Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 17.99 Billion |

| Market Size (2031) | USD 19.57 Billion |

| Growth Rate (2026 - 2031) | 1.69% CAGR |

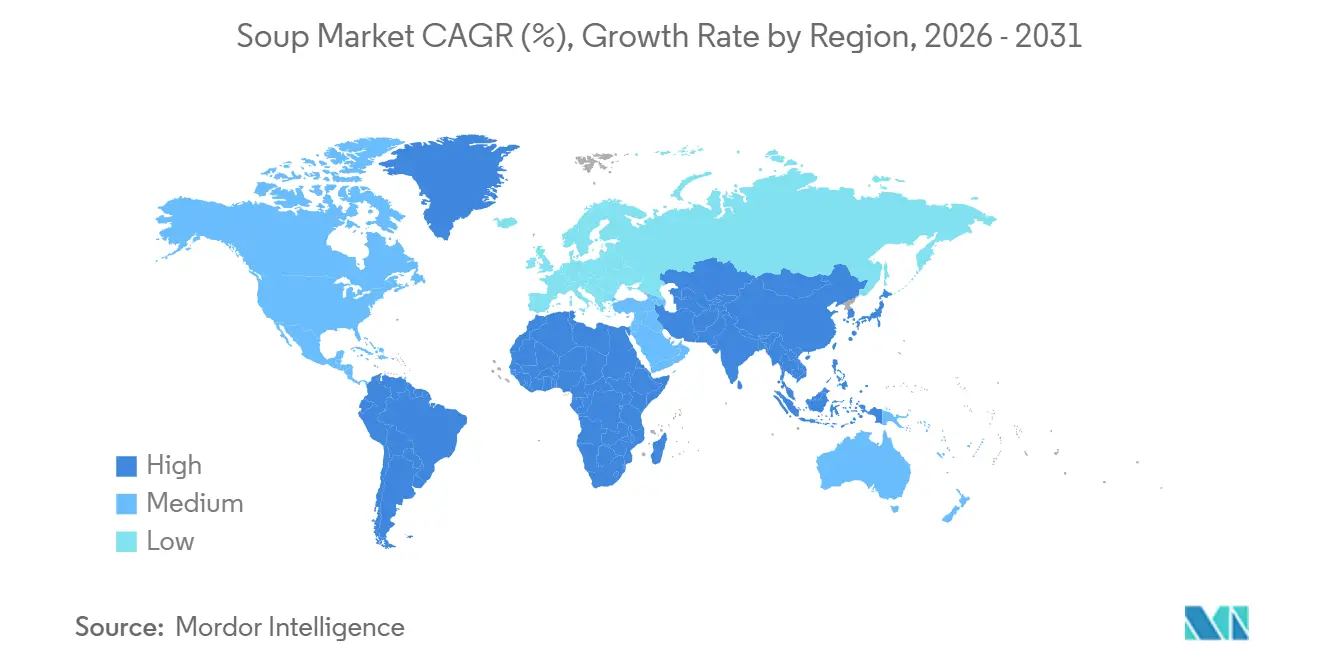

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Soup Market Analysis by Mordor Intelligence

The Soup Market size was valued at USD 17.70 billion in 2025 and estimated to grow from USD 17.99 billion in 2026 to reach USD 19.57 billion by 2031, at a CAGR of 1.69% during the forecast period (2026 to 2031). Shelf-stable lines still dominate household pantries, yet chilled products are adding new users through fresh-adjacent taste and shorter ingredient lists. Online retail is converting browsing into repeat orders as meal-kit operators and direct-to-consumer brands make delivery frictionless. Reformulation to meet the U.S. FDA's “healthy” claim, along with the rise of plant-forward recipes, is reshaping consumer perception from an emergency pantry staple to an everyday wellness option. Competitive intensity remains moderate, allowing regional specialists to scale through local sourcing stories, clean-label innovations, and ethnic-flavor innovations.

Key Report Takeaways

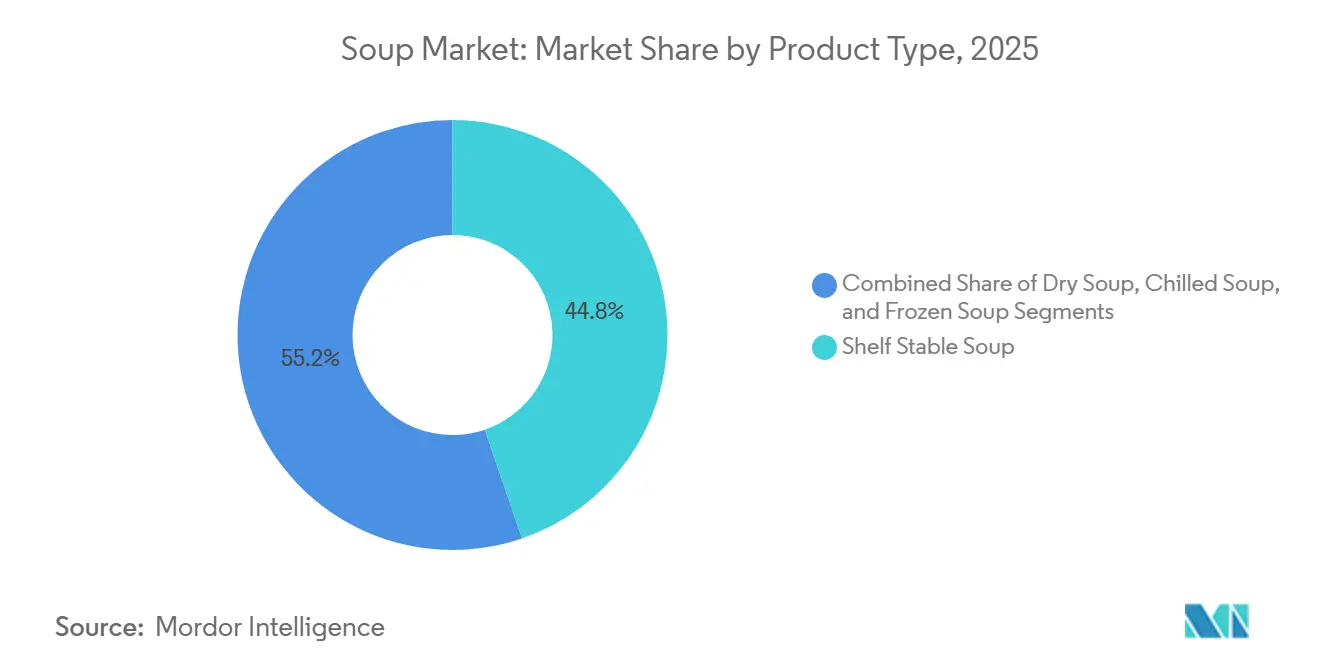

- By product type, shelf-stable soup held 44.76% of the soup market share in 2025, while chilled soup is expected to advance at a 1.88% CAGR through 2031.

- By category, vegetarian offerings accounted for 53.59% of the soup market size in 2025 and are projected to expand at a 2.06% CAGR through 2031.

- By packaging format, pouches accounted for 48.51% of the soup market share in 2025, whereas cans are expected to register the fastest growth rate of 2.62% from 2026 to 2031.

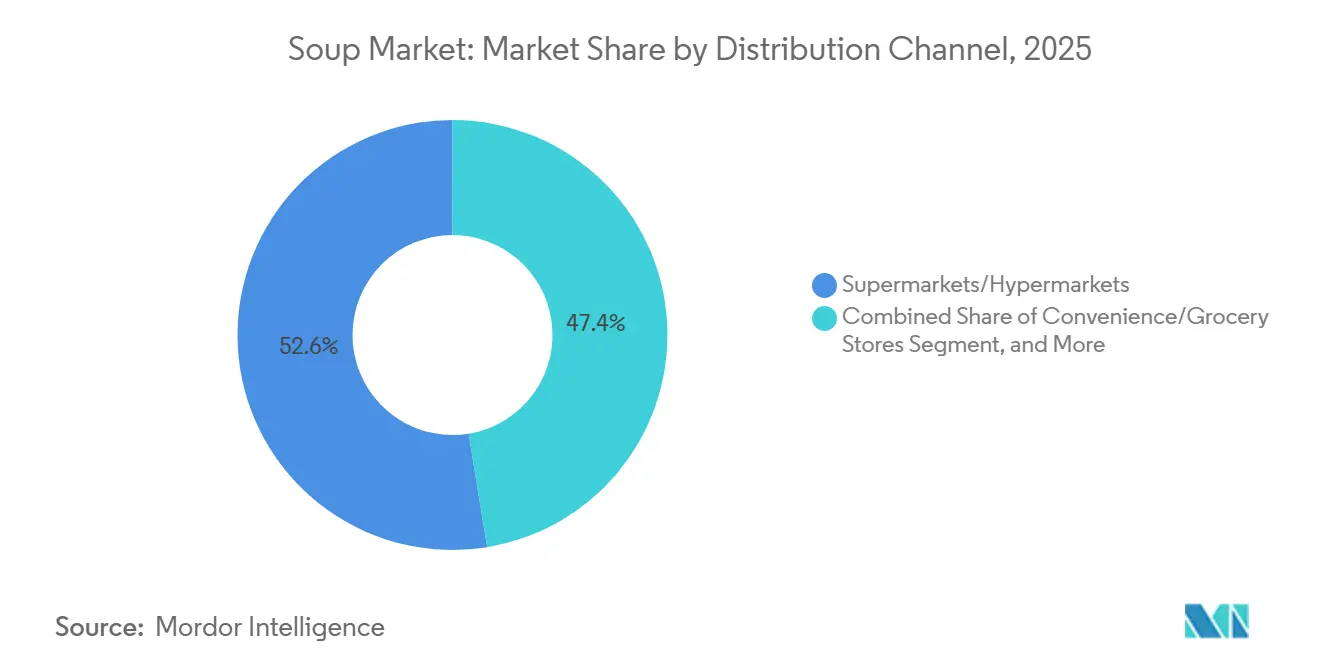

- By distribution channel, supermarkets and hypermarkets led with a 52.58% revenue share in 2025; online retail stores are projected to record the highest CAGR of 2.89% through 2031.

- By geography, Europe accounted for 36.42% of the 2025 value, while the Asia-Pacific region is the fastest-rising, with a 3.14% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soup Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of vegan and plant-based soups | +0.4% | Global, with strongest adoption in North America and Europe | Medium term (2-4 years) |

| Product innovation and variety | +0.3% | Global, led by developed markets | Long term (≥ 4 years) |

| Sustainable and eco-friendly packaging | +0.2% | Europe and North America primarily, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Seasonal demand variations | +0.2% | Global, with pronounced effects in temperate regions | Short term (≤ 2 years) |

| Influence of social media and influencers | +0.1% | Global, strongest in urban markets with high digital penetration | Medium term (2-4 years) |

| Demand for quick and easy meal solutions | +0.3% | Global, accelerated in urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising popularity of vegan and plant-based soups

Plant-based soups are gaining traction as flexitarian diets expand beyond coastal metropolitan areas into mainstream grocery aisles. According to the Good Food Institute, U.S. retail sales of plant-based foods reached USD 8.1 billion in 2024, with soups and broths emerging as a fast-growing subcategory driven by pea, lentil, and chickpea bases that provide complete amino acid profiles without animal inputs[1]Source: Good Food Institute, “Plant-Based Market Research,” gfi.org. This trend reflects not only changing dietary preferences but also supply-chain pragmatism, as pulse crops require less water and fertilizer than livestock, helping manufacturers mitigate commodity volatility. In 2024, FDA guidance clarified plant-based labeling, reducing litigation risk and enabling clearer shelf communication. European retailers are supporting the adoption of vegan products through dedicated end-cap displays during Veganuary and other campaigns, converting trials into repeat purchases. Strategically, brands that prioritize sensory optimization, enhancing umami depth and mouthfeel, are positioned to outperform those relying solely on health claims, as taste remains the primary barrier to mainstream acceptance.

Product innovation and variety

Flavor diversification and format experimentation are reshaping purchase drivers, with ethnic profiles such as Thai tom yum, Indian dal, and Mexican pozole migrating from foodservice to retail shelves. Unilever's Knorr brand launched a "Global Flavors" line in 2025, featuring region-specific recipes co-developed with culinary institutes in Bangkok, Mumbai, and Mexico City, targeting multicultural households and adventurous eaters. This innovation extends beyond taste to texture and preparation convenience; single-serve microwaveable pouches and cold-sippable formats are gaining traction among commuters and office workers who lack access to stovetops. Campbell Soup's "Well Yes!" line, which emphasizes visible vegetable pieces and no artificial ingredients, posted double-digit growth in 2024, demonstrating that transparency and ingredient integrity can command premium pricing. The underlying dynamic is a bifurcation: mass-market players are defending volume through value packs and promotional pricing, while premium entrants are capturing margin through limited-edition releases and chef collaborations that generate social media buzz and drive trial.

Sustainable and eco-friendly packaging

Packaging sustainability in the European plant-based soup market is evolving from a marketing narrative into an operational necessity, driven by EU regulations mandating minimum recycled content in food-contact plastics and extended producer responsibility schemes that assign end-of-life costs to manufacturers. The FDA's approval in 2024 of post-consumer recycled polyethylene terephthalate (rPET) for direct food contact, subject to strict migration testing, opened up supply-chain opportunities for soup producers aiming to reduce their use of virgin resin. Bonduelle’s 2025 commitment to convert 75% of its soup packaging to recyclable or compostable materials by 2027 demonstrates alignment with regulatory compliance and consumer demand[2]Source: Bonduelle, “Bonduelle Accelerates Sustainable Packaging Transition,” bonduelle.com. The strategic challenge is maintaining barrier performance for shelf life and food safety while improving recyclability, since multi-layer laminates are difficult to separate in municipal recycling systems. Brands investing in mono-material pouches or aluminum cans with high recycled content are likely to secure preferential shelf placement in sustainability-focused retailers, whereas laggards risk delisting or margin erosion from regulatory penalties.

Seasonal demand variations

Winter seasonality continues to dominate in temperate markets, with November-to-February sales accounting for 40–50% of annual volume in North America and Northern Europe, creating inventory risks and underutilized production capacity during warmer months. Campbell Soup’s fiscal 2025 earnings call highlighted initiatives to smooth demand through chilled gazpacho and cold-sippable bone broths aimed at summer consumption, reducing reliance on off-peak promotional discounting. The strategic insight is that manufacturers with flexible production lines capable of rapid format changeovers can capture incremental margin by avoiding the dilution caused by deep discounts. Climate volatility further compresses traditional seasonal windows: milder winters in the U.S. Midwest and Northeast reduced heating and cooling demand in early 2025, prompting retailers to liquidate inventory at reduced prices, according to the USDA ERS. Brands that establish year-round positioning, such as protein-forward soups for post-workout recovery or meal replacement, can mitigate seasonal earnings volatility and improve overall asset utilization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for fresh and homemade alternatives | -0.5% | Global, strongest in developed markets | Medium term (2-4 years) |

| Negative perceptions regarding healthiness | -0.3% | North America and Europe primarily | Short term (≤ 2 years) |

| Production efficiency challenges | -0.2% | Global, particularly affecting smaller manufacturers | Long term (≥ 4 years) |

| Supply chain disruptions | -0.3% | Global, with regional variations in severity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer preference for fresh and homemade alternatives

During periods of economic uncertainty, consumers increasingly prefer fresh food, perceiving homemade meals as both healthier and more economical compared to processed options. The shift in consumer preference challenges soup manufacturers to redefine their value propositions beyond convenience. To remain competitive, manufacturers must innovate by enhancing nutritional density and ensuring ingredient transparency to align with consumer expectations. Research on consumer behavior highlights that familiarity with traditional cooking methods often leads to more nuanced motivations for food preparation, such as nostalgia and perceived health benefits, which processed soups struggle to replicate. To address these challenges, companies need to invest in marketing strategies that emphasize the nutritional equivalence of their products to fresh alternatives. At the same time, they must maintain cost advantages to appeal to budget-conscious consumers, particularly during economic downturns. By balancing these factors, manufacturers can better position themselves in a market increasingly inclined toward fresh food preferences.

Negative perceptions regarding healthiness

Regulatory transparency is intensifying health perception challenges as it brings sodium and preservative content in food products under scrutiny, raising consumer concerns about long-term wellness. The FDA's voluntary sodium reduction goals, aimed at specific soup categories with defined baseline levels and reduction targets, highlight these health concerns while creating significant compliance pressures for manufacturers. Additionally, Regulatory uncertainty surrounding sodium reduction targets, particularly the FDA’s current “as-packaged” sodium concentration standards for dry soup mixes, poses a challenge for manufacturers. The lack of standardized “as-prepared” sodium benchmarks across various formats (dry, canned, bouillon) may lead to unfair comparisons and limit innovation, while ongoing discussions about reclassifying bouillons as non-target categories add further ambiguity[3]Source: The Food Industry Association, "fmi-comments-on-phase-ii-sodium-reduction-draft-guidance", www.fmi.org. Furthermore, front-of-package labeling requirements, which mandate the prominent display of nutrients consumers are advised to limit, could negatively impact impulse purchases, a key driver of soup sales historically. Public health organizations further emphasize that a substantial portion of sodium consumption originates from commercially processed foods, including soups, thereby increasing the demand for more aggressive sodium reduction targets to address these health concerns effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chilled Formats Capture Fresh-Adjacent Premium

Shelf-stable soup accounted for 44.76% of the market in 2025, driven by its extended shelf life, efficient ambient distribution, and ingrained consumer pantry habits. However, chilled soup is the fastest-growing segment, expanding at a 1.88% CAGR through 2031, as retailers expand their refrigerated sets and consumers increasingly seek fresh-adjacent convenience. Chilled formats offer sensory advantages, brighter vegetable colors, crisper textures, and flavors less affected by retort sterilization, allowing 20-30% price premiums over shelf-stable equivalents. Tideford Organic’s chilled soup range in UK supermarkets achieved 25% year-over-year growth in 2024, highlighting its short ingredient lists and emphasis on freshness cues. Frozen soup, although smaller in volume, caters to foodservice bulk packs and meal-kit applications, offering an extended shelf life without nutrient degradation. In contrast, dry soup mixes, historically dominant in emerging markets, face pressure as rising disposable incomes drive a trade-up to ready-to-eat formats.

The strategic implication is that manufacturers with cold-chain capabilities and regional production footprints can expand margins through chilled innovation, while those reliant on centralized shelf-stable production risk volume erosion. Campbell Soup’s 2025 launch of the “Fresh Starts” refrigerated line in the U.S. Northeast, featuring locally sourced vegetables and a 14-day shelf life, exemplifies this shift toward fresh-adjacent positioning. Regulatory compliance also affects format selection: FDA refrigerated food safety guidelines require continuous temperature monitoring, raising barriers for smaller brands but creating opportunities for regional specialists with tight, reliable supply chains.

By Category: Plant-Forward Eating Drives Vegetarian Dominance

Vegetarian soup accounted for 53.59% of the market in 2025 and is projected to grow at a 2.06% CAGR through 2031, outpacing non-vegetarian offerings as flexitarian diets become mainstream and plant-based eating expands beyond niche segments. This growth reflects multiple converging factors: environmental awareness, animal welfare concerns, health optimization, and advances in plant-protein technology that now deliver taste and texture comparable to meat-based broths. Non-vegetarian soups, including those based on chicken, beef, and seafood, retain loyal followings, particularly among older consumers and in colder climates, where hearty, protein-dense meals align with cultural norms. However, they face challenges from rising poultry and beef costs, as well as growing scrutiny of factory farming practices. Amy’s Kitchen’s organic vegetarian soup line, free from all animal products and USDA Organic–certified, expanded shelf presence in Whole Foods and Sprouts in 2024, demonstrating that clean-label vegetarian positioning can command premium pricing.

The strategic challenge for non-vegetarian soup brands lies in differentiation through premium protein sources, such as grass-fed beef, free-range chicken, or sustainably sourced seafood, to justify higher price points and appeal to conscious carnivores. Kettle & Fire’s bone broth, marketed as a collagen-rich wellness product rather than traditional soup, achieved 40% revenue growth in 2024 by targeting keto and paleo consumers prioritizing protein density and gut health. The broader category dynamic shows increasing blurring between segments: vegetarian soups are marketed for functional benefits such as fiber, antioxidants, and satiety, rather than simply as meat-free options, while non-vegetarian soups emphasize provenance and nutrient density to resist commoditization.

By Distribution Channel: Traditional Retail Maintains Scale Advantages

Supermarkets and hypermarkets accounted for 52.58% of the 2025 distribution share, reflecting entrenched shopping habits, promotional intensity, and the tactile reassurance of in-store browsing. However, online retail stores are the fastest-growing channel, with a 2.89% CAGR through 2031, as subscription models, direct-to-consumer brands, and meal-kit integration reshape purchase pathways. Deloitte's 2025 Future of Grocery report found that 38% of U.S. consumers now purchase packaged foods online at least monthly, up from 22% in 2020, driven by time savings, convenience of home delivery, and algorithm-driven personalization that surfaces niche brands. Other distribution channels, including foodservice, vending machines, and direct-to-consumer subscriptions, capture incremental volume but face higher per-unit logistics costs that compress margins.

The key takeaway is that maintaining an omnichannel presence has become essential. Brands that successfully balance visibility across both physical retail and digital platforms are set to outperform those relying on a single route to market. Campbell Soup’s 2024 collaborations with Instacart and Amazon Fresh, offering same-day delivery and online-exclusive product lines, illustrate this adaptive dual-channel approach. That said, online retail brings a new set of challenges: lower switching barriers, real-time price comparisons, and algorithms that reward brands with strong consumer reviews. Emerging players like Kettle & Fire and Tideford Organic are capitalizing on direct-to-consumer channels to sidestep traditional slotting costs and collect valuable consumer data for personalized marketing. Meanwhile, established brands face the dual pressures of protecting retail shelf presence from private labels and managing margin pressures driven by heavy promotions.

By Packaging Format: Pouches Dominate Through Convenience and Sustainability

Pouches captured 48.51% of the 2025 packaging share, driven by their lighter weight, lower material costs, improved shelf appeal, and a consumer perception of modernity compared to legacy cans. Stand-up pouches with resealable zippers enable portion control and refrigerated storage after opening, addressing single-person households and snacking occasions that cans cannot serve without transferring contents. Canned soup, despite legacy perceptions of high sodium and industrial processing, is posting the fastest growth at 2.62% CAGR through 2031 as manufacturers reformulate recipes to meet FDA "healthy" claim thresholds and introduce organic, reduced-sodium variants that rehabilitate the format's reputation. Campbell Soup's 2024 redesign of its iconic red-and-white cans, featuring transparent windows that showcase the contents of the soup, represents a strategic effort to combat negative perceptions and signal the quality of its ingredients.

Other packaging formats, including glass jars, Tetra Pak cartons, and microwaveable bowls, serve niche applications such as premium gifting, foodservice single-serve, and on-the-go consumption. The strategic implication is that packaging choice increasingly functions as a brand signal: pouches connote innovation and convenience, cans suggest value and tradition, and glass jars communicate premium quality and giftability. Brands that align packaging format with target demographics and consumption occasions will optimize shelf velocity, while those maintaining rigid format portfolios risk losing relevance as consumer preferences fragment. Sustainability considerations are intensifying as well; aluminum cans boast high recycled content and infinite recyclability, while multi-layer pouches face end-of-life challenges that may trigger regulatory restrictions in Europe and California as per the European Commission.

Geography Analysis

Europe accounted for 36.42% of the global soup market in 2025, remaining the largest regional segment due to the deep-rooted traditions of soup consumption in Germany, the United Kingdom, France, and Italy, where soups are often part of daily meals rather than occasional convenience options. Germany favors hearty lentil and potato varieties, the UK prefers tomato and chicken-based soups, and France emphasizes bisques and consommés, creating diverse flavor profiles that support strong regional brand loyalty. Growth in these mature markets is moderating, however, as private-label penetration intensifies; discount chains such as Aldi and Lidl captured 45% of German soup sales in 2024, compressing branded margins and driving innovation toward premium, organic, and chilled formats. EU food safety regulations, including EFSA guidelines on additives and allergen labeling, add compliance costs but also act as entry barriers, protecting established brands from low-cost imports.

The Asia-Pacific region is the fastest-growing, expanding at a 3.14% CAGR through 2031, driven by urbanization, rising disposable incomes, and the increasing adoption of packaged meal solutions in markets traditionally dominated by home-cooked broths. In China, younger consumers in tier-1 and tier-2 cities prioritize convenience over traditional preparation, allowing brands like Tingyi and Uni-President to capture market share with spicy and numbing flavor profiles. India's soup market is emerging rapidly, with Nestlé Maggi expanding into soup mixes in 2024, leveraging its brand equity and distribution network. Japan’s aging population drives demand for nutrient-dense, easy-to-consume formats such as miso- and collagen-based soups, while Australia’s multicultural consumers favor ethnic flavors and premium organic products.

North America, South America, and the Middle East & Africa collectively hold the remaining market share, with North America growing steadily via chilled and bone broth innovations, while South America and MEA remain price-sensitive, favoring dry mixes and shelf-stable value formats. Urban centers in South Africa and Nigeria present opportunities as cold-chain and retail infrastructure develop, though rural penetration remains constrained by affordability and traditional consumption habits.

Regulatory Landscape

The soup market is governed by a patchwork of food safety and labeling regimes led by national regulators (for example, the US FDA and EU authorities implementing EFSA-aligned rules), with additional influence from international reference standards under the FAO/WHO Codex Alimentarius. In July 2026, the Codex Alimentarius Commission (49th session, Geneva) adopted new guidance on precautionary allergen labeling (PAL) as an annex to the General Standard for the Labelling of Pre-packaged Foods (CXS 1-1985). This adds another harmonization anchor for global label design and risk communication across shelf-stable, chilled, and dry formats.

Market access and compliance costs are also shaped by evolving national measures and administrative requirements that can surface in WTO technical discussions, particularly around labeling and overseas producer registration. In China, authorities released 37 draft national food safety standards for public comment in April 2026 (comment window through June 2026), which exporters of soups, broths, and preparations must track. In Europe, policy attention includes efforts to simplify aspects of food and feed oversight across multiple legal acts (Council document on the EU simplification package, 2026), while keeping the framework of official controls and labeling obligations for additives, allergens, and product claims.

Value Chain Analysis

The soup value chain begins with agricultural inputs, including vegetables, pulses, herbs and spices, plus animal proteins for non-vegetarian recipes, and it extends to processing aids and packaging materials such as cans, pouches, cartons, and closures. Manufacturing covers dehydration and blending for dry mixes, retort and aseptic processing for shelf-stable soups, and shorter-horizon cold-chain production for chilled soups, followed by case packing, warehousing, and distribution into supermarkets/hypermarkets and e-commerce fulfillment. Brand owners typically depend on co-packers, ingredient suppliers, and packaging converters, while retailers shape assortment through shelf-space economics, private-label programs, and compliance expectations around nutrition labeling, allergens, and sustainability claims.

Recent evidence also points to upstream chemical inputs and logistics as binding constraints, even when core food ingredients are locally sourced. In 2026, disruptions linked to the Strait of Hormuz increased exposure to freight volatility, with reports of thousands of ships trapped during conflict-related closures and upstream interruptions affecting inputs such as fertilizer and industrial chemicals used across food production. Cost pressure from transport intensified as well, with Food Industry Executive reporting the FIE Input Cost Index reaching 148 in July 2026 and container freight benchmarks rising sharply week over week, encouraging manufacturers to diversify sourcing lanes, regionalize production footprints (especially for chilled lines), and redesign packaging toward lighter-weight formats to reduce landed-cost sensitivity.

Competitive Landscape

The European and global soup market exhibits moderate concentration, with the top five players, General Mills, Kraft Heinz, Campbell Soup, Nestlé, and Unilever, holding significant but non-monopolistic shares. This structure leaves room for regional specialists, organic brands, and direct-to-consumer disruptors to capture niche segments. Strategic activity reveals a bifurcation: incumbents defend volume through value packs, promotions, and shelf-stable efficiency, while simultaneously investing in premium, better-for-you portfolios that command higher margins and appeal to younger, health-conscious consumers. Campbell Soup’s USD 2.33 billion acquisition of Sovos Brands in 2024, which included the addition of Rao’s premium pasta sauces and Michael Angelo’s frozen entrees, illustrates this pivot toward quality over quantity and acknowledges the structural headwinds facing traditional condensed soups[4]Source: Campbell Soup Company, “Campbell Completes Acquisition of Sovos Brands,” campbellsoupcompany.com.

White-space opportunities exist in functional soups targeting gut health, immunity, or post-workout recovery, as well as in ethnic flavor profiles catering to multicultural households underserved by mainstream offerings. Emerging disruptors are leveraging e-commerce, clean-label formulations, and subscription models to bypass traditional distribution channels and establish direct customer relationships. For example, Kettle & Fire’s bone broth, positioned as a collagen-rich wellness product rather than a traditional soup, surpassed USD 100 million in annual revenue by 2024 via Amazon, direct-to-consumer subscriptions, and partnerships with Whole Foods and Target.

Technology adoption is accelerating across the sector: Unilever’s deployment of AI-driven demand forecasting and dynamic pricing in 2025 reduced out-of-stock incidents by 18% and improved promotional ROI, highlighting how digital capabilities are becoming competitive differentiators beyond product formulation. Regulatory compliance also functions as a competitive moat; updated FDA guidelines on “healthy” claims and front-of-package labeling favor brands with robust R&D and regulatory teams, while smaller entrants face higher per-unit compliance costs that constrain margin expansion.

Soup Industry Leaders

-

General Mills Inc.

-

The Kraft Heinz Company

-

The Campbell Soup Company

-

Nestlé S.A

-

Unilever Plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is performance-nutrition and functional positioning that upgrades soup from pantry staple to a daily-use meal solution, particularly in shelf-stable formats where portioned single-serve convenience supports protein and wellness claims. In July 2026, The Campbell Company launched a soup lineup featuring 20 grams of protein per can, which illustrates active portfolio renovation toward higher-protein, better-for-you cues. This can improve price realization and broaden usage occasions beyond cold-weather consumption. Plant-forward recipes and clean-label reformulation also create whitespace for vegetarian soups that emphasize ingredient transparency, including shorter ingredient lists and fewer artificial additives, while operating within tightening scrutiny of sodium and front-of-pack nutrition communication.

Another opportunity centers on format and channel specialization where operational capabilities become the differentiator, especially for refrigerated soups that require cold-chain reliability and online-first assortments that benefit from subscription replenishment and targeted discovery. Packaging and compliance are increasingly converging as a commercial lever, since producers respond to regulatory and retailer pressure by investing in recyclable-ready formats, mono-material pouch innovation, and claim substantiation processes aligned to major markets. Brands that combine regionally relevant flavor innovation, including ethnic profiles and localized recipes, with repeatable manufacturing platforms and omnichannel execution have more room to compete even in segments where private label is influential.

Recent Industry Developments

- July 2026: The Campbell Company rolled out a major protein-forward soup lineup across key markets, featuring 20 grams of protein per can. The launch expands the brand's wellness-focused portfolio and targets satiety-driven meals in mainstream retail. The move signals Campbell's ongoing commitment to higher-protein formats in soups and related categories.

- June 2026: The Campbell Company partnered with Banza to launch its first gluten-free condensed chicken noodle soup featuring chickpea pasta. The collaboration extends condensed soup into specialty dietary needs while leveraging Banza's gluten-free and legume-protein credentials. The agreement broadens packaging and recipe options to capture more value across both brands' audiences.

- May 2026: The Campbell Company completed its acquisition of a 49 percent interest in La Regina, a pasta sauce manufacturer with operations in Italy and in Alma, Georgia. The deal strengthens Campbell's center-of-store meal ecosystem around soups and adjacent meal components, bolstering manufacturing scale and distribution partnerships.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The soup market is defined as the retail value of packaged soup products that consumers buy for home use, across shelf-stable, chilled, frozen, UHT, and dry formats, including ready-to-eat and easy-to-prepare soups.

Scope exclusions: Freshly prepared food-service soups and restaurant or cafe soup sales are excluded from this sizing.

Segmentation Overview

-

By Product Type

- Dry Soup

- Shelf Stable Soup

- Chilled Soup

- Frozen Soup

-

By Category

- Vegetarian Soup

- Non-Vegetarian Soup

-

By Packaging Format

- Canned

- Pouches

- Other Packaging Format

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base and to keep inputs consistent across countries and time periods. We leaned on public sources such as national statistics offices for food consumption and CPI series, customs and trade portals for packaged food imports and exports, agriculture and food agencies for ingredient and processed food context, and trade associations that track packaged food and retail channel shifts.

Alongside these, we reviewed company filings and investor presentations to understand category exposure, pricing commentary, and region mix, which then helped shape realistic ranges for volume and price movement. A paid subscription covering company financials and intelligence was used selectively to standardize revenue splits when public disclosures were uneven, and a patent database was checked for directional signals around packaging and shelf-life claims. The desk sources listed here are not exhaustive, and we also used additional public references for data collection, validation, and clarification during analysis.

Primary Interviews and Surveys

Primary work was used to pressure-test what we saw in published data, especially around price realization, private label intensity, and how demand shifted between at-home meals and away-from-home eating. We spoke with a mix of manufacturers, ingredient and packaging participants, distributors, and retail-facing roles across major regions, so the assumptions on volumes, channel mix, and format shifts could be corrected before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | APAC: 42% |

| Mid tier: 45% | Functional/Unit leaders: 41% | EMEA: 34% |

| Smaller Players: 17% | Managers: 47% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where packaged food consumption and retail spend signals are used to reconstruct the demand pool for packaged soups by country, and then rolled up to regions and global totals. Once that structure was in place, results were cross-checked with selective bottom-up approximations, such as sampled country volumes multiplied by observed retail price bands, and supplier and channel checks that help confirm whether the totals look realistic.

Key inputs used in the model include retail price inflation and realized price progression, mix shifts between dry soups and ready-to-eat wet soups, penetration of modern retail and e-commerce for packaged foods, household and working-population indicators tied to convenience foods, and seasonality patterns that influence soup demand in colder months. When some indicators were missing for a smaller market, proxy variables from comparable countries were used, and then corrected through interviews before being accepted.

For forecasting, scenario analysis was used so the outlook stays readable and practical, with each scenario anchored to expected price inflation, packaging and distribution changes, and consumer down-trading or premiumization trends discussed by interviewees. The final forecast is then reconciled back to the historical path so step changes are explained rather than hidden inside a single growth rate.

Data Validation & Update Cycle

Validation is done through a set of cross-checks that compare the modeled market totals against independent signals like packaged food retail trends, trade movements for relevant processed food categories, and the direction of company commentary on volume and pricing. If a country shows an unusual jump, we trace the drivers back to inputs like inflation, channel share, or format mix, and we review assumptions again before sign-off.

A multi-step analyst review is followed so calculation logic, unit consistency, and currency conversions are checked cleanly. When material events occur, such as major pricing shocks, demand disruptions, or regulation changes affecting labeling and shelf life, we trigger targeted re-contact with experts to confirm what changed. Reports are refreshed annually, and right before delivery, a final pass is done to ensure the latest public information is reflected in the view shared with clients.

Mordor Intelligence's Soup Market Size Measured Against Other Published Estimates

Different published soup market values often do not match because the scope definition and the year chosen for the current size are not the same, and the pricing method can vary between studies. Some also mix retail sales with food-service consumption, which changes the total even if the product list looks similar.

The main gap comes from whether food-service soups and freshly prepared servings are included, and in Mordor Intelligence's model, only packaged retail soup formats sold through off-trade and e-commerce are counted, with restaurant and cafe servings kept out. Differences can also come from how ASP is moved forward, where some estimates apply a single global inflation factor instead of country-level price movement, and from how often assumptions are refreshed after major price spikes or channel shifts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.99 B (2026) | |

| Industry Publisher A | USD 18.30 B (2024) | Uses a different current-year anchor and appears to include a broader soup set that can blend packaged and freshly prepared options, which lifts totals versus a packaged-retail-only view. |

| Industry Data Provider B | USD 19.31 B (2024) | Retail-focused but anchored to 2024 and may apply different currency timing and category mapping across ambient, chilled, dried mixes, frozen, and UHT, which can shift value when compared to a later-year estimate. |

Taken together, the spread is mainly explained by scope choices and base-year timing, followed by how price progression is handled across countries and formats. By keeping the variables tied to observable retail demand signals and then stress-testing them with interviews, the estimate stays traceable and repeatable when the model is updated.

Key Questions Answered in the Report

How large is the global soup market in 2026?

The soup market size is USD 17.99 billion in 2026, and it is set to grow steadily through 2031.

Which product format is growing the fastest?

Chilled soup posts the highest CAGR at 1.88% because it marries fresh taste with grab-and-go convenience.

Why are pouches overtaking cans?

Pouches weigh less, reseal easily, and signal modernity, while advances in mono-material films address recycling concerns.

Which region adds the most incremental demand?

Asia-Pacific leads growth at a 3.14% CAGR as urban consumers adopt ready-to-eat solutions that fit tight schedules.

What health trend shapes new product launches?

Lower sodium and clean-label plant-based recipes dominate reformulation to meet FDA “healthy” criteria and consumer scrutiny.

Page last updated on: