Panama Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.58 Billion |

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

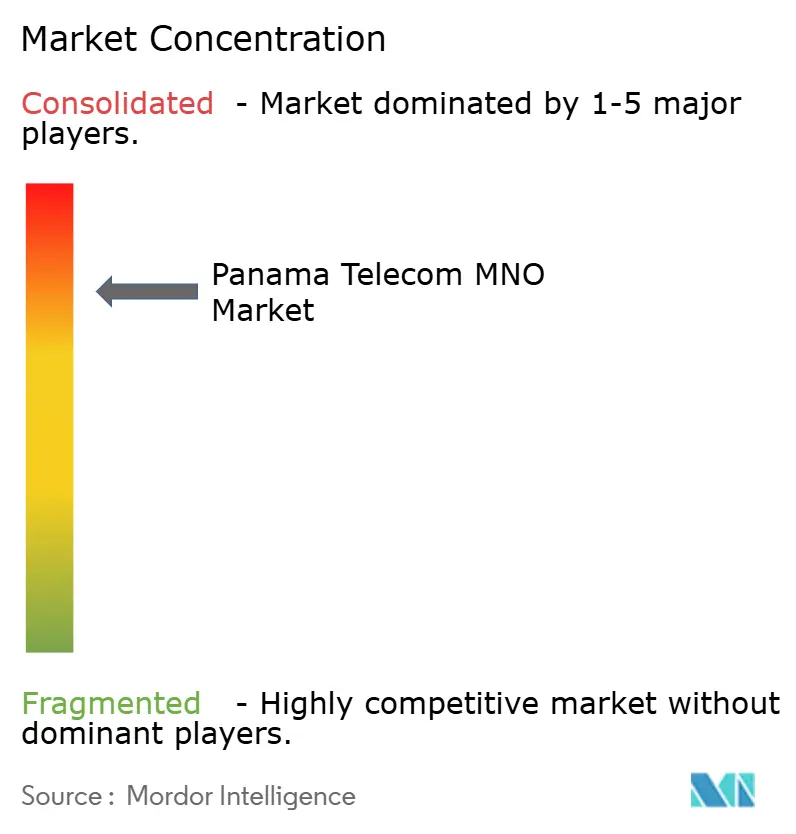

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Panama Telecom MNO Market Analysis by Mordor Intelligence

The Panama Telecom MNO Market size was valued at USD 1.58 billion in 2025 and estimated to grow from USD 1.65 billion in 2026 to reach USD 2.07 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031).

Shifts from voice-centric packages to data-heavy bundles, rising enterprise cloud connectivity requirements, and the government’s e-service modernization push all fuel demand, while Panama’s position as a regional digital hub attracts submarine cable investments that strengthen international backbones. Market consolidation from four to three mobile network operators (MNOs) heightens competitive intensity but also improves capital efficiency, enabling faster 5G roll-outs and wider fiber footprints. Consumer adoption of fixed–mobile converged bundles supports average revenue per user (ARPU) recovery, and infrastructure-sharing agreements such as Liberty Latin America’s tower sale unlock balance-sheet flexibility for network densification. Regulatory focus on spectrum auctions for the 2.5 GHz and 3.5 GHz bands in 2025 promises nationwide advanced mobile broadband, although near-term uncertainty around mobile virtual network operator (MVNO) pricing frameworks presents headwinds.

Key Report Takeaways

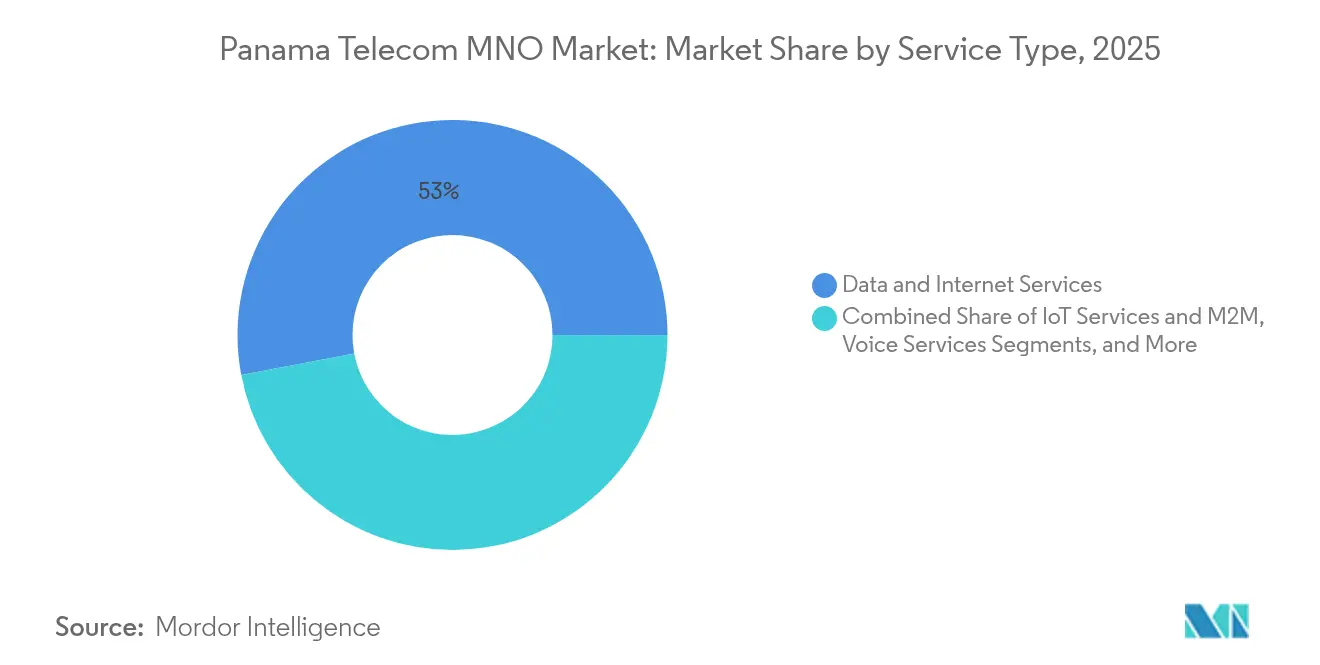

- By service type, data and internet services commanded 52.98% of Panama Telecom MNO market share in 2025 and continue to anchor revenue growth through 2031. OTT and PayTV services are the fastest-growing service type, expanding at a 4.78% CAGR between 2026 and 2031, driven by streaming video adoption and fixed–mobile converged offers.

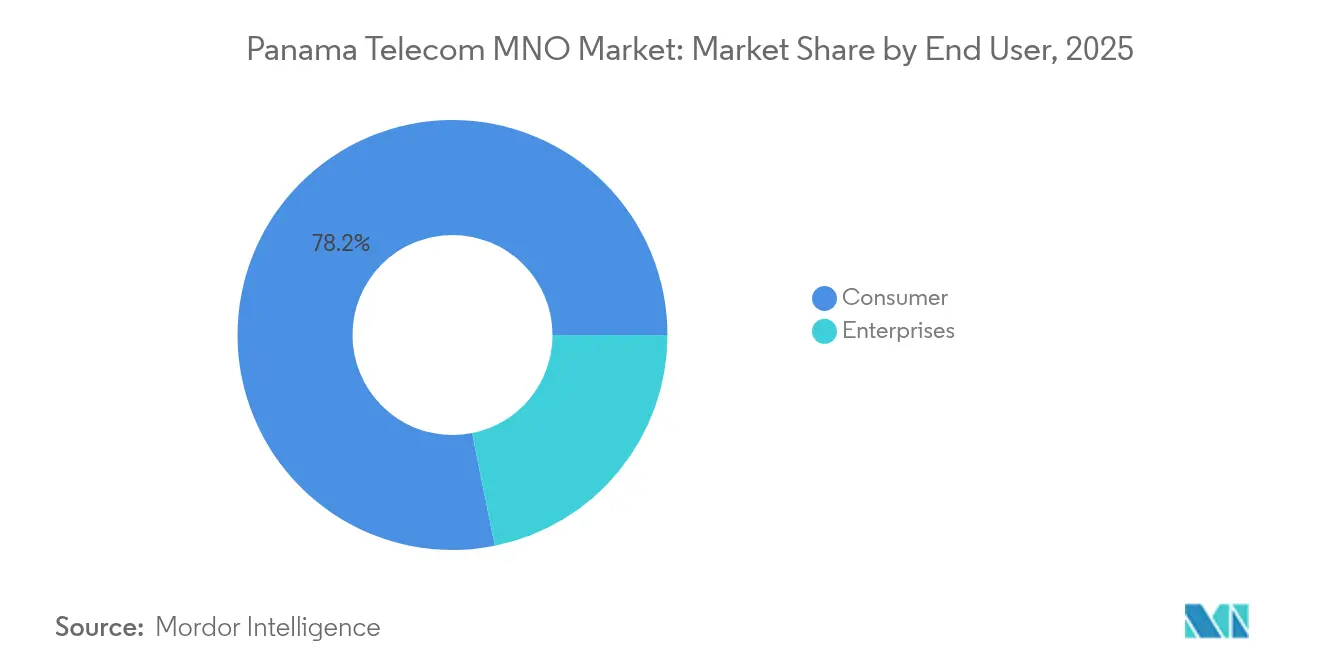

- By end user, the consumer segment captured 78.15% of the Panama Telecom MNO market size in 2025, while the enterprise segment is projected to rise at a 5.18% CAGR through 2031 on the back of cloud, IoT, and cybersecurity spend.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Panama Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-Data-Led ARPU Stabilization | +1.2% | Panama City, Colón | Medium term (2-4 years) |

| Enterprise Cloud-Connectivity Demand | +0.9% | Nationwide (Panama City, Colón Free Zone) | Short term (≤ 2 years) |

| E-government Digitalization Push | +0.7% | Nationwide | Medium term (2-4 years) |

| Underground Fiber Roll-outs to Colón Free Zone | +0.5% | Colón Free Zone | Long term (≥ 4 years) |

| Regional Submarine Cable Landings | +0.4% | Nationwide | Long term (≥ 4 years) |

| Converged FWA + 5G Home Broadband Bundles | +0.3% | Urban and suburban zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mobile-Data-Led ARPU Stabilization

ARPU began recovering after years of voice revenue decline as operators monetized mobile data through tiered and unlimited plans. +Móvil’s 5G launch across 366 Panama City sites recorded average down-link speeds of 18.7 Mbps, materially ahead of rivals and supporting premium pricing. [1]Opensignal, “Mobile Network Experience Report Panama,” opensignal.comTigo’s B/. 28 postpaid unlimited plan reduces churn while lifting blended ARPU, and Millicom’s enterprise-grade managed connectivity adds high-margin B2B revenue. Dynamic spectrum sharing lets carriers exploit existing holdings pending new 5G awards, accelerating monetization without incremental spectrum cost. The resulting revenue uplift improves cash flow, funding wider 5G coverage that reinforces the virtuous cycle of speed, usage, and ARPU growth.

Enterprise Cloud-Connectivity Demand

Panama’s 5,500 m² Digital Gateway data center opened with 3.5 MW of scalable power, positioning the country as a regional interconnection node and spurring demand for dedicated enterprise links. [2]Sparkle, “Panama Digital Gateway Launches Operations,” sparkle.comNear-shore service providers such as Prodapt expanded local operations to support cloud-native telecom workloads, adding traffic that conventional broadband cannot handle. IoT deployments in logistics and port automation generate outsized economic impact, and studies show a 10-percentage-point rise in IoT connections can lift GDP by 0.7% in middle-income economies. Private LTE networks and edge computing capabilities thus emerge as differentiators for operators targeting financial and logistics customers in the Colón Free Zone.

E-government Digitalization Push

The USD 30 million Programa Panamá en Línea modernizes citizen interfaces while demanding robust, secure connectivity for hundreds of agencies. Starlink’s license to connect 1,000 schools illustrates how satellite-terrestrial hybrids address rural inclusion mandates. Government contracts bundle cybersecurity, cloud hosting, and managed services, creating sticky revenues for MNOs that meet strict service-level agreements. Universal service funds partially subsidize capital outlays, aligning economic incentives with public-policy goals and enhancing operator compliance with coverage obligations.

Underground Fiber Roll-outs to Colón Free Zone

UFINET’s purchase of Gold Data Panamá added city-center buried fiber to its 15,000 km national network, lowering maintenance costs and boosting service reliability for high-frequency trading and just-in-time logistics clients. Fiber depth protects against tropical weather-related outages, supporting premium SLAs that command higher margins than residential links. Wholesale leasing of dark fiber adds incremental revenue while optimizing asset utilization across the national backbone, advancing the Panama Telecom MNO market’s transition toward diversified income sources.

Restraints Impact Analysis*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Spectrum Fees and Universal Service Levies | -0.8% | Nationwide | Short term (≤ 2 years) |

| Rural Back-haul Economics | -0.6% | Indigenous territories | Long term (≥ 4 years) |

| Regulatory Uncertainty on MVNO Price Floors | -0.4% | Nationwide | Medium term (2-4 years) |

| Delayed Number Portability for Fixed Lines | -0.2% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Spectrum Fees and Universal Service Levies

ASEP’s upcoming 2.5 GHz and 3.5 GHz auctions could demand over USD 100 million in upfront fees, squeezing capex budgets needed for network densification. Universal service levies compound the burden by requiring cross-subsidized rural coverage, forcing operators to weigh near-term profitability against long-term 5G objectives. Smaller carriers face greater strain, raising barriers to entry and risking reduced service innovation just as data traffic surges.

Rural Back-haul Economics

Millicom connected 44,000 residents in indigenous areas but acknowledged limited revenue potential relative to investment outlay. [3] Sparse populations mean higher per-site opex, while low purchasing power constrains ARPU. Satellite back-haul mitigates distance but adds recurring costs that community users cannot sustain. Persistently high cost-to-serve delays universal coverage, widening the urban–rural digital gap and muting the Panama Telecom MNO market’s full demand potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data and internet services contributed 52.98% to Panama Telecom MNO market share in 2025 and remain the backbone of revenue expansion as streaming video, cloud usage, and social platforms dominate consumption patterns. The Panama Telecom MNO market size attributed to data services is projected to rise in line with 4.62% headline CAGR, supported by wider 4G coverage and initial 5G launches. Voice and messaging continue losing relevance as consumers migrate to app-based calling, while OTT and PayTV services record the quickest growth at 4.78% CAGR as Latin American SVoD subscriptions edge toward 165 million by 2029. IoT and machine-to-machine (M2M) traffic adds incremental data usage, especially in logistics operations centered on the Canal corridor. Regulatory directives mandating rural coverage compel operators to bundle zero-rating for educational and health portals, indirectly lifting data adoption in underserved regions.

Operators monetize surging usage through tiered speed buckets, unlimited plans with fair-usage thresholds, and content partnerships that zero-rate specific platforms. Converged fixed–mobile packages bundle fiber or FWA with mobile data, raising household ARPU and lowering churn. Wholesale data resale to MVNOs supplies new revenue, although uncertainty around floor pricing restrains agreement length. Enterprise SLAs embed latency and uptime guarantees that justify premium tariffs, reinforcing data’s central role in cash-flow growth within the Panama Telecom MNO market.

By End User: Enterprise Segment Accelerates Digital Transformation

The consumer base dominated the Panama Telecom MNO market size with a 78.15% share in 2025, yet the enterprise segment is forecast to outpace at a 5.18% CAGR as corporations digitize operations. Demand clusters in finance, logistics, and government, where secure, low-latency links support data-intensive workloads. Cloud migration drives MPLS to SD-WAN conversions, while IoT sensors in ports and free-zone warehouses necessitate always-on connectivity backed by stringent SLAs. Operators differentiate through fully managed services that bundle connectivity, cybersecurity, and analytics, lifting enterprise ARPU above consumer averages.

Fixed–mobile convergence for small businesses pairs fiber broadband with mobile voice and data, simplifying billing and improving wallet share. Multi-cloud strategies and local data residency rules push enterprises toward Panama-hosted facilities, increasing leased-line volumes. Rural schools and clinics funded under universal-service schemes represent another enterprise-ish opportunity wherein MNOs provide bundled access, maintenance, and support, blending public funding with commercial income and further diversifying the Panama Telecom MNO market’s revenue mix.

Geography Analysis

Panama’s location as the isthmus linking the Americas bestows unique advantages on the Panama Telecom MNO market. Urban centers such as Panama City and Colón host the majority of the 95% 4G population coverage, offering dense clusters of high-value subscribers who readily adopt early 5G services. +Móvil’s first 366 5G sites leverage dynamic spectrum sharing to deliver improved speeds while operators await mid-band assignments, underscoring an urban-first deployment model. Submarine systems like CSN-1 and Deep Blue One enrich international backbones, lowering wholesale bandwidth prices and broadening the Panama Telecom MNO market’s addressable enterprise base.

In contrast, only 39% of land area has reliable mobile broadband, spotlighting the rural connectivity gap. Government contracts with satellite providers such as Starlink supply links to 1,000 schools, blending satellite down-links with terrestrial last-mile distribution to meet universal access objectives. Indigenous regions rely on grant-funded solar-powered base stations, yet opex remains high given back-haul distances. The Colón Free Zone, Latin America’s largest, underpins a premium enterprise segment requiring redundant fiber loops and low-jitter connectivity for trade finance and real-time inventory control. Northern Caribbean coastlines, historically under-served, benefit indirectly from new submarine cable landings that enable lateral fiber spurs.

The dollarized economy removes foreign-exchange risk, bolstering long-term investor confidence in nationwide network expansion. ASEP’s infrastructure-sharing regulations encourage passive tower co-location in remote zones, reducing cost-to-serve and enabling sooner 5G coverage extension beyond metropolitan areas. As the Panama Telecom MNO market evolves, the strategic blending of high-capacity international routes with widened rural footprints positions the country as both a regional transit hub and a leader in Central American digital inclusion.

Competitive Landscape

Three nationwide operators now dominate the Panama Telecom MNO market after +Móvil’s USD 200 million acquisition of Claro Panama, producing a moderately concentrated field that still fosters innovation. Millicom (Tigo) leads with 2.6 million mobile lines and an integrated fixed-mobile play that underpins superior customer lifetime value. +Móvil, backed by Cable and Wireless Panama, pursues a network-quality differentiation strategy, front-running 5G launches and touting opensignal-verified speed advantages. Liberty Latin America focuses on capital-light expansion, monetizing 1,300 towers for USD 244 million to fund spectrum bids and fiber densification.

Competition has evolved from price wars toward service quality, bundled offers, and enterprise vertical solutions. Tower-sharing and active-RAN agreements lower deployment costs, allowing carriers to channel savings into software-defined networking and edge compute nodes that improve latency-sensitive applications. MVNO entrants target niche segments but pause expansion amid uncertainty over wholesale rate floors. International over-the-top providers partner with MNOs for carrier billing, generating ancillary revenue while stimulating data consumption. Regulatory clarity on 5G spectrum refarming and future auction timelines remains a focal point for strategic capital allocation across the Panama Telecom MNO market.

Operators increasingly collaborate with hyperscalers to host cloud on-ramps inside local data centers, locking in enterprise traffic and defending against neutral co-location facilities. Fiber-to-the-home (FTTH) builds in Panama City intensify platform competition with cable DOCSIS, enticing households through symmetrical gigabit speeds bundled with unlimited mobile data. Rural network economics spur joint ventures in open RAN, leveraging low-cost hardware to extend 4G coverage before migrating to 5G non-stand-alone. The evolving mix of alliances, spectrum strategy, and differentiated service portfolios points toward sustained yet rational rivalry that benefits both shareholders and consumers in the Panama Telecom MNO market.

Panama Telecom MNO Industry Leaders

+movil (Cable & Wireless)

Tigo Panama

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: UFINET completed the acquisition of 100% of GOLD DATA Panamá, adding strategic buried fiber to its 15,000 km national network Capacity Media.

- October 2024: +Móvil launched the initial phase of its 5G network across 366 Panama City sites using dynamic spectrum sharing Developing Telecoms.

- September 2024: Telconet’s CSN-1 submarine cable finalized Panama landings, linking Florida, Colombia, and Ecuador BNamericas.

- June 2024: Panama’s ICT Ministry granted new spectrum permits to seven companies, widening the competitive field.

Panama Telecom MNO Market Report Scope

The Panamanian telecom MNO market study tracks the revenue generated by major telecom companies in Panama through the sale of various services, including data, voice, messaging, and roaming, to end users. The analysis combines insights from both secondary research and primary sources. It delves into the key drivers and restraints shaping the market's growth trajectory.

The study monitors crucial market parameters, identifies growth drivers, and profiles key industry vendors. These insights underpin the market estimations and growth projections for the forecast period. In addition, the study provides market trends, along with key vendor profiles.

The study provides an in-depth analysis of the telecommunication industry in Panama. The Panamanian telecom MNO market is segmented by services (voice services (wired and wireless), data and messaging services, and OTT and PayTV services).

The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the forecast value of the Panama Telecom MNO market in 2031?

The market is projected to reach USD 2.07 billion by 2031, growing at a 4.62% CAGR.

Which service type currently generates the largest revenue share in Panama’s mobile sector?

Data and internet services lead with 52.98% share of total 2025 revenue.

How many nationwide operators compete after recent consolidation?

Three nationwide operators remain following +Móvil’s purchase of Claro Panama.

Why is the enterprise segment growing faster than consumer lines?

Enterprises increasingly adopt cloud, IoT, and managed security solutions that command higher ARPU and lift segment CAGR to 5.18%.

What spectrum bands is ASEP auctioning for 5G?

ASEP plans mid-2025 auctions for the 2.5 GHz and 3.5 GHz bands to enable advanced mobile broadband.

How do submarine cables benefit Panama’s telecom sector?

New landings lower wholesale bandwidth prices and enhance international connectivity, reinforcing Panama’s role as a regional digital hub.

Page last updated on: