Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

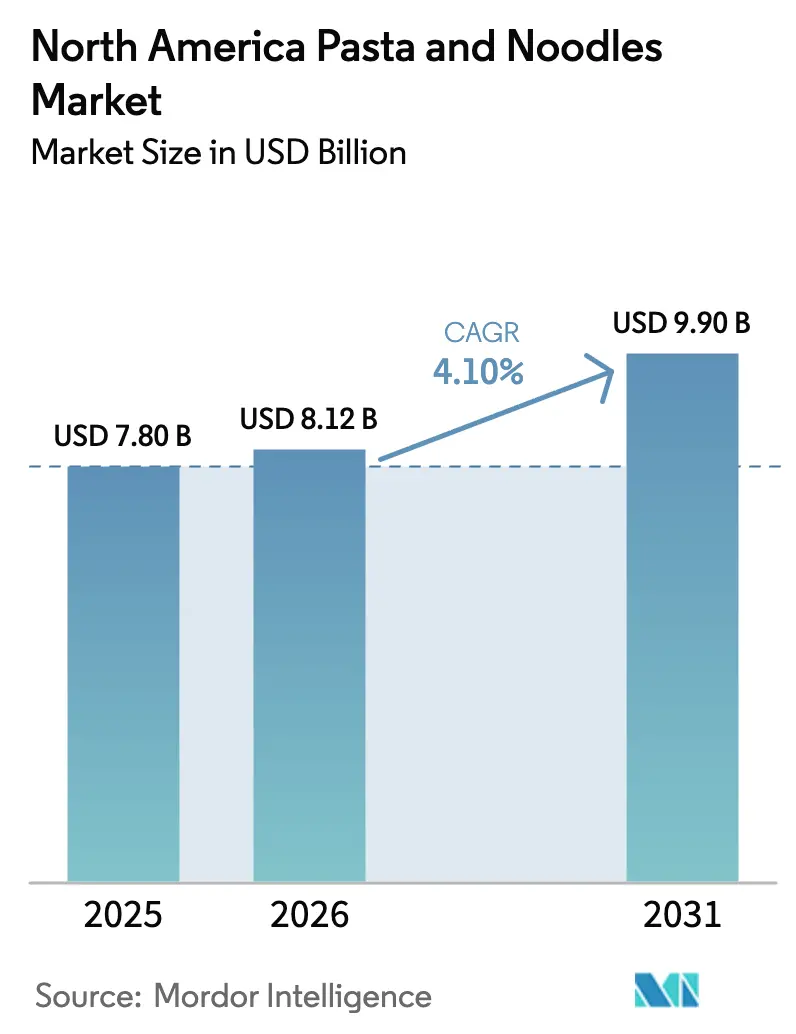

| Base Year Market Size (2025) | USD 7.80 Billion |

| Market Size (2026) | USD 8.12 Billion |

| Market Size (2031) | USD 9.9 Billion |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

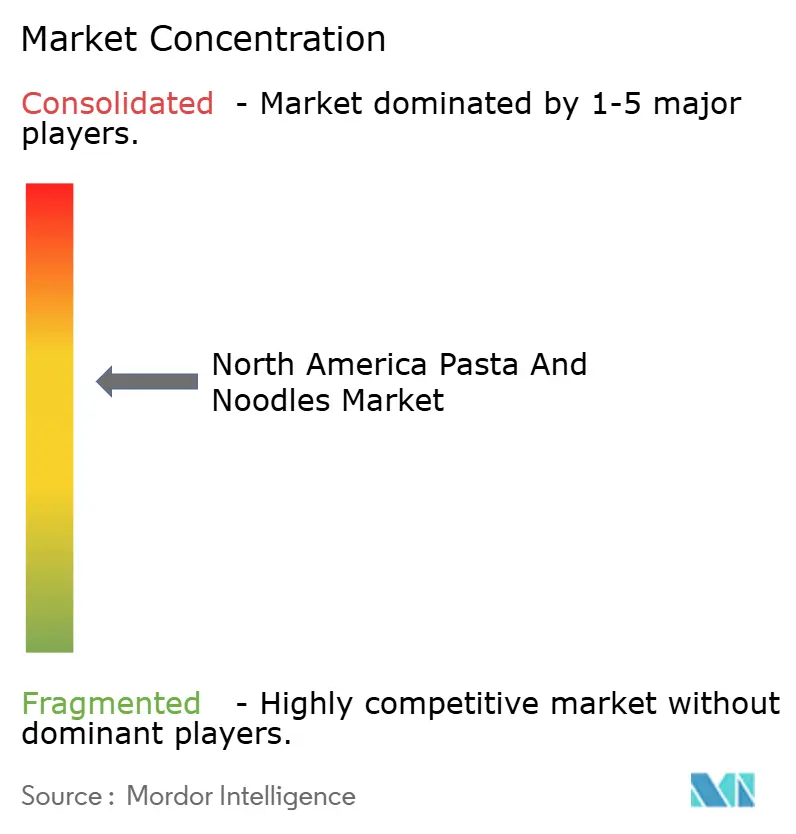

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Pasta And Noodles Market Analysis by Mordor Intelligence

North America pasta and noodles market size in 2026 is estimated at USD 8.12 billion, growing from 2025 value of USD 7.80 billion with 2031 projections showing USD 9.9 billion, growing at 4.1% CAGR over 2026-2031. This growth is primarily driven by consumers' increasing preference for quick and easy meal options, along with a rising demand for premium and high-quality products. Dried pasta continues to dominate the market, while gluten-free options are gaining popularity as more consumers seek healthier alternatives. The role of e-commerce is also growing significantly, enabling companies to deliver products directly to customers and expand their reach. The market is also witnessing a shift in ingredients, with traditional wheat-based products facing competition from alternatives like quinoa and chickpea-based pasta. Conventional products hold a significant share, but organic options are steadily gaining traction. Packaging trends are evolving as well, with companies adapting traditional formats to meet consumer demand for convenience and sustainability. The United States remains the largest market in terms of volume, while Canada is experiencing the fastest growth due to the increasing adoption of organic and clean-label products, which appeal to health-conscious consumers. The competitive landscape is balanced, with large multinational companies maintaining their dominance through economies of scale, while smaller, specialized brands are carving out niches in health-focused and innovative product segments.

Key Report Takeaways

- By product type, dried pasta held 67.10% of the North America pasta and noodles market share in 2025, while canned and frozen formats are forecast to expand at a 6.55% CAGR through 2031.

- By ingredient, wheat products accounted for a 56.20% share of the North America pasta and noodles market size in 2025; rice-based offerings are projected to grow at a 5.55% CAGR between 2026 and 2031.

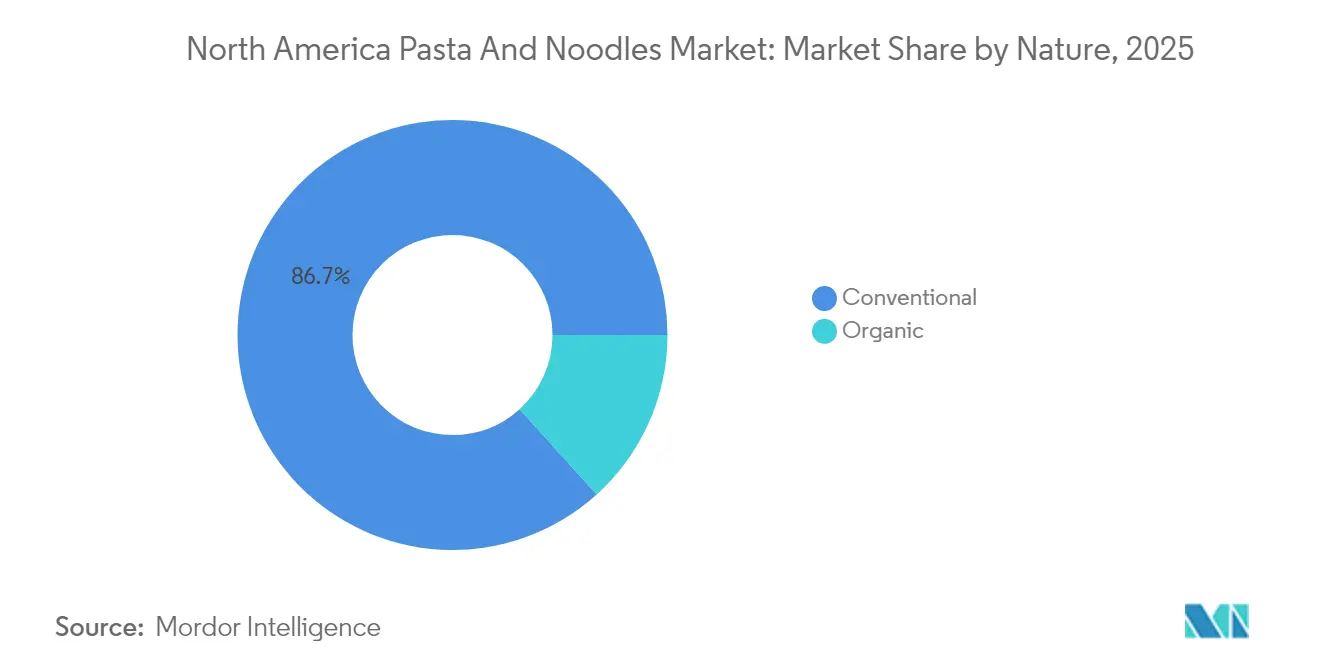

- By nature, conventional items controlled 86.70% of category revenue in 2025, whereas organic lines are pacing at a 6.18% CAGR to 2031.

- By packaging, packets/bags led with 62.10% share in 2025; cups/bowls are tracking a 5.62% CAGR through 2031.

- By distribution channel, supermarkets/hypermarkets captured 55.40% of sales in 2025, while online retail stores are poised to rise at a 6.42% CAGR through 2031.

- By country, United States controlled 74.10% revenue in 2025, whereas Canada is pacing at a 5.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Pasta And Noodles Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising consumption of convenience food | +1.2% | Strongest in United States urban centers | Medium term (2-4 years) |

| Increasing demand for gluten-free pasta and noodles | +0.8% | North America, premium segments | Long term (≥ 4 years) |

| Innovation and gourmet premiumization | +0.9% | United States and Canada metropolitan areas | Medium term (2-4 years) |

| Shift toward plant-based diets | +0.7% | North America, coastal regions | Long term (≥ 4 years) |

| Rising popularity of meal kits and ready meals | +0.6% | United States and Canada, suburban demographics | Short term (≤ 2 years) |

| Strong preference for clean-label ingredients | +0.5% | Educated consumer segments in United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumption of convenience food

The pasta and noodles market in North America is growing steadily, driven by the increasing demand for convenient and quick meal options. Many urban households, especially those with dual incomes, are looking for easy-to-prepare food that fits into their busy schedules. Pasta has become a staple, with a survey by the Share The Pasta Organization, revealing that 86% of respondents eat pasta at least once a week[1]Source: Share The Pasta Organization, "Pasta Facts," sharethepasta.org. This highlights how deeply pasta is integrated into everyday meals. Companies are introducing innovative products that enhance both convenience and enjoyment. For example, in 2024, Barilla launched a limited-edition pasta shape called 'Snowfall.' This unique pasta features intricate snowflake designs with poinsettia-like ridges and a heart at the center, symbolizing the brand’s tagline, 'A Sign of Love.' The product was designed to bring a sense of togetherness during the holiday season. Such creative offerings resonate with consumers, as nearly half of Americans have shown interest in fun and seasonal pasta shapes.

Shift toward plant-based diets

The increasing popularity of plant-based diets is influencing the North American pasta and noodles market as consumers are looking for healthier and nutritious options beyond traditional wheat-based products. Noodles made from lentils and chickpeas are gaining traction because they are high in protein. This trend aligns with the broader adoption of plant-based foods. According to the Good Food Institute, as of 2024, 53% of Americans have tried plant-based meat at some point, and 40% consumed it in the past year, indicating interest in plant-based alternatives[2]Source: Good Food Institute, "Plant Based Meat in the United States," gfi.org. In response to this demand, Veggiecraft relaunched its products nationwide in 2024 with improved recipes and updated packaging. Their offerings, such as Veggiecraft Zucchini Penne and Veggiecraft Sweet Potato Spaghetti, showcase innovation in plant-based pasta. Coastal states, in particular, are seeing higher adoption rates, which is helping the market diversify its ingredient options and cater to changing dietary preferences across the region.

Innovation and gourmet premiumization

The North American pasta and noodles market is undergoing significant changes, with consumers increasingly favoring innovative and premium options. For example, Barilla introduced chickpea spaghetti and chickpea orzo, priced at USD 2.99 and USD 3.49 respectively, to meet this growing demand. Companies are also adopting advanced production technologies, such as low-temperature extrusion, to improve product texture and consistency. Blockchain-enabled traceability is being used to ensure authenticity and enhance quality control and operational efficiency. These advancements help brands differentiate themselves in a competitive market. In May 2024, Maggi launched a new noodle line in the United States, featuring globally inspired flavors like Indian Classic Masala, Chinese Spicy Garlic, and Korean Spicy BBQ. This product line caters to the increasing demand for diverse flavors, particularly among younger consumers who are eager to try new and exciting culinary experiences.

Increasing demand for gluten-free pasta and noodles

The North American pasta and noodles market is experiencing a growing demand for gluten-free products, driven by both health concerns and changing consumer preferences. Around 0.75% of the United States population is estimated to have gluten intolerance, as per the World Population Review, as of 2025[3]Source: World Population Review, "Gluten Intolerance by Country 2025," worldpopulationreview.com. while many others are opting for gluten-free options due to perceived health benefits. To meet this demand, brands are introducing innovative products. For example, in August 2025, Banza launched a new gluten-free pasta line made from a blend of brown rice and chickpeas. This product, available at Whole Foods and other major retailers, aims to address common issues like texture and taste, which are often challenges for gluten-free alternatives. By focusing on quality and flavor, brands like Banza are making gluten-free pasta more appealing and accessible to a wider range of consumers, including those with dietary restrictions and those seeking healthier options.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Intense competition from alternatives | -0.9% | Strongest in health-conscious segments | Medium term (2-4 years) |

| Health concerns over refined carbs and sodium | -0.7% | North America, urban educated demographics | Long term (≥ 4 years) |

| Growing consumer shift toward low-carb / keto diets | -0.6% | United States and Canada, fitness-focused consumers | Medium term (2-4 years) |

| Climate-induced wheat supply volatility | -0.5% | Supply chain, regional price impacts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health concerns over refined carbs and sodium

Health concerns are becoming a significant factor affecting the North American pasta and noodles market, as more consumers prioritize whole-grain options and lower sodium levels to align with health recommendations. In August 2024, the United States' Food and Drug Administration (FDA) introduced draft guidelines for Phase II sodium reduction targets. These guidelines aim to reduce the average sodium intake from 3,400 mg/day to about 2,750 mg/day over 3 years. This effort is part of the FDA's broader initiative to lower sodium levels in processed, packaged, and prepared foods[4]Source: Food and Drug Administration, "Sodium Reduction in the Food Supply," fda.gov. In response, manufacturers are introducing healthier alternatives. For example, General Mills launched Carbe Diem pasta, which contains 55% fewer net carbs while maintaining the same texture as traditional pasta. Similarly, Fiber Gourmet offers high-fiber pasta options that cut calorie density by nearly half. However, these healthier products often come with higher price tags, making them less accessible to some consumers.

Intense competition from alternatives

The North American pasta and noodles market is encountering challenges due to rising competition from alternative meal options. Products such as ready-to-eat meals, frozen entrees, rice and grain substitutes, and plant-based noodles are becoming increasingly popular. These alternatives attract consumers by offering convenience, a variety of dietary choices, and unique flavors. Many of these options are also marketed as healthier or more affordable, while being quick and easy to prepare, making them appealing to busy or health-conscious individuals. This growing competition is pushing traditional pasta manufacturers to innovate and differentiate their products to stay relevant. The increasing availability of substitutes is not only dividing market share but also making it more difficult for conventional pasta products to maintain consumer loyalty and secure prominent shelf space in a highly competitive food industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shelf-Stable Dominance Faces Convenience Challenge

Dried pasta remains the leading segment in the North American pasta and noodles market, holding 67.10% of the total market share in 2025. Its popularity stems from its long shelf life, easy storage, and versatility, making it a staple in households. Consumers value dried pasta for its consistent quality, quick cooking time, and ability to be used in a wide range of dishes, from simple meals to elaborate recipes. Major brands continue to offer a variety of shapes and blends, catering to both traditional preferences and health-conscious trends. This segment’s dominance highlights its role as a dependable and convenient option for meal planning, maintaining its relevance despite shifting consumer preferences.

On the other hand, canned and frozen pasta products are gaining traction, with a projected CAGR of 6.55% through 2031, growing faster than the dried segment. These options appeal to consumers looking for convenience, as they eliminate the need for boiling and draining while offering precise portion control. This makes them ideal for smaller households or individuals seeking quick, ready-to-eat meals. Improved packaging technologies ensure freshness and flavor, making these products suitable for busy lifestyles. The rising demand for canned and frozen pasta reflects the needs of time-strapped urban consumers and dual-income families, who prioritize efficiency without sacrificing taste.

By Ingredient: Wheat Supremacy Challenged by Alternative Grains

Wheat-based pasta remains the most popular choice in the North American pasta and noodles market in 2025, accounting for 56.20% of the total market share. This dominance is due to the well-established infrastructure for wheat processing, affordable raw materials, and consumer trust in the quality and texture of semolina-based products. Wheat pasta is widely available in both retail stores and foodservice outlets, making it a convenient option for everyday meals. Its familiarity in traditional recipes and consistent quality from trusted brands further strengthen its position. Its versatility in various cuisines ensures it remains a staple in households across the region.

Rice-based pasta is steadily gaining popularity and is projected to grow at a CAGR of 5.55% from 2026 to 2031. This growth is driven by increasing demand from consumers with gluten sensitivities and a growing interest in Asian cuisine, where rice noodles are a key ingredient. Improvements in product quality, such as better texture and taste, along with wider availability in stores, are encouraging more consumers to try rice-based options. The rising awareness of gluten-free diets is also contributing to its growth. As a result, rice-based pasta is gradually expanding its market share, offering consumers more variety and catering to diverse dietary preferences.

By Nature: Conventional Scale Meets Organic Premiumization

Conventional pasta remained the leading segment in the North America pasta and noodles market in 2025, accounting for 86.70% of the total market share. This dominance is primarily due to the cost advantages of large-scale production facilities, which enable brands to offer competitive pricing. Conventional pasta is widely available across various retail channels, including supermarkets, hypermarkets, convenience stores, and online platforms. Established brands benefit from strong consumer trust and recognition, making conventional pasta the go-to choice for households looking for affordable and easily accessible meal options. Its long-standing presence in the market has solidified its position as a staple in many North American kitchens.

On the other hand, organic pasta is rapidly gaining traction as the fastest-growing segment, with a projected CAGR of 6.18% through 2031, significantly outpacing conventional pasta. Consumers are increasingly drawn to organic pasta due to its association with cleaner ingredients, USDA certification, and environmentally friendly farming practices. The rising focus on health and wellness, along with the growing demand for premium food products, is encouraging more people to try and repurchase organic options. As organic pasta becomes more widely available and the price difference compared to conventional pasta decreases, it is expected to secure a larger presence on store shelves across North America. This trend reflects a shift in consumer preferences toward healthier and more sustainable food choices.

By Packaging Type: Traditional Formats Adapt to Convenience Trends

Packets/bags were the most popular packaging format in 2025, making up 62.10% of the total volume in the North America pasta and noodles market. This format is widely preferred because it is affordable, easy to store, and readily available in supermarkets, club stores, and dollar stores. It is versatile and supports various product types, including dried pasta and instant noodles, making it a convenient choice for households. Many well-established brands rely on packets and bags for distribution, which has helped maintain their dominance in the market. Their ability to cater to both bulk purchases and everyday needs makes them a staple in pasta packaging.

On the other hand, cups/bowls are gaining popularity and are expected to grow at a faster rate, with a projected CAGR of 5.62% from 2026 to 2031. These packaging formats are particularly appealing to individuals with busy lifestyles, such as commuters, students, and smaller households, as they offer convenience, portion control, and quick preparation in just a few minutes. Innovations like improved insulation, recyclable materials, and premium flavor options are further driving their demand. As more people adopt on-the-go lifestyles, cups and bowls are likely to become a key growth area in the pasta and noodles market, offering a practical and modern solution for quick meals.

By Distribution Channel: Traditional Retail Faces Digital Disruption

Supermarkets/hypermarkets remained the leading sales channels for pasta and noodles in 2025, accounting for 55.40% of total revenue. These stores are popular because they offer a wide variety of products, including both regular and specialty options, all in one place. Shoppers often rely on them for their weekly grocery needs, and competitive pricing further attracts customers. Their strong supply chains ensure that essential items like pasta are always available on shelves. For many families in North America, supermarkets and hypermarkets are the most convenient and reliable places to shop for pasta and noodles.

On the other hand, online retail is growing rapidly and is expected to be the fastest-expanding distribution channel, with a projected CAGR of 6.42% through 2031. This growth is fueled by the increasing popularity of subscription services for pantry staples, partnerships with meal-kit companies, and greater consumer confidence in the safe delivery of groceries. Online platforms also provide access to unique, premium, and international pasta varieties, catering to a broader range of preferences. As more consumers prioritize convenience and adopt digital shopping habits, online sales are expected to steadily gain market share while complementing the dominance of physical stores.

Geography Analysis

The United States accounted for 74.10% of the market volume in 2025, driven by its large and diverse consumer base, strong Italian-American food culture, and widespread retail availability. Urban consumers prefer quick and convenient options like instant, microwaveable pasta bowls, while suburban families often opt for larger bulk packages. Coastal states are leading the way in adopting plant-based and organic pasta varieties, which often set trends that gradually spread to other regions. This layered demand highlights the varied preferences across different demographics and regions within the country, making the United States a dominant player in the North American pasta and noodles market.

Canada is the fastest-growing market in the region, with a projected compound annual growth rate (CAGR) of 5.60% through 2031. The country’s growing immigrant population is introducing a wider variety of culinary preferences, increasing the popularity of both wheat and rice noodles. Canada’s alignment with the United States Department of Agriculture organic standards has simplified cross-border trade, enabling brands to use United States manufacturing capabilities while customizing products for Canadian consumers. A mix of domestic and imported brands, such as Italpasta and other international options, are expanding choices for Canadian shoppers.

Mexico and other parts of North America present additional growth opportunities, supported by stable tariffs under the United States-Mexico-Canada Agreement. In southern markets, wheat-based pasta remains a staple, but rising disposable incomes and exposure to international cuisines are encouraging consumers to try gourmet and gluten-free options. Adapting to local preferences, such as offering region-specific sauce flavors and varying package sizes, is essential for brands to succeed in these culturally diverse markets. This focus on localization is helping companies tap into the growing demand for pasta and noodles across the region, particularly in areas with distinct culinary traditions.

Competitive Landscape

The North America pasta and noodles market is moderately concentrated, with major players like Barilla Holding SpA, Nestlé SA and Campbell Soup Company competing against emerging brands such as Banza and Jovial Foods. Large multinational companies maintain a competitive edge through cost advantages, vertical integration, and extensive brand portfolios. On the other hand, smaller specialty brands are gaining traction by offering unique products made from chickpea or lentil flour, promoting clean-label claims, and utilizing direct-to-consumer sales models. These strategies allow smaller players to build loyal customer bases within specific niches of the market.

Investments in technology are playing a significant role in shaping the market. For instance, Barilla has adopted AI-based optical sorting technology to detect surface defects, reducing waste and enhancing its premium product image. In late 2024, Winland Foods acquired Philadelphia Macaroni Company for USD 495 million, expanding its production capacity on the East Coast and strengthening its relationships with restaurant suppliers. Similarly, Colavita’s acquisition of Vitelli Foods in 2025 helped the company reinforce its authentic Italian-origin branding while increasing its distribution reach in the Northeast region.

Innovation in the market is focused on addressing emerging consumer needs and sustainability trends. Companies are exploring protein-fortified pasta bowls designed for Glucagon Like Peptide (GLP-1) medication users, developing packaging made from recycled materials, and implementing blockchain technology to ensure traceability of durum wheat. These advancements highlight the dynamic nature of competition in the North America pasta and noodles market, as companies strive to meet evolving consumer preferences and differentiate themselves in a crowded marketplace.

North America Pasta And Noodles Industry Leaders

-

Nissin Foods Holdings Co., Ltd.

-

Barilla Holding SpA

-

Ebro Foods SA

-

Campbell Soup Company

-

Nestlé SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Banza expanded its pasta portfolio by launching Brown Rice Pasta. This new product, which combined brown rice with Banza’s signature chickpeas, aimed to address two key challenges for gluten-free consumers: delivering exceptional flavor and maintaining texture even the next day.

- May 2025: Nestlé-owned seasonings, instant soups, and noodles brand, Maggi, expanded its presence in the United States market with the launch of Maggi Noodles. This initiative aimed to cater to the increasing demand for bold flavors and fusion cuisine.

- January 2025: Barilla announced the limited-edition launch of Barilla Love Pasta, a product designed to celebrate love in all its forms. The heart-shaped pasta aimed to provide Canadians with a unique way to create meaningful dining experiences.

- December 2023: Nissin Foods, the maker of Cup Noodles and Top Ramen, launched the Hot & Spicy Fire Wok packets in two flavors: Torched Teriyaki Chicken and Screamin' Sichuan Beef. The packets come with a square ramen pack containing spicy noodles infused with chili flakes.

North America Pasta And Noodles Market Report Scope

Noodles and pasta are types of food made from unleavened dough, which is rolled flat and cut, stretched, or extruded into long strips or strings. The North American pasta and noodles market is segmented by form, distribution channel, and geography. By form, the market is segmented into ambient/canned, dried, and chilled/frozen. By distribution channel, the market studied is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. By geography, the market studied is segmented into the United States, Canada, Mexico, and Rest of North America. The market size is done in terms of value (USD) for these segments.

By Product Type

| Dried |

| Instant |

| Canned and Frozen |

By Ingredient

| Rice |

| Corn |

| Millet |

| Wheat |

| Other Ingredients |

By Nature

| Conventional |

| Organic |

By Packaging Type

| Packets/Bags |

| Cups/Bowls |

| Boxes |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Channels |

By Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Dried |

| Instant | |

| Canned and Frozen | |

| By Ingredient | Rice |

| Corn | |

| Millet | |

| Wheat | |

| Other Ingredients | |

| By Nature | Conventional |

| Organic | |

| By Packaging Type | Packets/Bags |

| Cups/Bowls | |

| Boxes | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Channels | |

| By Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North America pasta and noodles market in 2026?

The North America pasta and noodles market size is USD 8.12 billion in 2026, with a projected value of USD 9.9 billion by 2031.

Which product segment expands the fastest through 2031?

Canned and frozen alternatives post the strongest growth at a 6.55% CAGR because they deliver heat-and-eat convenience.

Why are legume-based noodles gaining popularity?

Chickpea, lentil, and pea flours supply extra protein and align with plant-based diets, making them attractive to health-conscious buyers.

What drives online pasta sales in North America?

Direct-to-consumer bundles, meal-kit subscriptions, and wider SKU availability fuel a 6.42% CAGR for online retail channels.

Page last updated on: