Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

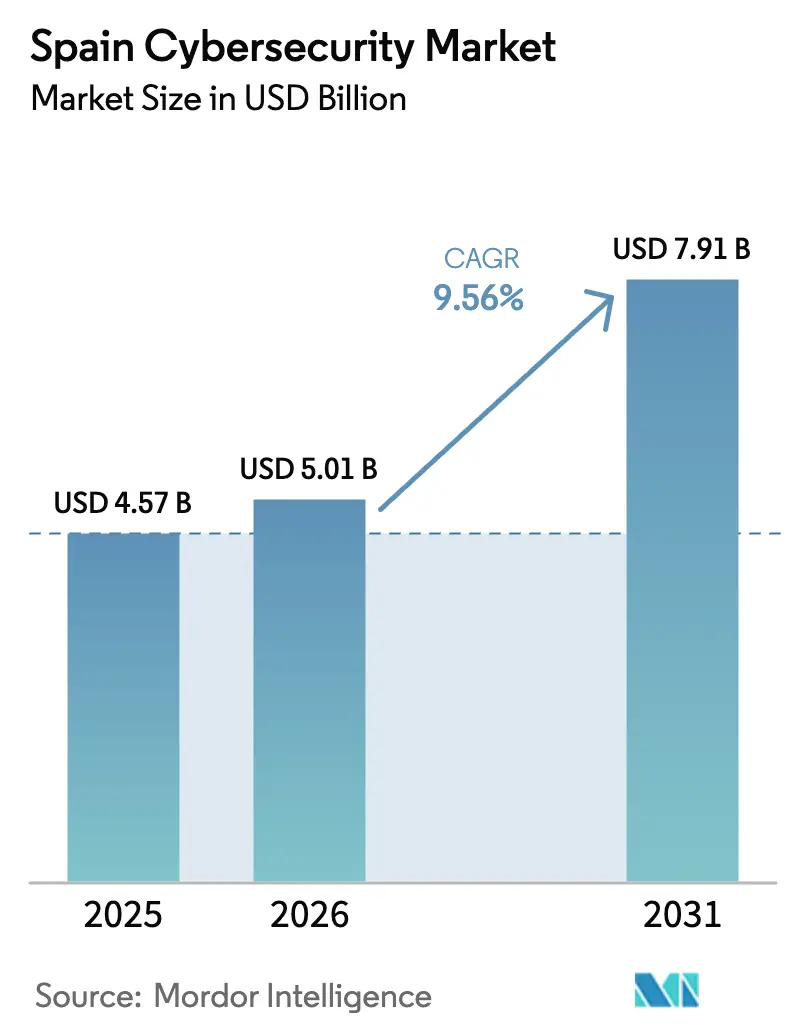

| Base Year Market Size (2025) | USD 4.57 Billion |

| Market Size (2026) | USD 5.01 Billion |

| Market Size (2031) | USD 7.91 Billion |

| Growth Rate (2026 - 2031) | 9.56% CAGR |

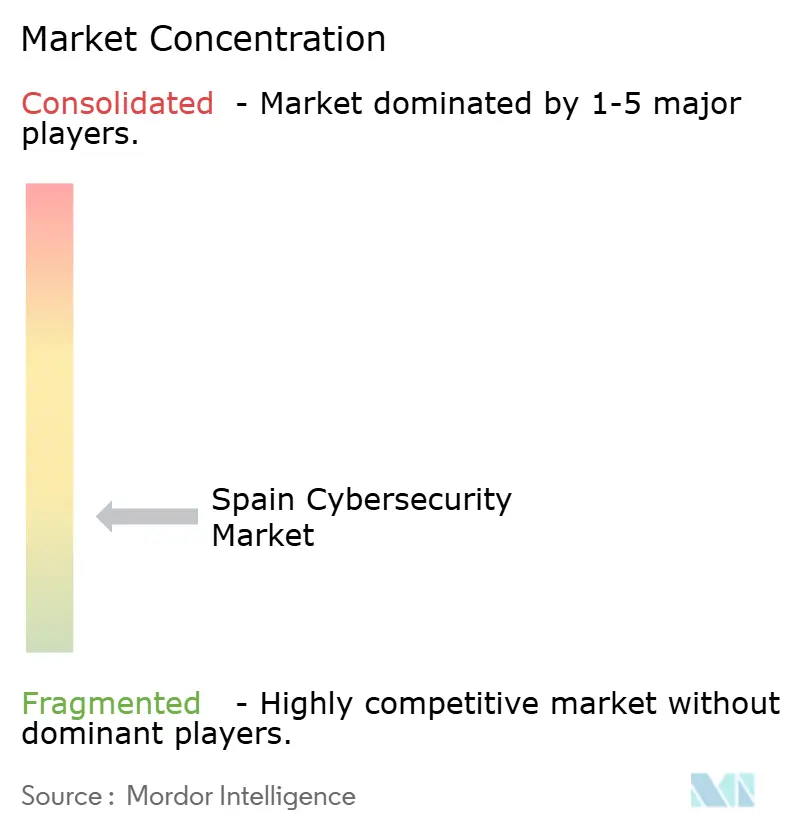

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Cybersecurity Market Analysis by Mordor Intelligence

The Spain cybersecurity market size was valued at USD 4.57 billion in 2025 and estimated to grow from USD 5.01 billion in 2026 to reach USD 7.91 billion by 2031, at a CAGR of 9.56% during the forecast period (2026-2031). Heightened regulatory pressure, accelerated cloud migration across all 17 autonomous communities, and an upsurge in sophisticated ransomware campaigns are simultaneously inflating security budgets and reshaping purchasing criteria. Spending momentum is reinforced by the EUR 1.157 billion (USD 1.24 billion) sovereign-resilience package approved in 2025, which earmarks fresh funds for regional security operations centers and workforce training. The operating environment also reflects Spain’s new National Cybersecurity Law, which extends 24-hour incident-reporting and third-party due-diligence duties to more than 10,000 entities, prompting boards to ring-fence security outlays as a stand-alone budget line. On the supply side, vendors are pivoting from perpetual-license appliances toward outcome-based managed detection and response (MDR) contracts, enabling enterprises of all sizes to externalize operations yet still meet stringent audit requirements.

Key Report Takeaways

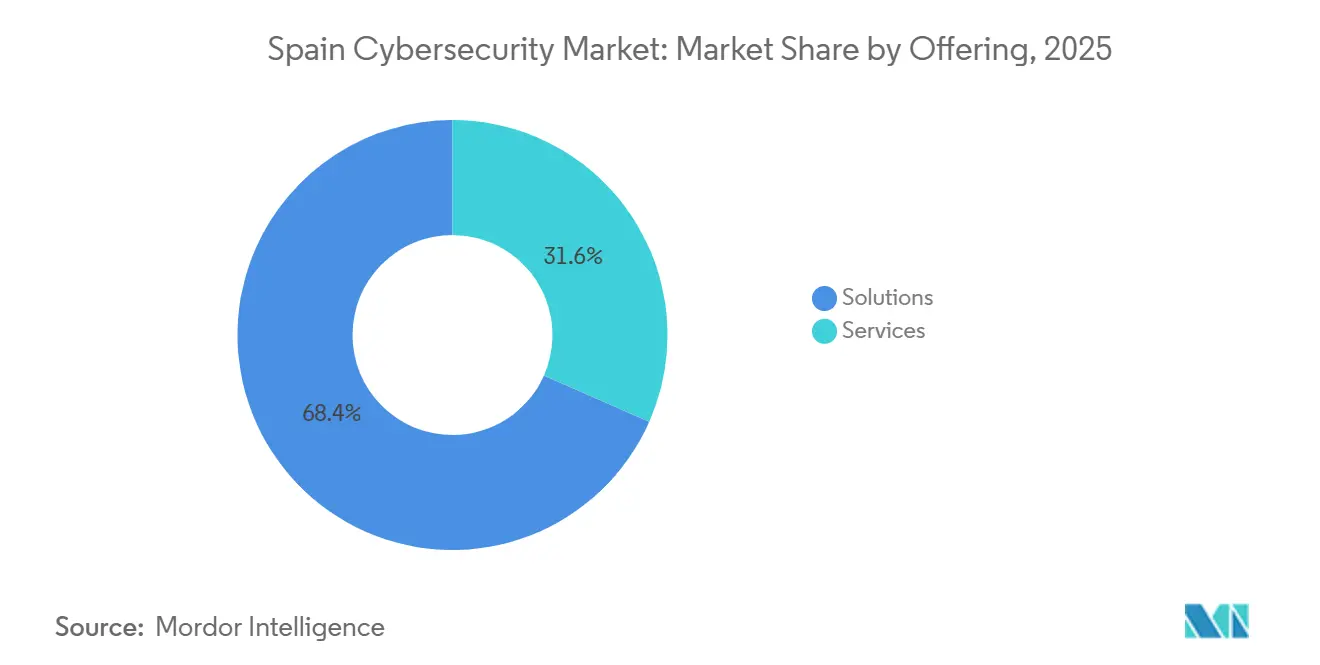

- By offering, solutions led with 68.38% revenue share in 2025, while services are projected to expand at a 10.23% CAGR through 2031.

- By deployment mode, cloud accounted for 64.37% of the Spain cybersecurity market share in 2025 and is forecast to grow at a 10.84% CAGR to 2031.

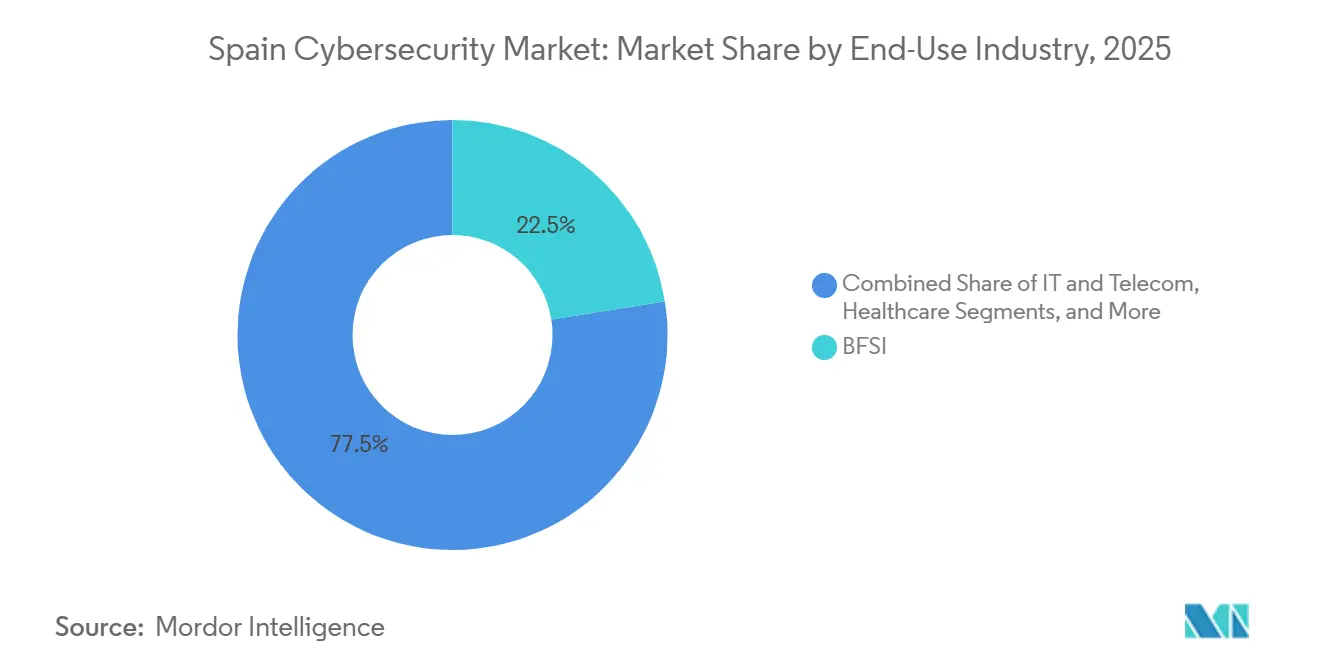

- By end-use industry, BFSI held 22.51% share of the Spain cybersecurity market size in 2025, whereas healthcare is advancing at an 11.16% CAGR through 2031.

- By enterprise size, large enterprises commanded 61.73% of 2025 spending, but small and medium enterprises are expanding at a 10.92% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Digitalization Across Spanish SMEs | +2.1% | National, with concentration in Madrid, Catalonia, Valencia | Medium term (2-4 years) |

| Stringent National Cybersecurity Law 43-2022 Enforcement | +1.8% | National, affecting all 17 autonomous communities | Short term (≤ 2 years) |

| Surge in Cloud Migration by Public Administration Bodies | +1.5% | National, led by central government and regional administrations | Medium term (2-4 years) |

| Growing Adoption of Zero-Trust Architectures | +1.3% | National, early adoption in BFSI and IT/Telecom sectors | Long term (≥ 4 years) |

| Rising Cyber Insurance Uptake Re-shaping Security Budgets | +1.2% | National, with higher penetration in Madrid and Barcelona | Medium term (2-4 years) |

| Expansion of 5G Networks Driving Edge Security Demand | +1.7% | National, with early gains in industrial hubs of Basque Country, Catalonia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digitalization Across Spanish SMEs

Spain’s 3.4 million small firms boosted basic digital-intensity penetration to 68% by Q1 2025, up seven points in two years. The Kit Digital voucher scheme subsidized endpoint protection, secure cloud storage, and multifactor authentication for 420,000 recipients, compressing the SME-to-large-enterprise maturity gap from two years to nine months. Voucher support reduced out-of-pocket endpoint detection and response costs by 60%, unleashing demand for managed MDR bundles that deliver 24/7 coverage without additional FTEs. Rapid telemetry growth is outstripping legacy SIEM capacity, steering purchasing toward AI-driven extended detection and response platforms that can ingest 10 terabytes of logs per day without manual tuning.[1]Cisco Systems, “Cybersecurity Readiness Index 2025,” cisco.com

Stringent National Cybersecurity Law 43-2022 Enforcement

Parliament’s January 2025 adoption of NIS2 obligations enlarged the regulated population to more than 10,000 organizations across 18 sectors.[2]European Commission, “NIS2 Directive Transposition – Spain,” digital-strategy.ec.europa.eu Essential entities must file incident notices within 24 hours and undergo annual third-party audits, with non-compliance fines reaching EUR 10 million (USD 10.73 million). The statute pushes security from an IT expense to a board-level risk-control category, triggering sustained budget allocations for tabletop exercises, forensic retainers, and supply-chain due-diligence tooling. Early audits found 38% of newly covered operators lacked formal response plans, spurring immediate consulting demand.

Expansion of 5G Networks Driving Edge Security Demand

Standalone 5G now covers 96% of urban zones and 80% of rural zones, enabling ultra-low-latency industrial use-cases in automotive, logistics, and remote healthcare. A EUR 3.26 billion (USD 3.50 billion) telecom and cybersecurity plan funds a national 5G security operations center tasked with monitoring network slices and detecting anomalous signaling traffic. Manufacturers deploying private 5G lines need lightweight intrusion-detection software that can run machine-learning inference on ARM-based gateways without adding latency. Demand is also rising for zero-touch provisioning tools that secure thousands of edge devices scattered across smart-factory floors.

Surge in Cloud Migration by Public Administration Bodies

Madrid’s pledge to fold 43 ministerial data centers into a sovereign cloud by 2027 unlocked an initial EUR 800 million (USD 858 million) budget in 2025. Regional governments in Catalonia, Andalusia, and the Basque Country are spinning up parallel platforms, each requiring cloud security posture management that can enforce uniform policies over hybrid footprints. Because 62% of public-sector entities still run pre-2018 on-premises Active Directory services, they also need federation bridges that extend single sign-on while applying device-posture checks.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified Cybersecurity Professionals | -1.4% | National, acute in regions outside Madrid and Barcelona | Long term (≥ 4 years) |

| Budget Constraints Among Micro-Enterprises | -0.9% | National, concentrated in rural areas and hospitality sector | Short term (≤ 2 years) |

| Fragmented Procurement Across 17 Autonomous Communities | -0.7% | National, affecting multi-region vendors | Medium term (2-4 years) |

| High Dependence on Imported Security Appliances | -0.6% | National, with supply-chain exposure to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Cybersecurity Professionals

ICT specialists made up only 4.4% of Spain’s workforce in 2024, below the EU average of 4.8%.[3]Eurostat, “ICT Specialists in Employment – Spain,” ec.europa.eu/eurostat Median time-to-hire for CISSP-level roles exceeded six months, and 68% of credentialed staff cluster in Madrid and Barcelona, leaving Galicia, Extremadura, and other regions underserved. Universities graduated roughly 8,000 ICT students in 2024, but barely 15% majored in security. To narrow the gap, Indra Sistemas and the Catalan government launched a program to train 2,000 analysts by 2028. Until supply balances, many mid-market firms will rely on managed service providers for fractional SOC staffing.

Budget Constraints Among Micro-Enterprises

Micro-entities representing 95% of Spain’s business population budgeted a median EUR 2,400 (USD 2,575) for security in 2024. The Kit Digital grant softened costs but closed in December 2024, leaving a funding gap unlikely to be filled before 2027. Reliance on free community tools creates a false sense of safety; Orange Cyberdefense recorded a 53% higher phishing-success rate among freemium users versus commercial platform adopters. Price sensitivity channels these firms toward basic controls, sustaining systemic risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Overtake Ownership Models

Services are forecast to expand at a 10.23% CAGR between 2026 and 2031, overtaking traditional appliances even though solutions captured 68.38% of 2025 revenues. Enterprises prefer outcome-based MDR subscriptions that shift operational risk onto providers; Telefónica Tech’s NextDefense bundle slashed customers’ mean time to response by 98% while avoiding new headcount. Financial audits mandated by the new law are also lifting demand for incident-response retainers and compliance consulting. The Spain cybersecurity market size for professional services is therefore scaling faster than capital purchases, though network and endpoint boxes still ship in compliance-sensitive ATMs and industrial control systems, preserving a sizeable solutions base.

Integrated risk-management dashboards, identity governance suites, and cloud workload protection platforms underpin the slower yet still solid 9.3% CAGR in solutions. Appliance margins, however, are compressing as hyperscalers bake firewall and anti-malware into infrastructure-as-a-service plans that attackers cannot bypass without triggering cloud-native alerts. Vendors answering this commoditization are embedding AI analytics and EU Common Criteria certifications to defend price points, an approach already seen in GMV’s EUCC-validated CyberSOC appliance.

By Deployment Mode: Cloud Expansion Under Sovereignty Rules

Cloud captured 64.37% of 2025 spending and is on track for a 10.84% CAGR through 2031. The Spain cybersecurity market share attached to sovereign-cloud projects is set to swell as ministries migrate 43 data centers into a Federated Cloud that keeps encryption keys on Spanish soil, satisfying data-residency mandates. Enterprise uptake follows a parallel course: 58% of firms already operate on two or more cloud platforms, increasing the Spain cybersecurity market size tied to multi-cloud policy orchestration tools. Identity-and-access bridges, container runtime defense, and confidential-computing services are particularly in demand among regional governments striving for NIS2 compliance.

On-premises estates remain vital for latency-critical banking cores and private 5G robotics, where cloud round-trips are unacceptable and regulators require offline fail-over. Hybrid designs oblige secure interconnects that apply uniform policies across both realms. Financial entities now stage disaster-recovery drills isolating hyperscaler dependencies, reinforcing residual on-premises appliance sales.

By End-Use Industry: Healthcare Rises, BFSI Holds Scale

Healthcare outpaces all sectors with an 11.16% CAGR as EUR 1.69 billion (USD 1.81 billion) in Digital Health Spain grants digitize 100% of primary-care centers. Interoperable electronic health records and telemedicine sessions now 40% of consultations draw previously isolated medical devices onto open networks. Hospitals therefore adopt asset-discovery and network-segmentation software that inventories legacy scanners while meeting GDPR safeguards. ENISA logged a 78% rise in EU hospital breaches during 2024, underlining the commercial urgency.

BFSI still accounts for 22.51% of 2025 revenue due to deep regulatory oversight and sizable IT budgets. The Digital Operational Resilience Act drives quarterly threat-led penetration tests and 24-hour incident reporting, pushing banks toward automated scenario-simulation tools and real-time third-party dashboards. Card-not-present fraud stood at EUR 140.97 million (USD 151.24 million) in 2024, intensifying demand for behavioral biometrics and tokenization solutions.

By Enterprise Size: SMEs Accelerate, Large Enterprises Sustain Volume

Small and medium enterprises are set to grow at a 10.92% CAGR to 2031, trimming their historical maturity gap. Kit Digital lowered the total cost of managed endpoint security to EUR 50-80 (USD 54-86) per device per month, catalyzing adoption even in low-margin hospitality businesses. Despite the funding hiatus, voucher alumni now budget security as an operating expense, creating recurring revenue for regional managed service providers. Still, micro-enterprises overtly rely on subsidized solutions, leaving them over-exposed once support ceases.

Large enterprises retain 61.73% of spending and pursue zero-trust architectures that span data-center, cloud, and edge domains. Cisco’s 2025 survey revealed only 4% had mature implementations, yet 86% reported AI-related incidents.[4]Cisco Systems, “Cybersecurity Readiness Index 2025,” cisco.com Boards thus approve multi-year roadmaps pairing identity-centric controls with extended detection and response analytics, bolstering absolute market value even as relative growth moderates.

Geography Analysis

Madrid and Catalonia jointly represented 52% of 2025 expenditure, owing to the clustering of national ministries, global banks, and hyperscale data-centers. Both regions benefit from submarine cable landings that turn local ISPs into European peering points, amplifying demand for DDoS scrubbing and custom threat-intelligence feeds. The Basque Country and Valencia now emerge as industrial-technology hotspots, where automotive and aerospace factories deploy 5G-linked robotics requiring sub-10 millisecond security gateways. Andalusia, Galicia, and Castilla y León trail, reflecting micro-enterprise dominance in agriculture and tourism and slower procurement cycles.

Fragmented purchasing frameworks across the 17 autonomous communities introduce 6-to-9-month delays in vendor onboarding, elevating compliance costs and discouraging national rollouts. The National Cybersecurity Law aims to standardize audit criteria, yet enforcement remains locally delegated, risking uneven penalty interpretation. Vendors therefore cultivate partnerships with regional managed security providers that can navigate local rules and provide on-site language support.

Spain’s geographic bridge between Europe, Africa, and Latin America confers external-connectivity advantages. New subsea cables into Senegal and Brazil anchor data-centers in Madrid and Barcelona, positioning Spain as Southern Europe’s security hub. The national 5G security operations center, financed in 2025, will also monitor cross-border network slices, fostering public-private sharing of anomaly telemetry with ENISA.

Competitive Landscape

The top five vendors Indra Sistemas, Telefónica Tech, GMV, Orange Cyberdefense, and Palo Alto Networks held major share of 2025 revenues, underlining moderate concentration. Spanish incumbents leverage deep government relationships, while global players like Cisco, Fortinet, and IBM extend platform subscriptions to court regional banks and telecoms.

Market strategy is tilting toward consumption contracts. Telefónica Tech’s NextDefense folds Cortex XSIAM analytics, threat intelligence, and 24/7 expertise into a per-user fee that removes capex hurdles. Indra Sistemas’ IndraMind platform aims for EUR 1 billion (USD 1.07 billion) by 2030, fusing AI and security orchestration to out-automate rivals.

White-space pockets remain in medical-device security, where fewer than 20% of hospitals deploy specialized platforms, and in edge-native intrusion detection for ARM gateways powering private 5G factories. WALLIX’s 2025 buyout of Malizen adds AI-based behavior analytics to meet DORA’s continuous-monitoring stipulations, indicating how niche acquisitions deliver regulatory alignment. GMV’s EUCC certification illustrates the procurement leverage achieved by synchronizing product roadmaps with EU policy.

Spain Cybersecurity Industry Leaders

Indra Sistemas S.A.

Telefónica Cybersecurity and Cloud Tech, S.A. (Telefónica Tech)

GMV Innovating Solutions S.L.

Inetum Espana S.A.

NCC Group Espana S.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Parliament is expected to finalize implementing rules for National Cybersecurity Law 43-2022, clarifying incident thresholds and audit cadence.

- December 2025: Indra Sistemas closed a EUR 725 million (USD 778 million) takeover of Hispasat, adding secure satellite communications to its portfolio.

- November 2025: WALLIX bought Malizen for EUR 1.6 million (USD 1.72 million), integrating AI-driven user analytics into its privileged-access suite.

- October 2025: Indra Sistemas and the Catalan government agreed to train 2,000 cyber-defense professionals by 2028.

Spain Cybersecurity Market Report Scope

The Cybersecurity Market encompasses global spending on solutions, software, and services designed to protect digital infrastructure, data, and operations across all industries, including cloud, network, endpoint, and application security; it includes enterprise, government, and SME segments but excludes physical security and pure consulting-only services, with the market evolving rapidly toward AI-driven automation, platform consolidation, and regulatory-driven transformation.

The Spain Cybersecurity Market Report is Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End Point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premises |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How large is Spain’s cybersecurity spending today and how fast is it growing?

The market stands at USD 5.01 billion in 2026 and is on track to reach USD 7.91 billion by 2031, supported by a 9.56% CAGR.

Which segment is expanding quickest inside Spanish security budgets?

Managed and professional services are accelerating at a 10.23% CAGR as firms shift from appliance ownership to outcome-based MDR contracts.

Why is healthcare now a priority customer group?

EUR 1.69 billion in Digital Health funds is connecting legacy medical devices to networks, raising breach exposure and lifting security procurement at an 11.16% CAGR.

How are new regulations influencing vendor selection?

National Cybersecurity Law 43-2022 mandates 24-hour incident reporting and audited response plans, so buyers favor suppliers offering turnkey compliance tooling.

What skills shortfall is slowing deployment projects?

Only 4.4% of the labor force are ICT specialists and security hiring windows exceed six months, pushing enterprises toward managed service providers.

Who holds the strongest share among local suppliers?

Indra Sistemas, Telefónica Tech, GMV, Orange Cyberdefense, and Palo Alto Networks collectively control 38% of domestic revenue.

Page last updated on: