Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

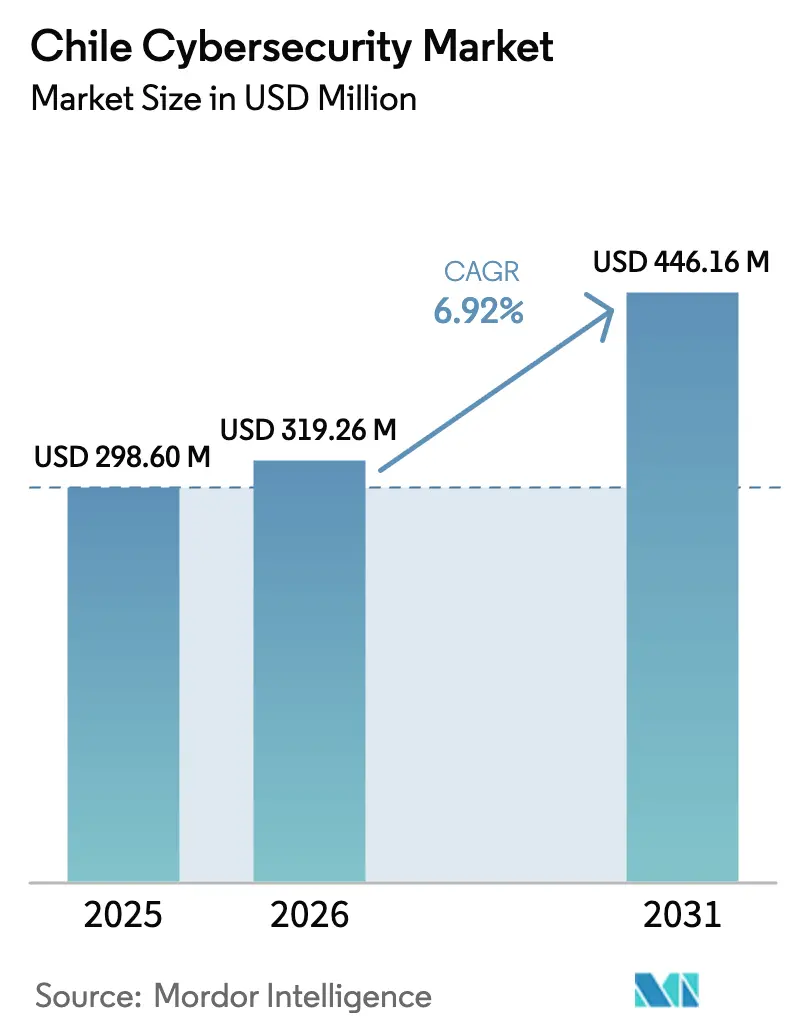

| Base Year Market Size (2025) | USD 298.6 Million |

| Market Size (2026) | USD 319.26 Million |

| Market Size (2031) | USD 446.16 Million |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

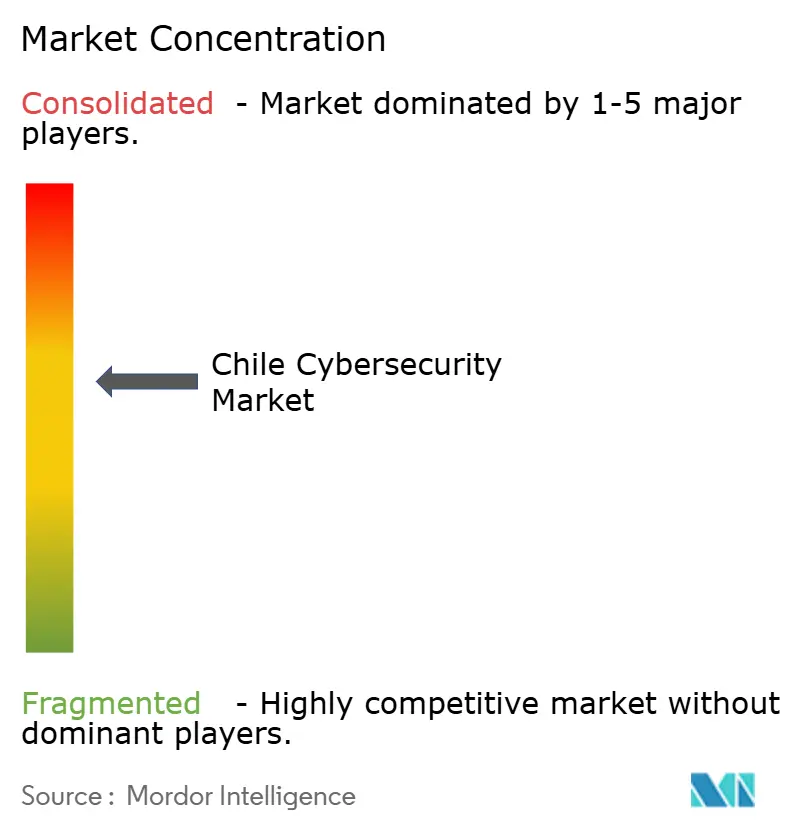

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Cybersecurity Market Analysis by Mordor Intelligence

The Chile cybersecurity market size was valued at USD 298.6 million in 2025 and estimated to grow from USD 319.26 million in 2026 to reach USD 446.16 million by 2031, at a CAGR of 6.92% during the forecast period (2026-2031). Local demand benefits from the Framework Law on Cybersecurity, effective January 2025, which created the National Cybersecurity Agency (ANCI) and introduced binding incident-reporting rules for critical infrastructure operators. Ongoing capital inflows—most visibly Amazon Web Services’ USD 4 billion cloud build-out scheduled for completion in 2026—are widening the threat surface yet simultaneously catalyzing greater spending on advanced controls. Enterprises are shifting from reactive endpoint tools toward platform-based, zero-trust architectures that integrate identity, network, and cloud security components. At the same time, skills shortages—Chile needs more than 15,000 trained practitioners by the end of 2025—are elevating the role of managed security services and driving vendor competition for automation-rich offerings. Collectively, these factors position the Chile cybersecurity market as the most structured and regulation-anchored ecosystem in Latin America.

Key Report Takeaways

- By offering, solutions retained 55.12% Chile cybersecurity market share in 2025, while the services segment is projected to grow 9.05% CAGR through 2031.

- By deployment mode, on-premise platforms commanded 55.20% of the Chile cybersecurity market size in 2025; cloud-based controls are forecast to post the fastest 8.62% CAGR to 2031.

- By end-user industry, BFSI led with a 28.20% revenue share in 2025, whereas healthcare is expected to exhibit the strongest 9.78% CAGR over the outlook period.

- By end-user enterprise size, large enterprises accounted for 62.85% of 2025 spending, but SMEs represent the quickest-expanding cohort at 9.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained Ransomware Surges Targeting Chilean BFSI and Retail Networks | +1.2% | National, with concentration in Santiago financial district | Short term (≤ 2 years) |

| 5G Roll-out and IoT Expansion Elevating Mobile and Edge-Node Attack Surfaces | +0.9% | National, with early deployment in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Digitization of Copper-Mining OT Environments Requiring ICS Protection | +0.8% | Northern regions (Antofagasta, Atacama), with spillover to central Chile | Medium term (2-4 years) |

| CORFO Cloud-Migration Subsidies Fueling SaaS Security Spend by Start-ups | +0.7% | National, with concentration in Santiago startup ecosystem | Short term (≤ 2 years) |

| AI Integration in Cybersecurity Solutions Driving Advanced Threat Detection | +0.6% | National, with early adoption in large enterprises | Long term (≥ 4 years) |

| New Data Protection Law Compliance Requirements Mandating Enhanced Security | +0.5% | National, affecting all sectors handling personal data | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustained Ransomware Surges Targeting Chilean BFSI and Retail Networks

Repeated ransomware incidents—highlighted by Banco Santander’s 2024 breach that exposed customer data in three countries—are reprioritizing spending toward automated detection and continuous response mechanisms. Financial institutions are consolidating siloed controls into unified security-information-and-event-management (SIEM) platforms that align with ANCI reporting windows. Retailers, whose omnichannel models gather vast payment records, now integrate threat-intelligence feeds directly into point-of-sale and e-commerce back-end systems to limit dwell time. Contract language is shifting toward outcome-based SLAs that benchmark incident-containment minutes rather than product features, creating a service-centric revenue lift across the Chile cybersecurity market. Taken together, ransomware forces organizations to treat zero-trust segmentation and immutable back-up architectures as board-level imperatives, accelerating the Chile cybersecurity market trajectory.

5G Roll-out and IoT Expansion Elevating Mobile and Edge-Node Attack Surfaces

Movistar Empresas’ LTE-M launch and other operator initiatives have multiplied connected endpoints across fleet-management and smart-city pilots. Private 5G deployments at Antofagasta’s mining sites illustrate how ultra-low-latency connectivity links OT sensors once kept offline, thereby extending adversaries’ reach into production environments. Security teams must now protect network slices, edge-compute clusters, and massive streaming datasets. Demand is shifting toward micro-segmentation gateways capable of inspecting machine-to-machine traffic at line speed. Vendors offering lightweight, container-based security agents capable of updating over-the-air are gaining adoption, especially where field crews operate hundreds of kilometres from network cores. Consequently, 5G’s rapid adoption contributes materially to Chile cybersecurity market growth in mid-term years.

Digitization of Copper-Mining OT Environments Requiring ICS Protection

Codelco’s alliance with ABB to cut emissions by integrating digital twins and autonomous hauling systems typifies mining’s rapid Industry 4.0 uptake. Because proprietary industrial protocols are now routable over IP networks, attackers can manipulate process-control logic to halt production. The Mining Cybersecurity Corporation—founded 2024 by Antofagasta and peers—shares threat telemetry to pre-empt such sabotage. Spending tilts toward anomaly-detection sensors that baseline vibration or voltage signatures rather than traditional file-centric antivirus software. Integration partners capable of certifying IEC 62443 compliance see heightened demand, adding volume to the Chile cybersecurity market, particularly for long-lifecycle contracts exceeding five years.

CORFO Cloud-Migration Subsidies Fueling SaaS Security Spend by Start-ups

Chile’s CORFO agency reimburses up to 50% of migration costs for early-stage companies that shift workloads to accredited domestic data centers [1]United Nations UNCTAD, “Chile National Data Centres Plan,” investmentpolicy.unctad.org. Subsidies free capital that start-ups channel into secure access service edge (SASE) subscriptions and cloud-native application-protection platforms. Because these firms are born-in-cloud, they sidestep legacy perimeter tools altogether, contributing to the fastest services growth slice in the Chile cybersecurity market. Yet compliance obligations introduced by the forthcoming Personal Data Protection Law task founders with embedding encryption-at-rest, data loss prevention, and continuous auditing from day one, expanding total addressable security spend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget Constraints Among Chilean SMEs Limiting Advanced Tool Uptake | -1.1% | National, with higher impact in regions outside Santiago | Short term (≤ 2 years) |

| Fragmented Legacy IT in Public Administration Slowing Zero-Trust Initiatives | -0.8% | National, affecting all government levels | Long term (≥ 4 years) |

| Low Cyber-Awareness Outside Santiago Hindering Nationwide Adoption | -0.6% | Regional, primarily affecting northern and southern provinces | Medium term (2-4 years) |

| Fragmented Vendor Landscape Increasing Implementation Complexity | -0.4% | National, affecting all organization sizes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints Among Chilean SMEs Limiting Advanced-Tool Uptake

Smaller enterprises generate 32% of national GDP yet rarely allocate more than 3% of IT budgets to security controls, leaving many reliant on open-source or freemium products [2]PLOS ONE Research Group, “Adoption of Open-Source Security in Latin-American SMEs,” plos.org. Limited in-house staff means patch cycles lag, raising exposure windows. Although CORFO credits defray some costs, license renewals and 24/7 monitoring remain prohibitive. MSSPs are responding with bundled offerings comprising endpoint, email, and cloud-gateway protection priced per user, but uptake is slowed where credit access is tight. The resulting protection gap suppresses overall Chile cybersecurity market CAGR in the near term.

Fragmented Legacy IT in Public Administration Slowing Zero-Trust Initiatives

Numerous municipal bodies still operate siloed data centers running decade-old applications developed under divergent standards. Integrating these into ANCI’s mandated zero-trust reference model requires asset discovery, identity federation, and extensive re-platforming. Budget allocations approved in 2025 earmark upgrades, yet procurement cycles spanning up to 18 months postpone meaningful deployments. Persistent heterogeneity therefore tempers Chile cybersecurity market velocity for the government vertical despite strong policy momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Accelerate Despite Solutions Dominance

Solutions commanded 55.12% of 2025 spending, underpinning perimeter firewalls, endpoint detection, and identity governance that large institutions deem non-negotiable. This foundation anchors the Chile cybersecurity market, yet tightening compliance timelines and continuous-monitoring demands are pushing service revenues higher. Consulting and incident-response engagements surged after the Santander breach, with many banks signing multiyear retainer contracts that guarantee one-hour remote support. Managed detection-and-response (MDR) adoption is also rising as enterprises seek 24/7 coverage while grappling with analyst shortages.

Professional-service providers are benefiting from new regulatory clauses that compel external audits at least annually. Demand for architecture reviews that align zero-trust and ISO 27001 requirements is notable among utilities and healthcare networks adopting electronic health records. Meanwhile, solution providers are embedding AI-driven analytics that reduce false positives, a capability often cited by buyers during request-for-proposal (RFP) scoring. The interplay of platform consolidation and service wraparounds sustains double-digit growth for the Chile cybersecurity market services layer.

By Deployment Mode: Cloud Gains Momentum Despite On-Premise Leadership

On-premise deployments kept 55.20% share in 2025, anchored by BFSI and mining customers that favor direct hardware control. These sectors routinely install redundant data halls in Santiago’s east side to ensure latency under 2 milliseconds to trading systems. Even so, hybrid architectures are proliferating: core banking systems remain on-site, while behavioral-analytics engines run in Amazon’s forthcoming local zones, a pattern reshaping the Chile cybersecurity market.

Cloud spending grows fastest where SaaS procurement sidesteps capex constraints. Subscription models permit SMEs to scale licenses monthly, and developers building fintech or telehealth applications now default to containerized workloads secured by cloud-native application-protection platforms. The new Personal Data Protection Law obliges data controllers to document encryption keys and audit trails; cloud dashboards simplify that evidence gathering. Hence cloud’s 8.62% CAGR is expected to lift its slice of the Chile cybersecurity market size to nearly parity with on-premise by decade’s end.

By End-User Industry: Healthcare Emerges as Growth Leader

BFSI retained 28.20% of 2025 outlays, a figure representing the largest Chile cybersecurity market share among verticals as banks comply with Basel III and ANCI’s 24-hour incident-reporting threshold. Spending priorities include real-time payment-fraud analytics and secure-access service edge for branch networks.

Healthcare, however, advances at the quickest 9.78% CAGR, fueled by telemedicine growth from 1.3 million virtual consults in 2024 to a projected 2.2 million in 2026. Hospitals now encrypt imaging archives and deploy identity federation across electronic record portals, channeling fresh budget into zero-trust shadow-IT discovery. Industrial firms follow, focusing on intrusion detection within supervisory control and data acquisition environments that manage copper-ore throughput, neutralizing threats that can halt conveyer belts.

By End-User Enterprise Size: SMEs Drive Future Growth

Large corporations consumed 62.85% of 2025 revenue, frequently operating multi-segment portfolios that include cloud, OT, and mobile assets. Their requirements stimulate demand for integrated extended-detection-and-response (XDR) platforms capable of correlating telemetry across thousands of endpoints.

Conversely, SMEs’ 9.35% CAGR springs from escalating ransomware incidents that threaten business continuity. Subsidized migration vouchers encourage cloud-native security stacks pre-integrated with identity, data-loss-prevention, and email scanning. MSSPs report a 34% jump in Chilean SME customers since the start of 2024, signalling durable tailwinds for the Chile cybersecurity market.

Geography Analysis

The Santiago Metropolitan Region anchors more than two-thirds of national revenues, leveraging 94.1% household internet penetration and fixed broadband speeds above 280 Mbps. Major banks, telcos, and government ministries cluster within a 10-kilometre radius, generating sustained demand for enterprise-grade SOC services that underpin the Chile cybersecurity market. Local universities, including the University of Chile, supply graduates to an expanding ecosystem of consulting firms, and a newly formed Cyber-Range at ANCI headquarters offers joint drills for public-private teams.

Northern regions such as Antofagasta and Atacama contribute an outsized share of OT security spending because copper-mining firms digitize haulage, smelting, and predictive-maintenance functions. Private 5G spectrum auctions facilitate remote-operation centers in Santiago that control mining trucks 1,200 kilometres away, necessitating encrypted back-haul and anomaly-detection gateways. These projects illustrate how industrial transformation sustains localized spikes in Chile cybersecurity market demand despite smaller overall population bases.

Southern provinces and smaller urban centers display lower uptake, impeded by fewer certified professionals and limited local reseller networks. The National Data Centers Plan pledges USD 2.5 billion to extend edge-compute facilities and close latency gaps, but until deployments complete after 2027, organizations outside the capital rely heavily on cloud services hosted in Santiago. ANCI has launched a mobile-training caravan that targets 50 municipalities per year, aiming to elevate baseline hygiene and thereby unlock further Chile cybersecurity market expansion in outlying areas.

Competitive Landscape

Global vendors account for a growing portion of contract value as enterprises consolidate toward one-stop platforms. Cisco’s security revenue climbed 117% year-on-year in FY2025 Q2, buoyed by uptake of its Secure Firewall 4200 line and AI-enriched Talos threat-intelligence feeds. Palo Alto Networks reported next-generation-security ARR of USD 4.8 billion, marking 37% growth and underscoring rising preference for platform bundles over point solutions [4]Palo Alto Networks, “Q2 FY2025 Investor Presentation,” paloaltonetworks.com. These results illustrate how scale players capture share across the Chile cybersecurity market.

Local specialists maintain strategic relevance through regulatory fluency and faster support cycles. NovaRed’s Chilean SOC handles more than 15,000 monthly alerts, with median triage time under five minutes according to the firm’s 2025 transparency report. iSentinel offers threat-hunting services mapped to ANCI notification forms, shortening compliance workloads for mid-tier banks. Such localization advantages ensure domestic firms remain credible alternatives, especially for public-sector tenders that favour local value creation.

Cloud-native entrants such as Cut Security exploit the pivot toward SaaS by offering agentless posture-management across AWS, Azure, and the newly announced Microsoft Chile Region. Their pay-as-you-grow models resonate with fintech and healthtech start-ups, intensifying price competition. As platformization progresses, acquisitions are likely; Stefanini Group already earmarked USD 100 million for Latin American cyber and AI targets to deepen its Chilean footprint. Overall, moderate consolidation juxtaposed with niche innovation defines the Chile cybersecurity market’s competitive dynamic.

Chile Cybersecurity Industry Leaders

Cisco Systems Inc.

Fortinet Inc.

Check Point Software Technologies Ltd.

Palo Alto Networks Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Microsoft opened its first Datacenter Region in Chile, providing in-country data residency and expanded security-compliance frameworks.

- March 2025: Stefanini Group announced plans to double Latin-American investment to more than USD 100 million over two years, prioritizing Chilean AI and cybersecurity acquisitions.

- January 2025: Chile’s Framework Law on Cybersecurity took effect, creating the National Cybersecurity Agency (ANCI) and a national CSIRT with mandatory incident-reporting mandates.

- August 2024: Genians highlighted its NAC-driven zero-trust capabilities at Deloitte Cyber Icon Chile, reflecting growing local appetite for network-access-control solutions.

Chile Cybersecurity Market Report Scope

Cybersecurity solutions assist an organization in monitoring, detecting, reporting, and countering cyber threats, which are internet-based attempts to damage or disrupt information systems and hack critical information using spyware and malware, and phishing. The market sizing estimation is based on end-user spending on cybersecurity solutions and services.

The Chile cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the current value of the Chile cybersecurity market?

The Chile cybersecurity market size is USD 319.26 million in 2026.

How fast is the market expected to grow through 2031?

Revenue is projected to rise at a 6.92% CAGR, reaching USD 446.16 million by 2031.

Which segment grows fastest within the market?

Cloud-deployed security solutions post the quickest 8.62% CAGR as organizations embrace hybrid and SaaS architectures.

Why is healthcare the fastest-expanding industry vertical?

Rapid telemedicine adoption and data-privacy mandates propel healthcare spending at a 9.78% CAGR.

Page last updated on: