Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

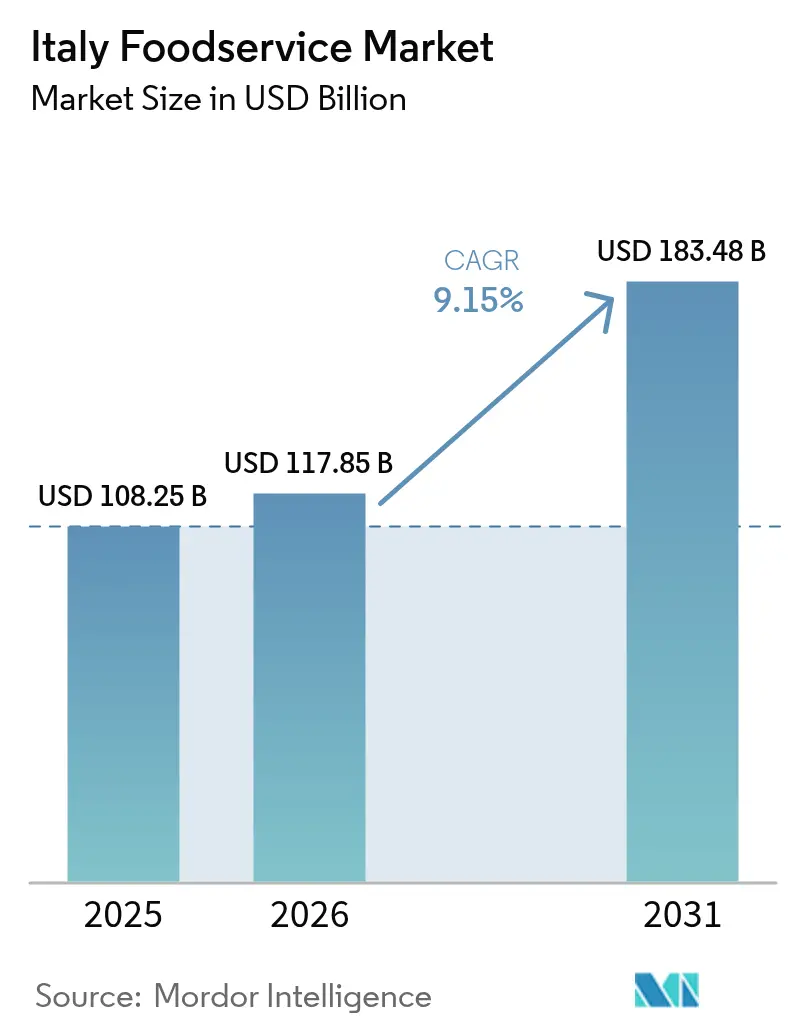

| Base Year Market Size (2025) | USD 108.25 Billion |

| Market Size (2026) | USD 117.85 Billion |

| Market Size (2031) | USD 183.48 Billion |

| Growth Rate (2026 - 2031) | 9.15% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Foodservice Market Analysis by Mordor Intelligence

The Italy foodservice market size is expected to grow from USD 108.25 billion in 2025 to USD 117.85 billion in 2026 and is forecast to reach USD 183.48 billion by 2031 at a 9.15% CAGR over 2026-2031. A rebound in international tourism, rapid roll-out of digital-ordering tools, and the widening presence of quick-service and fast-casual chains are reshaping the competitive landscape. Independent operators still dominate outlet count, yet chained brands are gaining ground as they unlock scale economies in purchasing and technology. Delivery demand remains sticky even after the pandemic, creating structural tailwinds for cloud-kitchen formats and for operators able to integrate first-party logistics. At the same time, higher energy tariffs and persistent labor shortages curb margin expansion and push operators toward equipment automation, data-driven staffing, and price-mix optimization.

Key Report Takeaways

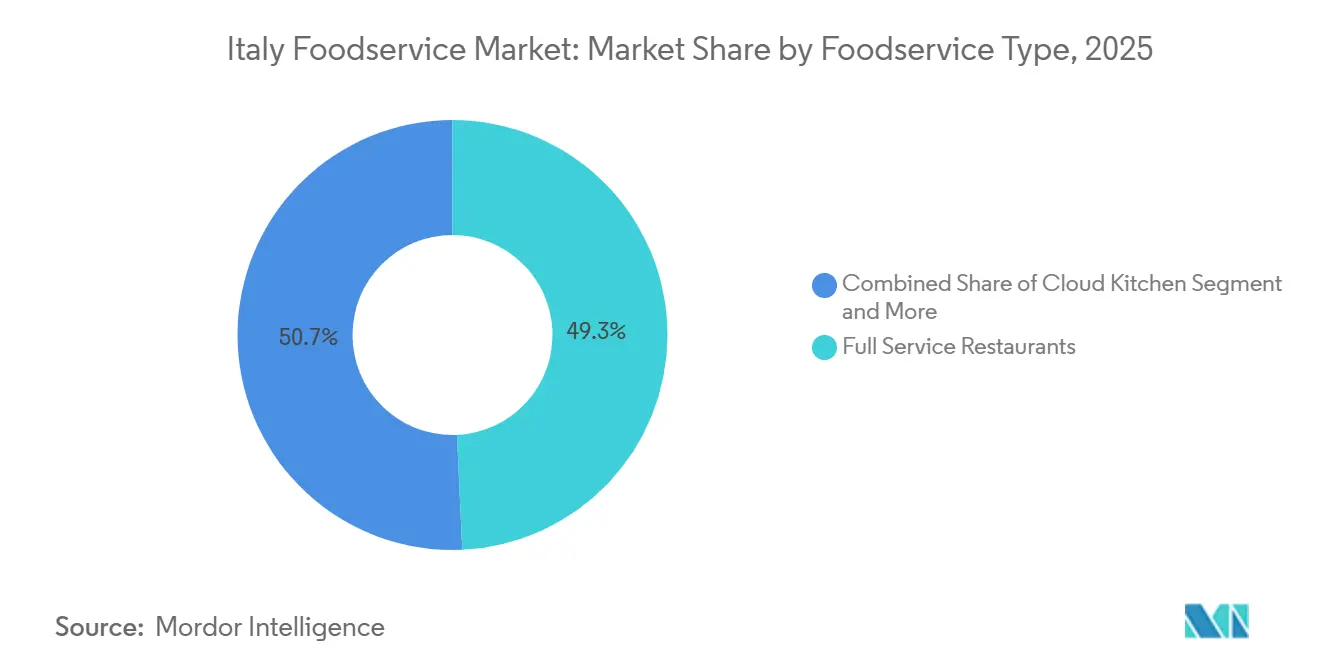

- By foodservice type, full-service restaurants held 49.28% of the Italy foodservice market share in 2025, while cloud kitchens are projected to expand at a 10.28% CAGR through 2031.

- By outlet, independent operators represented 75.38% of the Italy foodservice market share in 2025, whereas chained outlets are set to grow at a 10.86% CAGR to 2031.

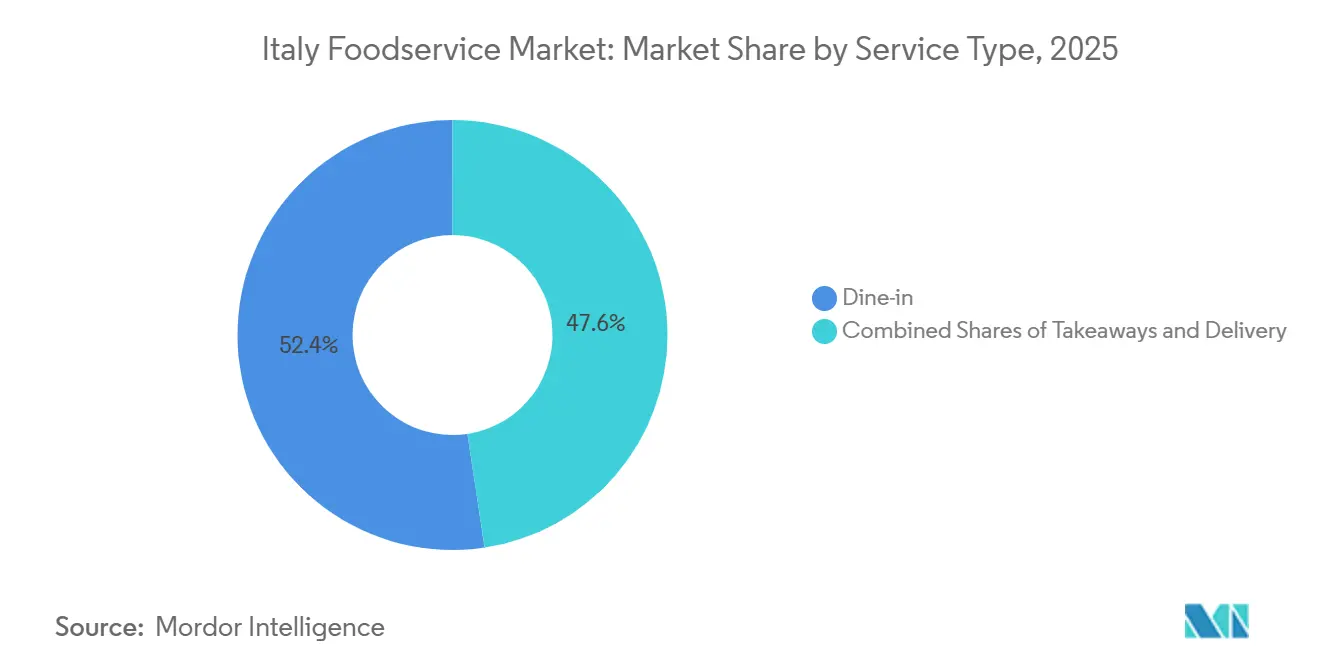

- By service type, dine-in accounted for 52.38% of transactions in 2025, yet delivery is forecast to post an 11.62% CAGR to 2031.

- By location, standalone venues captured 71.52% of spend in 2025, while travel-channel sites in airports and rail hubs are expected to register a 10.48% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-Focused Menus and Functional Snacking Trends | 1.2% | National, with concentration in Milan, Rome, Florence | Medium term (2-4 years) |

| Rapid Chain and QSR Expansion in Fragmented Markets | 1.8% | National, strongest in Northern Italy and major metropolitan areas | Short term (≤ 2 years) |

| Tourism Recovery Boosting Leisure and Travel Sites | 1.5% | National, peak impact in Venice, Rome, Florence, Amalfi Coast | Short term (≤ 2 years) |

| Advanced Digital Ordering and Third-Party Delivery | 1.4% | National, led by Milan, Rome, Turin, Bologna | Medium term (2-4 years) |

| Sustainability-Led Provenance and Zero-Waste Initiatives | 0.8% | National, early adoption in Northern regions | Long term (≥ 4 years) |

| AI-Powered Demand Forecasting for Micro-Formats | 0.9% | National, concentrated in chain operations and cloud kitchens | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health-Focused Menus and Functional Snacking Trends

Italian consumers are increasingly prioritizing transparency regarding ingredient origins and nutritional value, challenging the traditional focus on indulgent, carb-heavy dishes. By 2024, Michelin recognized 14 Italian restaurants with its prestigious Green Star, including Vite in Erbusco, àbitat in Milan, and Don Alfonso 1890 in Sant'Agata sui Due Golfi. These establishments, sourcing over 80% of their produce within a 50-kilometer radius, have seamlessly woven fermentation, plant-based proteins, and Mediterranean diet principles into their tasting menus, as highlighted in the Michelin Guide Italy 2024. In 2024, Eataly unveiled its "alla Radice" product line, incorporating QR codes on packaging to trace ingredients back to their farms. This initiative resonated with health-conscious shoppers, boosting basket sizes by 18%. Quick-service chains are also adapting: McDonald's Italy rolled out a quinoa-and-chickpea burger in early 2025, and Starbucks launched its Oleato olive-oil-infused beverage platform in February 2023, capitalizing on Italy's cultural appreciation for functional fats to stand out from conventional espresso drinks.

Rapid Chain and QSR Expansion in Fragmented Markets

In 2023, Italy had 262,561 foodservice outlets, with only 7,768 being chained locations, leaving 97% of the market in independent hands. This presents a significant consolidation opportunity, as noted in the USDA GAIN Report Italy HRI 2024[1]Source: USDA Foreign Agricultural Service, “Italy HRI Food Service Sector Report 2024,” apps.fas.usda.gov. McDonald's plans to invest EUR 800 million (USD 850 million) to open 150 restaurants by 2027, focusing on secondary cities in Emilia-Romagna and Puglia, where QSR penetration is 40% lower than in Milan. La Piadineria, Italy's second-largest chain by unit count, opened 75 locations in 2025 and aims to exceed 500 outlets by October 2025. Its rapid growth is driven by an asset-light franchising model and compact sites under 100 square meters, reducing build-out costs to EUR 150,000 per location. Wendy's signed a master franchise agreement in 2024 to open 170 restaurants by 2035, with the first two Milan units launching in early 2026. This move aligns with the growing Italian demand for premium burgers, as seen in Five Guys' 12-location expansion since 2016. The rise of chains pressures independent operators to join buying groups or lose market share to brands leveraging digital infrastructure and volume discounts.

Tourism Recovery Boosting Leisure and Travel Sites

In 2024, Italy recorded 88.6 million foreign trips, reflecting a 3.4% rise compared to the previous year. Tourists directed a substantial share of their spending, 42% of a total EUR 54.2 billion (approximately USD 57.6 billion), toward food and beverages. This amounts to around EUR 22.7 billion (USD 24.1 billion), which is 8 percentage points higher than the European average, according to the Bank of Italy's 2024 Tourism Statistics[2]Source: Banca d’Italia, “Annual Report 2024 – Tourism Statistics,” bancaditalia.it. Leveraging this trend, Autogrill launched 'Terrazza Eataly', a 1,200-square-meter food hall at Rome's Fiumicino Airport in July 2024, featuring 15 regional Italian brands. Later, in December 2024, they opened a new Food Court that includes well-known names such as All'Antico Vinaio, EXKI, and Lievito. Highlighting the profitability of airport dining, KFC entered the travel sector in July 2025, opening outlets at Milan's Bergamo Airport and Florence's Santa Maria Novella station. Their approach is based on the understanding that captive audiences are willing to pay a 20-30% premium and typically spend 40% more than at standard street locations.

Advanced Digital Ordering and Third-Party Delivery

Third-party delivery platforms permanently altered Italian dining habits during the pandemic. Currently, 65% of Italians order delivery at least once a month, with growth remaining positive despite moderation. Deliveroo and Just Eat dominate the market, holding a combined 70% share. However, their 25-35% commission rates strain restaurant margins, driving operators to develop proprietary apps or explore alternative aggregators. Technology adoption extends beyond delivery, with 84% of Italian restaurants using digital tools for operations by late 2025, and 70% leveraging AI for menu personalization, inventory management, and demand forecasting. In 2024, McDonald's Italy implemented dynamic pricing algorithms, adjusting combo-meal prices based on time and weather, boosting off-peak average checks by 6%. Cloud kitchens, growing 20% in 2025 and concentrated in Milan, Rome, and Turin, rely on digital orders and algorithmic routing, achieving 60% lower overheads by eliminating dining rooms and front-of-house labor.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Labor Shortages and Escalating Wage Pressures | -1.3% | National, most acute in Northern Italy and tourist destinations | Short term (≤ 2 years) |

| Aging Demographics Reducing Dine-In Visits | -0.9% | National, concentrated in rural and Southern regions | Long term (≥ 4 years) |

| Volatile High Energy and Raw Material Costs | -1.1% | National, disproportionate impact on energy-intensive formats | Medium term (2-4 years) |

| Strict Urban Licensing and NIMBY Resistance to Dark Kitchens | -0.6% | Milan, Rome, Turin, Bologna | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Labor Shortages and Escalating Wage Pressures

Italy's hospitality sector struggles with labor shortages, limiting growth and affecting service quality. The Bank of Italy's 2025 labor-market report highlights foodservice as one of the industries with the highest vacancy rates, driven by pandemic-era emigration, an aging workforce, and younger workers favoring remote jobs. Tourist hubs like Venice and the Amalfi Coast face staffing issues, leaving 15-20% of tables unserved during peak months like July and August. Wage inflation adds pressure, with 2024 collective bargaining agreements raising minimum hourly rates for kitchen and service staff by 8-10%. Competition from logistics and e-commerce centers, offering similar pay with stable schedules, further tightens labor supply. Platforms like Deliveroo and Just Eat fill some gaps but rely on non-standard employment, lacking benefits and training, which hinders skill development. Automation offers partial relief: 40% of Italian quick-service restaurants use self-ordering kiosks, and Italpizza's robotic pizza lines, targeting 575 million units annually by 2028, reduce manual labor. However, automating front-of-house roles remains difficult without compromising the social dining experience valued by Italians.

Aging Demographics Reducing Dine-In Visits

In 2024, Italy's median age of 48.4 years, the highest in the European Union, highlights a growing demographic challenge. By 2031, the 65 and older population is expected to rise from 24% to 27%, according to Istat Demographics 2024[3]Source: Istat, "Demographics 2024 – Population and Households." istat.it. Older Italians dine out 30 to 40% less than those aged 25 to 44, favoring home-cooked meals or meal kits suited to their dietary and mobility needs. This shift has reduced per-capita spending in senior-heavy regions like Liguria and Molise, where dine-in traffic dropped 6% from 2023 to 2025 despite steady tourist numbers. Millennials and Gen Z are driving demand for delivery, cloud kitchens, and experiential dining like Eataly's food halls, but their smaller share of the population (under 35s make up 32%) limits their impact. Traditional trattorias, once popular for family dinners, now see average party sizes fall from 4.2 in 2019 to 3.1 in 2025. Meanwhile, fast casual and grab-and-go formats attract solo diners and busy households. By 2050, Italy's population is projected to shrink by 3.8%, with rural areas hit hardest, pushing operators to focus on urban centers and accept lower activity in secondary markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Outpace Legacy Formats

In 2025, full-service restaurants accounted for 49.28% of Italy's foodservice spending, highlighting the nation's cultural emphasis on meals as social events rather than simple transactions. However, cloud kitchens led growth in the segment, achieving a 10.28% CAGR through 2031. These delivery-focused operators avoid the capital and labor demands of traditional restaurants. Concentrated in Milan, Rome, and Turin, these micro-fulfillment centers reduce fixed costs by 60% by eliminating dining spaces. Their advanced demand forecasting enables just-in-time inventory, cutting food waste by 25 to 30%. Quick-service restaurants (QSRs) captured 28% of the 2025 spending, supported by McDonald's 700 outlets and La Piadineria's 481, which together serve 3.5 million daily customers. Their efficient layouts generate annual revenue of EUR 1.2 to 1.5 million (USD 1.3 to 1.6 million) per location. Cafés and bars, including specialty coffee shops and traditional espresso counters, held an 18% market share. Starbucks' 40-plus Italian outlets and Nespresso's 75 HoReCa boutiques show that premium branding can align with Italy's café traditions.

In the QSR category, burger chains are growing the fastest, driven by McDonald's EUR 800 million (USD 850 million) investment and Wendy's planned entry. Pizza chains like Alice Pizza, with over 200 outlets, and bakeries such as Italpizza, producing 460 million units annually, leverage Italy's pizza heritage to expand domestically and export frozen products. Asian and Middle Eastern cuisines remain niche in full-service restaurants, contributing less than 8% of revenue, but their growth rates of 12 to 14% CAGR outpace European and North American categories. Younger diners are driving this trend with their interest in novelty and plant-based options. Latin American cuisine holds less than 2% market share, limited by ingredient availability and consumer unfamiliarity, though specialty chains in Milan and Rome are testing Peruvian and Mexican offerings.

By Outlet: Chained Operators Gain Ground in Fragmented Landscape

In 2025, independent outlets held a significant 75.38% share of Italy's foodservice market, reflecting the nation's culinary traditions, family-run establishments, and consumer preference for local authenticity. However, chained outlets are growing rapidly, with a 10.86% CAGR through 2031. Their growth is driven by advantages in procurement, technology, and marketing, which are reducing the lead historically held by independents. In 2025, McDonald's, La Piadineria, and Starbucks opened 180 new units, focusing on suburban shopping centers and transportation hubs with high foot traffic, standardized formats, and extended operating hours. Chained operators also benefit from digital infrastructure that many independents cannot afford. Investments in ordering apps, loyalty programs, and AI-driven menu optimization, costing EUR 50,000 to 100,000, remain a challenge for independents, with only 15% meeting this threshold by 2025.

Franchise models are driving chain expansion, especially in the QSR and café sectors. La Piadineria's asset-light strategy, where franchisees invest EUR 150,000 for a unit under 100 square meters, led to 75 new openings in 2025. The brand aims to exceed 500 outlets by October 2025. Alice Pizza, in partnership with Chef Express, plans to add 30 travel-channel locations from 2023 to 2028, leveraging Chef Express's 410 existing points of sale. Independent operators are responding by joining buying cooperatives like those organized by Camst Group and CIRFOOD, which pool purchasing power across more than 1,000 outlets. However, these alliances lack the brand recognition and digital tools that national chains use to attract younger, tech-savvy consumers.

By Service Type: Delivery Surges as Dine-In Stabilizes

In 2025, dine-in services accounted for 52.38% of Italy's foodservice transactions, highlighting the nation's cultural focus on communal dining and the value placed on full-service restaurants. However, the delivery segment is driving growth, with an 11.62% CAGR projected through 2031. This growth is supported by third-party platforms, proprietary apps, and cloud kitchens, which are normalizing off-premise dining. Home-delivery orders increased by 35% between 2020 and 2021. Currently, 65% of Italians order delivery at least once a month. While this frequency has stabilized, it remains 40% higher than pre-pandemic levels. Deliveroo and Just Eat lead the third-party delivery market, but their commission rates of 25% to 35% have encouraged restaurants to develop direct-ordering apps. For example, McDonald's Italy reported that 38% of its delivery orders in 2025 came through its proprietary app, up from 22% in 2023. This shift reduces commission costs and enables the collection of first-party customer data.

Cost-conscious consumers avoiding delivery fees and busy professionals seeking quick lunches are increasingly using these direct-ordering platforms. Labor shortages are limiting table capacities, and an aging population is reducing visit frequency. However, premium full-service restaurants are maintaining their appeal. Between 2024 and 2025, average checks at Michelin-starred restaurants rose by 12%, reflecting affluent diners' preference for experience over convenience. Geography also influences service preferences. Delivery services exceed 35% penetration in cities like Milan and Rome but fall below 18% in rural areas, where limited courier availability and longer distances affect delivery economics.

By Location: Travel Channels Capitalize on Mobility Recovery

In 2025, standalone locations such as street-front restaurants, suburban outlets, and neighborhood cafés dominated Italy's foodservice market, accounting for 71.52% of spending. Their success was driven by unrestricted operating hours, flexible menu formats, and proximity to residential areas. Meanwhile, travel channel sites in airports, railway stations, and motorway service areas are growing at a 10.48% CAGR through 2031. This growth is supported by mobility recovery and captive audience economics, enabling these sites to charge 20-30% price premiums. Airport concessions are particularly profitable. For example, Autogrill's Terrazza Eataly, opened in July 2024 at Rome Fiumicino, spans 1,200 square meters and features 15 regional brands. Additionally, the terminal's food and beverage offerings expanded in December 2024 with the launch of the Food Court, adding brands like All'Antico Vinaio, EXKI, and Lievito.

Retail embedded foodservice, including food courts in shopping malls and dining options anchored by supermarkets, captured 9% of spending in 2025. Eataly, with its 12 Italian locations, demonstrated the potential of hybrid grocery-restaurant formats, generating EUR 80-100 million (USD 85-106 million) per site by cross-selling packaged goods and prepared meals. Lodging-based foodservice, covering hotel restaurants and resort dining, accounted for 6% of revenue. This segment is growing at an 8.2% CAGR, driven by luxury properties in Tuscany, Sicily, and the Dolomites that integrate farm-to-table dining into multi-day guest experiences. Leisure sites, including stadiums, theme parks, and entertainment venues, represent 5% of spending. However, they face challenges from sporadic traffic and regulatory limits on alcohol sales. Serie A football clubs are upgrading concession offerings to increase per-fan spending during match days.

Geography Analysis

Northern Italy drives value creation in the Italian foodservice market owing to higher income levels and robust tourism corridors that link Milan, Venice, and the lakes district. Lombardy alone hosts more than 20% of national outlets and benefits from business-travel flows that sustain weekday lunch demand. The Veneto region leverages Venice’s 5.6 million annual visitors to support premium trattorias and café-patio formats able to charge the highest average checks in the country.

Central regions, led by Lazio and Tuscany, blend domestic offices with heritage tourism. Rome’s metro population underpins late-night dining, while Florence’s art circuit lifts seasonal peaks that justify hybrid retail-restaurant spaces catering to foreign travelers prioritizing provenance storytelling. Eataly’s Florence store exemplifies this mix, achieving one of the chain’s highest sales per square meter.

Southern Italy and the islands present a more polarized picture, with Sicily and Campania enjoying cruise-ship and vacation-home inflows but facing lower resident purchasing power. Smaller town centers exhibit outlet density yet lower ticket sizes, prompting chains to stick to coastal cities where per-capita spend exceeds EUR 1,200. Aging demographics in Calabria and Molise suppress weekday eating-out frequency, nudging operators to shorten trading windows or pivot toward delivery on weekends.

Competitive Landscape

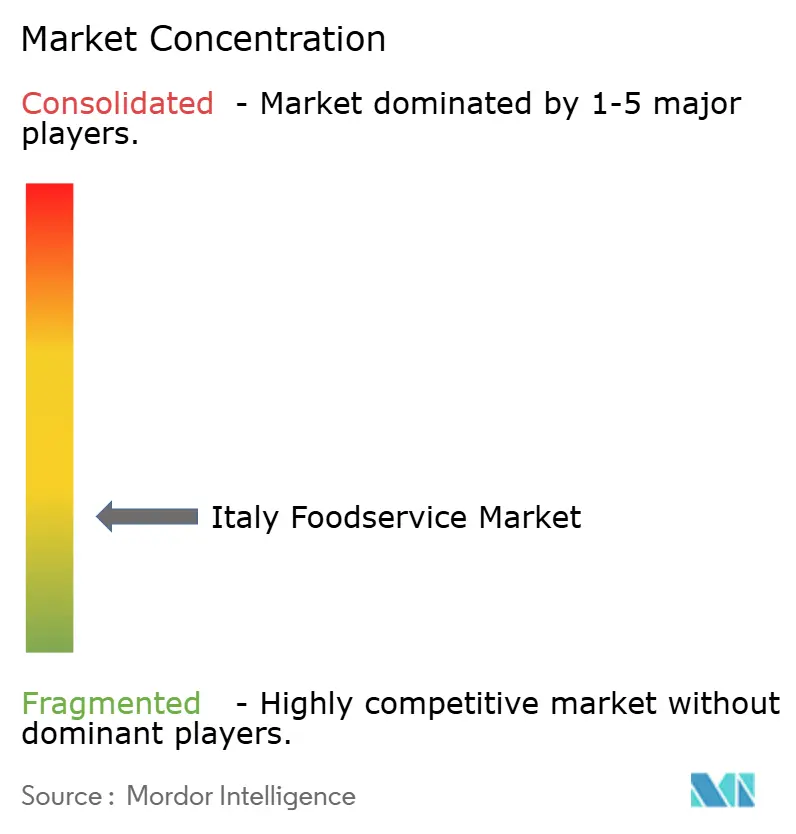

The Italy foodservice market remains fragmented. The top 20 players command under 25% share, leaving considerable white space for consolidation. McDonald’s leads with 700 units and plans for 150 additional sites by 2027, funded by a EUR 800 million capital budget. Dynamic pricing software and an owned delivery fleet allow the chain to capture demand spikes without ceding margin to aggregators.

La Piadineria operates 481 outlets and opened 75 stores during 2025 by exploiting an asset-light franchise model. Its average unit cost of EUR 150,000 and sub-12-month payback attract entrepreneurial capital, particularly in underserved secondary cities. Autogrill, Chef Express, and Lagardère Travel Retail dominate travel concessions, where long-term leases and high entry fees deter new entrants. Even so, KFC entered the segment in 2025 with airport and rail-station openings, proving that global QSR brands view captive-audience venues as incremental growth vectors.

Technology remains the chief battleground: roughly 84% of outlets use some form of digital back-office tool, yet only one in five independents have adopted AI modules. Chains can leverage predictive analytics for labor scheduling and menu engineering, widening the performance gap. Cloud-kitchen operators and platform-native brands also eye Italy’s urban cores, but zoning restrictions and neighborhood pushback continue to slow roll-outs in Milan, Rome, and Bologna.

Italy Foodservice Industry Leaders

-

Autogrill SpA

-

Cremonini SpA

-

McDonald's Corporation

-

CIGIERRE SpA

-

Restaurant Brands International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Corinthia London unveiled Mezzogiorno by Francesco Mazzei, transforming the former Northall restaurant into a vibrant Southern Italian-inspired venue drawing from the chef's Calabrian roots and Baroque palazzo aesthetics.

- October 2025: La Gioia group has recently introduced Al Baretto Sant’Ambrogio, a new restaurant located in Milan. This addition is part of the La Gioia project, which has established a strong reputation for delivering exceptional seafood dishes and offering a refined Italian dining experience. With this new venue, the group aims to further enhance its presence in the culinary scene by combining tradition with innovation.

- February 2025: Nusret Gökçe, the Turkish chef and entrepreneur widely recognized as Salt Bae, has announced opened three new restaurants in Italy. The selected cities for this expansion are Rome, Milan, and Naples.

Italy Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.

By Foodservice Type

| Café and Bars | By Cuisine | Bars and Pubs |

| Café | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

By Outlet

| Chained Outlets |

| Independent Outlets |

By Locations

| Leisure |

| Lodging |

| Retail |

| Sandalone |

| Travel |

By Service Type

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Café and Bars | By Cuisine | Bars and Pubs |

| Café | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Sandalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms