White Mushroom Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 14.25 Billion |

| Market Size (2031) | USD 19.44 Billion |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

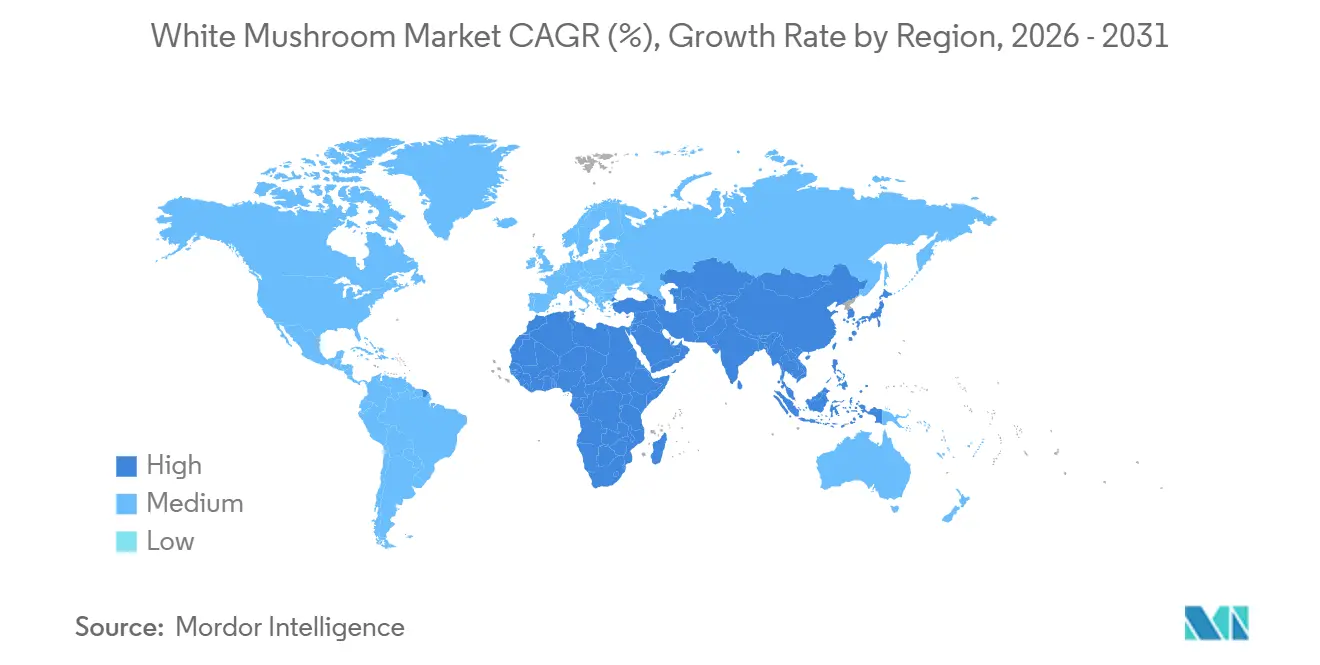

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

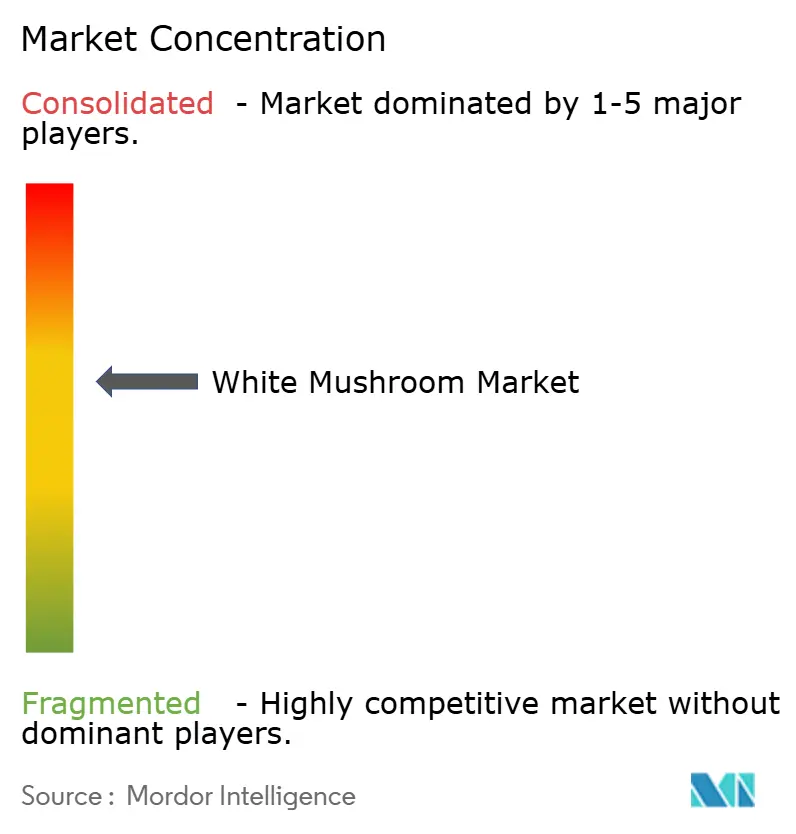

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

White Mushroom Market Analysis by Mordor Intelligence

The White Mushroom Market size is projected to be USD 13.16 billion in 2025, USD 14.52 billion in 2026, and reach USD 19.44 billion by 2031, growing at a CAGR of 6.41% from 2026 to 2031. This growth is fueled by dietary shifts favoring low-carbon proteins, retailer efforts to promote fresh produce, and the rising prominence of functional foods, particularly those fortified with vitamin D. Leading producers are implementing controlled-environment agriculture and circular strategies to cut costs, while retailers are expanding private-label offerings and enhancing online sales channels. However, rising input costs and cold-chain vulnerabilities are pressuring margins, prompting smaller operators to either optimize capacity or form partnerships to scale. Consequently, competition is increasingly driven by advancements in technology, substrate innovations, and the ability to generate value from spent mushroom substrates through energy and fertilizer co-products.

Key Report Takeaways

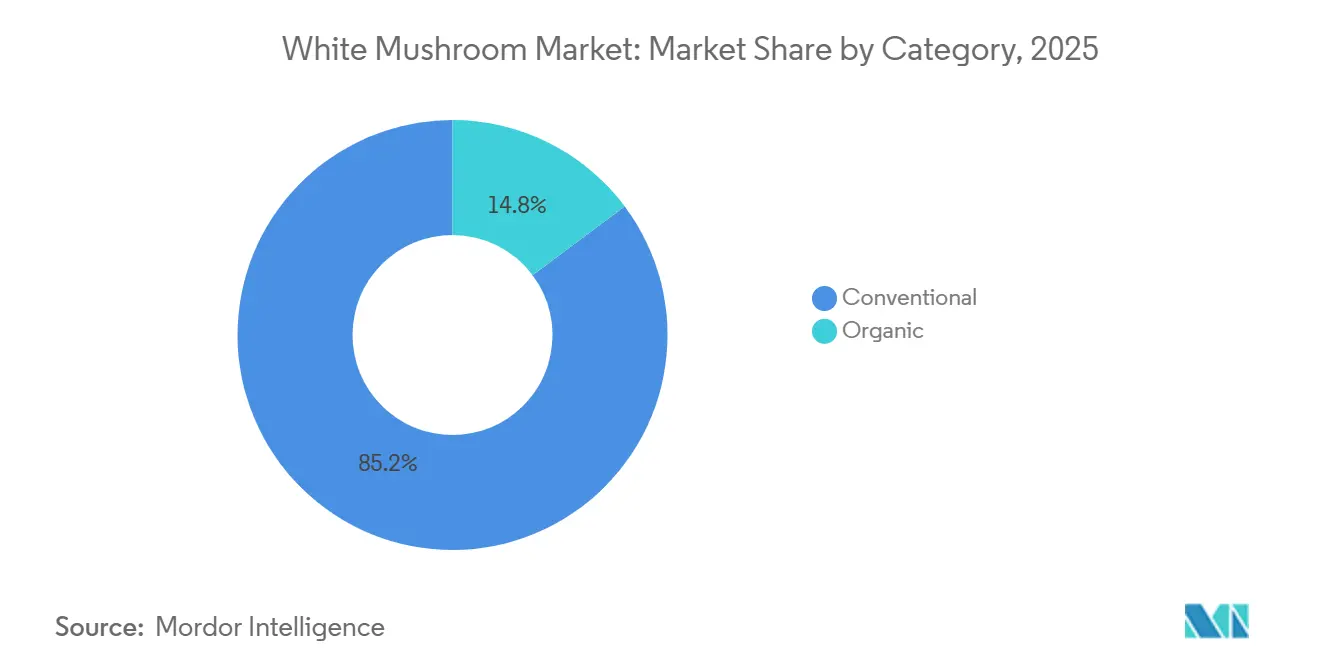

- By category, conventional mushrooms commanded 85.21% of 2025 revenue, whereas organic is forecast to advance at a 7.20% CAGR through 2031.

- By form, fresh formats held 66.04% of the 2025 white mushroom market share, and dried formats are projected to register an 8.22% CAGR over 2026-2031.

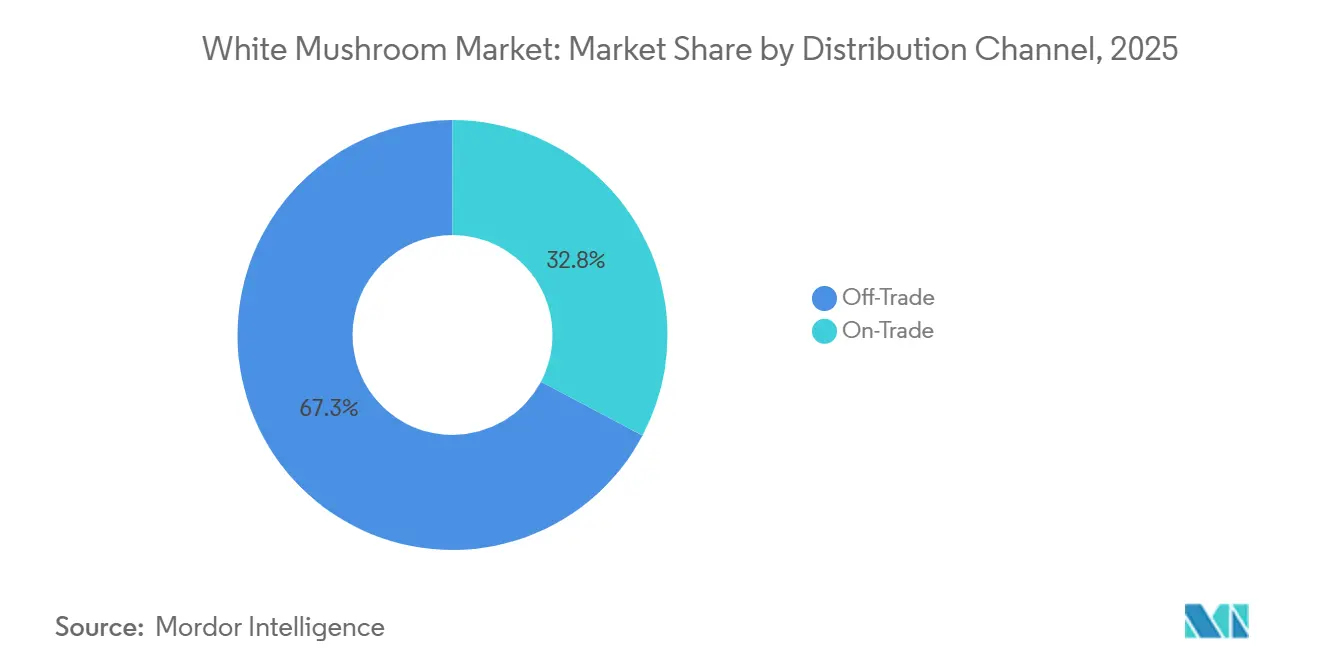

- By distribution channel, off-trade retail captured 41.30% of value in 2025, while on-trade foodservice is expected to post a 6.64% CAGR to 2031.

- By geography, Asia-Pacific held 60.28% of the 2025 white mushroom market share, and the Middle East and Africa are projected to register a 6.82% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global White Mushroom Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating consumer shift toward plant-based protein | +1.2% | Global, with early gains in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rapid expansion of organized retail and private-label SKUs | +0.9% | North America, Europe, and emerging Asia-Pacific (India, Indonesia, Thailand) | Short term (≤ 2 years) |

| Advances in controlled-environment agriculture lowering unit costs | +1.0% | North America, Europe, Middle East, and East Asia | Long term (≥ 4 years) |

| Functional-food positioning via vitamin-D fortification | +0.7% | North America, Europe, Japan, and Australia | Medium term (2-4 years) |

| AI-enabled predictive yield analytics in vertical farms | +0.5% | North America, Europe, and China (early adopters) | Long term (≥ 4 years) |

| Circular revenues from spent-substrate bio-fertiliser | +0.4% | Europe, North America, and select Asia-Pacific markets with biogas infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating consumer shift toward plant-based protein

White mushrooms are gaining prominence in the plant-based protein market, not as direct meat substitutes but as whole-food ingredients. They provide umami flavor, adaptable textures, and a favorable amino-acid profile, avoiding the processing concerns linked to extruded soy or pea isolates. The rising vegan population is driving the demand for mushrooms. For instance, the number of vegans in the UK grew by 1.1 million between 2023 and 2024, reaching 2.5 million, approximately 4.7% of the adult population, according to the Jewish, Vegan, Sustainable Organization[1]Source: Jewish, Vegan, Sustainable Organization, "Veganism on the Rise in the UK", jvs.org.uk. Foodservice innovations are enhancing this protein positioning. Quick-service and fast-casual chains are incorporating mushrooms into burger patties and plant-forward bowls, reducing beef content by 20-30% while maintaining taste and texture. This strategy has been validated through multiple pilot programs in North America and Europe during 2024-2025. On the regulatory side, the FDA has approved health claims linking mushroom consumption to improved immune function and cardiovascular health. However, manufacturers must validate these claims by demonstrating bioactive content through standardized testing. This regulatory framework particularly supports vertically integrated producers with in-house analytical capabilities.

Rapid expansion of organized retail and private-label SKUs

Organized retail penetration is redefining the distribution economics of white mushrooms, particularly in emerging Asia-Pacific markets. Modern trade formats, supported by the growth of supermarket chains in India, Indonesia, and Thailand, have increased their share of fresh-produce sales from 38% in 2023 to a projected 43% in 2025. This shift challenges mid-tier branded producers who lack scale or differentiation, pushing them to either consolidate or focus on niche markets such as organic, specialty, or value-added products. Additionally, the rise of private labels has significantly expanded SKU variety. Leading retailers now stock 8-12 mushroom SKUs per store, covering sliced, whole, organic, and pre-portioned options, compared to 4-6 SKUs a decade ago, catering to the growing demand for convenience. E-commerce is further driving this trend. In the U.S., nonstore retail sales are surpassing traditional brick-and-mortar channels, enabling direct-to-consumer models that eliminate traditional distributor markups.

Advances in controlled-environment agriculture lowering unit costs

Optimized facilities have achieved significant cost reductions by installing LED arrays and heat-recovery ventilation systems, bringing the cost per kilogram down to EUR 0.85-1.75 (USD 0.92-1.90) from EUR 1.20-2.10 in 2022. These upgrades have also decreased electricity consumption to below 8 kWh/kg, enhancing operational efficiency. In a move that underscores the importance of high-efficiency infrastructure in water-scarce regions, Saudi Arabia’s development bank has committed USD 400 million to greenhouse and vertical-farm projects. Additionally, the adoption of modular designs has reduced upfront capital requirements by 30-40%, shortening payback periods to approximately five years and making these projects more attractive to institutional investors. Together, these advancements are flattening the supply curve and strengthening the long-term competitiveness of the white mushroom market, particularly when compared to animal protein.

Functional-food positioning via vitamin-D fortification

According to the WHO, nearly 1 billion people globally grapple with vitamin D deficiency, spurring a surge in demand for food-based solutions that offer an alternative to traditional pills[2]Source: Food and Agriculture Organization, “Vitamin D Deficiency,” who.int. Regulatory approvals in the U.S., EU, and UK have facilitated the mainstream adoption of Vitamin D fortification in white mushrooms. These approvals establish standardized protocols to ensure mushrooms provide 400-800 IU of vitamin D₂ per 100-gram serving. In December 2024, Monterey Mushrooms submitted a food-additive petition to the FDA to amend 21 CFR 172.382. The petition seeks approval to expose sliced or diced Agaricus bisporus mushrooms to UV light during processing. This approach enables vitamin D fortification at the packing stage, streamlining production and increasing market potential. In North America and Europe, these fortified mushrooms are sold at a premium price. Millennials and Gen Z consumers, who value nutrient density and clean-label ingredients, exhibit the highest willingness to pay. Clinical research collaborations are gaining momentum. For instance, Farlong Holding Corporation signed a USD 137,750 preclinical study agreement with City of Hope in October 2024. This study aims to evaluate white button mushroom extract for immune-support applications, reflecting a growing interest in bioactive compound extraction and nutraceutical product innovation. The DSHEA regulatory framework in the U.S. and the EU's Novel Food Regulation provide pathways for structure-function claims. However, producers with strong analytical and clinical-trial capabilities are better positioned to meet the substantiation requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High perishability and cold-chain gaps | -0.8% | Sub-Saharan Africa, South Asia, and Latin America (excluding Brazil, Argentina) | Short term (≤ 2 years) |

| Rising energy and labour costs in climate-controlled cultivation | -0.6% | Europe, North America, and developed Asia-Pacific (Japan, South Korea, Australia) | Medium term (2-4 years) |

| Market price volatility driven by seasonal oversupply | -0.4% | Global, with acute effects in China, North America, and Europe during Q2-Q3 | Short term (≤ 2 years) |

| Regulatory squeeze on peat-moss casing supply | -0.3% | United Kingdom, European Union, and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High perishability and cold-chain gaps

Fresh white mushrooms, when stored under optimal refrigeration conditions (at 2-4°C and 95% relative humidity), have a shelf life of 5-7 days. However, the cold-chain infrastructure in Sub-Saharan Africa and South Asia is fragmented. This fragmentation results in postharvest losses of up to 37% for fresh produce, driven by inadequate refrigerated transport, unreliable electricity supply, and insufficient cold-storage capacity at retail points. These infrastructural gaps limit market penetration in regions with favorable demographics and growing protein demand. Growers face a difficult choice: invest significantly in cold-chain assets or endure reduced margins due to spoilage and distressed sales. According to the World Bank, bridging the cold-chain gap in developing economies would require USD 150-200 billion in cumulative infrastructure investments by 2030. This financial challenge is further exacerbated by low returns on rural cold-storage facilities and regulatory uncertainties surrounding public-private partnership frameworks. Processed formats, such as canned, dried, and frozen, offer partial relief, but consumer preferences in emerging markets strongly favor fresh mushrooms. Fresh mushrooms account for 55-70% of retail volume in the Asia-Pacific and Latin America regions, limiting the potential market for shelf-stable alternatives. Additionally, the fragility of the cold-chain increases food-safety risks. Temperature fluctuations during distribution promote microbial growth, leading to retailer rejections and damage to brand reputation. This issue disproportionately impacts smaller growers who lack vertical integration into logistics.

Rising energy and labour costs in climate-controlled cultivation

During 2024-2025, energy costs for climate-controlled mushroom cultivation in the EU increased by 8-12%. This rise was driven by the rebound of industrial electricity prices from pandemic-induced lows and the impact of carbon pricing mechanisms, which elevated fossil-fuel generation costs. Growers relying on grid electricity instead of on-site renewable sources experienced significant margin pressures. At the same time, labor costs in North America and Western Europe grew by 5-7% annually. This growth was attributed to minimum-wage increases, stricter immigration policies that reduced the agricultural workforce supply, and competition from the warehouse and logistics sectors, which offered comparable wages in less physically demanding roles. These combined cost pressures raised the break-even price for fresh white mushrooms by USD 0.20-0.35 per kilogram in high-cost regions. However, due to the commoditized nature of conventional white mushrooms and the strong pricing power of supermarket chains, growers could not fully pass these costs onto retail buyers. Automation provides some relief, with robotic harvesting systems now capable of picking 80-120 kilograms per hour compared to 40-60 kilograms by manual labor. However, the upfront capital investment of USD 150,000-250,000 per robotic unit limits adoption to large-scale operations producing over 2,000 tonnes annually. Additionally, renewable energy integration, such as on-site solar arrays and biogas cogeneration from spent mushroom substrate, can reduce grid electricity dependence by 40-60%. Despite this, payback periods of 6-8 years deter investment in markets with volatile electricity prices or uncertain subsidy frameworks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Conventional Scale Versus Organic Momentum

In 2025, conventional supply dominated the market landscape, accounting for 85.21% of the total revenue. This stronghold was primarily supported by long-term contracts for wheat straw and manure, which effectively kept production costs 20-30% lower compared to organic alternatives. Foodservice buyers, who prioritize price stability, further reinforced the leadership of conventional supply in terms of volume. However, this dominance is facing challenges as pesticide-reduction targets under the EU's Farm to Fork Strategy and the increasing influence of private-label brands are exerting pressure on profit margins.

Although organic white mushrooms currently represent a smaller share of the market, they are projected to grow at a compound annual growth rate (CAGR) of 7.20% during the forecast period of 2026-2031. This growth rate exceeds that of conventional mushrooms by 60 basis points, driven by the development of certification infrastructure and a growing consumer willingness to pay a premium for organic produce, particularly in North America, Europe, and urban areas of the Asia-Pacific region. While certification processes increase production costs by 15-25%, they enable growers to command shelf premiums of 30-50%, ensuring attractive profit margins for integrated producers. Additionally, the emergence of shelf-stable organic formats is addressing cold-chain limitations in regions such as Asia and Africa, unlocking opportunities for market expansion in these under-penetrated geographies.

By Form: Fresh Core, Dried Acceleration

In 2025, the fresh segment contributed 66.04% of total sales, establishing itself as the primary driver of consumer engagement and impulse purchases. However, supermarkets are grappling with spoilage losses ranging from 8% to 12%, primarily due to insufficient humidity control measures. This issue is prompting retailers to adopt modified-atmosphere packaging and sliced stock-keeping units (SKUs), which not only mitigate spoilage but also offer the advantage of higher profit margins.

The dried product segment is projected to grow at a compound annual growth rate (CAGR) of 8.22%, driven by increasing demand in regions where refrigeration infrastructure is either expensive or unreliable. Recent advancements in freeze-dry technology have enabled the preservation of up to 95% of original micronutrients, including fortified vitamin D, making these products highly suitable for inclusion in packaged soups and meal kits. Additionally, the adoption of lightweight, ambient-temperature shipping methods has significantly reduced e-commerce logistics costs by up to 60%. This cost reduction allows direct-to-consumer brands to efficiently cater to health-conscious consumers while bypassing distributor mark-ups, thereby enhancing their market reach and profitability.

By Distribution Channel: Retail Strength, Foodservice Rebound

In 2025, off-trade outlets, which include supermarkets, hypermarkets, convenience stores, and online platforms, represented 41.30% of the market's total value. Supermarkets currently dominate this space, but online grocery shopping is emerging as the fastest-growing segment. This surge is largely attributed to the rising popularity of same-day cold delivery services and subscription-based purchasing models, both of which offer added convenience to consumers. Furthermore, the increasing penetration of the internet bolsters these online retail channels. For instance, data from the International Telecommunication Union (ITU) highlights a rise in global internet access: 74% of the population was online in 2025, up from 71% in 2024[3]Source: International Telecommunication Union (ITU), "Individuals Using Internet", itu.int. Moreover, the growing presence of private-label products in off-trade channels is not only shaping pricing strategies but also expanding the variety of stock-keeping units (SKUs) available to consumers.

On-trade channels are witnessing a robust resurgence, evidenced by a 6.64% year-over-year uptick in U.S. foodservice sales in January 2026. Menu innovations are spotlighting mushroom blends as a sustainable substitute to curtail beef consumption. Concurrently, premium restaurants are turning to organic and specialty-grade ingredients, aiming to set their dishes apart and cater to a more discerning clientele. The foodservice distribution channel, emphasizing just-in-time delivery, commands prices up to 25% higher per kilogram than retail. This pricing trend, combined with the resurgence of dining-out habits, positions the foodservice channel as a lucrative growth avenue for market players.

Geography Analysis

In 2025, the Asia-Pacific region led the global white mushroom market, contributing 60.28% of its value. This leadership is primarily due to China's extensive industrial-scale production infrastructure and Japan's significant per capita consumption of fresh and processed mushrooms. In China, market concentration is high, with Zhongxing Mushroom Industry and Yuguang, the top producers, collectively controlling 55% of domestic capacity. This dominance enables effective supply management and pricing stability, particularly during periods of weaker demand. Japan's Ministry of Agriculture, Forestry and Fisheries reported stable mushroom marketing quantities for 2024-2025. Fresh white mushrooms represented 12-15% of total edible fungi consumption, driven by their integration into traditional dishes like nabemono and tempura, as well as modern fusion cuisine. India and Southeast Asia are emerging as high-growth sub-regions, where organized retail expansion and rising middle-class incomes are boosting fresh mushroom adoption. However, production scalability faces challenges due to gaps in cold-chain logistics and substrate supply infrastructure. Australia and New Zealand have established themselves as premium export markets. Despite a 6-8% annual increase in import values during 2024-2025, domestic production falls short of meeting demand from foodservice and retail sectors, which increasingly prioritize locally sourced, organic, and specialty mushroom varieties.

North America and Europe exhibit mature consumption patterns, characterized by high per capita availability and advanced retail distribution systems. In Europe, markets are divided between high-volume conventional production in the Netherlands, Poland, and Ireland, and premium organic and specialty production in France, Germany, and the UK. A significant industry development occurred in November 2024 when Monaghan Mushrooms, one of Europe's largest producers, introduced a peat-free substrate formulation. This innovation positions the company to comply with the UK's upcoming peat ban while maintaining yield and quality standards. As environmental regulations tighten across the EU, this technological advancement could transform substrate sourcing practices throughout the region.

Although the Middle East and Africa hold a smaller share of the market, they are projected to grow at the fastest rate, with a 6.82% CAGR forecast for 2026-2031. This growth is driven by sovereign investments in food security and increasing import demand, particularly in Gulf Cooperation Council economies. Saudi Arabia, which imports approximately 80% of its food supply, is prioritizing controlled-environment agriculture. In 2023, the Agricultural Development Fund approved loans totaling 1.5 billion SAR (USD 400 million) to support greenhouse, vertical farming, and hydroponic projects, including advanced mushroom cultivation facilities designed for desert climates with minimal water usage. Similarly, the UAE and Qatar are leveraging sovereign wealth to develop climate-controlled growing facilities, aiming to reduce import dependence and enhance supply-chain resilience during geopolitical disruptions. In Sub-Saharan Africa, production is concentrated in South Africa, Kenya, and Nigeria, but the market remains underdeveloped. Despite the availability of agricultural waste substrates like maize stalks and rice husks, which are suitable for mushroom cultivation, inadequate cold-chain infrastructure and low consumer awareness limit market penetration.

Competitive Landscape

The white mushroom market's moderate fragmentation creates significant opportunities for consolidation and strategic initiatives by industry leaders. Key players such as Monaghan Mushrooms, Bonduelle Group, Giorgio Fresh Co., Costa Group (Costa Mushrooms), and Shanghai Finc Bio-Tech dominate the market. These companies efficiently manage spawn production, substrate, cultivation, and distribution, strengthening their bargaining position with retailers. Their adoption of AI-driven climate controls not only lowers costs and improves yields but also increases the competitive gap with smaller growers. At the same time, consolidators are focusing on family-run farms without succession plans, offering 6-8× EBITDA multiples to integrate these farms into their national networks seamlessly.

Advancements in functional foods set industry leaders apart: Monterey Mushrooms launched an FDA-approved vitamin D2 powder, while Infinite Roots secured USD 58 million to scale its asset-light mycelium fermentation model, as reported by AGFUNDERNEWS.COM. Sustainability remains a key focus; Bonduelle is utilizing SMS in biogas digesters to cut Scope 1 emissions and attract ESG-focused investors. Start-ups like Eden Grow Systems are capitalizing on hydroponic Mycoponics™ racks, which deliver 25% greater space efficiency, and are prioritizing tech-licensing agreements over traditional, capital-intensive farming.

The growing share of private-label products is increasing retailer influence, prompting manufacturers to develop exclusive varietals and provide detailed category insights. Innovative players are partnering with e-grocers to ensure timely deliveries, reduce shrinkage, and leverage shopper data. In emerging markets, collaborations with local producers not only facilitate market entry but also mitigate risks from currency fluctuations. While automation tends to favor well-capitalized incumbents, niche artisans focusing on premium varietals and agritourism ventures continue to find opportunities for growth.

White Mushroom Industry Leaders

-

Monaghan Mushrooms

-

Bonduelle Group

-

Giorgio Fresh Co.

-

Costa Group (Costa Mushrooms)

-

Shanghai Finc Bio-Tech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Infinite Roots secured USD 58 million Series B funding to scale its mycelium fermentation platform for asset-light production expansion.

- October 2024: CSIRO-backed Hi-D startup advanced UV-exposed mushroom vitamin-D products for India’s supplement market

- September 2024: Eden Grow Systems launched MyCo subsidiary to commercialize Mycoponics™ hydroponic cultivation for yield gains and cost savings.

Global White Mushroom Market Report Scope

White mushrooms, scientifically known as Agaricus Bisporus, are the most common, mild-flavored, and widely consumed edible fungi globally. . The global white mushroom market report is segmented by category, form, distribution channels, and geography. By category, the market is segmented into organic and conventional. By form, the market is segmented by fresh, canned, dried, and frozen. By distribution channel, the market is segmented into on-trade and off-trade. By geography, the market is segmented by North America, Europe, Asia-Pacific, South America, the Middle East and Africa. For each segment, the market forecasts are provided in terms of value (USD) and volume (tons).

| Organic |

| Conventional |

| Fresh |

| Canned |

| Dried |

| Frozen |

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience and Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Category | Organic | |

| Conventional | ||

| By Form | Fresh | |

| Canned | ||

| Dried | ||

| Frozen | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Convenience and Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the white mushroom market in 2031?

It is forecast to reach USD 19.44 billion by 2031 at a 6.41% CAGR during 2026-2031.

Which category is growing fastest within global supply?

Organic white mushrooms are expected to post a 7.20% CAGR through 2031, outpacing conventional supply.

Why are dried formats gaining traction in emerging economies?

Shelf stability, lower freight costs, and improved nutrient retention let dried mushrooms bypass cold-chain gaps and grow at a 8.22% CAGR.

How are retailers influencing pricing dynamics?

Private-label penetration now tops 30% in Western Europe, enabling supermarkets to undercut branded prices by up to 20%.

Page last updated on: