Peru Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

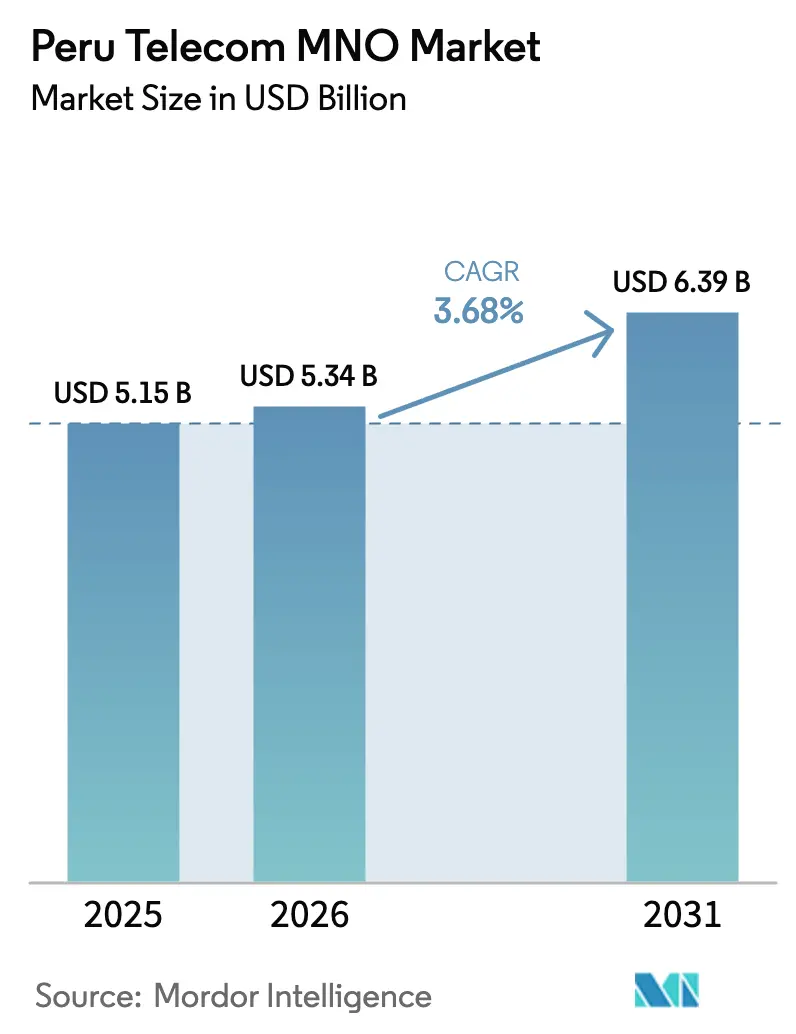

| Base Year Market Size (2025) | USD 5.15 Billion |

| Market Size (2026) | USD 5.34 Billion |

| Market Size (2031) | USD 6.39 Billion |

| Growth Rate (2026 - 2031) | 3.68% CAGR |

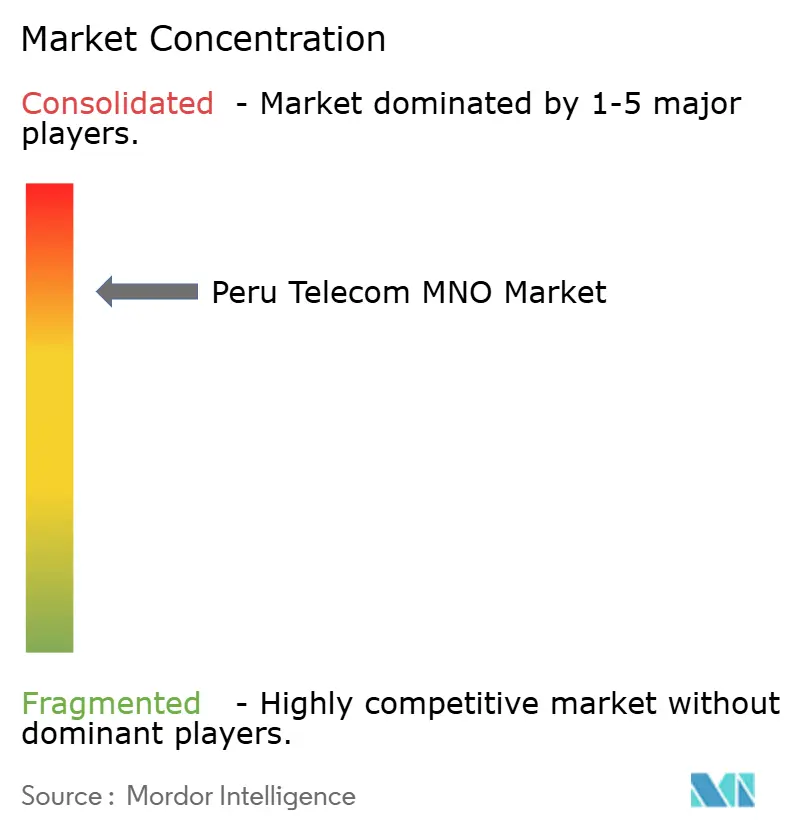

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peru Telecom MNO Market Analysis by Mordor Intelligence

The Peru Telecom MNO Market size was valued at USD 5.15 billion in 2025 and estimated to grow from USD 5.34 billion in 2026 to reach USD 6.39 billion by 2031, at a CAGR of 3.68% during the forecast period (2026-2031).

This steady climb reflects a maturing arena where revenue gains come less from fresh subscriber additions and more from infrastructure upgrades, 4G densification, and early-stage 5G monetization. Operators lean on enterprise IoT contracts, cloud enablement, and bundled video plans to offset margin pressure in core connectivity. Government moves, most notably direct 5G spectrum assignment and ongoing Red Dorsal fiber expansion, lower backhaul costs, and hasten rural build-outs. At the same time, tower-sharing deals with SBA Communications and American Tower help decrease CAPEX, freeing cash for network automation and energy-efficiency projects. Foreign-exchange swings and unresolved spectrum-refarming rules still cloud spending plans, but wider smartphone affordability and zero-rated OTT products continue to lift data ARPU in both urban and peri-urban zones.

Key Report Takeaways

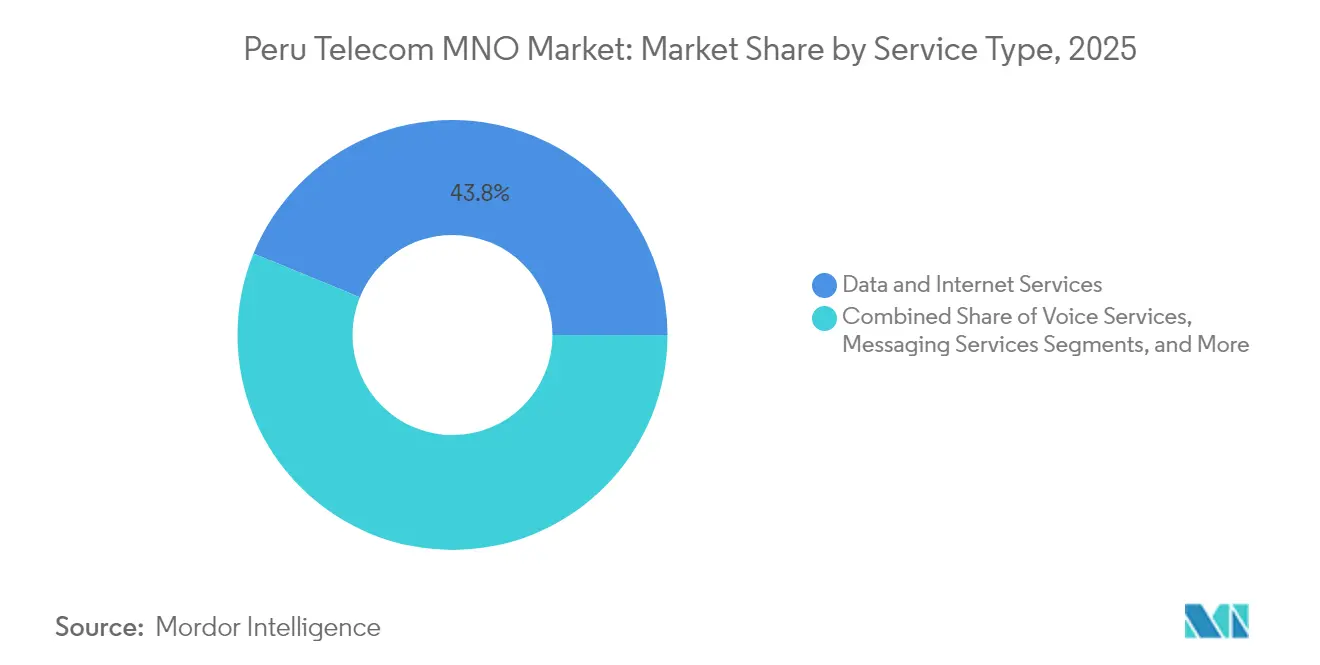

- By service type, data and internet held 43.82% of Peru telecom MNO market share in 2025, while IoT and M2M services are projected to expand at a 3.76% CAGR through 2031.

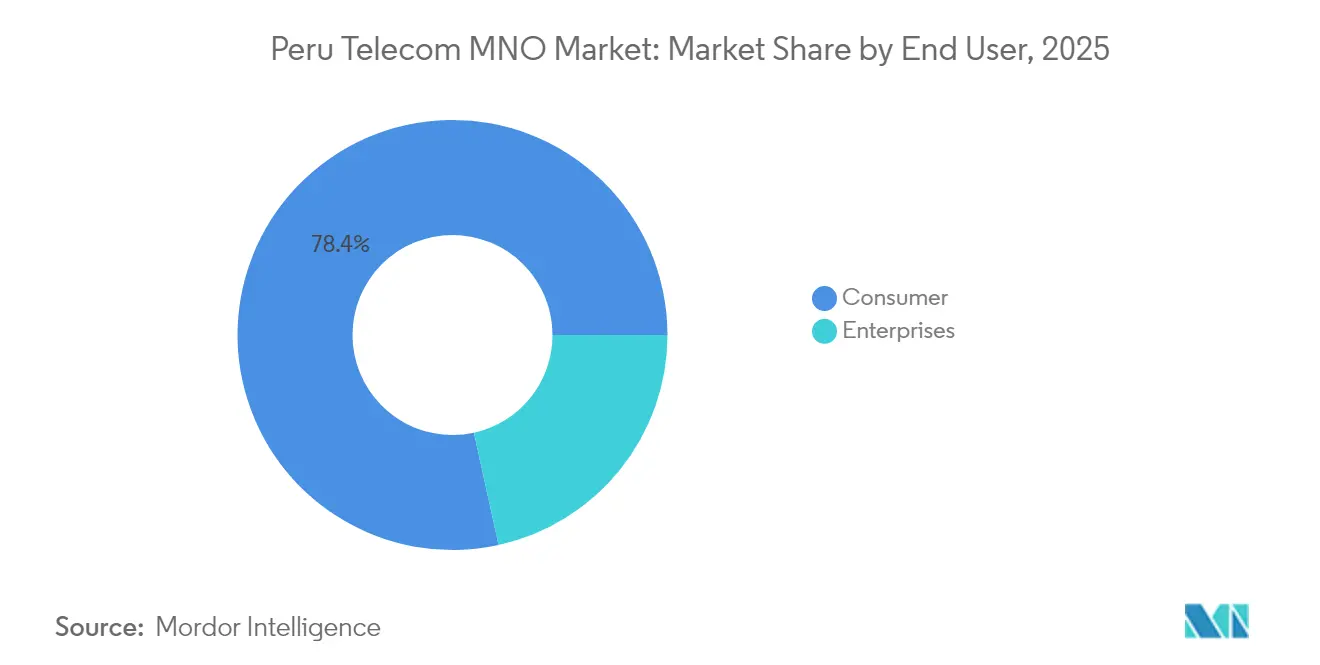

- By end user, consumer lines contributed 78.44% of the Peru telecom MNO market size in 2025; the enterprise segment is advancing at a 4.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Peru Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 4G/5G densification in remote Amazon and Andean regions | +0.8% | Amazon basin, Andean highlands, rural Peru | Medium term (2-4 years) |

| Explosive consumer video-driven data demand | +0.9% | National, with concentration in Lima, Arequipa, Trujillo | Short term (≤ 2 years) |

| 'Red Dorsal' fiber backbone lowering back-haul costs | +0.6% | National, connecting 180 provincial capitals | Long term (≥ 4 years) |

| Enterprise IoT uptake in mining and agriculture | +0.4% | Mining regions (Cajamarca, Arequipa), agricultural zones (La Libertad, Ica) | Medium term (2-4 years) |

| Zero-rated OTT bundles reviving ARPU | +0.3% | National, higher impact in urban areas | Short term (≤ 2 years) |

| Cheaper smartphones and tax incentives boosting 4G adoption | +0.5% | Rural and peri-urban areas, lower-income segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 4G / 5G densification in remote Amazon and Andean regions

Direct 5G spectrum assignment eliminates auction delays, letting operators bring sites online months faster than under competitive bidding. Entel pledged USD 200 million in 2025, with 60% of Claro’s grid earmarked for 5G by 2028 [1]“Entel invertirá más de USD 200 millones en Perú,” El Comercio, ELCOMERCIO.PE. Coverage expansion targets 76,300 unserved population centers, a move that spurs both social inclusion and incremental revenue. Tower-sharing with American Tower and IHS cuts deployment cost per site by up to 35%, strengthening the business case. Community pushback against antenna installations remains a sporadic risk, making local engagement critical for on-time delivery.

Explosive consumer video-driven data demand

Streaming adoption pushes average monthly mobile traffic beyond 14 GB per user, stressing RAN capacity yet opening up sell avenues. A 2024 sales tax on OTT services yields PEN 800 million (USD 215 million) for the treasury but has not dented subscriber growth meaningfully [2]Luis Rojas, “Impuesto a streaming en Perú,” TAVI Latam, TAVILATAM.COM . Claro led Opensignal’s 2023 Video Experience score at 58.1, leveraging that edge in bundles that pair unlimited data with Disney+ or HBO Max. Unlimited plans, however, cap usage-based margins, so quality-of-experience metrics now underpin differentiation. Zero-rating of WhatsApp and Facebook mitigates peak-time congestion and keeps churn below 2.1% quarterly in prepaid cohorts.

Red Dorsal fiber backbone lowering backhaul costs

The USD 300 million national backbone links 180 provincial capitals over 13,000 km of fiber, slicing rural backhaul tariffs by up to 45% [3]“Gilat Receives USD 153.6 Million for National Fiber Backbone,” Via Satellite, SATELLITETODAY.COM. Critics flag high upkeep, yet Gilat’s USD 153.6 million contract and Internexa’s third fiber ring prove enduring private interest. Lower transport outlay lets MNOs introduce competitively priced LTE plans in towns once tied to satellite. Future value hinges on wholesale rate regulation and fair-access rules now under OSIPTEL review.

Enterprise IoT uptake in mining and agriculture

Mining majors deploy private LTE for haul-truck automation and worker safety, such as Nokia’s network at Las Bambas, 4,600 m above sea level. OptConnect’s 2024 takeover of M2M DataGlobal signals foreign appetite for local machine-connectivity contracts. Agricultural cooperatives adopt LoRaWAN soil sensors for irrigation control, increasing yield by up to 12%. Despite rugged topography, improved RF planning and cloud-native core platforms lower network latency, enabling real-time analytics and predictive maintenance.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty over spectrum refarming and 5G auctions | -0.6% | National, affecting all operators | Medium term (2-4 years) |

| Prepaid dominance curbing post-paid ARPU growth | -0.4% | National, higher impact in lower-income segments | Long term (≥ 4 years) |

| FX volatility inflating imported network CAPEX | -0.5% | National, affecting equipment procurement | Short term (≤ 2 years) |

| Dollar-indexed tower lease escalation | -0.3% | National, concentrated in high-traffic areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory uncertainty over spectrum refarming and 5G auctions

March 2025 rules outline direct spectrum grants yet leave frequency blocks and pricing undefined, slowing radio-planning cycles [4]Baker McKenzie, “Regulations to promote 5G,” INSIGHTPLUS.BAKERMCKENZIE.COM . A proposed merger of OSIPTEL with energy and water regulators could trim red tape but may disrupt established processes during transition. Operators juggling 2G sunset plans and 5G rollouts hesitate to allocate capital until clarity emerges, deferring roughly USD 120 million of planned rural sites into 2026.

Prepaid dominance curbing post-paid ARPU growth

Prepaid lines still make up 67% of SIMs, mirroring income volatility and limited credit penetration. Lower ARPU, higher churn, and thin data-consumption profiles complicate 5G monetization. MNOs offset by packaging micro-credit top-ups, but revenue elasticity remains weak. Customer-data scarcity hampers targeted upsell, reducing effectiveness of premium content bundles relative to post-paid peers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data and internet services controlled 43.82% of the Peru telecom MNO market share in 2025 as usage per smartphone climbed to 14 GB monthly. The Peru telecom MNO market size for data is projected to be fueled by streaming, gaming, and cloud backup demand. IoT and M2M services, though small, will log the fastest 3.76% CAGR through 2031 as mines, farms, and smart-city pilots scale. Voice traffic inches downward at 1.2% annually, yet remains relevant for low-income customers using basic handsets. Messaging revenue erodes rapidly because zero-rated WhatsApp and Facebook Messenger cannibalize SMS. OTT and PayTV bundles gain traction after operators strike wholesale deals with Netflix and Disney+, mitigating the 16% VAT that took effect in October 2024. Other value-added services, cyber-security, managed Wi-Fi, and device insurance, grow off a small base, contributing stickiness rather than a significant topline impact.

Beyond headline revenue, data services supply the performance yardstick that defines brand hierarchy. Claro’s 800-MHz refarm and carrier aggregation deliver superior downlink speeds, sustaining a 6-point NPS lead over Movistar. Entel leverages Red Dorsal backhaul to lower per-gigabyte cost by 18%, enabling aggressive unlimited-plan pricing in secondary cities. Bitel, the rural specialist, markets single-tower LTE deployments linked via satellite, bridging the last mile where fiber remains scarce. Together, these moves illustrate how operators pivot from voice ARPU to quality-centric data monetization, aligning investment with sites that promise quick payback even at compressed margins.

By End User: Enterprise Segment Accelerates Digital Adoption

The enterprise slice is set to outpace overall growth at 4.15% CAGR. Cloud connectivity, cyber-resilience, and mission-critical IoT anchor spending. Mining entities request private LTE with quality of service guarantees, while manufacturers in Lima’s industrial belt adopt low-latency 5G for robotics. Agriculture outfits deploy sensor networks to cut water usage by 15% and improve fertigation schedules. Against this backdrop, WIN Empresas, a fiber-first challenger, captured high-margin contracts via bundled SD-WAN and security. Incumbents respond by spinning off enterprise units with consultative sales teams, underscoring the pivot from commodity bandwidth toward solutions revenue.

Consumer lines, although mature, remain the cash generator thanks to their 78.44% share in 2025. Growth comes mainly from upselling bundled video and device-financing plans rather than SIM net-adds, as penetration already exceeds 120%. Number-portability rules revised in February 2024 shrink porting time to 24 hours, intensifying churn wars. Operators counter with loyalty apps and micro-loans for handset upgrades. Over time, shifting disposable-income patterns will nudge a subset of prepaid customers into entry-level post-paid, aiding ARPU uplift albeit modestly.

Geography Analysis

Peru telecom MNO market performance varies sharply by region. Lima, with 47.1% household internet penetration, absorbs close to half of national mobile data traffic and generates premium ARPU north of USD 6.50, owing to dense fiber backhaul and large post-paid clusters. Arequipa and Trujillo follow, each benefiting from Movistar’s fiber rollout that now passes 290,000 homes. Coastal corridors see above-average 5G readiness because carriers reuse existing microwave links for mid-band spectrum.

High-altitude Andean zones house copper and gold mines whose automation plans spur private-network demand. Cajamarca alone accounts for an estimated USD 25 million in annual enterprise connectivity spend, a figure expected to grow as Open-Pit 4.0 projects launch. Amazon basin towns, reachable only by river or small aircraft, remain underserved despite Red Dorsal’s presence. Pronatel subsidies incentivize bit-mile reach, yet operators must contend with seasonal weather that disrupts maintenance windows.

Policy makers earmark USD 236 billion for multi-sector infrastructure by 2035, with telecom fiber and towers eligible for tax credits. Environmental management rules require projects to submit an instrument that details waste and land-use impact, extending time-to-build by roughly 90 days but enhancing long-term sustainability. As a net effect, network rollouts should proceed at a measured yet steady pace, gradually shrinking the urban-rural digital divide without compromising ecological safeguards.

Competitive Landscape

Four nationwide players split the subscriber pie, giving the Peru telecom MNO market a consolidated profile. Claro leads the market, followed by Movistar, Entel, and Bitel. Telefónica’s 2025 bankruptcy and USD 1 million divestiture to Integra Tec marked a pivotal reshuffle, freeing spectrum blocks and cell-sites ripe for absorption. Claro aspires to cover 60% of populated areas with 5G by 2028, banking on Huawei’s 5G-Advanced test that hit 10 Gbps downloads. Movistar, still deleveraging, modernized 1,000 base stations to reclaim urban capacity.

Competition now hinges on service breadth rather than pure price. WIN Empresas carves a niche supplying SD-WAN and SOC-as-a-Service to banks and retailers, while Bitel courts rural youth with TikTok-centric bundles. Infrastructure-sharing gains steam; SBA Communications targeted 400 additional towers in 2025, and IHS finalized its first Peruvian acquisition. These deals cut opex per site by an estimated 22%, allowing lower entry-level pricing without sacrificing EBITDA. Regulatory oversight remains tight: OSIPTEL scrutinizes promos to prevent predatory pricing, and planned consolidation of watchdog bodies could alter approval timelines for future M&A.

Disruptors from adjacent sectors add pressure. Amazon’s Kuiper LEO constellation seeks VSAT licenses, promising 100 Mbps to remote schools. Yape, the fintech app with 16 million users, leverages TerraPay rails to integrate prepaid top-ups, turning digital wallets into an alternative distribution for SIMs. Such cross-industry moves blur the line between pure telecom and digital-services revenue pools.

Peru Telecom MNO Industry Leaders

Movistar (Integratel Perú)

Claro Perú (América Móvil)

Entel Perú S.A.

Bitel (Viettel Perú S.A.C)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Internexa opened its third fiber optic ring in Peru, enhancing backbone infrastructure capacity and providing additional connectivity options for enterprise customers and wholesale partners.

- July 2025: Claro Peru and Huawei successfully tested 5G-Advanced technology achieving 10 Gbps download speeds, ten times faster than current 5G, utilizing mid-band and millimeter-wave spectrum temporarily allocated by Peru’s Ministry of Transport and Communications.

- June 2025: Movistar modernized 1,000 base stations and accelerated deployment of its new mobile network across Peru as part of its infrastructure enhancement strategy.

- April 2025: Telefónica completed the sale of its Peruvian subsidiary to Argentine company Integra Tec for approximately USD 1 million, marking the end of the Spanish operator’s 31-year presence in Peru.

Peru Telecom MNO Market Report Scope

The Peruvian telecom MNO market study tracks the revenue generated by major telecom companies in Peru through the sale of various services, including data, voice, messaging, and roaming, to end users. The analysis combines insights from both secondary research and primary sources. It delves into the key drivers and restraints shaping the market's growth trajectory.

The study monitors crucial market parameters, identifies growth drivers, and profiles key industry vendors. These insights underpin the market estimations and growth projections for the forecast period. In addition, the study provides market trends, along with key vendor profiles.

The study provides an in-depth analysis of the telecommunication MNO industry in Peru. The Peruvian telecom market is segmented by services (voice services (wired and wireless), data and messaging services, and OTT and PayTV services).

The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming, Enterprise and Wholesale etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming, Enterprise and Wholesale etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Peru telecom MNO market in 2026?

The Peru telecom MNO market size is USD 5.34 billion in 2026 with a 3.68% CAGR forecast through 2031.

Which service type generates the most revenue for operators?

Data and internet services lead with 43.82% share, driven by expanding video streaming and enterprise cloud usage.

What segment is growing fastest to 2031?

IoT and M2M connections will post the highest 3.76% CAGR as mining, agriculture, and manufacturing automate operations.

How is government policy influencing 5G rollout?

Direct spectrum assignment speeds deployment by skipping auctions, while Red Dorsal fiber lowers rural backhaul costs.

Which operator currently holds the largest subscriber base?

Claro leads with 30.1% mobile share, followed by Movistar, Entel, and Bitel.

What primary risk could slow growth over the next four years?

Regulatory uncertainty around spectrum refarming may delay investment decisions and network upgrades.

Page last updated on: