Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

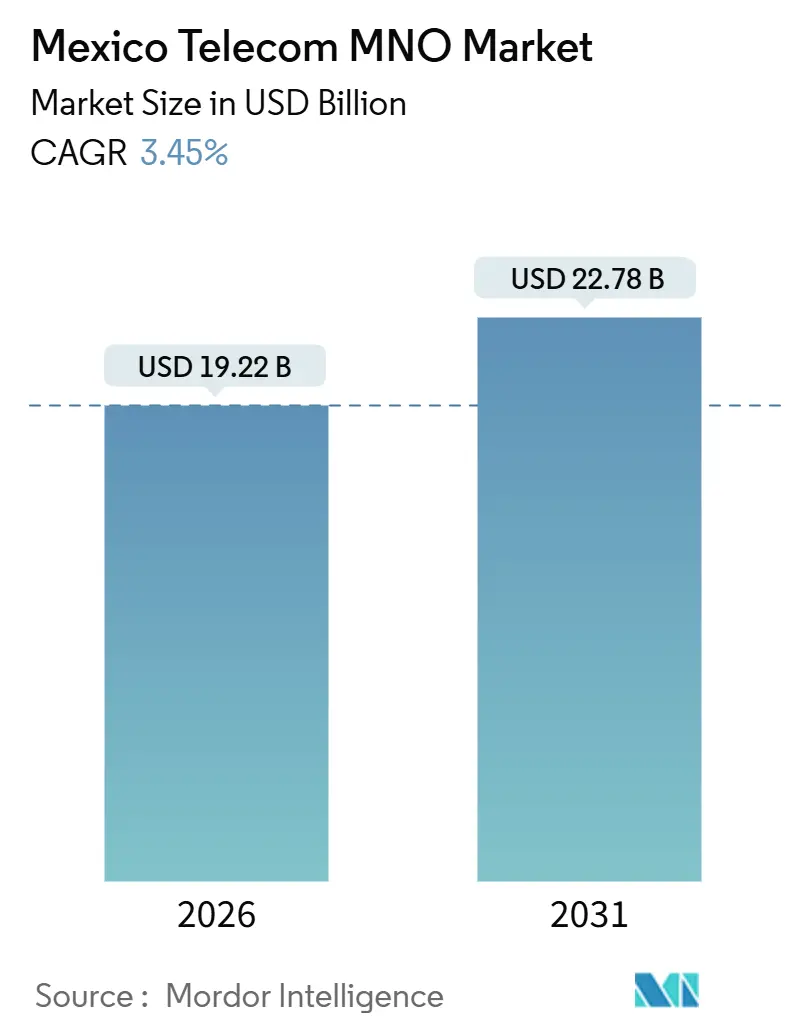

| Market Size (2026) | USD 19.22 Billion |

| Market Size (2031) | USD 22.78 Billion |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Telecom MNO Market Analysis by Mordor Intelligence

The Mexico Telecom MNO Market size is estimated at USD 19.22 billion in 2026, and is expected to reach USD 22.78 billion by 2031, at a CAGR of 3.45% during the forecast period (2026-2031). In terms of subscriber volume, the market is expected to grow from 133.83 million subscribers in 2026 to 155.19 million subscribers by 2031, at a CAGR of 3.01% during the forecast period (2026-2031).

This expansion of the Mexico telecom MNO market reflects a delicate balance: rising postpaid adoption and IoT monetization are pushing data average revenue per user higher, while persistent prepaid churn and spectrum fees that sit roughly 60% above global norms are compressing margins. Operators are channeling capital into mid-band 5G, yet the structural overhaul of the regulatory framework in 2025 has created uncertainty around future spectrum auctions, forcing firms to adopt staged roll-out plans. Private-sector spending on towers and fiber has accelerated because new passive-infrastructure-sharing rules allow multiple carriers to lease the same sites, reducing redundant capex and shortening payback periods. Meanwhile, the wholesale Red Compartida network has lowered rural coverage costs, allowing more than 100 MVNOs to undercut incumbent pricing and intensifying competition for the Mexico telecom MNO market.

Key Report Takeaways

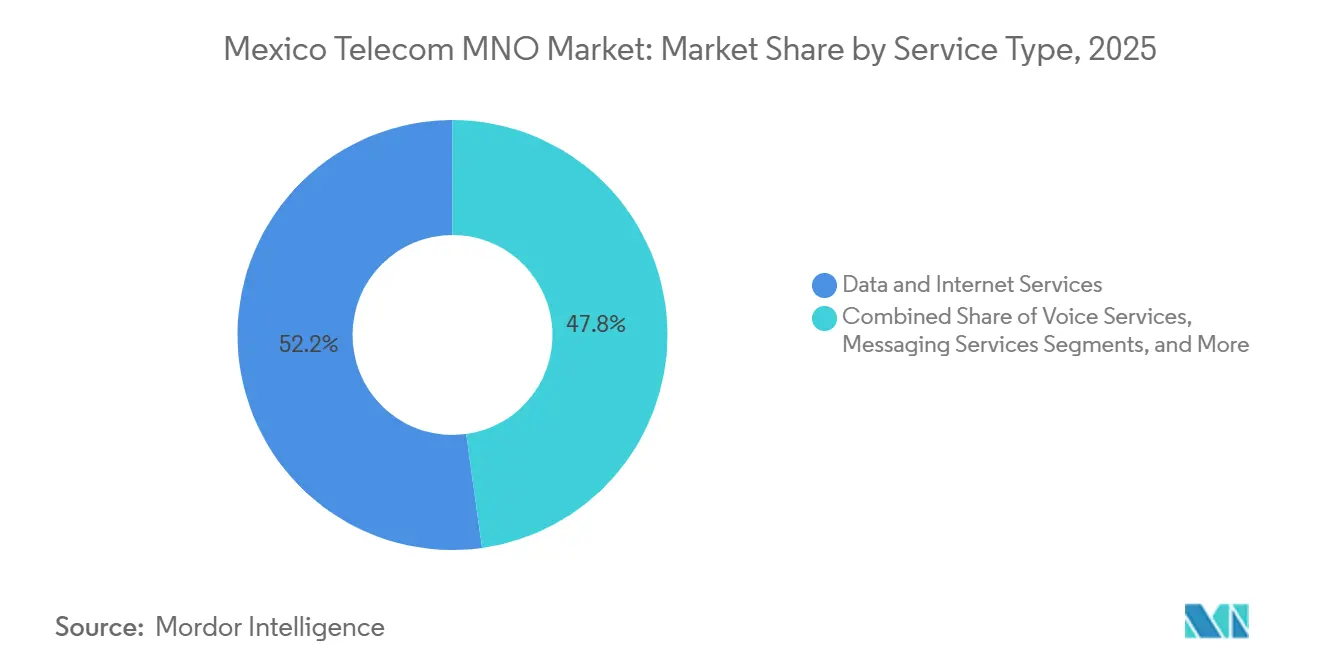

- By service type, Data and Internet Services led with 52.19% of the Mexico telecom MNO market share in 2025; IoT and M2M Services are poised to expand at a 4.57% CAGR through 2031.

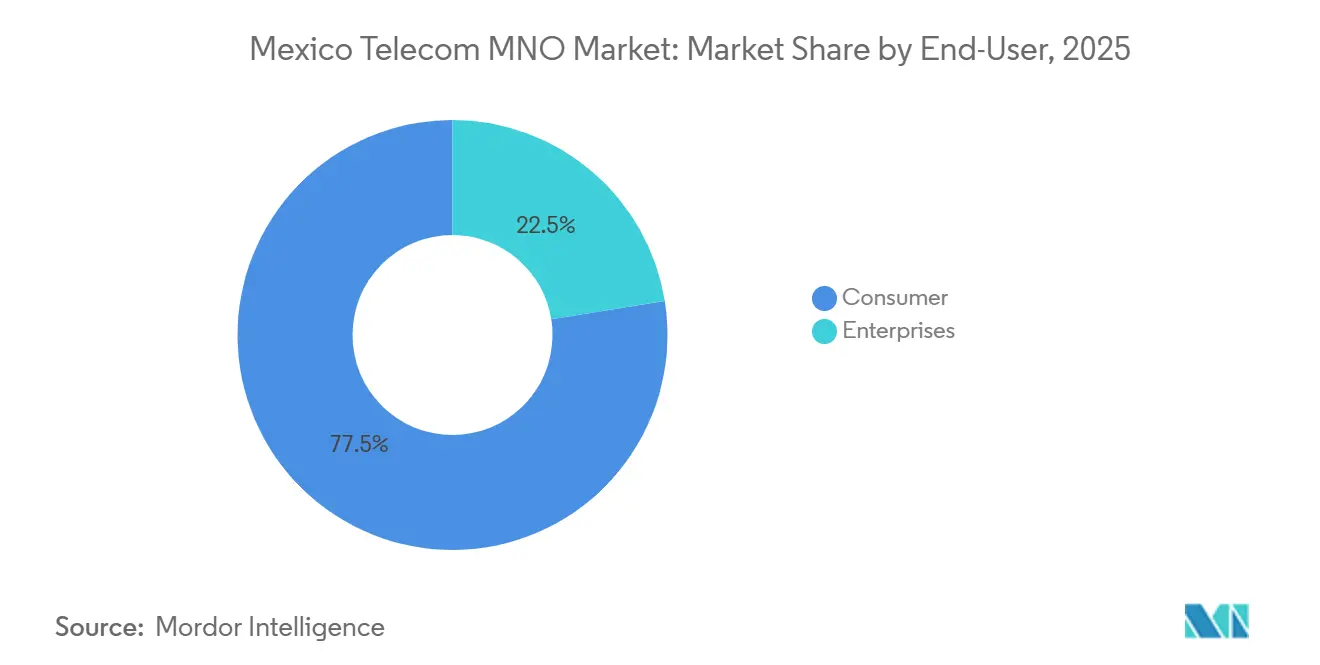

- By end-user, the Consumer segment accounted for 77.52% of the Mexico telecom MNO market size in 2025, while the Enterprises segment is projected to grow at a 3.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G Roll-Out Boosts Data ARPU | +1.2% | National, concentrated in Mexico City, Monterrey, Guadalajara metropolitan areas | Medium term (2-4 years) |

| IoT Demand from Nearshoring Manufacturing and Automotive Clusters | +0.9% | Northern states (Nuevo León, Querétaro, Guanajuato, Baja California) with spillover to Aguascalientes, San Luis Potosí | Medium term (2-4 years) |

| Red Compartida Lowers Rural Roll-Out Cost and Expands Coverage | +0.6% | National, priority in underserved rural municipalities | Long term (≥ 4 years) |

| OTT Video and Mobile-Gaming Partnerships Drive Traffic Monetization | +0.4% | National, skewed toward urban postpaid and youth demographics | Short term (≤ 2 years) |

| 2G and 3G Sunset Frees Sub-1 GHz Spectrum for Capacity | +0.3% | National, accelerated impact in rural areas | Medium term (2-4 years) |

| New Passive-Infrastructure-Sharing Rules Cut Capex | +0.2% | National, benefiting operators in high-density urban zones and underserved rural sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Roll-Out Boosts Data ARPU

Telcel’s network covered 125 cities and 12.3 million 5G subscribers by late 2024, posting median download speeds near 228 Mbps, roughly four times the all-technology average. Postpaid blended ARPU rose to MXN 186 during 2025, a 4.9% year-on-year uplift, as speed and latency improvements enabled premium tiers bundling unlimited social media and cross-border calling [1]América Móvil, “América Móvil’s third quarter of 2025 financial and operating report,” americamovil.com. Performance leadership has let Telcel price above peers, while AT&T and Movistar trail with 5G speeds below 70 Mbps, cementing a two-tier market. Operators now view 5G less as a coverage race and more as a margin lever, targeting latency-sensitive use cases such as cloud gaming. The Mexico telecom MNO market therefore links 5G investment directly to revenue quality rather than subscriber counts, encouraging capital allocation to high-density corridors before rural expansion. Over the medium term, sustained ARPU growth hinges on successful migration of prepaid users to postpaid plans that monetize 5G performance.

IoT Demand from Nearshoring Manufacturing and Automotive Clusters

IoT and M2M connections topped 15 million in 2024, with automotive and electronics manufacturers leading adoption as supply chains shift from Asia under USMCA incentives. General Motors, Ford, and Tesla assembly sites in Nuevo León, Querétaro, and Guanajuato depend on ultra-reliable low-latency connectivity for robotics and quality control, pushing operators to offer private LTE slices and edge-computing bundles.[2]Reuters, “America Movil forecasts USD 6.7 billion capex for 2025,” reuters.com Source: Telecom Review Americas, “Telefónica México: The Disruptive Operator of Connectivity Democratization,” telecomreviewamericas.com Regional revenue outperforms national averages by up to 300 basis points because each plant deploys thousands of sensors. Managed IoT services lift ARPU multiples three-fold, redefining the growth narrative for the Mexico telecom MNO market from consumer scale to enterprise margin. Operators that integrate cybersecurity and analytics with connectivity are positioned to claim a deeper share of manufacturer IT budgets. As nearshoring accelerates, the IoT growth vector is expected to remain the fastest within the service portfolio through 2031.

Red Compartida lowers rural roll-out cost and expands coverage

Operated by CFE Telecomunicaciones, Red Compartida hit 70% national coverage in 2024, offering 700 MHz wholesale capacity that reduces per-site capex by up to 60% compared with traditional builds. Hispasat’s Ka-band satellite backhaul unlocked 65 additional remote base stations, connecting 600,000 people in low-density areas.[3]HISPASAT, “HISPASAT will provide Ka band satellite links to extend Altán la Red Compartida,” hispasat.com The model shifts rural economics for the Mexico telecom MNO market, enabling MVNOs to introduce sub-MXN 200 plans and compelling incumbents to re-price entry-level tariffs. While Telcel has challenged state support in court, government commitment to universal service indicates that wholesale coverage will keep expanding, narrowing the urban-rural divide. Over the long term, rural adoption will become a volume engine, though operators must differentiate through quality and bundled content rather than pure footprint.

OTT video and mobile-gaming partnerships drive traffic monetization

Average monthly data consumption per user has risen sharply as carriers package zero-rated access to Netflix, Disney+, and Amazon Prime Video into mid-tier plans. The strategy trades network costs for lower churn and higher lifetime value, supporting higher pricing in the Mexico telecom MNO market. Telcel recorded the top 5G gaming experience score at 82.93 in late 2024, with median 80 ms latency, allowing operators to market cloud-gaming bundles that add 10%-15% to high-end ARPU. Increasingly, value propositions center on guaranteed latency rather than volumetric data, transforming tariff structures. Partnerships with gaming publishers are expected to mature into dedicated network slices, further segmenting premium user tiers. Short-term gains materialize quickly, but sustaining momentum will depend on continuous network upgrades to maintain service quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum Fees Among the World’s Highest Limit 5G Coverage | -0.8% | National, heavier drag on rural and peri-urban economics | Long term (≥ 4 years) |

| Proposed 2025 Telecom Law Clouds Regulatory Certainty | -0.6% | National, affects auctions, sharing, and competition policy | Medium term (2-4 years) |

| High Prepaid Churn Suppresses Profitability | -0.4% | National, concentrated in low-income segments | Short term (≤ 2 years) |

| Rural Backhaul Gaps Keep 18% Population Outside 4G | -0.3% | Rural municipalities in Oaxaca, Chiapas, Guerrero | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Spectrum Fees Among the World’s Highest Limit 5G Coverage

Reserve prices that run 60% above global averages crippled the 2021 spectrum auction, with only 3 of 41 blocks sold. The follow-up tender slated for late 2024 was canceled, freezing access to mid-band frequencies desperately needed for capacity. A coverage-for-discount auction has been penciled in for 2026, but the newly formed Telecommunications Regulatory Commission lacks a track record, raising the risk of design flaws or delays. América Móvil’s Mexico EBITDA margin of 41.3% in 2024 underscores capital discipline amid spectrum scarcity. Without fee reform, nationwide 5G roll-out will remain skewed toward dense urban corridors, capping total addressable revenue for the Mexico telecom MNO market.

Proposed 2025 Telecom Law Clouds Regulatory Certainty

The July 2025 dissolution of the autonomous IFT split policy formulation from enforcement, creating potential for conflicting mandates. Operators remain uncertain whether asymmetric rules on Telcel will be eased, maintained, or tightened, complicating investment planning. The OECD has warned that predictability in spectrum policy underpinned past investment success.[4]OECD, “Bridging Connectivity Divides,” oecd.org Capital allocation for the Mexico telecom MNO market now contemplates regulatory risk equal to competitive and technological risk, prompting Telefónica to weigh a full exit. Until clarity emerges, carriers may defer rural expansion and secondary-city densification, slowing the sector’s growth cadence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Dominance Meets IoT Acceleration

Data and Internet Services commanded 52.19% of the Mexico telecom MNO market in 2025, mirroring nationwide smartphone penetration above 80% and the ubiquity of unlimited social-media bundles. Voice revenues have commoditized, with pay-as-you-go minutes priced at MXN 0.0125, while SMS traffic continues to migrate to OTT applications. IoT and M2M Services represent the fastest-growing slice at a 4.57% CAGR through 2031, reflecting industrial sensor deployments and smart-city pilot projects in Monterrey and Guadalajara. OTT and PayTV add stickiness to high-value tariffs via bundled content, exemplified by Telcel’s 2025 “Libre” plans.

Differentiation now hinges on upselling managed IoT platforms that combine connectivity with edge analytics and cybersecurity, lifting margins well above basic data transport. Operators that execute on this pivot can turn low-ARPU machine connections into corporate accounts generating triple the revenue of consumer plans. Wholesale capacity and roaming remain adjunct revenue streams, useful for extracting value from excess backhaul and spectrum. Overall, the Mexico telecom MNO market is evolving toward a portfolio mix that favors high-bandwidth consumer data and high-margin enterprise IoT, while legacy voice and messaging steadily lose relevance.

By End-User: Consumer Scale Versus Enterprise Margin

Consumers delivered 77.52% of 2025 revenue, anchored by 84.6 million wireless lines of which 81% were prepaid. Churn rates above 3% per month reflect fierce price competition fueled by more than 100 MVNOs leveraging Red Compartida’s wholesale access. Postpaid penetration, however, is rising at 3.1% year-on-year, and postpaid ARPU is double that of prepaid, making migration strategies a priority.

Enterprises account for only 22.48% of current revenue but are advancing at a 3.86% CAGR, supported by nearshoring manufacturers that demand private LTE and edge solutions. Multi-year contracts, vertical integration, and cross-sell potential create resilient cash flows. Operators investing in dedicated enterprise sales teams and industry-specific solutions stand to capture disproportionate gains. Regulatory outcomes that determine Telcel’s bundling rights will influence competitive dynamics, but regardless of policy, enterprise digitalization is set to raise the strategic importance of this segment within the Mexico telecom MNO market.

Geography Analysis

Metropolitan Mexico City, Monterrey, and Guadalajara attract over three-quarters of new 5G investment because densities above 1,000 inhabitants per square kilometer and postpaid penetration north of 30% shorten payback periods for mid-band roll-outs. Northern manufacturing hubs in Nuevo León, Querétaro, and Baja California post enterprise connectivity growth that is two to three percentage points faster than the national rate as automotive and electronics plants demand low-latency IoT links. Red Compartida’s 70% footprint, reinforced by Hispasat Ka-band satellite backhaul, has pulled towns under 10,000 people into the coverage map and enabled more than 100 MVNOs to introduce sub-MXN 200 plans, shaving the urban-rural divide. These gains coexist with spectrum scarcity, so operators focus first on corridors where blended ARPU exceeds MXN 180, then layer incremental sites outward once fiber backhaul is in place. As a result, the Mexico telecom MNO market shows a mosaic of ultrafast pockets surrounded by legacy 4G zones that still host 18% of the population.

Urban centers generate roughly 75% of service revenue even though they house only 60% of residents, a gap driven by higher smartphone ownership and stronger enterprise demand. Border states such as Baja California monetize cross-border calling bundles to the United States, while inland cities like Puebla, León, and Tijuana are emerging as secondary 5G nodes because they combine acceptable density with lower competitive intensity than Mexico City or Monterrey. Rural deployment can cost 60% more in mountainous Oaxaca and Guerrero, so carriers lean on passive tower sharing and Red Compartida wholesale access to keep cash needs manageable. The planned 2026 coverage-for-discount spectrum tender is designed to lower upfront fees for operators willing to serve underserved municipalities, a policy that, if executed cleanly, could accelerate 4G and 5G reach.

Secondary-city momentum is creating fresh connectivity corridors: industrial parks in San Luis Potosí and Aguascalientes now attract tier-one automotive suppliers that request dedicated fiber and private LTE slices, generating enterprise revenue where little existed five years ago. Tower companies such as Telesites, American Tower, and Mexico Tower Partners lease sites to multiple tenants, trimming redundant capex by up to 30% and making low-density roll-outs economically viable. Government support remains pivotal, as the state-owned Red Compartida plans to hit 92.2% population coverage by 2028, an ambition that would narrow geographic revenue imbalances but will not erase them because income gaps and enterprise density still favor large metros. Overall, geography will matter less for basic coverage but more for premium service uptake, with ARPU differentials enduring even as physical connectivity improves.

Competitive Landscape

Telcel dominates the Mexico telecom MNO market with about 70% share, a position fortified by deep C-band spectrum holdings and an exclusive retail presence in 15,000 Oxxo stores that drew a USD 94 million fine in June 2025 for anticompetitive behavior. AT&T moved to exit by selling its local unit to Telefónica for USD 2.2 billion in October 2024, and Telefónica has since weighed a full departure by mid-2026, underscoring pressure on second-tier players. More than 100 MVNOs, riding on Red Compartida, now offer entry plans priced 30%-50% below incumbent tariffs, siphoning price-sensitive prepaid users and forcing constant promotional activity from network operators.

Technology leadership is Telcel’s chief moat: median 5G speeds exceed 200 Mbps with 89.7% consistency, allowing premium price tiers and lower churn among high-value accounts. Competitors compensate by renting rather than owning assets, leveraging tower portfolios from American Tower and Telesites to keep capital needs in check. Passive-sharing rules introduced in 2024 lowered urban build costs by up to 30%, making network densification feasible for smaller brands. MVNOs such as Flash Mobile and Bait rely on this wholesale fabric to stay asset-light and focus on marketing, yet their razor-thin margins limit large-scale investment in differentiated services.

Future rivalry will hinge on regulatory resolve. If the Telecommunications Regulatory Commission keeps asymmetric obligations on Telcel and mandates fair access to Red Compartida, challengers can scale enterprise IoT and rural niches where bespoke solutions outweigh raw coverage. Should oversight soften, Telcel’s economies of scale and spectrum depth could entrench its lead, potentially lifting its share beyond today’s already high level. Enterprise accounts offer the best hedge for rivals because managed services tie customers into multi-year contracts and yield margins above 50%. For Telcel, protecting dominance means converting its speed advantage into ecosystem stickiness, pairing 5G with exclusive video, gaming, and fintech bundles. Overall, the market blends high concentration with pockets of agile innovation, a recipe that sustains intense yet asymmetric competition across consumer and enterprise segments.

Mexico Telecom MNO Industry Leaders

Telcel (América Móvil)

AT&T México

Telefónica Movistar México

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Telefónica reiterated that a decision on its potential Mexico exit is expected by mid-2026, citing ongoing regulatory uncertainty and currency volatility.

- August 2025: América Móvil confirmed deployment of 1,000 additional 5G sites across secondary cities such as Puebla, León, and Tijuana, advancing its rural densification plan.

- June 2025: Mexico’s telecom regulator fined Telcel USD 94 million for monopolistic SIM-card distribution with Oxxo convenience stores.

- May 2025: Telcel introduced “Telcel Libre” plans, eliminating minimum-term contracts and adding cashback up to 42%.

- April 2025: América Móvil earmarked USD 6.7 billion in 2025 capex, partially funding 5G expansion and backhaul upgrades in Mexico.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Mexico telecom MNO market covers every revenue stream earned inside the country by mobile network operators, including voice plans, mobile data, messaging, IoT/M2M connectivity, and related value-added services, measured in USD value and active subscriber volume. Our study tracks only operator service revenue that originates within Mexico; inter-carrier settlement flows and device hardware proceeds are excluded.

Scope exclusions include fixed broadband, pay-TV, tower leasing, and telecom equipment sales, which sit outside this assessment.

Segmentation Overview

- Overall Telecom Revenue and ARPU

- Service Type

- Voice Services

- Data and Internet Services

- Messaging Services

- IoT and M2M Services

- OTT and PayTV Services

- Other Service Type

- End-user

- Enterprises

- Consumer

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed operator strategy managers, former regulators, network equipment suppliers, and consumer advocacy groups across Mexico City, Monterrey, and Guadalajara. These conversations validated usage elasticity assumptions, 5G roll-out timelines, and regional prepaid-to-postpaid mix, while filling gaps left by secondary reports.

Desk Research

We started with publicly available datasets from tier-one institutions such as the Federal Telecommunications Institute, INEGI, the International Telecommunication Union, the World Bank, and GSMA Intelligence. These sources offered subscriber counts, spectrum holdings, and macro-economic baselines. Company filings, investor presentations, and trade-press archives gathered through Dow Jones Factiva and D&B Hoovers helped us benchmark operator ARPU swings, capex intensity, and tariff moves. Additional context came from policy notes, quarterly traffic statistics, and customs shipment data that clarify handset import volumes. The sources listed illustrate the range consulted; many other open and subscription repositories informed data cross-checks and clarifications.

Market-Sizing & Forecasting

We applied one combined top-down and bottom-up logic. Service-level revenue pools were first reconstructed from regulator billing data, household penetration ratios, and traffic growth metrics, then corroborated with sampled operator-level roll-ups of subscribers multiplied by average revenue. Key variables like mobile subscriber base, blended ARPU, data traffic per user, spectrum fee burden, and 5G coverage reach drive the model. Multivariate regression aligned historic revenue with these drivers and produced the 2025-2030 outlook, while ARIMA smoothing caught short-term shocks. Where bottom-up proxies diverged from macro totals, variance thresholds triggered targeted interviews before final adjustment.

Data Validation & Update Cycle

Outputs pass three reviews: automated anomaly flags, peer analyst scrutiny, and senior sign-off. We refresh the model yearly and reopen it after material events such as spectrum auctions or major M&A, so clients receive the most current view.

Why Mordor's Mexico Telecom Baseline Commands Reliability

Published figures on Mexico's telecom size frequently differ because providers choose unlike service bundles, forecasting windows, and update cadences.

We acknowledge those gaps upfront and show how disciplined scoping and continual validation make our baseline dependable for decision makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.04 bn (2025) | Mordor Intelligence | - |

| USD 35.30 bn (2024) | Regional Consultancy A | Includes fixed-line and pay-TV services; macro revenue extrapolation only; bi-annual refresh |

| USD 35.31 bn (2025) | Trade Journal B | Bundles device sales and optimistic ARPU escalation assumptions |

| USD 17.83 bn (2024) | Industry Association C | Excludes IoT and OTT revenue; limited primary validation |

The comparison shows that when scope and variable discipline slip, estimates swing widely.

By grounding forecasts in clearly defined service revenue, cross-verified traffic trends, and a transparent update cadence, Mordor Intelligence delivers a balanced, repeatable baseline clients can trust.

Key Questions Answered in the Report

How large is the Mexico telecom MNO market in 2026?

The market is valued at USD 19.22 billion, advancing at a 3.46% CAGR toward 2031.

Which service category is expanding fastest in Mexican mobile?

IoT and M2M Services lead with a projected 4.57% CAGR through 2031, outpacing other segments.

What share of revenue comes from consumer subscribers?

Consumers account for 77.52% of 2025 revenue, driven by more than 84 million wireless lines.

Why are spectrum fees seen as a restraint?

Prices are roughly 60% above global norms, limiting operator participation in auctions and slowing 5G coverage.

How does Red Compartida influence competition?

The wholesale network lowers rural capex and supports over 100 MVNOs that offer low-priced plans, intensifying competitive pressure.

What regions benefit most from nearshoring-driven IoT demand?

Nuevo León, Querétaro, and Guanajuato see the strongest enterprise IoT growth due to automotive and electronics manufacturing clusters.

Page last updated on: