybrid or multi-cloud estates, yet almost half still lack uniform security baselines, leaving misconfigured storage buckets open to credential-stuffing bots. Consumption pricing denominated in USD lets firms in hyper-inflationary markets such as Argentina smooth spending when local currencies plunge. Cloud access security brokers, workload protection, and posture management tools integrate natively with hyperscaler APIs, automating ISO 27001 and LGPD checks. Telcos bundle secure access service edge (SASE) with connectivity, relieving SMEs of VPN appliance upkeep. As remote work normalizes, single-sign-on and zero-trust network access replace perimeter firewalls, shifting addressable spend from capital expenditure to operating expenditure.

Government Cybersecurity Capacity-Building Programs in Brazil and Chile

Brazil’s draft Bill 4752/2025 would establish a National Cybersecurity Authority empowered to set baseline controls for critical infrastructure and accredit training to close an estimated 750,000-person talent gap.[2]Government of Brazil, “Bill 4752/2025: National Cybersecurity Authority,” GOV.BR Chile’s Framework Law, effective March 2024, already requires 24-hour incident reporting for utilities and telecom operators. Regional tabletop exercises run by the Organization of American States in 2025 exposed gaps in cross-border evidence sharing, prompting model legal templates. Japan funded OT-security scholarships for 500 Chilean public servants, transferring protocol-specific expertise. Such initiatives stoke demand for governance, risk, and compliance (GRC) platforms that align controls with multiple statutes, as well as multilingual security-awareness content targeting frontline staff.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Data-Protection Regulations Across Countries | -0.9% | Regional, affecting multinational operations across Brazil, Argentina, Chile, Colombia, Peru | Medium term (2-4 years) |

| Acute Cybersecurity Skills Shortage in Spanish- and Portuguese-Speaking Talent Pools | -1.2% | Regional, most severe in Brazil, Argentina, Chile | Long term (≥ 4 years) |

| Economic Volatility Limiting Cap-Ex Budgets for SMEs | -1.1% | Argentina, Brazil; secondary impact in Chile, Colombia | Short term (≤ 2 years) |

| High Cost of Advanced Threat-Detection Platforms | -0.8% | Regional, particularly affecting SMEs and public-sector entities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Data-Protection Regulations Across Countries

Brazil’s LGPD obliges 72-hour breach disclosure and data-protection officers, Chile’s new law mirrors European notice periods, yet Peru still allows 10 business days. Multinationals juggle divergent consent rules and cross-border transfer bans, forcing data-residency workarounds that drain budgets earmarked for threat hunting. Without a South American equivalent of the EU’s adequacy regime, firms deploy country-specific encryption gateways, multiplying tooling and audit costs. The patchwork also deters regional SOC centralization because alerts containing personal data cannot always cross borders for correlation. This inefficiency disadvantages local vendors that cannot amortize compliance engineering over wider markets.

Acute Cybersecurity Skills Shortage in Spanish and Portuguese Talent Pools

ISG pegged the regional shortfall at 750,000 practitioners in 2024, a gap widened by North American firms recruiting remotely at dollar-denominated salaries. Universities offer limited hands-on labs, and industrial control system curricula are almost absent. Organizations backfill with managed security services, yet language mismatches hamper threat-triage accuracy when offshore analysts misclassify culturally nuanced phishing lures. Governments mandate training, Chile now certifies critical-infrastructure practitioners, but pipelines will take years to mature. Meanwhile, vendors embedding automation and low-code playbooks gain favor because they stretch thin analyst benches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Capture Growth Momentum

Services expanded at an 11.18% CAGR from 2026-2031, eclipsing the broader South America cybersecurity market rate as banks, hospitals, and miners outsourced 24/7 monitoring to offset staffing gaps. Although solutions controlled a 61.76% slice of South America cybersecurity market share in 2025, buyers realized that appliances are inert without expertise to tune alerts and run threat hunts. Regulatory triggers like Resolution 538 forced mid-tier banks to prove real-time incident response, making managed detection and response contracts a faster path to compliance than building internal SOCs. Cloud security and identity suites led solution spending thanks to hybrid architectures, while commodity network firewalls ceded ground to multifunction platforms.

Professional services assessment, integration, migration remain essential when enterprises pivot to zero trust. Demand rises for consultants who map LGPD, Chile’s Framework Law, and sector mandates into unified control matrices. Managed services now bundle GRC dashboards, threat intel feeds, and automated containment, delivering enterprise-grade outcomes to SMEs on a per-user basis. Integrators with Portuguese and Spanish SOC analysts, such as Tempest Security Intelligence, differentiate against global players that primarily staff English-only centers.

By Deployment Mode: Cloud Narrows the Gap

Cloud deployments are tracking an 11.24% CAGR through 2031, steadily shrinking the on-premises majority that stood at 53.43% in 2025. The tipping point came as hyperscalers opened São Paulo and Santiago zones, satisfying data residency clauses and slicing latency for real-time payments. Consumption pricing resonates in inflationary economies because monthly invoices preserve cash flow and hedge currency swings. South America cybersecurity market size for cloud tools grows as SMEs procure web-native firewalls, workload protection, and secure access edge components without capital outlays.

On-premises estates persist in core banking, health records, and defense environments where sovereignty and legacy system interdependence demand physical control. Yet even here, unified consoles like Microsoft Defender for Cloud enforce common policies across physical and virtual machines. Telcos now position SASE gateways inside their metropolitan networks, offering elastic bandwidth married with inline threat inspection. As shadow IT declines, the locus of policy enforcement moves from branch routers to identity-centric overlays.

By End-Use Industry: Healthcare Sets the Pace

The banking sector retained the biggest slice of South America cybersecurity market size at 27.88% in 2025, but healthcare is outstripping every vertical with a 12.23% CAGR. Ransomware that froze patient admissions in São Paulo and Buenos Aires validated ministerial studies forecasting USD 1 million-plus recovery bills per incident. Hospitals scramble for immutable backup, least-privilege identity, and network micro-segmentation because many still run unsupported operating systems. Financial institutions, obligated to secure Pix instant payments that hit 42 billion transactions in 2024, invest in behavioral analytics and real-time fraud scoring.[3] Central Bank of Brazil, “Resolution 538,” BCB.GOV.BR

Mining, energy, and utilities allocate fresh capital to OT security as converged IT-OT networks expose programmable logic controllers to Internet scouting. Retailers blend payment card compliance with bot mitigation to curb credential-stuffing. Telecom operators harden core networks against signaling exploits that can pivot into subscriber data. Across segments, demand coalesces around integrated platforms that collapse endpoint, identity, and cloud visibility into one analytics fabric.

By End-User Enterprise Size: SME Adoption Rises

Large enterprises still accounted for 58.61% of 2025 outlays, reflecting complex estates and mandatory audits, yet SMEs embody the fastest climb with a 10.93% CAGR. The shift mirrors South America cybersecurity market dynamics where cloud subscriptions circumvent capital scarcity. Argentine retailers, squeezed by 200% inflation in 2024, gravitated to monthly USD-denominated plans for email and endpoint defense. Off-the-shelf SASE bundles from telcos let ten-employee firms gain zero-trust network access without owning any hardware.

Enterprises with security staff buy best-of-breed and integrate via security orchestration, automation, and response (SOAR) layers. SMEs prefer converged agents that cover endpoint, DNS, and file sandboxing. Regional managed service providers target this cohort with tiered packages that guarantee breach notification compliance and deliver CISO-level reports for board meetings. As compliance deadlines compress, SMEs become the incremental dollar driving double-digit growth.

Geography Analysis

Brazil dominates South America cybersecurity market spending with the weight of its economy, a proactive Central Bank, and hyperscaler capital inflows. Resolution 538 compels banks to log and alert within 24 hours, fueling purchases of security information and event management (SIEM) suites and managed SOC contracts. Pix’s mass adoption intensifies investment in real-time fraud analytics as credential-stuffing syndicates probe account recovery flows. The proposed National Cybersecurity Authority would further standardize baseline controls, paving the way for federal procurement frameworks that favor platform consolidators. Microsoft’s USD 1.3 billion São Paulo and Rio builds lock in cloud workload residency for financial and healthcare customers.

Chile records the highest growth trajectory as its mining-dependent economy secures remote OT sites and as the government implements its 2024 Framework Law requiring 24-hour incident disclosure. Accession to the Counter Ransomware Initiative grants Chile privileged threat feeds, sharpening SOC analytics. Japanese technical assistance is seeding a new cadre of OT-security engineers able to audit copper smelters and desalination plants. Telcos leverage fiber upgrades to upsell SASE, and cloud regions near Santiago help SaaS providers sidestep cross-border data transfer friction.

Argentina, Colombia, and Peru trail in absolute dollars but present leapfrog potential. Argentina’s inflationary spiral forces CFOs to pivot from upfront licenses toward usage-based cloud security, a dynamic that benefits vendors offering peso billing hedged in USD. Colombia’s strict cross-border data approval slows hyperscaler adoption, yet domestic SIEM vendors win government tenders by hosting logs onshore. Peru drives growth through e-commerce expansion but lacks mandatory breach disclosure, delaying proactive investment. Organization of American States tabletop drills exposed legislative bottlenecks to extradition and digital evidence exchange, encouraging convergence but not yet rewriting risk appetites.[4]Organization of American States, “Regional Cybersecurity Exercises,” OAS.ORG

Competitive Landscape

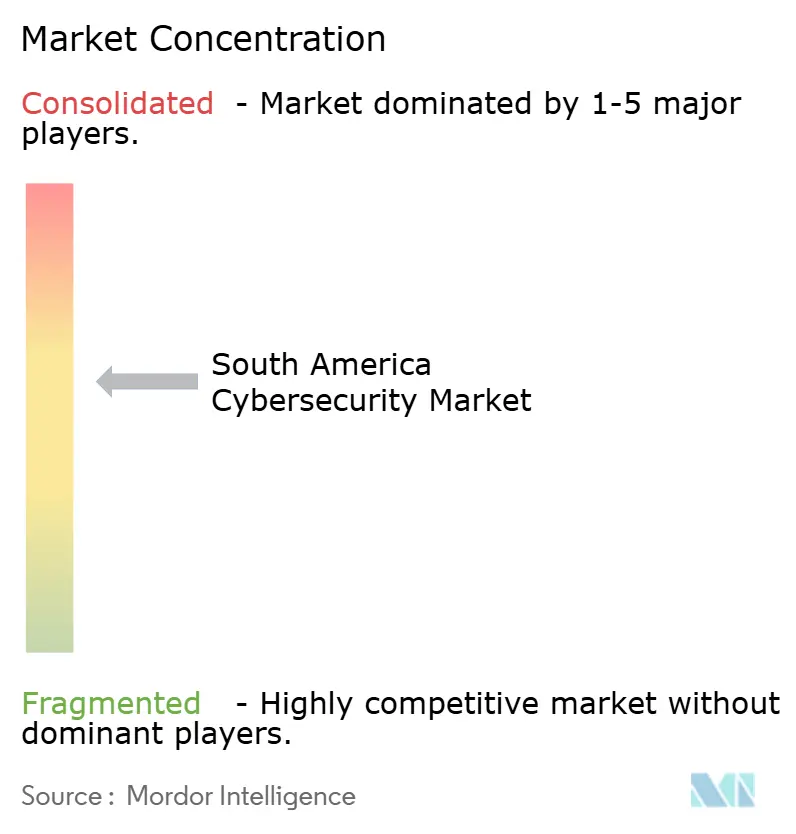

The South America cybersecurity market shows moderate concentration. Microsoft, Palo Alto Networks, Fortinet, and IBM anchor the top tier, leveraging distributor ecosystems and Portuguese-Spanish support desks. Microsoft bundles Azure Sentinel, Defender, and Entra ID into enterprise agreements, making stand-alone replacements costly once data pipelines are entrenched. Palo Alto Networks’ Prisma Cloud and Cortex XDR resonate with hybrid estates, while Fortinet exploits channel reach and appliance price-performance to capture SMEs.

Regional specialists fill gaps: Tempest Security Intelligence and Modulo Security Solutions pair LGPD know-how with managed SOCs staffed by locally certified analysts. Stefanini IT Solutions taps its BPO heritage to deliver incident response retainers in Portuguese and Spanish, sidestepping language barriers that offshore centers face. Telcos Telefónica and Claro monetize network visibility by embedding DNS filtering and zero-trust network access into connectivity contracts. CrowdStrike and Zscaler, courting cloud-native unicorns, opened São Paulo hubs to shorten sales cycles and meet residency requirements, illustrating how niche plays can scale quickly.

Industrial control system security remains less contested. Dragos and Claroty dominate pilot projects in petrochemical and mining sites because legacy IT vendors lack deep protocol expertise. As OT ransomware headlines grow, hardware-agnostic anomaly detection engines have gained board-level sponsorship. Governance, risk, and compliance platforms such as Archer and ServiceNow fight for share as multi-jurisdiction data-protection rules drive audit automation demand. Given that the top five vendors jointly control roughly 55% of regional billings, competition remains open for challengers that localize quickly and partner aggressively.

South America Cybersecurity Industry Leaders

IBM Corporation

Microsoft Corporation

Palo Alto Networks Inc.

Fortinet Inc.

Check Point Software Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Resecurity, a U.S.-based global leader in cybersecurity and threat intelligence, is expanding its operations in Brazil, as Brazilian enterprises, government institutions, and infrastructure providers strive to comply with Lei Geral de Proteção de Dados (LGPD) requirements.

- April 2025: Stellar Cyber, a leader in cybersecurity solutions, has appointed Silvio Eberardo as its first-ever Country Manager for Brazil. This move underscores the company's swift expansion and dedication to the Brazilian market.

- November 2024: Kaspersky’s Security Bulletin forecast more resilient ransomware strains and an uptick in database-poisoning attacks for 2025, with mobile threats in Colombia rising 72% year-on-year.

- September 2024: Brazil enacted Lei 14.967, imposing stricter cybersecurity obligations on private security firms and creating fresh compliance demand.

South America Cybersecurity Market Report Scope

The Cybersecurity Market encompasses global spending on solutions, software, and services designed to protect digital infrastructure, data, and operations across all industries, including cloud, network, endpoint, and application security; it includes enterprise, government, and SME segments but excludes physical security and pure consulting-only services, with the market evolving rapidly toward AI-driven automation, platform consolidation, and regulatory-driven transformation.

The South America Cybersecurity Market Report is Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-User Vertical

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Other End-User Verticals |

By Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By Country

| Brazil |

| Argentina |

| Peru |

| Chile |

| Colombia |

| Ecuador |

| Venezuela |

| Rest of South America |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Other End-User Verticals | ||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Country | Brazil | |

| Argentina | ||

| Peru | ||

| Chile | ||

| Colombia | ||

| Ecuador | ||

| Venezuela | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the South America cybersecurity market today?

It stood at USD 20.33 billion in 2026 and is on track to hit USD 33.74 billion by 2031, supported by a 10.66% CAGR.

Which customer segment is growing fastest?

SMEs are registering a 10.93% CAGR because cloud subscriptions eliminate upfront capital outlays.

Why is healthcare outpacing other verticals?

Electronic health record digitization and frequent ransomware attacks push hospitals to upgrade defenses, driving a 12.23% CAGR.

What is the primary regulatory catalyst in Brazil?

Central Bank Resolution 538, effective Dec 2025, obliges banks to maintain continuous monitoring and rapid incident reporting.

How are currency swings influencing buying decisions?

Inflation and depreciation, particularly in Argentina, lead firms to favor USD-denominated pay-as-you-go cloud security instead of multi-year hardware licenses.

Which technologies will attract the most spending through 2031?

Cloud workload protection, identity and access management, and managed detection and response services are poised for double-digit growth as hybrid environments expand.

Page last updated on: