Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

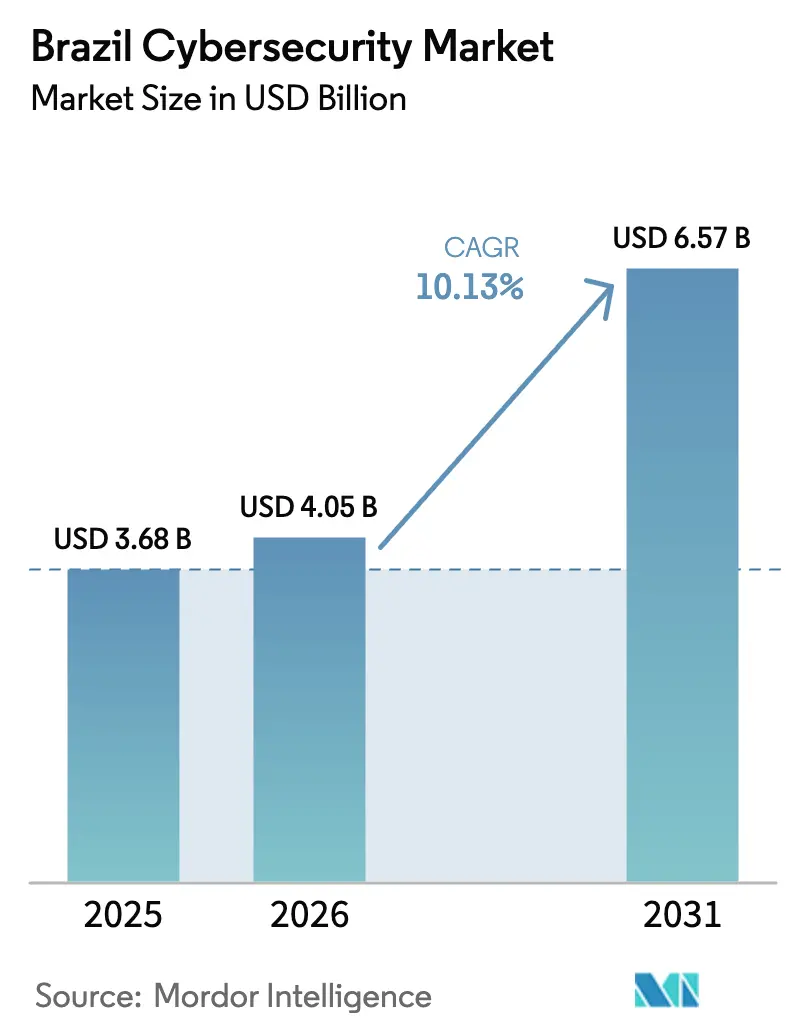

| Base Year Market Size (2025) | USD 3.68 Billion |

| Market Size (2026) | USD 4.05 Billion |

| Market Size (2031) | USD 6.57 Billion |

| Growth Rate (2026 - 2031) | 10.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Cybersecurity Market Analysis by Mordor Intelligence

The Brazil cybersecurity market size is expected to grow from USD 3.68 billion in 2025 to USD 4.05 billion in 2026 and is forecast to reach USD 6.57 billion by 2031 at 10.13% CAGR over 2026-2031. Growth is underpinned by the mass adoption of Pix, rapid public-sector migration to GovCloud, steady 5G roll-outs and heightened LGPD enforcement. As digital payments exceed 3 billion monthly transfers, banks, retailers and utilities allocate larger budgets to threat detection platforms while shifting capital-intensive appliance refreshes to later years. Currency volatility pressures import-oriented hardware purchases, yet spending remains resilient because incident-response costs now dwarf preventive outlays. The acute talent gap is another structural driver: with SOC analysts scarce outside São Paulo, many firms outsource monitoring to managed service providers. A parallel trend sees compliance investment morphing into broader resilience programmes as organisations unify privacy, fraud-prevention and disaster-recovery initiatives under one governance umbrella.

Key Report Takeaways

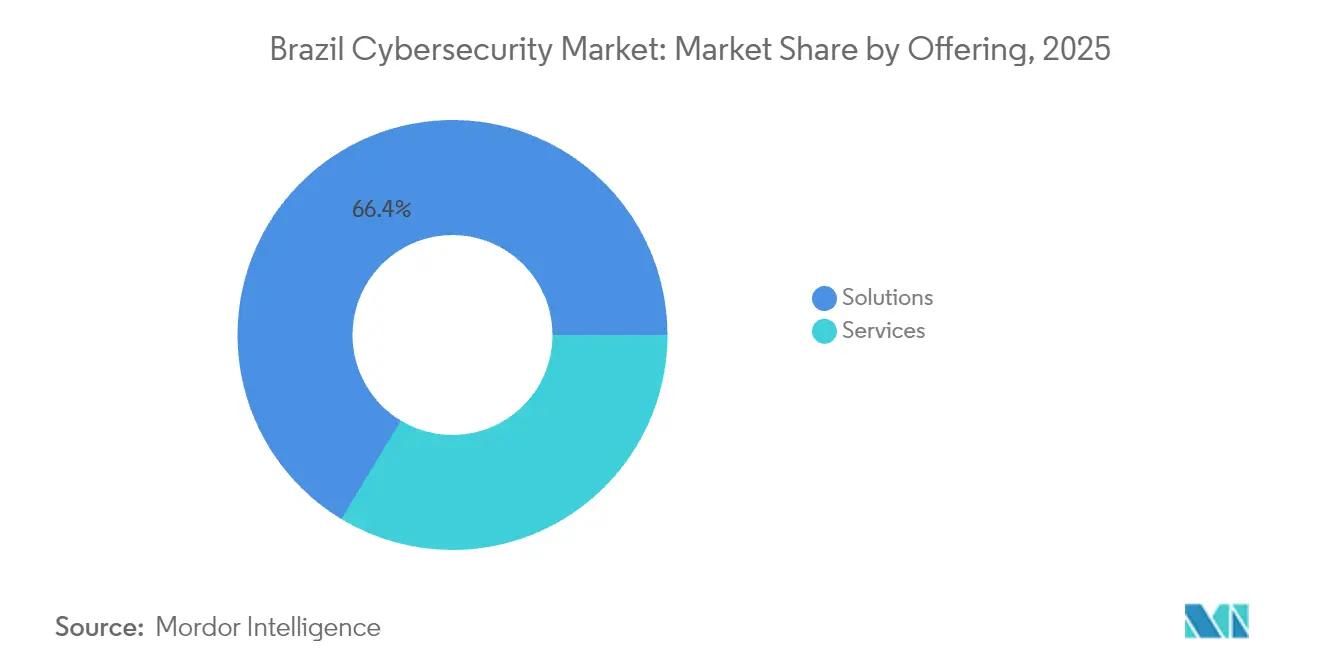

- By offering, Solutions captured 66.35% of 2025 revenue, whereas Services are forecast to expand at a 14.78% CAGR to 2031.

- By deployment mode, On-premises deployments held 60.80% of the 2025 Brazil cybersecurity market share, while Cloud-based models are set to grow at a 17.25% CAGR.

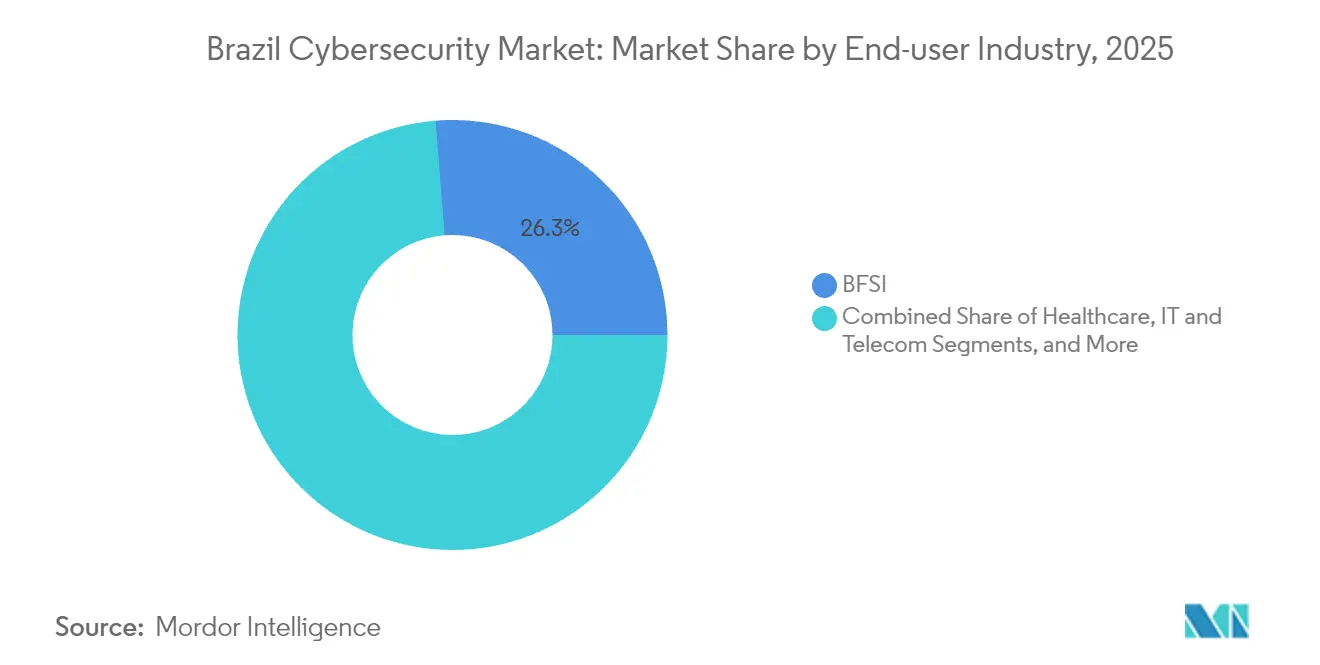

- By end-user industry, BFSI led with 26.25% revenue share in 2025; Healthcare is poised to record the fastest 17.45% CAGR through 2031.

- By end-user enterprise size, Large enterprises commanded 71.60% of 2025 spending, whereas SMEs are projected to increase outlays at a 13.74% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide roll-out of Open Finance and Pix driving new threat vectors | +2.5% | Major urban centres | Short term (≤ 2 years) |

| Government “Cloud First” and GovCloud mandates boosting security spend | +2.0% | Brasília first, expanding nationwide | Medium term (2–4 years) |

| Surging ransomware on critical infrastructure post-2022 election | +1.5% | Energy, water, transport networks nationwide | Short term (≤ 2 years) |

| LGPD and Central Bank Res. 4658 compliance deadlines | +2.3% | BFSI and healthcare hubs | Medium term (2–4 years) |

| Rapid 5G rollout expanding IoT attack surface | +1.8% | Urban nodes, widening to interior regions | Medium term (2–4 years) |

| Venture-capital inflow into fintech scale-ups demanding resilient security | +1.2% | São Paulo–Rio corridor and emerging tech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Nationwide Roll-out of Open Finance and Pix Driving New Threat Vectors

Pix processed about 3 billion transactions a month in early 2024, drawing sophisticated malware such as “PixPirate” that hijacks mobile transfers [1]Roberto Campos Neto, “Relatório Pix Mensal,” Banco Central do Brasil, bcb.gov.br. Seventy percent of all Pix traffic now originates on smartphones, escalating endpoint exposure. Because Open Finance lets users link multiple accounts, breaches at one institution propagate laterally across the ecosystem. Banks respond by hard-coding quarterly refreshes of fraud-detection models and subscribing to shared threat-intelligence exchanges. As a result, demand for API-security gateways and mobile-security SDKs increases faster than any other protection layer inside the Brazil cybersecurity market.

Government Cloud First and GovCloud Mandates Boosting Security Spend

A presidential decree in 2024 obliges federal agencies to default to cloud resources and align with new national cybersecurity policy frameworks [2]GSI/PR, “Política Nacional de Segurança Cibernética,” Institutional Security Cabinet, gov.br. Procurement teams therefore bundle workload-protection and configuration-audit tools into every new SaaS contract. Uniform baseline controls shorten the sales cycle for vendors with early certifications, enabling them to capture disproportionate Brazil cybersecurity market share inside public-sector accounts. Spill-over effects reach state and municipal bodies as federal grants require adherence to GovCloud specifications.

Surging Ransomware on Critical Infrastructure Post-2022 Election

Confirmed ransomware incidents on utilities jumped from zero a decade ago to 16 in 2024; experts assert the real figure is higher due to voluntary disclosure rules. Organised crime groups exploit legacy industrial-control protocols, shrinking the defender’s dwell-time window. Utilities now redirect operational-expenditure budgets toward network segmentation, OT-SOC outsourcing and immutable backup tiers. Consequently, service-heavy contracts outpace appliance deals, reinforcing the growth of managed services inside the Brazil cybersecurity market.

LGPD and Central Bank Resolution 4658 Compliance Deadlines

Resolution CD/ANPD 15 requires organisations to disclose material incidents to the National Data Protection Authority within three business days, raising the bar for automated detection and response. Financial institutions must also observe Central Bank Resolution 4658, which mandates five-year audit-log retention. Companies now integrate user-behaviour analytics, file-integrity monitoring and immutable storage in a single compliance stack. This convergence accelerates platform adoption and enlarges the Brazil cybersecurity market because one investment simultaneously satisfies privacy, resilience and fraud-prevention objectives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of SOC analysts inflating MSSP pricing | −1.8% | Most severe outside São Paulo–Rio | Medium term (2–4 years) |

| Double-digit BRL depreciation versus USD squeezing appliance-import capex | −1.5% | Import-dependent sectors nationwide | Short term (≤ 2 years) |

| Legacy systems resisting integration with modern OT-security platforms | −1.3% | Manufacturing and utilities | Long term (≥ 4 years) |

| Highly fragmented VAR/MSSP ecosystem outside the São Paulo–Rio corridor | −0.8% | Regional cities and rural areas | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of SOC Analysts Inflating MSSP Pricing

Brazil graduates fewer than 8,000 cybersecurity specialists per year against an open-position count exceeding 37,000, creating wage inflation and vacancy backlogs [3]Cetic.br, “Pesquisa TIC Empresas 2024,” NIC.br, cetic.br. Talent scarcity drives hourly MSSP rates up to 35% higher outside the São Paulo-Rio corridor, straining provincial budgets. Many mid-tier enterprises therefore adopt cloud-delivered detection platforms that embed orchestration and automated playbooks. While this shift supports spending growth, the skills gap narrows only gradually and remains a structural brake on the Brazil cybersecurity market.

Double-Digit BRL Depreciation Squeezing Appliance-import Capex

The BRL lost more than 10% against the USD between 2023 and 2024, inflating imported firewall and router prices. Hardware refresh cycles now stretch from four to six years, delaying appliance revenue. Enterprises prioritise software licences billed in local currency, and vendors respond by offering flexible subscription plans. Although depreciation tempers near-term hardware sales, the broader shift toward operational-expense models ultimately favours services and cloud offerings within the Brazil cybersecurity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Momentum as Skills Gap Widens

Solutions held 66.35% of 2025 spending, cementing the Brazil cybersecurity market share for appliance and software vendors. Network-security boxes and next-generation firewalls dominate, especially in BFSI and telecom environments that require deterministic latency. Yet, services grow at a 14.78% CAGR because CIOs concede that internal teams cannot keep pace with detection complexity. Managed detection and response contracts often bundle compliance reporting, enabling buyers to rationalise overlapping tools. Vendors embedding machine-learning analytics into service dashboards differentiate themselves and capture premium pricing.

The services surge also reflects regulatory pressure: LGPD audits increasingly request evidence of continuous monitoring, a requirement more easily satisfied by external SOCs. National-scale integrators therefore purchase regional MSSPs to secure talent and footprint, driving consolidation. Over the forecast horizon, integrated solution-service bundles gain popularity, blurring traditional demarcations and raising the average deal size in the Brazil cybersecurity market.

By Deployment Mode: Cloud Security Approaches Parity

On-premises deployments owned 60.80% of 2025 revenue because data-sovereignty mandates historically favoured local processing. Core banking systems, telecom signalling and defence networks still depend on dedicated hardware and air-gapped segments. Cloud-based security, however, is set to expand at a 17.25% CAGR, narrowing the gap and transforming procurement patterns. The government’s Cloud First edict obliges every new agency project to show why cloud is not viable, flipping the burden of proof.

Service providers respond by building sovereign-cloud zones in São Paulo and Rio that comply with LGPD localisation rules. Hyperscalers partner with domestic telcos to shorten last-mile latency and embed threat-intelligence feeds natively. Hybrid architectures dominate transition roadmaps, allowing organisations to protect sensitive workloads on-premise while harnessing cloud analytics for internet-facing applications. As confidence in remote key-management matures, cloud security will likely eclipse a third of total Brazil cybersecurity market size before the forecast period ends.

By End-user Industry: Healthcare Rises on Data-Protection Mandates

BFSI held 26.25% of 2025 spend, reinforcing its status as largest buyer because fraud pressure and strict Central Bank audits compel continuous control upgrades. Institutions integrate behavioural biometrics with Pix transaction monitoring, elevating analytics licences as a share of wallet. Healthcare, meanwhile, posts the highest 17.45% CAGR, propelled by digital records expansion and LGPD clauses on sensitive data. Hospitals deploy zero-trust network micro-segmentation to stop lateral malware movement, and health insurers insist on encryption-at-rest before settling breach-related claims.

Industrial OT environments also accelerate spending as 5G connectivity links sensors once isolated behind serial lines. Utilities migrated SCADA traffic into modern protocols, exposing legacy assets to internet-routed threats. Because regulatory mandates for OT security are still emergent, early movers voluntarily adopt ISA/IEC 62443 frameworks, setting de facto standards that suppliers must meet to remain on vendor lists. This multi-sector investment portfolio sustains double-digit growth across the Brazil cybersecurity market.

By End-user Enterprise Size: SMEs Turn Security into Sales Enabler

Large enterprises contributed 71.60% of 2025 revenue because of complex, multi-site environments and 24/7 monitoring requirements. Their budgets underpin early adoption of extended detection and response and breach-attack simulation. SMEs, conversely, lead growth at a 13.74% CAGR because digital supply-chain contracts now demand proof of information-security controls. Merchants exporting through global marketplaces must present security questionnaires aligned with ISO 27001 or NIST frameworks; failure blocks sales channels.

Cloud-native security platforms priced per user or per asset lower adoption barriers. Municipal economic-development agencies offer subsidised cyber-readiness training, creating shared buying syndicates that negotiate volume discounts. These mechanisms extend security coverage faster than direct subsidies could, enlarging the Brazil cybersecurity market without distorting competition. As cyber-insurance carriers incorporate security attestation into premium models, SMEs further prioritise investment.

Geography Analysis

Most cybersecurity revenue concentrates in the Southeast, where São Paulo hosts 80% of national data-centre capacity and the majority of tier-one incident-response teams. Corporates headquartered here enjoy sub-one-hour response times and faster threat-intelligence cross-pollination. Local universities collaborate with banks to run capture-the-flag competitions, enlarging the skilled-graduate pipeline. These factors reinforce São Paulo’s dominance within the Brazil cybersecurity market and attract foreign investment that amplifies ecosystem maturity.

Rio de Janeiro forms the second pole, driven by energy majors and critical-infrastructure operators. The city’s offshore oil platforms rely on low-latency satellite links secured by purpose-built encryption overlays. Regional development agencies offer tax incentives for SOC build-outs, drawing managed-service providers to the port zone. Cross-pollination between maritime and utilities segments accelerates adoption of OT-aware detection tools. As 5G covers metro districts, telcos bundle endpoint-security add-ons with consumer broadband, broadening market reach.

Interior and northern regions historically lagged but are closing the gap as federal grants require compliance with GovCloud blueprints. States such as Pernambuco and Ceará deploy regional data hubs anchored by renewable-energy micro-grids. Agritech innovators in Goiás secure drone telemetry via light-weight certificate-based authentication, demonstrating that cyber-enabled productivity now extends beyond urban corridors. The expansion of regional IXPs lowers latency for cloud-security traffic, improving user experience and encouraging more rural enterprises to adopt advanced controls. Collectively these trends extend the geographic footprint of the Brazil cybersecurity market.

Competitive Landscape

Global vendors such as Cisco, Fortinet and Microsoft dominate network-security, identity management and cloud-workload protection. Their pre-certified GovCloud integrations and worldwide telemetry confer trust advantages for regulated buyers. To localise offerings, they partner with telecom operators and managed service providers that supply Portuguese-first interfaces and LGPD compliance modules. This symbiosis deepens penetration into federal agencies and tier-one banks, underpinning high-margin maintenance renewals.

Local specialists, including Tempest Security Intelligence and Modulo, leverage cultural fluency and bespoke consulting to win projects where regulatory nuance matters more than technology breadth. They excel in readiness assessments, LGPD gap analysis and incident-response retainers. Many white-label global XDR engines but wrap them with region-specific playbooks that address Pix-centric fraud vectors. Such layering delivers quicker mean-time-to-detect than generic templates, yielding measurable risk reduction that clients value.

Fragmentation persists in managed security services, yet consolidation accelerates. International entrants have begun acquiring regional VARs to gain client relationships and fulfil service-level obligations outside metropolitan hubs. Hyperscalers embed select MSSPs into marketplace contracts, rewarding partners that meet sovereign-cloud attestation. As talent scarcity persists, merger rationales hinge on SOC workforce pooling and playbook standardisation rather than purely geographical access. This consolidation trend will gradually raise the combined top-five Brazil cybersecurity market share, though niche providers will survive by specialising in OT or privacy audit services.

Brazil Cybersecurity Industry Leaders

IBM Corporation

Microsoft Corporation

Check Point Software Technologies Ltd.

Palo Alto Networks, Inc.

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Resecurity, a U.S.-based global leader in cybersecurity and threat intelligence, is expanding its operations in Brazil, as Brazilian enterprises, government institutions, and infrastructure providers strive to comply with Lei Geral de Proteção de Dados (LGPD) requirements.

- April 2025: Stellar Cyber, a leader in cybersecurity solutions, has appointed Silvio Eberardo as its first-ever Country Manager for Brazil. This move underscores the company's swift expansion and dedication to the Brazilian market.

- February 2025: Valsoft acquired VHL Sistemas to enter Latin American cybersecurity and fold offerings into its risk-intelligence stack.

- September 2024: Microsoft allocated USD 2.7 billion for Brazilian data-centre expansion, earmarking funds for AI-driven threat detection and sovereign-cloud services.

Brazil Cybersecurity Market Report Scope

Companies turn to cybersecurity solutions to shield their digital operations from looming cyber threats. With dangers like ransomware, spyware, and data breaches on the rise, businesses risk significant operational disruptions. That's where solution providers step in, offering essential cybersecurity services and products to fortify these companies against such threats. Brazil cybersecurity market is segmented by offering (solutions (application security, cloud security, data security, identity and access management, infrastructure protection, integrated risk management, network security equipment, end-point security, and other solutions), and services (professional services and managed services)), by organization size (SMEs, and large enterprises), by end-user industry (IT and telecom, BFSI, retail and e-commerce, manufacturing, defense, government, and other end users). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the forecast Brazil cybersecurity market size in 2031?

The Brazil cybersecurity market size is projected to reach USD 6.57 billion by 2031, up from USD 3.68 billion in 2025 and USD 4.05 billion in 2026.

Which deployment model is growing fastest?

Cloud-based security is expanding at a 17.25% CAGR, outpacing on-premises deployments as agencies comply with Cloud First mandates.

What drives healthcare’s rapid growth?

Digitisation of patient records and LGPD requirements boost healthcare cybersecurity spending at a 17.45% CAGR.

How does Brazilian currency volatility affect spending?

BRL depreciation raises the cost of imported appliances, prompting a shift toward locally priced software and cloud subscriptions.

Page last updated on: