Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.40 Billion |

| Market Size (2026) | USD 2.5 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Telecom MNO Market Analysis by Mordor Intelligence

Pakistan Telecom MNO Market size in 2026 is estimated at USD 2.5 billion, growing from 2025 value of USD 2.40 billion with 2031 projections showing USD 3.06 billion, growing at 4.11% CAGR over 2026-2031.

This healthy trajectory reflects sustained data consumption growth, the scheduled June 2025 5G launch, and regulator-driven quality-of-service mandates that are compelling operators to accelerate network upgrades. Rapid 4G migration, rising smartphone penetration, and an expanding digital-payments ecosystem are lifting average data usage per subscriber. At the same time, operators face a tight squeeze between dollar-denominated spectrum fees and rupee volatility, forcing careful tariff recalibration and energy-efficiency investments. Enterprise demand for private LTE and IoT connectivity in Pakistan’s industrial corridors is opening new, higher-margin revenue streams that diversify away from low-ARPU consumer voice. Intensifying competition among the four national MNOs, coupled with looming market consolidation through the proposed PTCL-Telenor transaction, underscores the need for differentiated digital services, especially mobile financial solutions and content bundles.

Key Report Takeaways

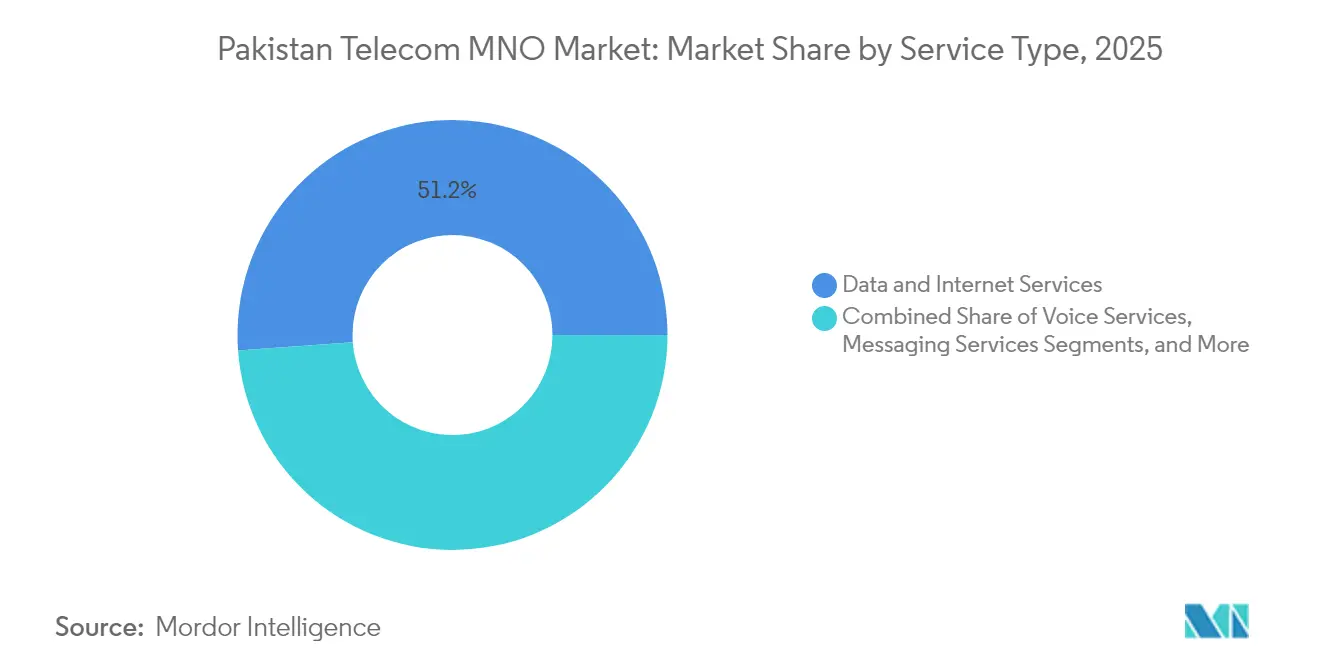

- By service type, data and internet services captured a 51.15% revenue share of the Pakistan telecom MNO market in 2025, whereas IoT and M2M services are advancing at a 4.18% CAGR through 2031.

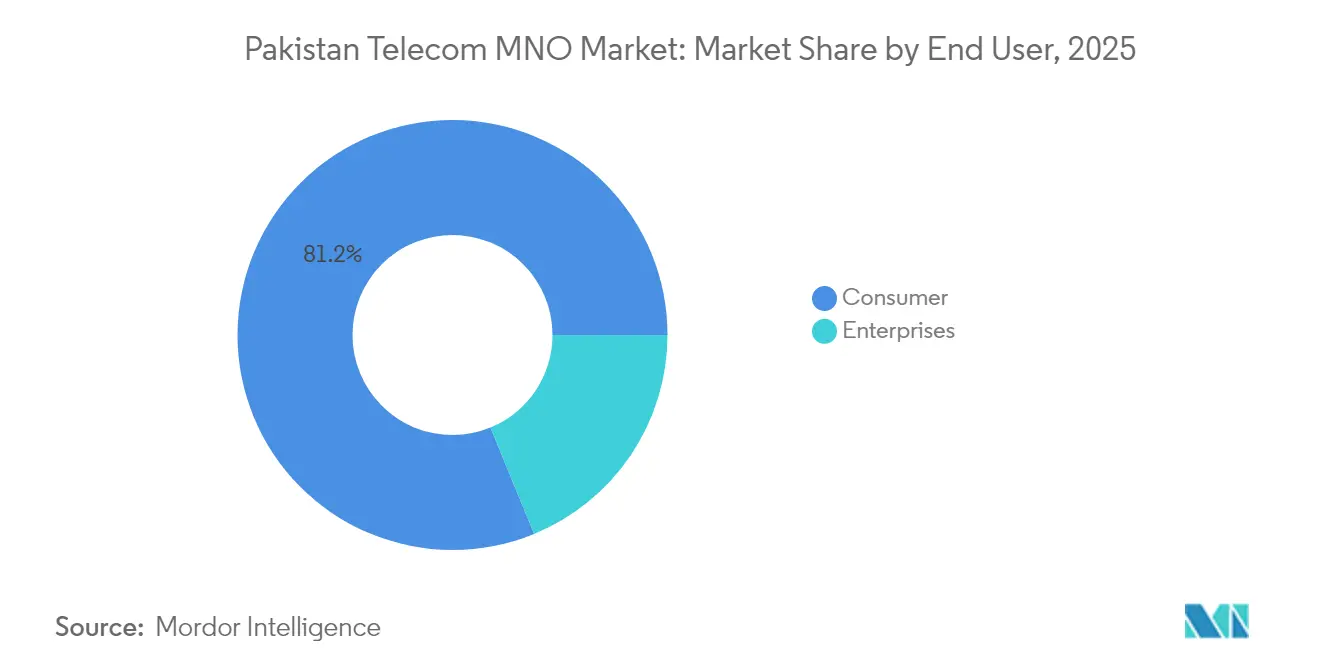

- By end user, consumer connections held 81.20% of the Pakistan telecom MNO market size in 2025, while enterprise subscriptions are expanding at a 4.59% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 4G/5G spectrum refarming and rollout commitments | +1.2% | National, with early deployment in Karachi, Lahore, Islamabad | Medium term (2-4 years) |

| Surge in mobile broadband consumption and digital-payments adoption | +1.5% | Urban centers expanding to tier-2 cities | Short term (≤ 2 years) |

| PTA-driven quality-of-service (QoS) enforcement boosting network CAPEX | +0.8% | National coverage areas, focused on network quality metrics | Medium term (2-4 years) |

| Enterprise push for private LTE/5G and IoT connectivity in manufacturing corridors | +0.6% | Industrial zones in Punjab, Sindh manufacturing hubs | Long term (≥ 4 years) |

| Growing diaspora traffic stimulating international voice and OTT bundles | +0.4% | Major urban centers with diaspora connections | Short term (≤ 2 years) |

| Nationwide fiber-to-tower programme unlocking backhaul bottlenecks | +0.7% | Rural and semi-urban areas, northern regions via CPEC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 4G/5G Spectrum Refarming and Rollout Commitments

Jazz completed its nationwide 3G switch-off in November 2024, freeing 900 MHz and 2100 MHz blocks for 4G, while the Ministry of IT and Telecom approved a June 2025 commercial 5G launch covering 700 MHz, 2300 MHz, 2600 MHz, and 3500 MHz bands valued at USD 831.8 million [1]Tahir Amin, “Jazz to phase out 3G services,” Business Recorder, brecorder.com. Coordinated refarming increases spectral efficiency, lowers per-bit cost, and accelerates nationwide 4G population coverage toward the PTA’s 98% target.

Surge in Mobile Broadband Consumption and Digital-Payments Adoption

Average monthly data use climbed to 4.3 GB per subscriber in FY 2024-25, a 68.9% jump year over year, while mobile banking transactions hit 1.69 billion during the same period [2]Attia Naveed, “Digital-payments surge,” Daily Times, dailytimes.com.pk . JazzCash’s 48 million registered wallets confirm how integrating payments with connectivity boosts stickiness and lifts blended ARPU above the sector’s USD 1 baseline.

PTA-Driven Quality-of-Service Enforcement Boosting Network CAPEX

The Pakistan Telecommunication Authority routinely publishes city-level KPIs and has fined operators for sub-par call-drop ratios, pushing capital intensity above 30% of service revenue in 2024. PTA also recognized Zong as the top performer in voice and data, encouraging a virtuous investment race that lifts nationwide network reliability.

Enterprise Push for Private LTE/5G and IoT Connectivity in Manufacturing Corridors

Jazz Business has rolled out industrial routers, NB-IoT trackers, and edge-cloud analytics packages for exporters clustered around Lahore and Karachi port zones. Edge connectivity allows real-time quality control and predictive maintenance, translating into measurable productivity gains that justify premium tariffs and multi-year contracts.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rupee volatility inflating dollar-denominated spectrum fees | -1.1% | National impact on all licensed operators | Short term (≤ 2 years) |

| Energy-cost spikes eroding EBITDA margins of tower/edge sites | -0.9% | National, particularly affecting rural tower operations | Medium term (2-4 years) |

| Delayed USF disbursements slowing rural coverage targets | -0.3% | Rural and underserved areas nationwide | Medium term (2-4 years) |

| Grey-routing via OTT side-loading curbing international call revenues | -0.5% | Urban centers with high OTT adoption rates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy-Cost Spikes Eroding EBITDA Margins of Tower and Edge Sites

Average utility tariffs rose 29% in FY 2024-25, and diesel costs increased a further 16%, inflating network OPEX by roughly PKR 18 billion across the four licensees. Hybrid solar-battery retrofits are underway but carry high upfront costs, slowing break-even and stretching balance sheets already burdened by foreign-currency debt.

Rupee Volatility Inflating Dollar-Denominated Spectrum Fees

The rupee lost 17% against the USD in 2024, forcing operators to find an extra PKR 44 billion to meet annual license-renewal installments pegged to the greenback [3]Kalbe Ali, “Telcos protest dollar-linked license fees,” Dawn, dawn.com. Operators warn that ARPU must rise to at least USD 1.5 to sustain capex requirements for 5G rollout without jeopardizing debt covenants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Sustain Dominance while IoT Gains Momentum

Data and internet services controlled a 51.15% share of the Pakistan telecom MNO market in 2025 and will remain the revenue anchor through 2031. Voice continues to contribute meaningful cash flows despite usage declines as operators pivot toward diaspora-oriented international bundles priced in hard currency. IoT and M2M connections represent only 1.3% of SIMs today but are growing fastest at a 4.18% CAGR. The agricultural cold-chain, smart metering, and fleet-tracking verticals are early adopters, and regulator-approved e-SIM frameworks should improve provisioning efficiency. Messaging revenue is shrinking because free OTT applications substitute SMS, yet bundled enterprise A2P services such as one-time-password delivery still generate sticky margins. OTT and PayTV gains reflect operator platforms that aggregate local dramas and sports rights, creating upsell paths beyond connectivity. These shifts confirm that data monetization, IoT enablement, and content bundling constitute the three pillars for sustaining top-line growth in a low-ARPU environment.

The IoT opportunity also elevates the importance of edge computing and narrowband spectrum allocations. Operators capable of integrating connectivity, devices, and analytics hold a first-mover advantage with export-oriented manufacturers subject to strict ISO traceability. In this context, the Pakistan telecom MNO market size for IoT services could surpass USD 191 million by 2031, albeit from a small base. Meanwhile, persistent rupee weakness adds urgency for operators to localize device supply chains to mitigate forex exposure, reinforcing the strategic value of domestic assembly partnerships.

By End User: Consumer Base Remains Foundation while Enterprise Accelerates

Consumers accounted for 81.20% of the Pakistan telecom MNO market share in 2025, translating into 193 million active SIMs. Smartphone penetration now exceeds 56%, and 4G users represent nearly 60% of total subscribers. Nonetheless, enterprise lines are expanding at a 4.59% CAGR, outpacing the overall subscriber base. Demand stems from manufacturers, logistics providers, and financial institutions that need guaranteed throughput, dedicated SLAs, and secure IoT overlays. The Universal Service Fund (USF) disbursed PKR 141.66 billion to expand rural fiber and LTE coverage, indirectly benefiting enterprise customers operating in secondary cities and export-processing zones.

Corporate digitization further lifts data center and cloud colocation demand, widening opportunities for operators with integrated connectivity-plus-cloud propositions. Jazz’s enterprise segment already delivers mid-teens EBITDA margins, well above the group’s consumer average. Over the forecast period, enterprise ARPU is projected to climb toward USD 21 per month, mitigating the chronic low consumer ARPU that hovers just under USD 1. The Pakistan telecom MNO industry, therefore, views enterprise engagement not merely as diversification but as a margin-accretive imperative.

Geography Analysis

Punjab and Sindh provinces generate almost 69.20% of sector revenue, thanks to dense urban clusters and relatively high disposable incomes. Punjab alone hosts 33% of total cell sites, and average 4G downlink rate of 19.9 Mbps in H1 2024, ranked highest nationwide. Faisalabad recorded peak speeds of 22 Mbps, underscoring the correlation between fiberized backhaul and throughput. Karachi maintains the greatest subscriber base but grapples with right-of-way delays that slow tower builds and cap spectral efficiency gains.

Khyber Pakhtunkhwa and Balochistan together account for just 11.20% of sector revenue, yet represent the largest untapped rural population. The USF’s 400-kilometer fiber-to-tower program, completed in December 2024, delivered backhaul to 646 remote sites, cutting diesel reliance by 18% and enabling LTE expansion. Operators continue to deploy solar-hybrid power systems in rugged, off-grid terrain, although security concerns inflate insurance premiums and extend project cycles.

The 820-kilometer cross-border fiber link with China has upgraded northern region connectivity, lowering latency for Gilgit-Baltistan e-commerce traffic and creating redundancy against submarine-cable outages. Upcoming Starlink service, slated for December 2025, may offer satellite backhaul for mountainous districts, though its PKR 25,000 (USD 146) monthly fee restricts mass uptake. Consequently, terrestrial MNOs maintain a price advantage in sparsely populated zones, provided they continue to leverage USF subsidies and shared-tower models to contain deployment costs.

Competitive Landscape

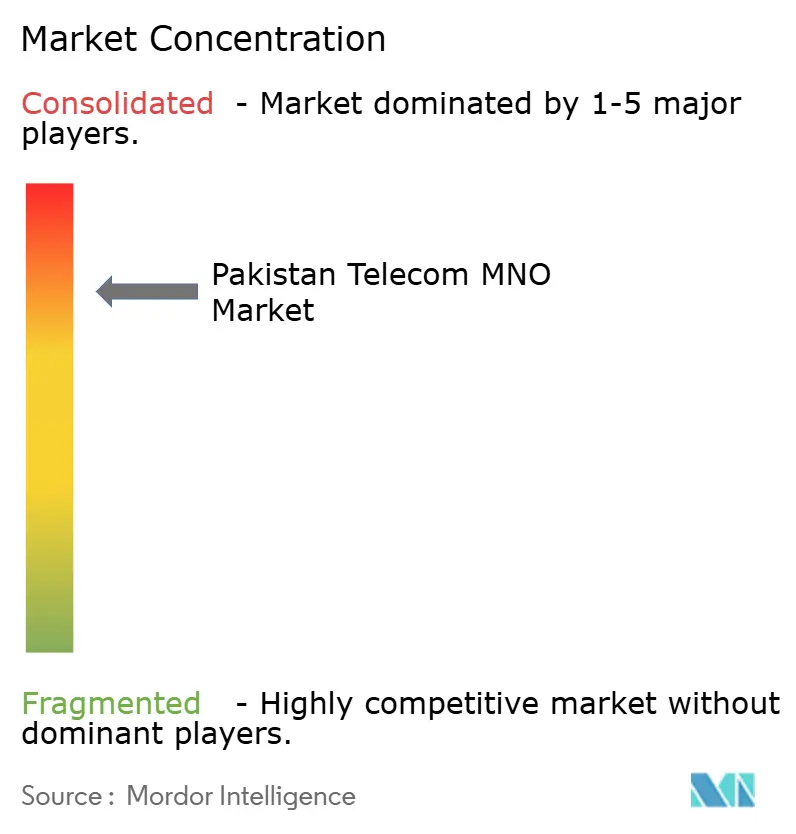

Pakistan’s telecom sector is a concentrated four-player arena where Jazz commands 66.4 million subscribers, Zong holds roughly 26%, and Ufone and Telenor share the remainder. The proposed PTCL-Telenor integration, financed by a USD 400 million IFC-led tranche, would merge Ufone’s mobile assets with Telenor’s 45 million customers and 13,000 towers, reducing the field to three national licensees. Jazz’s cumulative USD 9.6 billion capital outlay since 2016 underscores the investment threshold required for leadership, while VEON’s launch of ROX, a lifestyle-centric brand, signals a pivot toward digital engagement tailored to Pakistan’s under-30 demographic.

Competition increasingly revolves around spectrum depth, network quality scores, and value-added ecosystems. Zong’s 10×10 MHz holdings in both 1800 MHz and 2100 MHz bands underpin its “No.1 voice and data” award from PTA, whereas Jazz leverages its mobile-money scale to cross-sell loans and investments. PTCL Group is betting on fiber backhaul and cloud hosting to bundle end-to-end digital services for SMEs. Against this backdrop, energy cost inflation and FX liabilities drive collaborative tower sharing; Jazz and Zong already co-locate on 6,200 sites, and new passive-infrastructure joint ventures are under evaluation.

Regulatory scrutiny will intensify post-merger to safeguard consumer welfare. PTA’s draft Cyber Security Strategy 2023-2028 mandates ISO 27001 certification, centralized threat-intelligence sharing, and network-function-virtualization hardening, all of which raise compliance expenditure. Operators that can internalize these costs while sustaining capex on 5G and rural coverage are better positioned to defend share.

Pakistan Telecom MNO Industry Leaders

Jazz (Pakistan Mobile Communications Ltd)

Zong (CMPak)

Telenor Pakistan

Ufone (PTCL Group)

Special Communications Organization (SCO)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: PTA released the final 5G auction timetable confirming commercial launch in June 2025 across four spectrum bands, unlocking a USD 831.8 million investment round.

- October 2024: Jazz completed the country’s first full 3G shutdown, reallocating spectrum to boost 4G capacity under its “4G for All” program.

- September 2024: An IFC-led consortium committed USD 400 million to PTCL to fund the purchase of Telenor Pakistan and Orion Towers, accelerating market consolidation.

- February 2024: VEON debuted ROX, a digital-first brand aimed at Gen Z, bundling streaming, gaming, and payment features within a single app.

Pakistan Telecom MNO Market Report Scope

Telecom or Telecommunication is the long-range transmission of information by electromagnetic means.

Pakistan's Telecom MNO Market includes in-depth trend analysis based on connectivity like Fixed Networks, Mobile Networks, and Telecom Towers. The telecom services are divided into Voice Services (Wired and Wireless), Data and Messaging Services, and OTT and PayTV Services. The adoption of telecom services is likely driven by several factors, including an increasing demand for 5G.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Pakistan telecom MNO market in 2026?

The market stands at USD 2.5 billion in 2026 and is projected to reach USD 3.06 billion by 2031.

What is driving revenue growth for mobile operators?

Rapid data-usage growth, upcoming 5G services, and expanding fintech ecosystems are the primary growth engines.

Which service type holds the largest share?

Data and internet services represent 51.15% of 2025 revenue.

When will 5G services launch commercially?

The Ministry of IT and Telecom has set June 2025 for nationwide 5G rollout.

How will the PTCL-Telenor merger affect competition?

The merger will reduce national MNOs to three, raising market concentration to roughly 62%.

What challenges threaten operator profitability?

Dollar-denominated spectrum fees, energy-price inflation, and cyber-security compliance costs weigh on margins.

Page last updated on: