Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

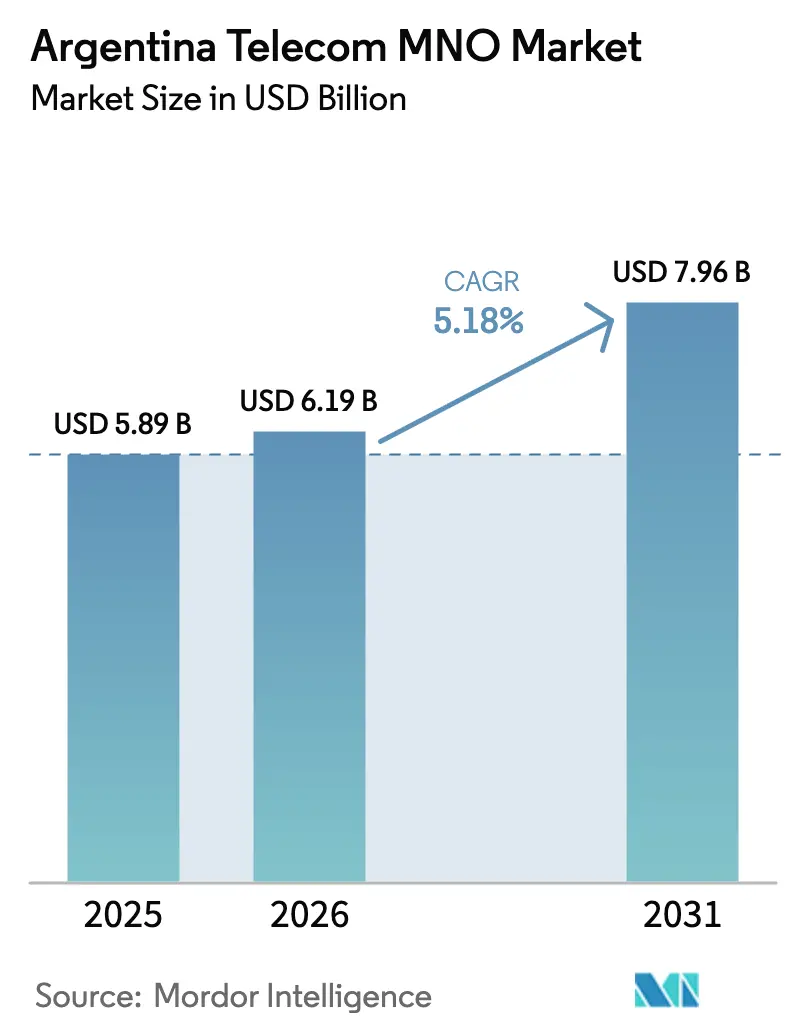

| Base Year Market Size (2025) | USD 5.89 Billion |

| Market Size (2026) | USD 6.19 Billion |

| Market Size (2031) | USD 7.96 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

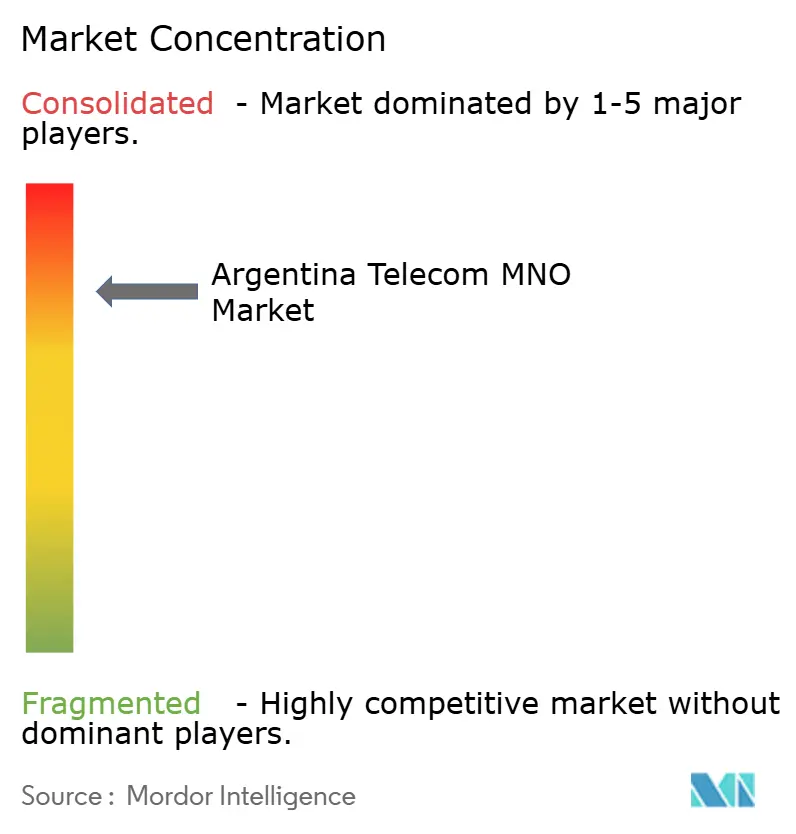

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Telecom MNO Market Analysis by Mordor Intelligence

The Argentina Telecom MNO Market size in 2026 is estimated at USD 6.19 billion, growing from 2025 value of USD 5.89 billion with 2031 projections showing USD 7.96 billion, growing at 5.18% CAGR over 2026-2031.

The current expansion rests on three pillars: rapidly rising mobile-data usage on 4G and 5G networks, renewed tariff flexibility following the repeal of price caps, and a fresh wave of enterprise digitalization programs across agriculture, mining, and manufacturing. Operators have redirected capital toward nationwide fiber backbones and dense radio-access upgrades, a shift that shortens latency, reduces dropped-call ratios, and boosts average data speeds for both urban and rural customers. The Argentina telecom MNO market also benefits from a supportive spectrum roadmap that unlocks contiguous 3.5 GHz blocks and commits public-sector funds to rural coverage, allowing carriers to time their rollouts in line with cash-flow conditions. At the same time, operators face elevated inflation, which erodes ARPU in real terms, yet they mitigate pressure through USD-denominated premium plans and enterprise IoT contracts that preserve hard-currency revenue streams. Convergent quad-play bundles further strengthen retention by integrating fixed broadband, mobile, pay-TV, and VoIP into single bills that cushion households from unpredictable monthly price swings.

Key Report Takeaways

- By service type, data and internet services led with 62.08% of Argentina telecom MNO market share in 2025, while IoT and M2M services are forecast to expand at a 5.32% CAGR through 2031.

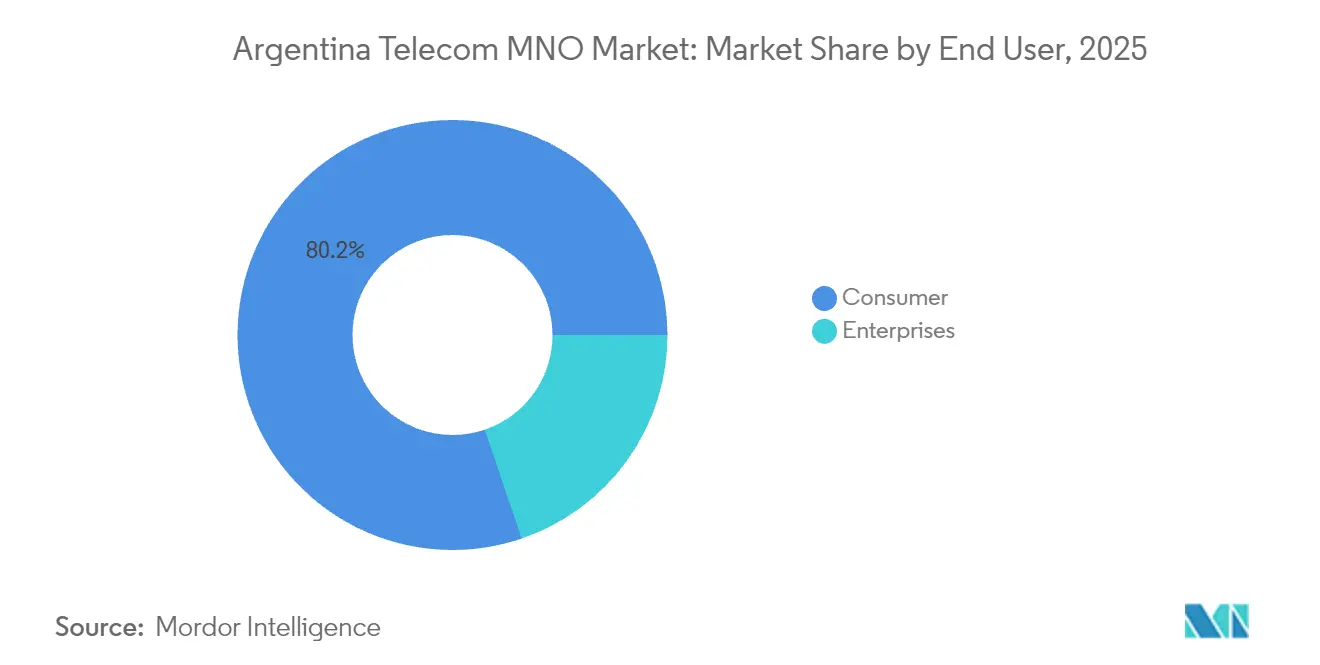

- By end-user, the consumer segment accounted for 80.22% of the Argentina telecom MNO market size in 2025, whereas enterprise connections are projected to grow at a 5.65% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive mobile-data consumption on 4G/5G | +1.2% | Nationwide; peaks in Buenos Aires, Córdoba, Rosario | Medium term (2 – 4 years) |

| 5G spectrum auctions and fibre backbone build-out | +0.8% | Metro corridors first, then secondary cities | Long term (≥ 4 years) |

| Uptake of convergent quad-play bundles | +0.6% | Country-wide; strongest in dense urban neighborhoods | Medium term (2 – 4 years) |

| Enterprise digitalization and IoT demand | +0.9% | Agriculture belts, mining zones, industrial clusters | Long term (≥ 4 years) |

| USD-denominated premium plans | +0.4% | High-income pockets in all provinces | Short term (≤ 2 years) |

| Passive-infrastructure sharing rules | +0.3% | Under-served rural districts | Medium term (2 – 4 years) |

| Source: Mordor Intelligence | |||

Explosive Mobile-Data Consumption on 4G/5G Networks

Total cellular-data traffic more than doubled between 2023 and 2025 as video streaming, mobile gaming, and agricultural sensor feeds converged on upgraded LTE and early 5G carriers. Median download speeds on Personal’s 5G network hit 432 Mbps, confirming the platform’s ability to support bandwidth-hungry enterprise and consumer applications. Farmland IoT pilots rely on low-power wide-area modules that upload soil-moisture and crop-health readings every fifteen minutes, generating steady, high-margin traffic even during macroeconomic slowdowns. Operators use dynamic spectrum-sharing to re-farm 1,800 MHz bands, squeezing extra capacity out of existing assets while the 3.5 GHz grid densifies in metropolitan corridors. These developments secure data-centric revenue streams and reinforce the long‐term relevance of the Argentina telecom MNO market.

5G Spectrum Auctions and Fibre-Backbone Build-Out

The 2024 spectrum tender released 100 MHz from state-owned ARSAT and an additional 50 MHz from ENACOM, bundling coverage obligations with discounted reserve prices to make deployments financially workable. Winning bidders receive staggered payment schedules and 12-year licenses, enabling cost recovery over a full depreciation cycle. Parallel fiber builds interconnect 1-TBps metro rings with 400-Gbps long-haul links, creating the backhaul headroom needed for massive-MIMO cell sites. Claro alone allocated USD 200 million to extend AI-enabled fiber deeper into edge nodes, accelerating the transition to network-function virtualization and cloud-native cores. Taken together, these infrastructure moves add 0.8 percentage points to the projected CAGR of the Argentina telecom MNO market.

Enterprise Digitalization and IoT Connectivity Demand

Private LTE and early 5G stand-alone networks now underpin drilling automation in Patagonia, autonomous haul-trucks in Santa Cruz gold mines, and smart conveyer lines in automotive plants north of Buenos Aires. Agriculture presents the largest addressable base with 34 million hectares under precision-farming schemes that require GNSS-linked harvesters and real-time pest detection cameras. ARSAT’s satellite-backed narrow-band IoT service fills connectivity gaps in regions where terrestrial footprints remain sparse, ensuring uniform sensor coverage. Government grants under the National Science, Technology and Innovation Plan 2030 subsidize proof-of-concept pilots, accelerating take-up across SMEs and boosting overall enterprise contract value. These forces collectively raise the Argentina telecom MNO market by an estimated 0.9% CAGR contribution. [1]ARSAT, “Proyecto Satelital de Internet de las Cosas,” arsat.com.ar

Uptake of Convergent Quad-Play Bundles

Households facing volatile monthly inflation migrate toward fixed-price service umbrellas that combine unlimited mobile data, symmetrical fiber broadband, and on-demand TV catalogs. Telecentro’s USD 400 million HFC-to-fiber overhaul unlocks gigabit speeds that sit at the heart of its “all-inclusive” offers. Telecom Argentina reports that bundled customers churn 42% less frequently than single-service subscribers, making convergence a defensive and offensive tactic. Operators amplify appeal with loyalty programs, mobile payment wallets, and cloud-storage add-ons that tighten ecosystem lock-in. Even in smaller towns, tower-sharing agreements lower capex, allowing carriers to extend bundles without prohibitive investment, a dynamic that adds 0.6 percentage points to sector growth. [2]Telecom Argentina, “Memoria y Estados Financieros 2024,” telecomargentina.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-inflation diluting real ARPU | –1.8% | Nationwide; deepest in low-income areas | Short term (≤ 2 years) |

| Tariff freeze / price-cap regulations | –0.7% | Dependent on future policy revisions | Medium term (2 – 4 years) |

| Slow eSIM portability approval for IoT | –0.3% | Country-wide IoT integrators | Medium term (2 – 4 years) |

| High import duties on 5G RAN equipment | –0.5% | All provinces; raises capex burdens | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyper-Inflation Diluting ARPU in Real Terms

The consumer-price index rose above 100% in 2024, outpacing nominal tariff hikes and slicing 7.7% off sector revenue once adjusted for inflation. Pre-paid SIMs now represent 61% of all mobile lines, indicating a flight to usage-controlled plans that keep discretionary spend in check. Operators partially insulate margins by pegging premium 5G tiers to the U.S. dollar, thereby shielding higher-income customers from peso volatility. They also broaden wholesale fiber sales and cloud-managed security to stabilize enterprise cash flows. However, the drag on mass-market purchasing power remains the single largest brake on the Argentina telecom MNO market, shaving 1.8 percentage points from forecast growth. [3] Banco Central de la República Argentina, “Informe de Inflación 2024,” bcra.gob.ar

High Import Duties on 5G RAN Equipment

Radio-access components sourced from overseas suppliers face duties of up to 16% in addition to freight-on-board surcharges attributable to port congestion. Since equipment must be paid in USD while revenue is peso-denominated, carriers encounter natural currency mismatches that complicate procurement cycles. To manage exposure, the three nationwide MNOs extend vendor-financing tenors from five to seven years and ramp up tower-sharing pacts that dilute per-site hardware costs. Nonetheless, the higher landed cost of massive-MIMO arrays and millimeter-wave modules delays the full-scale rollout schedule, trimming 0.5 percentage points off the Argentina telecom MNO market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Dominance Reshapes Revenue Mix

Data and internet services generated 62.08% of Argentina telecom MNO market share in 2025, a proportion that rises steadily as voice minutes migrate to OTT calling and rich-media apps. The segment benefits from nationwide 4G population coverage exceeding 99% and growing 5G pockets that handle immersive video and enterprise sensor streams. In numerical terms, data contracts contributed USD 3.66 billion to the Argentina telecom MNO market size during 2025. IoT and M2M lines posted the fastest expansion, logging a 5.32% CAGR outlook to 2031 on the back of agriculture, mining, and manufacturing automation projects. Operators package data with cloud-storage and edge analytics, converting what was once a commodity pipe into a multi-layer service stack with higher per-connection margins.

Messaging, VAS, and roaming revenues continue to fade as customers adopt app-based communication and remote-work platforms that bypass legacy SMS frameworks. Still, roaming rebounds during outbound tourism spikes, aided by simplified regional rate plans that keep travelers on-net. Pay-TV’s integration into mobile bundles secures incremental stickiness despite intense streaming rivalry. Collectively, the evolving service portfolio underlines the Argentina telecom MNO market’s pivot toward digital solutions capable of monetizing bandwidth, latency, and security rather than pure minutes of use.

By End-User: Enterprise Momentum Accelerates

Enterprises remain the fastest-growing constituency, with connections forecast to climb 5.65% CAGR through 2031, even as consumers hold an 80.22% revenue share today. Private LTE deployments inside mining pits and factory floors drive average-line revenue four times higher than retail smartphone ARPU, lifting overall profitability. An estimated 28,000 agricultural IoT gateways now blanket row-crop regions, feeding analytics platforms that optimize irrigation and fertilizer usage. Manufacturing plants in Córdoba deploy time-sensitive networking over 5G to synchronize robotics and reduce assembly-line downtime. The Argentina telecom MNO market size for enterprise mobile services totaled USD 1.17 billion in 2025 and is on course to double by 2031.

On the consumer side, convergent billing and device-financing plans sustain unit additions despite inflationary headwinds. Government digital-ID and mobile-passport programs deepen engagement, making phones essential for public-service access. Yet low-income users gravitate toward ad-supported data bundles that offer zero-rated social media and messaging, underscoring a bifurcated demand curve. The dual-speed trajectory allows operators to cross-fund suburban 5G densification with enterprise cash flows, aligning investment with both short-term and strategic objectives of the Argentina telecom MNO market.

Geography Analysis

Argentina’s three largest conurbations, Buenos Aires, Córdoba, and Rosario, generate roughly 70% of mobile revenue thanks to dense populations, strong household incomes, and large enterprise campuses. Average downlink speeds exceed 55 Mbps in these corridors, supporting cloud-gaming, UHD video, and real-time industrial control. The Atlantic Coast technology belt enhances this leadership by hosting the nation’s first stand-alone 5G clusters that anchor edge-compute zones servicing port logistics and fisheries. Mid-tier cities such as Mendoza and Salta experience a second wave of fiber overlays, backed by Universal Service Fund grants that lower last-mile build costs. Collectively, metro areas keep the Argentina telecom MNO market size on a solid upward trend as premium-tier consumer plans and enterprise contracts cluster where per-capita GDP is highest.

Rural provinces present contrasting dynamics. Thousands of square miles in La Pampa and Santa Fe rely on NB-IoT modules tethered to silo temperature sensors and livestock trackers, driving a specialized connectivity niche that commands resilient, subscription-like revenue. ENACOM’s National Critical Communications Infrastructure Plan leverages spectrum set-asides and tower-sharing incentives to extend 4G/5G reach, closing digital gaps without burdening any one operator with disproportionate capex. Regional tax incentives further sweeten deployment economics, cutting permit fees and fast-tracking rights-of-way approvals, yet zoning inconsistencies still lengthen site-acquisition timelines in isolated municipalities.

Cross-border trade flows with Chile, Brazil, and Uruguay add a third geographic layer. Roaming agreements and expanded interconnection gateways enable enterprises to run seamless telemetry over contiguous networks, especially valuable for mining and agribusiness firms that straddle frontiers. Satellite backhaul in Patagonia supports oil-field automation and environmental monitoring where terrestrial loops remain commercially unviable. Extreme-weather resilience dictates hardened tower specifications, pushing O-ring sealed antennas and battery-shelter climate control to prevent downtime during heatwaves or snowstorms. These geography-specific investment patterns knit together a cohesive yet nuanced growth fabric for the Argentina telecom MNO market.

Competitive Landscape

Argentina hosts three full-scale mobile network operators that compete across coverage, technology, and convergent service depth. Telecom Argentina, post-acquisition of Telefónica’s local unit, would command roughly 61% of mobile subscribers and up to 80% of residential broadband in certain districts, pending regulatory clearance. Claro Argentina counters with agile spectrum holdings and AI-driven network-resource orchestration that lifts peak capacity 18% while trimming energy per bit by 14%. Movistar positions itself as the enterprise-transformation partner, offering managed security, multi-cloud orchestration, and software-defined WAN overlays that ride on its nationwide fiber spine.

Technology differentiation remains central. Personal (Telecom) recorded Argentina’s fastest 5G median throughput at 432 Mbps after upgrading to 200-MHz carrier aggregation in the sub-6 GHz band. Claro built 400 5G radio nodes by mid-2025 and expects 60% population coverage by 2028, leveraging Nokia air-scale radios that support future 6 GHz extensions. Movistar’s edge-cloud collaboration with hyperscale partners offers ultra-low latency for VR training simulators in automotive plants. The pace of small-cell densification, use of open-RAN pilots, and nationwide IPv6 migrations provide further axes of competition that enrich the Argentina telecom MNO market.

Strategic moves during 2024-2025 illustrate the spectrum of competitive responses. Telecom Argentina floated a USD 100 million sustainability-linked bond to finance renewable-energy PPAs that quarantine future electricity costs. Claro earmarked USD 200 million for AI-enhanced fiber rollouts, reducing truck rolls through predictive maintenance. Telecentro’s full-fiber conversion underscores the lure of gigabit tiers bundled with 5G mobile lines, showing how fixed assets fortify wireless value propositions. Despite occasional tariff wars, pricing is less dominant than network quality and service integration in shaping share shifts, a reality that aligns with renewed pricing freedom restored when ICT services lost “public-utility” status in 2024.

Argentina Telecom MNO Industry Leaders

Claro Argentina

Movistar Argentina

Personal (Telecom Argentina S.A)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Claro Argentina’s 5G network expansion reached 400 radio stations toward its 60% coverage target for 2028.

- February 2025: Telefónica agreed to sell its Argentine subsidiary to Telecom Argentina for USD 1.245 billion; the deal entered a six-month regulatory review.

- February 2025: Telecom Argentina filed its 2024 Form 20-F with the U.S. SEC, disclosing a USD 4.78 billion market capitalization

- October 2024: ENACOM released 150 MHz of additional 3.5 GHz spectrum to stimulate 5G competition.

Argentina Telecom MNO Market Report Scope

Telecom or Telecommunication is the long-range transmission of information by electromagnetic means.

Argentina Telecom MNO Market includes in-depth trend analysis based on connectivity like Fixed Networks, Mobile Networks, and Telecom Towers. The telecom services are divided into Voice Services (Wired and Wireless), Data and Messaging Services, OTT, and PayTV Services. The adoption of telecom services is likely driven by several factors, including an increasing demand for 5G.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming, Enterprise and Wholesale etc.) |

End-User

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming, Enterprise and Wholesale etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the projected value of the Argentina telecom MNO market in 2031?

The market is expected to reach USD 7.96 billion by 2031, growing at a 5.18% CAGR.

Which service category holds the largest revenue share?

Data and internet services contributed 62.08% of revenue in 2025.

How fast is the enterprise segment expanding?

Enterprise mobile connections are forecast to grow at a 5.65% CAGR through 2031.

What share of connections does consumer prepaid represent?

Pre-paid lines make up 61% of total mobile subscribers as of 2026.

How much additional 3.5 GHz spectrum was released in 2024?

ENACOM opened 150 MHz-100 MHz from ARSAT and 50 MHz from its own allocation.

Page last updated on: