Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

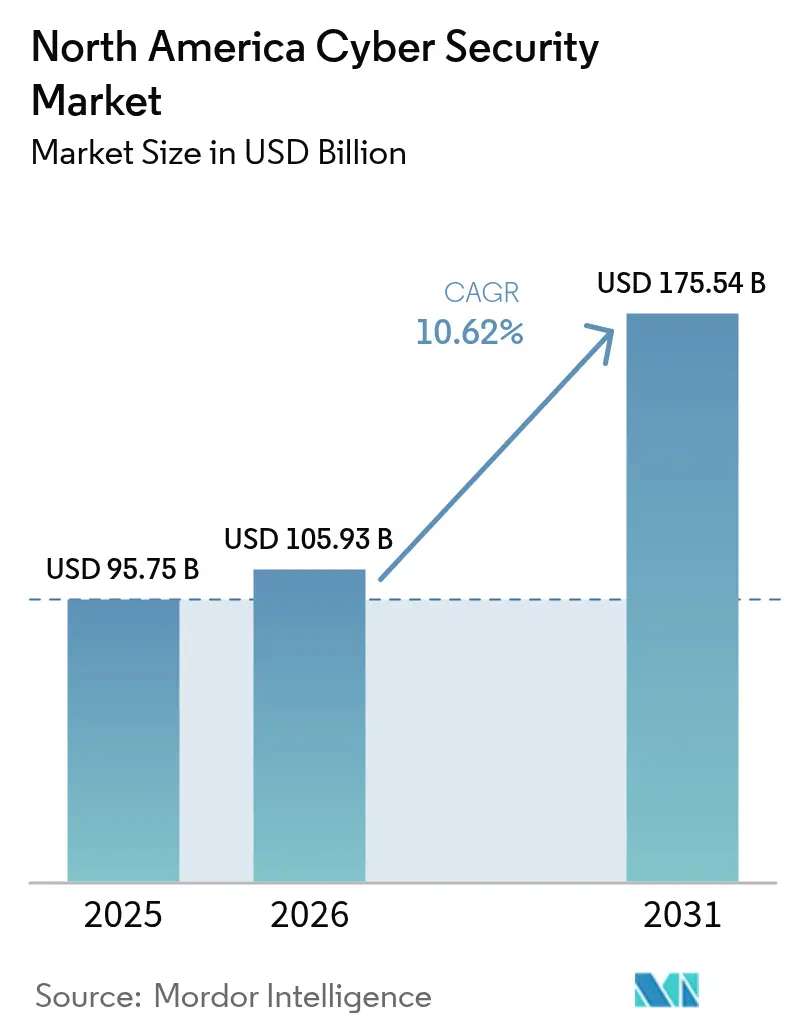

| Base Year Market Size (2025) | USD 95.75 Billion |

| Market Size (2026) | USD 105.93 Billion |

| Market Size (2031) | USD 175.54 Billion |

| Growth Rate (2026 - 2031) | 10.62% CAGR |

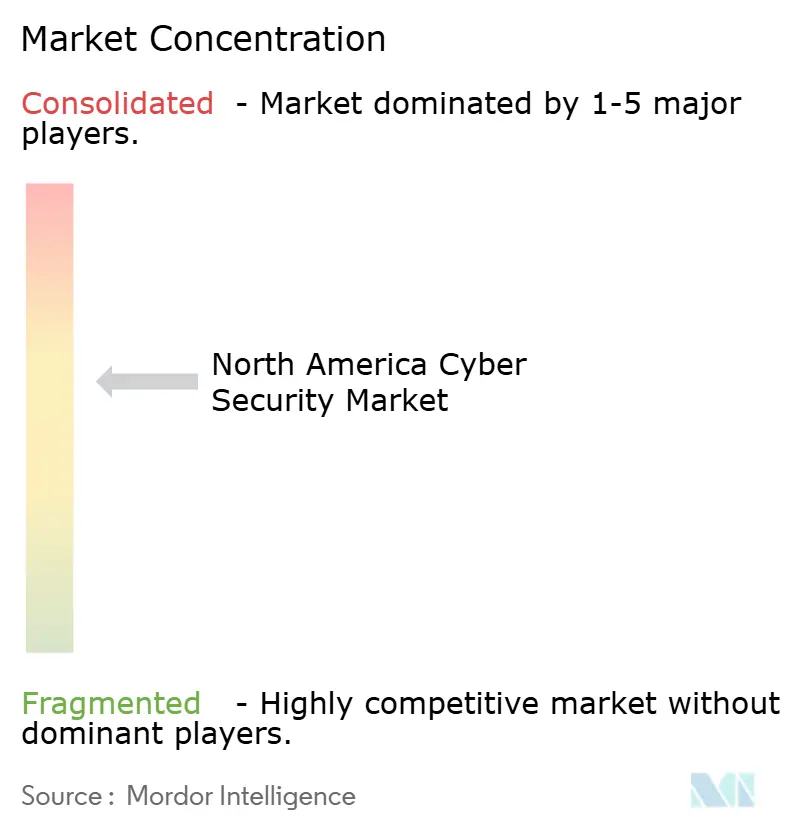

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Cybersecurity Market Analysis by Mordor Intelligence

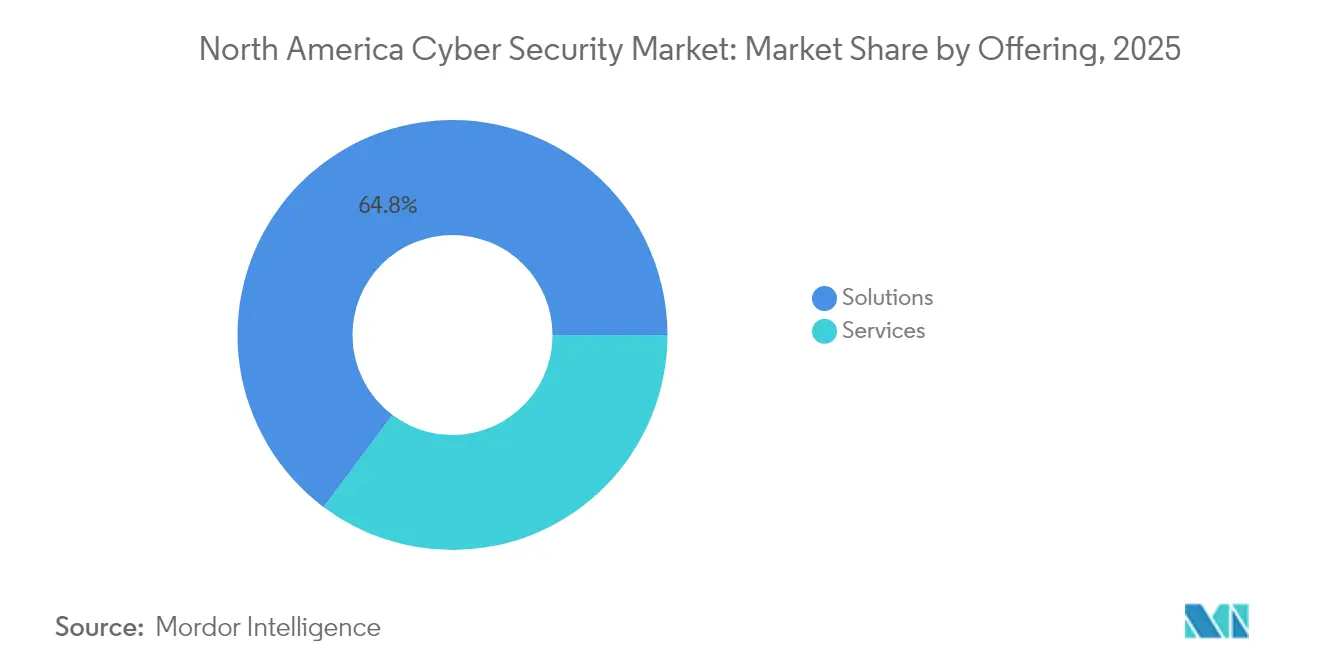

The North America Cybersecurity Market size was valued at USD 95.75 billion in 2025 and estimated to grow from USD 105.93 billion in 2026 to reach USD 175.54 billion by 2031, at a CAGR of 10.62% during the forecast period (2026-2031). Stringent federal and state regulations, the spread of sophisticated threats, and accelerated digital-transformation programs across critical industries are the primary growth engines. Mandatory breach-disclosure laws in all 50 U.S. states and new Securities and Exchange Commission reporting rules compel firms to invest in preventive controls instead of purely reactive incident response models. Spending is further fueled by the federal transition to post-quantum cryptography, which requires agencies and contractors to overhaul encryption systems by 2030-2035. The United States retains the lion’s share of regional demand, yet Canada registers the fastest expansion as Bill C-26 tightens critical-system requirements and stimulates vendor activity. Across offerings, solutions still represent 65.5% of revenue, although managed and professional services are growing faster as enterprises outsource security operations to close skills gaps.

Key Report Takeaways

- By offering, solutions accounted for 64.78% revenue share in 2025, while services are set to advance at a 13.52% CAGR to 2031.

- By deployment mode, on-premise held 55.63% of the North America cybersecurity market share in 2025; cloud deployment is projected to expand at 16.76% CAGR through 2031.

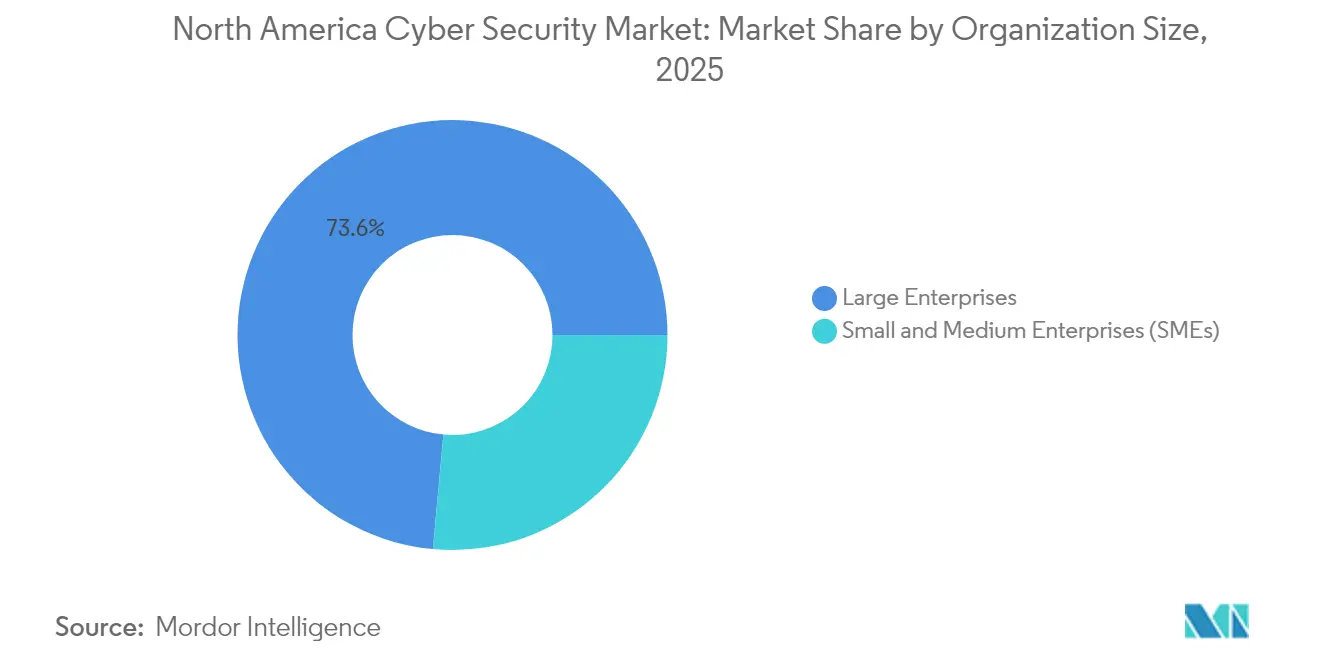

- By organization size, large enterprises controlled 73.55% of the North America cybersecurity market size in 2025, whereas the SME segment is forecast to post 12.88% CAGR between 2026-2031.

- By end-user, the BFSI sector led with 26.89% of the North America cybersecurity market share in 2025; healthcare is advancing at a 13.07% CAGR to 2031.

- By country, the United States dominated at 82.74% share in 2025, while Canada is on track for 12.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory breach disclosure laws and surging attack volumes | +2.1% | United States, Canada | Short term (≤ 2 years) |

| Cloud migration and zero-trust adoption momentum | +1.8% | North America | Medium term (2-4 years) |

| Explosion of IoT/IIoT endpoints across industry | +1.5% | United States, Mexico | Medium term (2-4 years) |

| U.S. federal post-quantum cryptography transition deadlines | +1.2% | United States | Long term (≥ 4 years) |

| Cyber-insurance underwriting tying premiums to controls | +0.9% | North America | Short term (≤ 2 years) |

| AI-powered SecOps platforms cutting mean-time-to-respond | +1.4% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory Breach Disclosure Laws and Surging Attack Volumes

Regulatory scrutiny intensified when the SEC levied USD 7 million in penalties on four listed technology companies for deficient SolarWinds-related disclosures, underscoring that incomplete cyber-risk reporting now carries tangible financial consequences. [1]Greenberg Traurig, “SEC Files Actions Against 4 Public Companies for Negligent Cybersecurity Disclosures,” gtlaw.com Coupled with 583 enforcement actions and USD 8.2 billion in remedies during fiscal 2024, the climate pushes boards to treat cybersecurity as a core compliance function rather than a discretionary IT spend. At the same time, Mexico logged 42.4 million malware attempts in 2024—116,000 per day—reflecting the wider regional surge in threat volume that now hits manufacturing hardest. Because every U.S. state enforces a notification statute and federal rules require disclosure within four business days of a material incident, enterprises have shifted budgets toward continuous monitoring, automated detection, and breach-containment platforms that shorten response cycles and cap liability.

Cloud Migration and Zero-Trust Adoption Momentum

Zero-trust models replaced perimeter-centric strategies once federal Executive Orders and NIST SP 800-207 established identity-focused architectures as the public-sector default. [2]National Institute of Standards and Technology, “Post-Quantum Cryptography,” csrc.nist.gov Today, 60% of North American enterprises have an active zero-trust program, and 94% have deployed at least one element; the transition is inseparable from sustained cloud-adoption waves that re-shape network edges and authentication flows. Organizations implementing zero-trust within hybrid or multi-cloud environments report 152% ROI through diminished incident handling and policy-maintenance burdens, a finding that resonates with finance and healthcare entities balancing regulatory mandates with cost discipline. The confluence of cloud migration and zero-trust tooling propels demand for secure access service edge (SASE) and identity-and-access-management platforms, reinforcing a structural service opportunity for MSSPs that specialize in multi-cloud governance.

Explosion of IoT/IIoT Endpoints Across Industry

Half of all connected devices in North American factories, hospitals, and utilities still ship with exploitable vulnerabilities, and one-third of recent regional breaches involved an IoT component. Healthcare incidents inflict the steepest financial harm at roughly USD 10 million per breach, magnified by patient-safety risks and HIPAA fines. Unpatched firmware explains 60% of IoT compromises, while legacy industrial equipment relies on outdated operating systems that resist modern security agents. As a result, ransomware events targeting manufacturing grew 73% year over year, with downtime costs often dwarfing ransom sums. Energy-based anomaly detection has emerged as a complementary control, using power-consumption deviations to flag suspicious device behavior.

U.S. Federal Post-Quantum Cryptography Transition Deadlines

NIST has scheduled the retirement of RSA-2048 and ECC-256 inside federal systems by 2030 and complete migration by 2035, allocating USD 7.1 billion for the effort. Agencies and contractors must catalog cryptographic assets, deploy hybrid algorithms, and acquire quantum-safe hardware. Post-quantum solutions revenue is forecast to climb from USD 302.5 million in 2024 to USD 1.887 billion in 2029, expanding the North America cybersecurity market as financial services and telecom operators adopt similar standards for long-term data confidentiality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of skilled cyber-security professionals | -1.7% | North America | Medium term (2-4 years) |

| High cost & complexity of multi-vendor tool stacks | -1.1% | United States, Canada | Short term (≤ 2 years) |

| Legacy OT systems expanding unmanaged attack surface | -0.8% | United States, Mexico | Long term (≥ 4 years) |

| Energy footprint of always-on analytics limiting adoption | -0.4% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Skilled Cyber-Security Professionals

North America entered 2025 with 542,687 open cybersecurity positions, a 4% increase even after employer headcount cuts of 2.7% in 2024. Budget freezes struck 37% of firms, but 90% still reported material skill gaps, particularly in AI-enabled analytics and zero-trust configuration. Mexico alone needs 35,000 specialists by 2025, yet 65% of local organizations cite talent scarcity as their top barrier, triggering an 80% uptick in advanced-technology spending to compensate. Skills shortages expose enterprises to prolonged dwell times, and breaches blamed on understaffed teams averaged USD 4 million in direct losses, adding pressure to adopt managed detection and response services that wrap technology and expertise in subscription packages.

Legacy OT Systems Expanding Unmanaged Attack Surface

Manufacturing and energy installations rely on decades-old control systems, including Windows XP derivatives, that lack vendor support and integration hooks for contemporary security agents. Virtual patching and network segmentation provide partial relief, but true risk reduction requires capital-intensive equipment replacement—an option many plants defer. Dragos' research found that OT-focused ransomware outbreaks rose during Q3 2024, with production downtime often eclipsing ransom amounts. The Department of Homeland Security warns that attackers now pivot from IT footholds into OT domains, threatening safety outcomes and regional supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Accelerate Despite Solutions Dominance

Solutions retained a 64.78% share of the North America cybersecurity market in 2025, yet services are on pace for 13.52% CAGR through 2031 as organizations outsource 24/7 monitoring to counter evolving threats. The services uptrend directly mitigates the skills shortage while giving firms rapid access to AI-driven analytics platforms. Professional services for quantum-safe cryptography assessments and zero-trust road-mapping have also risen. Managed detection and response illustrates this shift: eSentire now protects data for 2.5 million patients, underscoring demand in regulated fields.

The North America cybersecurity market size for managed services is expanding fastest among healthcare and mid-market manufacturing firms. Service-based consumption models help firms consolidate sprawling toolsets and secure board approval by treating cybersecurity as an operating expense. Vendors, in turn, bundle AI, threat intelligence, and human expertise, capturing sticky multiyear contracts and boosting recurring revenue visibility.

By Deployment Mode: Cloud Transformation Reshapes Security Architecture

On-premise deployments still made up 55.63% of the North America cybersecurity market size in 2025, but cloud security spending is advancing at 16.76% CAGR as hybrid work exposes perimeter-centric gaps. Federal zero-trust mandates, coupled with executive orders on cloud-first strategies, accelerate cloud-native adoption in defense and civil agencies. For private-sector adopters, the pivot lowers capital expenditure, integrates policy orchestration, and enables continuous compliance.

Large enterprises operate hybrid models for data-sovereignty reasons, while SMEs leapfrog straight to fully managed cloud-security service edges. Oracle’s framework for zero-trust cloud controls demonstrates how identity governance, micro-segmentation, and encryption converge to tighten attack surfaces. Vendors that automate policy creation and misconfiguration remediation find traction as multicloud complexity scales.

By Organization Size: SME Growth Outpaces Enterprise Maturity

Large enterprises held 73.55% of the North America cybersecurity market share in 2025, yet SMEs are expanding at 12.88% CAGR thanks to rising cyber-insurance requirements. Only 10% of SMEs carry cyber policies today, but insurers increasingly tether premiums to demonstrated controls such as MFA and endpoint detection. As a result, managed-service subscriptions that bundle compliance reporting are attracting resource-constrained firms.

SMEs also face costly breaches: Mexican businesses averaged USD 2.5 million in recovery expenses during 2024, a figure that often exceeds annual IT budgets. Vendor ecosystems that deliver enterprise-grade protections in pay-as-you-go formats unlock new addressable demand and support deeper regional market penetration.

By End-user: Healthcare Surge Challenges BFSI Leadership

The BFSI vertical led the North America cybersecurity market with 26.89% revenue share in 2025, driven by stringent supervision from the Federal Financial Institutions Examination Council and similar Canadian regulators. Healthcare, however, is accelerating at 13.07% CAGR after average breach costs hit USD 9.8 million, eclipsing finance as the costliest victim category. Mandatory encryption and logging rules proposed by the Department of Health and Human Services add pressure for hospital systems to upgrade controls.

Retail, telecom, and manufacturing maintain steady spending trajectories, but operational-technology-heavy sectors such as energy and utilities confront unique OT-IT integration challenges. They increasingly adopt anomaly-based monitoring and secure-gateway technologies to shield proprietary protocols from credential theft and ransomware exploits.

Geography Analysis

The United States dominated with 82.74% of the North America cybersecurity market in 2025, underpinned by federal post-quantum budgets and the world’s largest ecosystem of cyber vendors. Enforcement signals from the SEC, plus 50-state disclosure statutes, keep spending elevated. The United States anchors the regional ecosystem with robust federal investment, a vibrant vendor landscape, and layered statutes that stimulate steady demand. Federal agencies alone will channel USD 7.1 billion into quantum-safe implementations by 2035, and leading suppliers such as Palo Alto Networks, CrowdStrike, and Fortinet continue to post double-digit subscription ARR gains. Combined, these conditions reinforce the North America cybersecurity market’s position as the global benchmark for regulatory-driven security spending.

Canada’s 12.52% CAGR reflects Bill C-26 obligations and a USD 13.74 billion domestic market in 2025, helped by a CAD 917.4 million budget boost for national cyber operations. Canada’s ascent is propelled by legislative momentum and targeted public funding. Ottawa’s CAD 917.4 million allocation enhances national cyber capabilities, while a USD 240 million investment in Cohere Inc. fosters AI talent and data-sovereignty solutions. The Cyber Security Innovation Network catalyzes R&D collaborations between universities and firms like Ericsson, positioning Canada as a complementary innovation node within the regional value chain.

Mexico, though smaller at an expected USD 3.19 billion by 2028, shows improving readiness as companies earmark higher budgets and align with USMCA standards for incident cooperation. Mexico’s digital-economy expansion and 97 million internet users create a widening attack surface, yet the government—backed by USMCA cooperation frameworks—is tightening guidelines and launching capacity-building initiatives. Enterprises that align with cross-border supply-chain requirements gain preferential access to U.S. partners, reinforcing investment in modern controls, especially among manufacturers exporting into U.S. markets.

Competitive Landscape

Merger and acquisition activity underscores moderate consolidation. Forty-five transactions were announced in January 2025, and the aggregate 2024 deal value reached USD 45.7 billion as incumbents raced to acquire AI analytics, cloud-native architectures, and verticalized OT security capabilities. [4]SecurityWeek, “Cybersecurity M&A Roundup: 45 Deals Announced in January 2025,” securityweek.com Enterprise buyers juggle an average of 83 disparate tools from 29 vendors, so suite vendors promoting unified platforms gain traction.

AI is the definitive differentiator. Palo Alto Networks’ Cortex XSIAM 3.0 claims 99% noise reduction in vulnerability alerts, while Microsoft’s unified SecOps platform trims mean time to detect by 88% and lowers breach risk by 60%. Cisco’s acquisitions of SnapAttack and Robust Intelligence highlight the premium on automated threat simulation and AI model validation.

White-space remains in the SME and OT security niches. Only 10% of smaller firms possess cyber insurance, revealing a service onboarding opportunity, and legacy control systems require bespoke solutions that few mainstream vendors address. Start-ups focused on generative-AI-driven threat detection and quantum-safe encryption boast higher valuations, signaling investor confidence that innovation rather than scale will unlock the next wave of regional growth.

North America Cybersecurity Industry Leaders

Palo Alto Networks, Inc.

Fortinet, Inc.

CrowdStrike Holdings, Inc.

Cisco Systems, Inc.

Check Point Software Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ericsson was named a Top International Corporate Citizen for the third consecutive year and pledged USD 635 million to Canadian R&D in 5G, AI, and cloud security.

- May 2025: SEALSQ Corp detailed USD 7.2 million in 2025 R&D spending to advance quantum-resistant chips, targeting a post-quantum segment forecast to hit USD 1.887 billion by 2029.

- April 2025: Palo Alto Networks introduced Cortex XSIAM 3.0, positioning the product for a USD 37 billion addressable AI SecOps market.

- March 2025: Canada finalized a USD 240 million investment in Cohere Inc. for AI compute capacity to strengthen data-sovereignty protections.

- March 2025: Rubrik closed FY 2025 with subscription ARR of USD 1.092 billion, up 39%, evidencing momentum in cyber-resilience services.

- February 2025: Fortinet posted USD 5.96 billion in 2024 revenue, forecasting USD 6.65-6.85 billion in 2025 on unified SASE and SecOps growth.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North America cybersecurity market as all revenue generated from software, services, and connected security appliances deployed to detect, prevent, and respond to malicious activity across IT, OT, and cloud assets within the United States, Canada, and Mexico; values are captured at vendor billings net of channel mark-ups according to Mordor Intelligence.

Scope Exclusions: Physical guarding, analog access-control hardware, and stand-alone fraud analytics tools are outside this coverage.

Segmentation Overview

- By Offering

- Solutions

- Application Security

- Cloud Security

- Data Security

- Identity and Access Management

- Infrastructure Protection

- Integrated Risk Management

- Network Security Equipment

- Endpoint Security

- Other Solutions

- Services

- Professional Services

- Managed Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premise

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-user

- BFSI

- Healthcare

- IT and Telecom

- Industrial and Defense

- Retail

- Energy and Utilities

- Manufacturing

- Other End-users

- By Country

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with CISOs, SOC engineers, cloud-security architects, and managed-service executives across eight U.S. states, two Canadian provinces, and Mexico City to validate adoption rates, post-quantum pilot budgets, and average service mark-ups. This closed the loops left by secondary data.

Desk Research

We mapped baseline demand using open datasets from CISA breach tallies, FBI IC3 loss reports, NIST digital-trust indexes, Statistics Canada ICT spending tables, and Mexico's INEGI trade codes. We then tied these to sectoral ICT budgets. Publicly available filings, federal procurement logs, CSA and ISACA briefs, plus news and private-company snapshots drawn from D&B Hoovers and Dow Jones Factiva provided pricing corridors and vendor mix.

Additional context came from patent counts on Questel, WSTS semiconductor output, and voluntary incident disclosures under U.S. SEC rules, which jointly signaled technology refresh rates and service uptake. This list is illustrative, not exhaustive, and many more sources fed the desk review.

Market-Sizing & Forecasting

We built a top-down pool from regional ICT outlays, regulated breach-cost multipliers, and cyber-budget shares, which is then pressure-tested through selective bottom-up roll-ups of protected endpoints multiplied by blended ASPs and distributor channel checks. Key model variables include zero-trust penetration, average cost per data breach, cloud workload share, regulated-sector headcounts, and managed security outsourcing intensity. Forecasts employ multivariate regression on these drivers with ARIMA overlays for macro ICT cycles, and gap-fill assumptions are revisited in expert re-contacts.

Data Validation & Update Cycle

Outputs pass three-layer variance checks versus historical attack volume, vendor revenue disclosures, and customs trade flows. Senior reviewers sign off quarterly; reports refresh annually, with mid-cycle updates for material regulations or mega-breaches. Only after these filters are applied and every anomaly is reconciled do we freeze the baseline.

Why Mordor's North America Cyber Security Baseline Commands Reliability

Published estimates often diverge because research firms slice geography, threat classes, and pricing bundles differently, and some extend historical vendor totals without fresh field checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 95.75 B (2025) | Mordor Intelligence | |

| USD 86.94 B (2024) | Industry Tracker A | Omits Mexico and hardware firewalls; relies on 2023 vendor filings |

| USD 84.09 B (2024) | Global Consultancy B | Bundles network equipment with SaaS yet excludes managed-service fees |

| USD 91.65 B (2024) | Regional Consultancy C | Uses constant-currency 2022 rates and counts software licenses only |

Differences of up to USD 10 billion arise once scope, currency year, or channel margins shift. By anchoring clearly stated inclusions, multi-source primary checks, and an annual refresh cadence, Mordor Intelligence delivers a transparent, decision-ready baseline that executives can trace back to measurable spending signals.

Key Questions Answered in the Report

What is the current value of the North America Cybersecurity Market?

The market stood at USD 105.93 billion in 2026 and is on track to reach USD 175.54 billion by 2031.

Which country leads regional spending?

The United States commands 82.74% of total spending, propelled by federal mandates and a dense vendor ecosystem.

Why is healthcare cyber security growing faster than BFSI?

Healthcare breaches average USD 9.8 million, exceeding finance, so providers are rapidly upgrading controls to limit financial and patient-safety impacts.

How does the post-quantum transition affect vendors?

Agencies must retire RSA-2048 by 2030, driving demand for quantum-safe algorithms and boosting cryptography services revenue at 42.15% CAGR.

What role does managed detection and response play for SMEs?

MDR delivers enterprise-grade monitoring without in-house teams, helping SMEs satisfy cyber-insurance prerequisites and reduce breach exposure.

Is talent shortage still a major restraint?

Yes. North America has 542,687 unfilled cyber roles, prompting firms to adopt AI-enabled platforms and outsourced services to bridge the skills gap.

Page last updated on: