Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

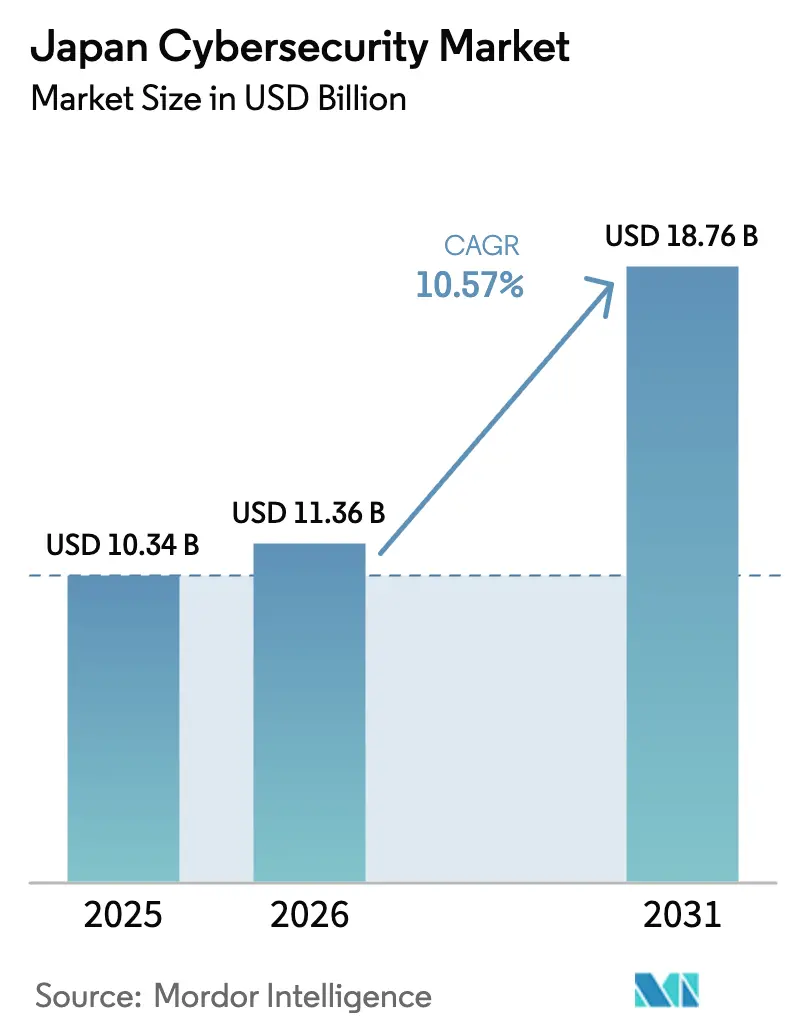

| Base Year Market Size (2025) | USD 10.34 Billion |

| Market Size (2026) | USD 11.36 Billion |

| Market Size (2031) | USD 18.76 Billion |

| Growth Rate (2026 - 2031) | 10.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Cybersecurity Market Analysis by Mordor Intelligence

The Japan cybersecurity market size is expected to increase from USD 10.34 billion in 2025 to USD 11.36 billion in 2026 and reach USD 18.76 billion by 2031, growing at a CAGR of 10.57% over 2026-2031. Strong public-sector capital expenditure, forward-leaning regulations, and the rapid migration of enterprise workloads to hybrid and multi-cloud architectures have moved spending from isolated incident response toward always-on threat hunting. Cloud-delivered controls, sovereign extended detection and response (XDR) platforms, and zero-trust building blocks now dominate procurement conversations, while talent scarcity continues to channel budget toward managed security services. Intensifying ransomware activity and new Tokyo Stock Exchange disclosure rules have elevated cyber resilience to a financial governance priority, compelling boards to treat breaches as material events. Intensifying 5G private-network rollouts, especially across smart factories in Chubu and Kanto, are reinforcing demand for operational-technology (OT) security that can protect industrial internet-of-things assets without disrupting production uptimes.

Key Report Takeaways

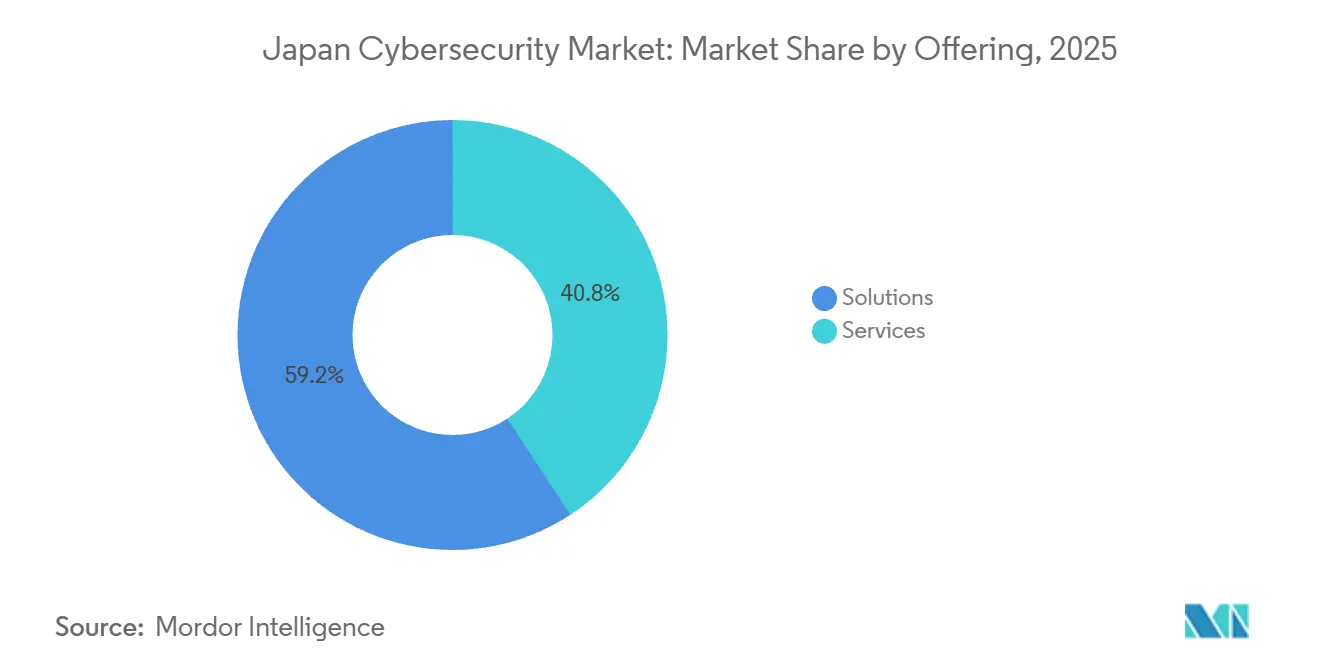

- By offering, solutions led with 59.24% of Japan cybersecurity market share in 2025. However, services are projected to expand at an 11.32% CAGR through 2031, the fastest growth rate within the segmentation.

- By deployment mode, cloud accounted for 54.86% of market share in 2025, and is forecast to grow at a 11.56% CAGR to 2031, outpacing on-premises alternatives.

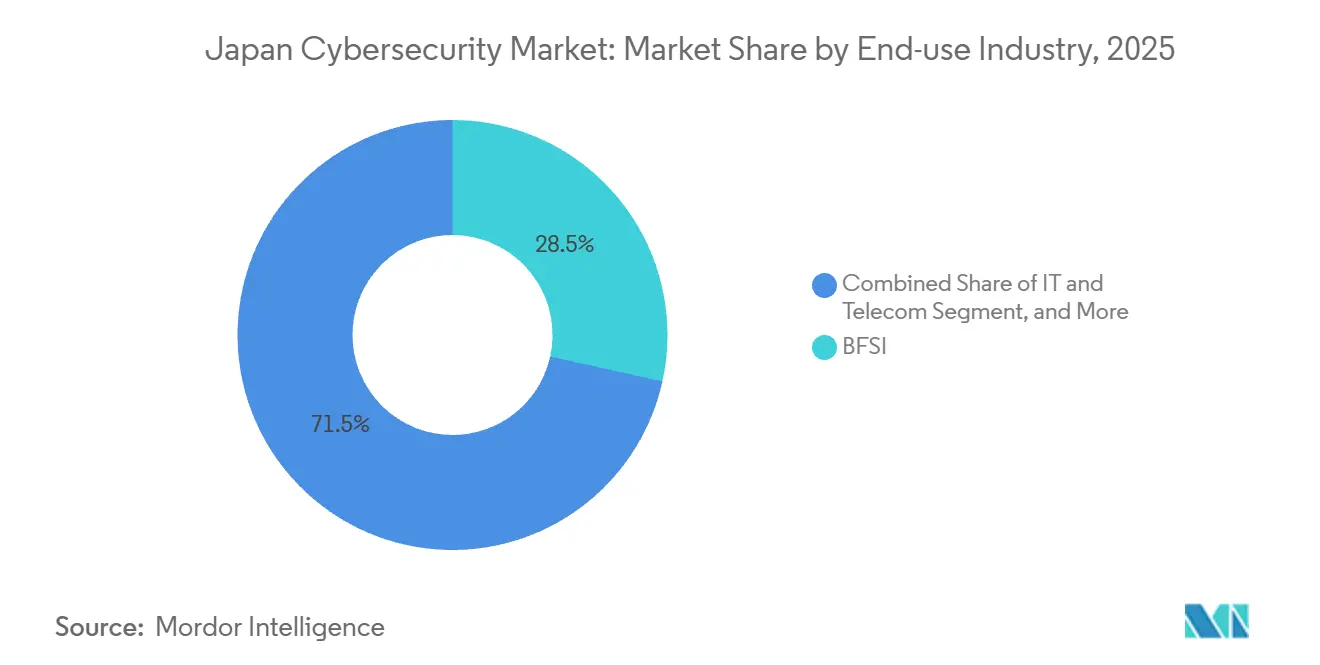

- By end-use industry, banking, financial services, and insurance captured 28.46% of share in 2025, whereas information technology and telecommunications are expected to advance at a 12.12% CAGR through 2031, the quickest among verticals.

- By enterprise size, large enterprises accounted for 64.69% of share in 2025. Whereas, small and medium enterprises are projected to grow at an 11.72% CAGR to 2031, the highest rate within this segmentation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Japanese Government CAPEX Surge Post Digital Agency Formation | +2.1% | National, Tokyo, Osaka, Nagoya metropolitan areas | Medium term (2-4 years) |

| Mandatory Zero-Trust Guidelines for Critical Infrastructure by 2026 | +1.8% | National, 14 critical-infrastructure sectors | Short term (≤ 2 years) |

| Generative-AI-Driven Attack-Surface Expansion Across Enterprises | +1.5% | Global, acute in IT and Telecom, BFSI, Manufacturing | Short term (≤ 2 years) |

| 5G Private-Network Roll-outs in Smart Factories, Especially Chubu | +1.3% | Chubu and Kanto industrial belts | Medium term (2-4 years) |

| Tokyo Stock Exchange Cyber-Risk Disclosure Rules Boost Spending | +1.2% | National, all TSE-listed companies | Medium term (2-4 years) |

| Legacy OT Modernisation Ahead of Osaka-Kansai Expo 2025 | +0.9% | Kansai region with spillover to host cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Japanese Government CAPEX Surge Post Digital Agency Formation

A multiyear spending cycle is unfolding after the Digital Agency’s creation, with more than USD 3.8 billion in 2025 public-private cyber projects and a JPY 21.3 trillion (USD 142 billion) stimulus that declares cyber defense on par with energy and telecom. Competitive grants funnel capital toward threat-intelligence hubs, deception platforms, and automated response orchestration that meet the Active Cyber Defense Law’s pre-emptive posture.[1]National center of Incident Readiness and Strategy for Cybersecurity, “Active Cyber Defense Law,” nisc.go.jp METI’s strategy to scale the domestic sector from JPY 0.9 trillion to JPY 3 trillion within ten years earmarks JPY 30 billion (USD 200 million) for research in fiscal 2025, providing the seedbed for sovereign XDR and quantum-safe cryptography. Government procurement rules cascade into the private supply chain, compelling vendors of all sizes to certify against National Center of Incident Readiness and Strategy for Cybersecurity benchmarks. As ministries target 50,000 certified professionals by 2030, integrators are racing to automate basic security-operations-center (SOC) workflows, freeing scarce analysts for proactive hunting.

Mandatory Zero-Trust Guidelines for Critical Infrastructure by 2026

Zero-trust blueprints released in January 2025 require 14 critical-infrastructure sectors to verify every user, device, and workload before granting access.[2]Cloud Security Alliance, “Zero-Trust Architecture Guidance for Critical Infrastructure,” cloudsecurityalliance.org The Financial Services Agency mirrored these principles in its July 2025 update, obligating banks to practice least-privilege segmentation and continuous authentication. Supply-chain evaluations planned for fiscal 2026 will extend obligations to thousands of SME vendors, accelerating purchase orders for identity governance, micro-segmentation, and software-defined perimeters. Early adopters in banking and telecom already run pilot environments, while manufacturing and utilities wait for stricter enforcement triggers. Ongoing dialogue among the FSA, the Financial System Information Center, and regulated firms underscores the still-evolving guidance on cloud outsourcing and generative-AI usage.

Generative-AI-Driven Attack-Surface Expansion Across Enterprises

The May 2024 conviction for AI-generated ransomware proved that offensive tooling is now widely accessible. During 1H 2025, Japan logged 68 ransomware incidents, 40% more than a year earlier, with the Qilin group behind roughly 40% of attacks. Prominent breaches at Asahi Group Holdings and Askul Corporation each exposed tens of gigabytes of data, while CrowdStrike flagged Japan as a top Asia-Pacific target for AI-accelerated phishing. Boards are therefore funding behavioral analytics, deception grids, and XDR suites able to baseline user behavior and shut down machine-generated anomalies in real time. Rising crime losses of JPY 3.22 trillion (USD 22 billion) in 2024 forced regulators to impose 24-hour breach-notification windows, raising both reputational and financial stakes.

5G Private-Network Roll-outs in Smart Factories, Especially Chubu

Automotive and precision-machinery giants in Aichi Prefecture have become Japan’s proving ground for secure local 5G. NTT East’s February 2025 project achieved a 96% success rate across 265 verification scenarios, including 44 security tests.[3]NTT East, “Local 5G Optimization Project Results,” ntt-east.co.jp Cisco, Mitsui, and KDDI opened a demo facility at the Komaki Smart Factory Innovation Center that merges edge computing with real-time threat detection. Parallel trials by Fujitsu and Trend Micro validated anomaly detection for industrial-IoT traffic. Sumitomo Electric and SoftBank began mass-producing private-5G terminals in June 2025, shrinking deployment lead times. Updated METI factory guides warn that rogue base stations and man-in-the-middle exploits can bypass legacy OT defenses, spurring incremental demand for industrial firewalls and zero-trust segmentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Cyber-Talent Shortage Inflating SOC Service Costs | -1.4% | National, especially Tokyo, Osaka, Nagoya | Long term (≥ 4 years) |

| Multi-Tier Channel Structure Inflating SME Solution Pricing | -0.9% | National, acute in regional SMEs | Medium term (2-4 years) |

| Conservative Corporate Culture Slows Zero-Trust Adoption | -0.7% | Manufacturing and utilities sectors | Long term (≥ 4 years) |

| Fragmented SME Base Despite METI Subsidies | -0.5% | Regional supply-chain economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Cyber-Talent Shortage Inflating SOC Service Costs

Japan is short roughly 110,000 security professionals, and even METI’s plan to certify 50,000 experts by 2030 will leave a large gap. Scarcity drives analyst salaries higher, forcing managed-service providers to pass costs downstream through steeper retainers and per-incident fees. NTT DATA, which holds the world’s number-two managed-security share, mitigates wage inflation by rotating work across offshore SOCs, yet still battles for Japanese-language reverse engineers and threat hunters. Specialized skills in OT security, cloud-native architectures, and AI governance are rarer still, extending project timelines and inflating the total cost of ownership. SMEs, unable to match pay scales set by major banks and telecoms, either outsource all security or defer projects until government-funded training programs bear fruit.

Multi-Tier Channel Structure Inflating SME Solution Pricing

Most vendors rely on global-to-national distributors who resell to regional value-added resellers, creating markups of 30–50% before software reaches SMEs. Although METI covers up to 75% of eligible digitalization expenses, reimbursements arrive post-implementation, forcing cash-constrained firms to pre-finance purchases. The economics deter many local shops from modernizing defenses, especially outside metropolitan Tokyo and Osaka. Sovereign start-ups such as Japan Cyber Defense are offering transparent software-as-a-service pricing to bypass intermediary layers, yet conservative buyers still trust legacy brands. Until direct-sales or marketplace models mature, fragmented procurement channels will remain a margin-inflating drag on SME adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain as Talent Scarcity Drives Outsourcing

Solutions held 59.24% of Japan cybersecurity market share in 2025 as enterprises procured firewalls, endpoint protection, and identity suites to cover immediate compliance gaps. Yet the acute labor shortage is pushing boards to hand continual monitoring to outside specialists, causing the services segment to expand at an 11.32% CAGR through 2031, the quickest pace inside the Japan cybersecurity market. Managed SOCs, professional consulting, and incident-response retainers are therefore becoming default line items, particularly for regional lenders and smart-factory operators that lack certified staff. Vendors are replacing perpetual licenses with subscription bundles that embed 24/7 monitoring, using automation to compress analyst workload. This shift keeps platform loyalty high, because once telemetry from network, endpoint, and cloud flows into one provider’s console, switching costs escalate.

Demand within the solutions bucket is nonetheless evolving. Identity and access management and cloud-native controls are cannibalizing legacy network appliances as zero-trust rules kick in. Governance, risk, and compliance dashboards are selling briskly among TSE-listed corporates that now disclose cyber incidents as material events. Application and API security is also surging as developers containerize workloads and expose microservices, exposing new attack vectors. Meanwhile, integrated risk platforms that stitch compliance, detection, and reporting into a single pane of glass are gaining ground, promising boards an auditable path from executive KPIs to SOC playbooks. The Ministry of Economy, Trade and Industry’s growth roadmap will further amplify domestic software production, but given certification lead times, services will remain the higher-growth slice of the Japan cybersecurity market.

By Deployment Mode: Cloud Dominance Reflects Hybrid-IT Migration

Cloud held 54.86% of the market share in 2025, making it the largest component of the Japan cybersecurity market. With an 11.56% CAGR forecast through 2031, cloud controls are widening their lead as software-as-a-service adoption climbs. Financial Services Agency rules now require banks to vet provider security and retain incident-response authority, conditions that are steering demand toward regionally hosted data centers. Sovereign clouds operated by domestic integrators appeal to government agencies keen to keep sensitive telemetry within Japanese jurisdiction. At the same time, vendors such as Palo Alto Networks are deploying Prisma Access Browser in Japan to meet low-latency access and data-residency requirements.

On-premise deployments persist inside air-gapped operational-technology grids, where latency tolerance is low, and data sovereignty is absolute. Critical-infrastructure players are therefore combining local packet capture and industrial firewalls with cloud-hosted analytics nodes, yielding blended architectures that keep production traffic isolated yet benefit from scalable machine-learning engines. Factory-security guidelines published in April 2025 formalize this duality, recommending segmentation that leaves programmable-logic controllers on isolated networks while extracting metadata to cloud SIEMs. Sovereign XDR start-ups add a middle path, offering fully domestic hosting that placates economic-security hawks without depriving buyers of elastic compute. Over the forecast horizon, hybrid patterns will dominate, but every new SaaS workload still tips budget toward cloud-delivered security.

By End-Use Industry: IT and Telecom Surge Amid 5G Rollouts

Banking, financial services, and insurance commanded 28.46% of the market share in 2025, anchoring the Japan cybersecurity market size because regulators demand always-on controls and instant breach notification. Even so, information technology and telecommunications is the fastest-growing vertical, advancing 12.12% annually as carriers secure 5G core networks, edge-compute nodes, and slicing orchestration. Successful 5G pilots in Chubu demonstrated that deterministic latency and robust encryption can coexist, encouraging telcos to commercialize private-network blueprints for automotive OEMs and precision-machinery exporters. Each private-network deal pulls through identity, micro-segmentation, and real-time packet inspection, swelling vendor backlogs.

Healthcare spending is accelerating as hospitals digitize records and expand telemedicine, yet procurement remains fragmented across public and private bodies. Industrial manufacturing is reinforcing OT perimeters to support smart factories, pushed by METI guidance and OEM demands for secure supply-chain data sharing. The retail sector, scarred by 2025 ransomware disruptions at leading e-commerce portals, is busy integrating payment fraud analytics into XDR pipes. Energy and utilities, legally bound to embrace zero-trust, are budgeting for identity verification and continuous monitoring that can interoperate with supervisory control and data-acquisition gear. Defense primes, meanwhile, view quantum-safe crypto and edge AI as future differentiation, as signaled by the February 2026 Fujitsu-Lockheed MOU to co-develop dual-use technology.

By End-User Enterprise Size: SMEs Accelerate Despite Pricing Headwinds

Large enterprises accounted for 64.69% of the market share in 2025, consistent with their deeper pockets and heavier regulatory mandates. Smaller firms, however, are the fastest-moving cohort, growing at an 11.72% CAGR through 2031 as ransomware frequency climbs and subsidy awareness spreads. Because SMEs cannot tolerate the total-cost premium baked into legacy distribution, they gravitate toward SaaS bundles with transparent pricing and minimal configuration. Seed-funded sovereign platforms promise domestic-language support and one-click onboarding, addressing concerns that foreign telemetry sharing might conflict with economic security rules. Ransomware statistics from 1H 2025, which showed that SMEs accounted for a sizable share of the 68 reported incidents, have further jolted boards into action.

Large enterprises continue to rationalize tool sprawl, migrating stand-alone antivirus and IDS boxes onto unified XDR consoles to streamline alert fatigue. Trend Micro’s 58% surge in platform recurring revenue illustrates this consolidation play, especially among banks and telecoms that manage heterogeneous operating systems. NEC is pairing its cotomi generative-AI engine with global SOC footprints to automate level-one triage and shrink mean-time-to-contain. NTT DATA’s partnership with Palo Alto Networks adds AI-powered managed XDR across cloud and edge, signaling that hyperscale visibility is now table stakes. For SMEs, managed-service bundles that hide complexity remain the only sustainable on-ramp, yet subsidy reimbursement cycles and multi-tier markups still temper adoption velocity.

Geography Analysis

Japan remains a single-country market, but spending clusters mirror the nation’s industrial topography. Tokyo, as the financial nucleus, concentrates governance-risk-and-compliance expenditures because Tokyo Stock Exchange rules require prompt cyber-risk disclosure. Osaka and Nagoya anchor manufacturing and logistics corridors where smart-factory pilots and OT-modernization projects proliferate. The Digital Agency’s creation accelerated national funding, channeling more than USD 3.8 billion into 2025 projects and earmarking an additional JPY 21.3 trillion stimulus that explicitly names cybersecurity a strategic pillar. Passage of the Active Cyber Defense Law aligned Japan with allies practicing preemptive threat neutralization, elevating demand for intelligence fusion centers and deception grids that can identify attackers upstream.

Chubu’s automotive cluster exemplifies how 5G private-network deployments influence regional spending. Proof-of-concepts in Aichi delivered a 96% validation rate for security controls, assuring factory chiefs that LTE-replacement networks will not jeopardize safety PLCs. As deployments scale, each new cell brings incremental orders for identity gateways and micro-segmentation software. The Kansai region experienced a similar uplift ahead of the Osaka-Kansai Expo, where biometric ticketing and facial-authentication rollouts forced legacy OT to integrate modern encryption and analytics. Post-expo spillover is driving municipalities to replicate security blueprints for civic venues and metro systems, adding tail-winds to regional integrators.

Talent shortages cut across all prefectures but are sharpest in Tokyo, where banks and tech titans vie for reverse engineers conversant in Japanese-language malware. Offshore staffing by global integrators tempers wage escalation, yet localized threat-intel interpretation remains a scarce skill, extending project lead times. Across the archipelago, SMEs in secondary cities face the steepest distribution markups because multi-tier resellers add costs as solutions move away from urban centers. METI subsidies alleviate capex, but reimbursement cycles still force rural SMEs to self-finance before seeing refunds, slowing penetration outside megacities. Consequently, geography shapes both demand intensity and go-to-market friction inside the Japan cybersecurity market.

Competitive Landscape

The Japan cybersecurity market hosts a moderately fragmented roster where domestic integrators coexist with global platform vendors. Trend Micro leads indigenous suppliers, reporting record fiscal-2025 revenue of JPY 276 billion (USD 1.84 billion) and 58% platform annual-recurring-revenue growth as enterprises consolidate onto its XDR fabric. NEC strengthened its global reach by earning Cisco Gold Provider status and launching a Cyber Intelligence and Operation Center that applies cotomi generative AI to automate routine SOC triage, shrinking analyst burden. NTT DATA, ranked second worldwide in managed-security share, bolstered service depth via a Cortex-powered managed XDR partnership with Palo Alto Networks, giving clients unified visibility from cloud to edge.

International players fortify local presence by aligning with data-residency and sovereignty priorities. Palo Alto Networks expanded Japanese cloud infrastructure to host Prisma Access Browser, ensuring telemetry remains within domestic borders. Fortinet and CrowdStrike fused FortiGate firewalls with Falcon Insight XDR to blend network traffic inspection and AI-driven endpoint analytics, a bundle that resonates with hybrid-work architects seeking platform rationalization. IBM, Cisco, and Microsoft continue to sell SIEM modernization and zero-trust blueprints, but differentiators increasingly center on automated playbooks and sovereign hosting credentials.

White-space opportunities abound in OT-specific threat intelligence, machine-identity governance, and AI-agent security. Japan Cyber Defense’s USD 6.7 million seed round underscores investor appetite for homegrown XDR that embeds local language and regulatory tailoring from day one. Start-ups also target multi-tier distribution inefficiencies by offering direct SaaS procurement, a gambit that could compress channel markups if buyers overcome brand-trust inertia. The race to synthesize SOC telemetry with large language models is maturing rapidly, suggesting that the next competitive battleground will be who can operationalize AI without leaking customer data to offshore inference engines.

Japan Cybersecurity Industry Leaders

IBM Corporation

Cisco Systems Inc

Fortinet Inc.

F5, Inc.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Lockheed Martin and Fujitsu signed a memorandum of understanding to co-develop dual-use technologies covering quantum computing, edge sensing, and multi-domain network solutions.

- February 2026: Trend Micro published fiscal-2025 results, logging record revenue of JPY 276.0 billion (USD 1.84 billion) and 58% growth in platform annual recurring revenue.

- November 2025: Japan Cyber Defense secured JPY 1 billion (USD 6.7 million) in seed funding to build a sovereign, domestically hosted XDR platform.

- October 2025: NEC earned Cisco Gold Provider status, validating its capacity to deliver Cisco solutions worldwide.

Japan Cybersecurity Market Report Scope

Cybersecurity solutions help organizations detect, monitor, report, and counter cyber threats to maintain data confidentiality. The adoption of cybersecurity solutions is expected to grow in line with the rising internet penetration among developing and developed countries. The need for cybersecurity has increased as every system in today's world is connected to the Internet, making data more accessible to cybercriminals.

The Japan Cybersecurity Market Report is Segmented by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace Military and Defense, and Other End-use Industries), and End-User Enterprise Size (Large Enterprises, and Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| Endpoint Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| Endpoint Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the current size and projected growth of the Japan cybersecurity market?

The market is valued at USD 11.36 billion in 2026 and is forecast to reach USD 18.76 billion by 2031 at a 10.57% CAGR.

Which deployment mode is growing fastest in Japan?

Cloud-based controls are expanding at an 11.56% CAGR as enterprises shift workloads to hybrid and multi-cloud environments.

Why are Japanese SMEs accelerating cybersecurity spending?

Rising ransomware incidents and METI subsidies that reimburse up to 75% of eligible costs are pushing SMEs to adopt managed security services and SaaS-based platforms.

How are talent shortages influencing vendor strategies?

A deficit of about 110,000 professionals is driving automation and managed-service outsourcing, with platform vendors embedding AI to reduce analyst workload.

Which end-use industry will see the highest growth through 2031?

The information technology and telecommunications sector is projected to grow at a 12.12% CAGR as carriers secure 5G private networks and edge nodes.

What role do zero-trust mandates play in market demand?

Mandatory zero-trust guidelines for 14 critical-infrastructure sectors by 2026 are accelerating procurement of identity, micro-segmentation, and continuous-verification technologies.

Page last updated on: