Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

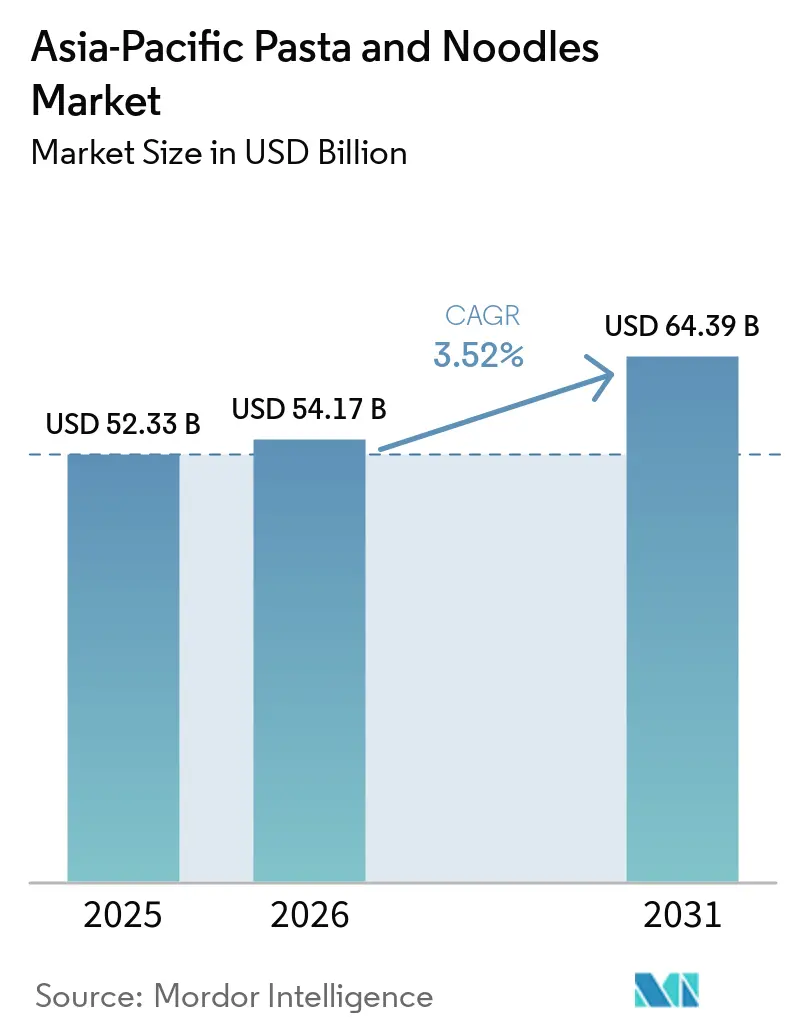

| Base Year Market Size (2025) | USD 52.33 Billion |

| Market Size (2026) | USD 54.17 Billion |

| Market Size (2031) | USD 64.39 Billion |

| Growth Rate (2026 - 2031) | 3.52% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Pasta And Noodles Market Analysis by Mordor Intelligence

The Asia-Pacific pasta and noodles market size in 2026 is estimated at USD 54.17 billion, growing from 2025 value of USD 52.33 billion with 2031 projections showing USD 64.39 billion, growing at 3.52% CAGR over 2026-2031. The market growth stems from traditional dietary preferences and changing consumer lifestyles across the region. Noodles maintain market dominance, particularly in China, Japan, South Korea, India, and Indonesia, due to their affordability, convenience, and cultural importance. The increasing influence of Western diets, higher disposable incomes, and urbanization has increased pasta demand, especially among younger, health-conscious consumers and working professionals seeking quick, nutritious meals. The market expansion is supported by e-commerce growth, retail development, and marketing initiatives from global and regional manufacturers. The increasing interest in international cuisines and demand for ready-to-eat and convenience foods in the post-pandemic period are shaping market competition. These factors are driving the evolution of the Asia-Pacific noodles and pasta market, which combines traditional and contemporary consumer preferences.

Key Report Takeaways

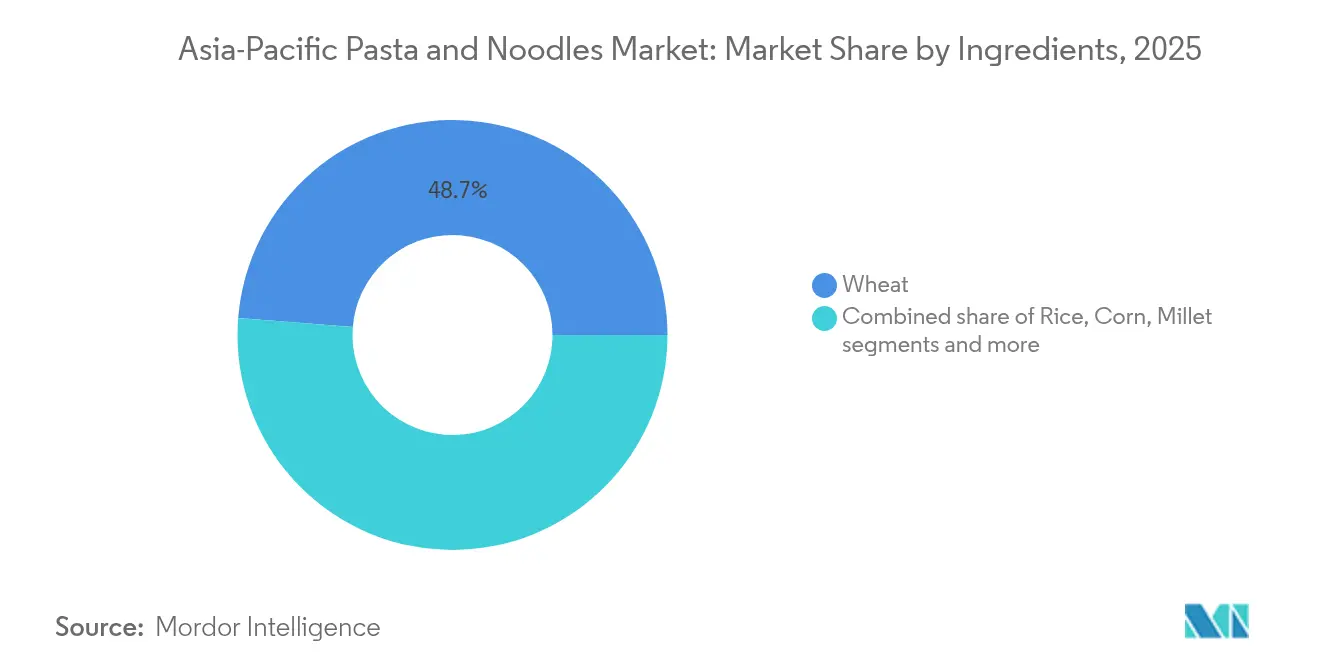

- By ingredient, wheat dominated with a 48.74% share of the Asia-Pacific pasta and noodles market in 2025, while the millets segment is expected to grow at a 3.97% CAGR through 2031.

- By product type, dried formats held 73.15% of the Asia-Pacific pasta and noodles market share in 2025; canned and frozen variants are projected to grow at a 4.25% CAGR through 2031.

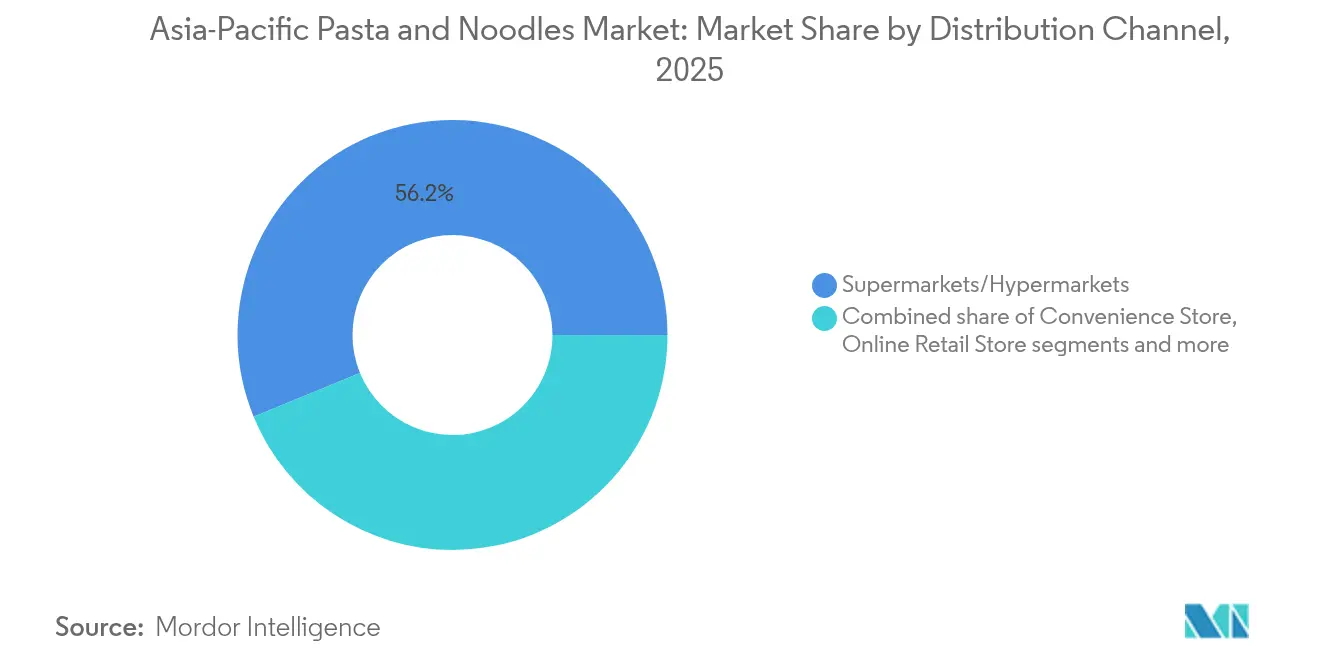

- By distribution channel, supermarkets/hypermarkets secured 56.20% revenue share in 2025, while online retail is poised for the fastest 5.33% CAGR to 2031.

- By geography, China controlled 40.10% of the Asia-Pacific pasta and noodles market share in 2025; India is forecast to grow at a 4.82% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Pasta And Noodles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased preference for international cuisine among urban consumer | +0.9% | China, India, Australia, Japan | Medium term (2-4 years) |

| Rising popularity of millet-based noodles/pasta | +0.6% | India, China, Rest of Asia-Pacific | Long term (≥ 4 years) |

| Demand for affordable, ready-to-eat food options | +0.8% | Asia-Pacific region, particularly China, India | Short term (≤ 2 years) |

| Government support accelerates millet-based product development | +0.5% | India, China, Rest of Asia-Pacific | Medium term (2-4 years) |

| Manufacturing advances enhance product quality | +0.4% | Japan, China, Australia, India | Medium term (2-4 years) |

| Retail and e-commerce expansion improves product reach | +0.7% | Asia-Pacific region, particularly urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increased Preference for International Cuisine Among Urban Consumer

Consumer preferences in urban Asian markets have evolved significantly, influencing the noodles and pasta market as international cuisines gain popularity beyond traditional consumption patterns. This market transformation is evident in metropolitan areas of China, India, and Australia, where higher disposable incomes and exposure to global food trends drive the adoption of Italian, Mediterranean, and fusion cuisines. The shift has created opportunities in the premium segment for authentic international products. This change reflects broader lifestyle modifications, with pasta becoming a staple in middle-class household meals. In 2024, China consumed approximately 43,802 million servings of instant noodles, according to the World Instant Noodles Association (WINA), demonstrating strong demand in this category [1]Source: World Instant Noodles Association (WINA), "Demand Rankings", instantnoodles.org. These factors contribute to a dual growth trajectory in the Asia-Pacific noodles and pasta market.

Rising Popularity of Millet-Based Noodles/Pasta

Millet integration is transforming the Asia-Pacific noodles and pasta market as consumers actively seek healthier, sustainable, and culturally significant products. Major food manufacturers in India and China now incorporate millets as premium ingredients in their noodle and pasta products, responding to this market shift. These ancient grains provide superior nutritional benefits, containing 10-12% protein content and maintaining a lower glycemic index compared to wheat-based alternatives. The diabetic population in the Asia-Pacific region particularly benefits from these millet-based products due to their blood sugar management properties. Food companies are accelerating their product development efforts to capture this growing market opportunity. ITC Limited demonstrates this trend through its comprehensive millet program launched in January 2023, which introduced various millet-based products, including noodles, pasta, dosa mix, and idli mix. The company's initiative reflects the broader industry movement toward incorporating traditional grains into modern food products while meeting consumer demands for healthier alternatives.

Demand for Affordable, Ready-to-Eat Food Options

Consumers across Asia-Pacific increasingly choose affordable ready-to-eat (RTE) pasta and noodles to match their fast-paced urban lifestyles. Working professionals, dual-income families, and time-pressed urban residents actively seek quick and satisfying meal solutions. Instant and semi-cooked noodles and pasta products offer this perfect balance of convenience and taste. These products appeal to consumers across all income groups, particularly in busy cities where traditional cooking demands significant time investment. Nuclear families, students, and migrant workers in India, Vietnam, and Indonesia regularly rely on these convenient meal options. Urban residents, especially in cities like Thailand, where traffic congestion limits cooking time, depend on these quick meal solutions. The USDA Foreign Agricultural Service confirms this trend, reporting that Thailand's retail food industry has reached USD 5.1 billion in 2023, as consumers actively purchase convenient and packaged food items [2]Source: United States Department of Agriculture (USDA), "Retail Foods Annual", usda.gov.

Government Support Accelerates Millet-Based Product Development

The governments across Asia-Pacific are actively implementing initiatives and providing institutional support to transform the noodles and pasta market. These initiatives focus on encouraging farmers to cultivate millets and helping manufacturers develop millet-based products. India leads this transformation through specific policies, particularly by designating millets as "nutri-cereals" and successfully advocating for the United Nations to declare 2023 as the International Year of Millets. The Ministry of Food Processing Industries actively supports this transition through various programs. The government's Pradhan Mantri Kisan Sampada Yojana directly supports food processing companies by offering capital subsidies between 35%-50% for developing millet-based products. Additionally, the government has established dedicated research and development centers that develop new millet processing techniques and create commercial formulations for pasta and noodles, which helps strengthen every step from millet farming to finished products reaching consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over MSG, sodium, and additives in packaged noodles and pasta | -0.4% | Japan, Australia, China, India | Medium term (2-4 years) |

| Varying food safety standards across Asia-Pacific countries | -0.3% | Asia-Pacific region, particularly developing markets | Long term (≥ 4 years) |

| Diverse food safety regulations create compliance issues | -0.2% | Asia-Pacific region, cross-border operations | Long term (≥ 4 years) |

| Traditional rice-based meal preferences limit pasta adoption | -0.3% | Southeast Asia, rural Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over MSG, Sodium, and Additives in Packaged Noodles and Pasta

The growing health consciousness among consumers presents a significant challenge to the Asia-Pacific noodles and pasta market. Increased awareness about nutritional content, particularly regarding high sodium levels, monosodium glutamate (MSG), and artificial preservatives, has led to increased scrutiny of conventional instant noodles and processed pasta products. This trend is particularly evident in developed markets like Japan and Australia, where consumers demand transparent food labeling and prefer low-sodium, preservative-free, and nutritionally balanced options. The impact of health awareness extends to emerging urban markets in China and India, where dietary education and wellness-focused purchasing decisions are becoming more prevalent among middle-class consumers. Government regulations are also evolving to address these health concerns. For instance, Malaysia's Salt Reduction Strategy requires manufacturers to meet specific sodium reduction targets for processed foods, including instant noodles, by 2025. These regulatory requirements create operational challenges for manufacturers, who must reformulate products while maintaining taste and shelf life, often requiring significant investment.

Varying Food Safety Standards Across Asia-Pacific Countries

The Asia-Pacific pasta and noodles market faces significant growth constraints due to complex regulatory frameworks across multiple jurisdictions. Manufacturers encounter stringent compliance requirements, as countries implement distinct standards for ingredients, processing methods, and product labeling, which substantially increase operational costs and reduce manufacturing efficiency. Companies operating in the region must continuously modify their product formulations to align with diverse market-specific requirements. The implementation of Indonesia's mandatory halal certification in October 2024 exemplifies these regulatory pressures, imposing additional compliance obligations and ingredient restrictions on manufacturers. The 2025 National Trade Estimate Report identifies substantial technical barriers and sanitary measures that impede food exports across the region. Furthermore, food safety incidents in any single market can significantly impact a manufacturer's credibility throughout the Asia-Pacific region, necessitating comprehensive regulatory adherence to maintain market position and consumer trust.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredients: Wheat Dominates While Alternatives Gain Momentum

In 2025, wheat commands a dominant 48.74% share of the Asia-Pacific noodles and pasta market, underpinned by its versatility and a well-established manufacturing base. This wheat dominance is especially pronounced in China and Japan, where wheat-based noodles play a pivotal role in traditional dishes. Meanwhile, millet-based products are on an upward trajectory, with a projected CAGR of 3.97% from 2026 to 2031, as manufacturers tap into their nutritional advantages and resilience to climate variations.

Rice noodles enjoy robust market traction, particularly in Southeast Asia, and are witnessing a surge in global demand, fueled by a growing appetite for gluten-free options and the rising allure of Asian cuisine. Innovations, like seaweed-enhanced formulations, are propelling the "Other Ingredients" segment, boosting both nutritional value and sustainability. Corn-based alternatives continue to see steady demand, especially in the gluten-free arena. The market is also witnessing a rise in hybrid formulations, with manufacturers crafting ingredient blends that optimize nutrition, texture, and production efficiency.

By Product Type: Dried Products Lead While Canned and Frozen Segment Accelerates

In the Asia-Pacific noodles and pasta market, the dried product segment maintains a commanding 73.15% market share in 2025. This market leadership position is attributed to the segment's inherent advantages in product longevity, logistical efficiency in distribution networks, and established consumer acceptance throughout the region. The segment encompasses both traditional Asian noodle variants and Western pasta products, with dried instant noodles representing a significant market component.

The instant noodle category demonstrates market advancement through strategic premiumization initiatives, with manufacturers implementing sophisticated product development protocols. These include the integration of premium-grade ingredients and enhanced flavor formulations to address the requirements of price-sensitive yet quality-conscious consumers. The canned and frozen segment projects substantial growth opportunities, with an anticipated CAGR of 4.25% during 2026-2031, primarily attributed to progressive urbanization patterns and systematic improvements in cold chain infrastructure across developing market territories.

By Sales Channel: Supermarkets and Hypermarkets Lead While E-commerce Disrupts

Supermarkets and hypermarkets dominate noodles and pasta distribution in the Asia-Pacific region, accounting for 56.20% market share in 2025. These retailers excel through comprehensive product ranges and in-store product examination opportunities. The format shows particular strength in developed markets like Japan and Australia, where organized retail has high penetration. The online retail segment is growing at a projected CAGR of 5.33% during 2026-2031, reshaping traditional distribution methods. In the Philippines, food and beverage retailers generated sales of USD 36 billion in 2024, with modern retail formats expanding their footprint .

Convenience stores remain influential, particularly in urban areas where space constraints and consumer mobility drive demand for compact retail formats. In Japan, these stores function as primary neighborhood food outlets. The "Other Sales Channel" category, including institutional buyers and food service operators, manages significant volume, especially in basic pasta and noodle products. Retailers are adapting through omnichannel strategies, using physical stores as fulfillment centers for online orders. Digital platforms provide market access opportunities for smaller, innovative brands that face challenges securing shelf space in traditional retail channels.

Geography Analysis

China holds a 40.10% share of the Asia-Pacific pasta and noodles market in 2025, supported by its large population and established noodle consumption culture. The market shows strong premiumization trends, particularly in tier-one cities, where consumers seek higher-quality ingredients and international pasta varieties alongside traditional Chinese noodles. The market features product innovations incorporating traditional Chinese medicine concepts into noodle formulations. China's extensive manufacturing infrastructure enables efficient production and distribution, despite challenges from increasing raw material costs and growing health awareness.

India emerges as the region's fastest-growing market with a projected CAGR of 4.82% from 2026-2031. This growth stems from urbanization, higher disposable incomes, and changing dietary habits. Government initiatives supporting millet-based products are driving innovation in healthier noodle and pasta alternatives. The expansion of e-commerce, especially in urban areas, provides new distribution channels for established and emerging brands. India's large youth population, increasingly receptive to international cuisines and convenience foods, further strengthens market growth potential.

Japan's market emphasizes quality, authenticity, and health-conscious offerings. Product development focuses on functional food attributes and premium variants to meet consumer demands. The competitive landscape drives continuous innovation among major manufacturers. The aging population influences product development, with emphasis on nutritional content and digestibility. Australia and other Asia-Pacific regions maintain distinct market characteristics based on local food traditions and economic conditions.

Competitive Landscape

The Asia-Pacific pasta and noodles market demonstrates moderate fragmentation, characterized by strategic competition between established multinational corporations and regional manufacturers. Regional players maintain significant market presence through their established distribution networks, deep understanding of local consumer preferences, and long-standing customer relationships. The competitive landscape includes prominent industry leaders such as Nestlé S.A., Unilever PLC, Nissin Foods Holdings Co. Ltd., Samyang Foods Inc., and ITC Limited.

The market presents substantial opportunities in developing integrated product solutions that combine convenience with nutritional benefits, addressing a notable gap in current market offerings. This market opportunity has attracted new market entrants, particularly in the direct-to-consumer segment, where digital-first brands leverage e-commerce platforms to establish direct consumer relationships. Companies are establishing competitive advantages through strategic technological investments, implementing advanced processing methodologies that maintain nutritional integrity and extend product shelf life without artificial preservation methods.

Market participants are increasingly focusing on vertical integration strategies to strengthen their supply chain control and enhance operational efficiency. Companies are also expanding their product portfolios through strategic acquisitions and partnerships, particularly in emerging markets where local brands hold significant market share. Additionally, manufacturers are investing in research and development to introduce innovative packaging solutions and sustainable production practices, responding to growing consumer demand for environmentally responsible products.

Asia-Pacific Pasta And Noodles Industry Leaders

-

Nestlé S.A.

-

Unilever PLC

-

Nissin Foods Holdings Co. Ltd.

-

Samyang Foods Inc.

-

ITC Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Haraku Ramen Halal, an Indonesian noodle brand under the Ismaya Group, has introduced The One Noodle, a limited-edition product specifically designed for gamers. Featuring a thicker texture for improved flavor absorption, it enables players to remain fully engaged in their gameplay without interruptions.

- December 2024: Samyang Foods, the South Korean food company known for its instant noodles, has announced the establishment of its first overseas factory in China to meet the increasing demand for spicy noodles.

- November 2024: Nissin Foods Company and Nissin Asia have established a joint venture, Australia Nissin Foods Pty., Ltd., to expand their instant noodle and snack market presence in Australia and New Zealand. The venture focuses on developing a distribution network for importing and selling instant noodles and food products.

- October 2024: WokTok by Veeba expanded its product portfolio with new Chinese sauces and instant noodles. The company introduced instant cup noodles in five variants: Chowmein, Manchurian, Masala, Kung Pao, and Spicy Korean 1X. The noodles are manufactured without refined flour (maida), palm oil, or monosodium glutamate (MSG).

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Asia-Pacific pasta and noodles market as all packaged dried, instant, chilled, frozen, and canned pasta or noodle products that reach retail or foodservice shelves in China, India, Japan, Australia, and the rest of the region. Products made from wheat, rice, corn, millet, and other grains are included because shoppers treat them as direct substitutes when choosing quick-cook staples.

Scope exclusion: freshly prepared, unpackaged items produced in restaurants or household kitchens do not enter our sales model.

Segmentation Overview

-

By Ingredients

- Rice

- Corn

- Millet

- Wheat

- Other Ingredients

-

By Product Type

- Dried

- Instant

- Canned and Frozen

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Store

- Online Retail Stores

- Other Distribution Channel

-

By Geography

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We validate desk estimates through structured interviews and short surveys with procurement managers at large supermarket chains, noodle plant engineers in China and Vietnam, packaging film suppliers, and nutrition academics tracking sodium-reduction rules. These conversations help us gauge real consumption shifts, promotional intensity, and likely channel-wise sell-through across urban and semi-urban catchments.

Desk Research

Mordor analysts first map the value pool with public datasets such as FAO production statistics, UN Comtrade shipment lines, the World Instant Noodles Association's country sales briefs, national consumer price series from the Reserve Bank of Australia and the Reserve Bank of India, and health ministry import alerts that influence ingredient flows. Company filings, investor decks, and quarterly earnings transcripts enrich the channel mix and average selling price checks, while paid interfaces like D&B Hoovers and Dow Jones Factiva flag revenue breakouts for leading branded players. Many additional open data feeds and trade journals are consulted; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down build starts with retail scanner sales, domestic production, and net trade to reconstruct apparent consumption, followed by selective bottom-up roll-ups of branded manufacturer revenues and sampled price-per-kilogram data to fine-tune totals. Key model drivers include per-capita wheat and rice intake, urbanization rate, e-commerce share in packaged foods, wheat futures prices, and government fortification mandates. Forecasts apply multivariate regression, feeding the above variables into an autoregressive trend to 2030, while scenario analysis adjusts for raw-material shocks. Where bottom-up checks deviate beyond three percent, assumptions are revisited with fresh store-check or customs inputs before locking the baseline.

Data Validation & Update Cycle

Outputs pass a double-analyst variance screen, after which senior reviewers probe anomalies against independent signals such as wholesale flour quotes and shipping container rates. Reports refresh each year; mid-cycle events, regulatory bans, plant shutdowns, or currency swings trigger an ad-hoc recalibration so clients always receive the latest view.

Why Mordor's Asia-Pacific Pasta And Noodles Baseline Commands Reliability

Published figures often vary because firms pick different product mixes, rely on incomplete retail trackers, or apply single-factor growth rates.

By aligning scope with on-shelf reality and blending market-specific variables with two-track modeling, Mordor Intelligence delivers a balanced, reproducible baseline buyers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 52.33 B (2025) | Mordor Intelligence | - |

| USD 48.47 B (2021) | Regional Consultancy A | historical base year carried forward with straight-line CAGR |

| USD 44.33 B (2022) | Trade Journal B | retail-only scope; excludes foodservice |

| USD 44.20 B (2024) | Global Consultancy C | treats pasta share of mixed rice-pasta packs as rice sales |

Differences show how start year choice, channel coverage, and product definitions swing totals. By updating annually, validating with dual lenses, and documenting every assumption, we ensure our Asia-Pacific pasta and noodles numbers remain the dependable reference for strategic decisions.

Key Questions Answered in the Report

What is the current size of the Asia-Pacific pasta and noodles market?

The market stands at USD 54.17 billion in 2026, with a 3.52% CAGR projected through 2031.

Which country holds the largest share of Asia-Pacific pasta and noodles market?

China leads with 40.10% share as of 2025, driven by entrenched noodle culture and extensive manufacturing scale.

Why are millet-based noodles and pasta gaining traction?

Millets offer higher protein and lower glycaemic index than wheat, aligning with health agendas and benefiting from strong government support in India and China.

Which sales channel is expanding fastest?

Online retail shows the highest 5.33% CAGR forecast to 2031, propelled by mobile commerce and omnichannel fulfilment.

Page last updated on: