Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

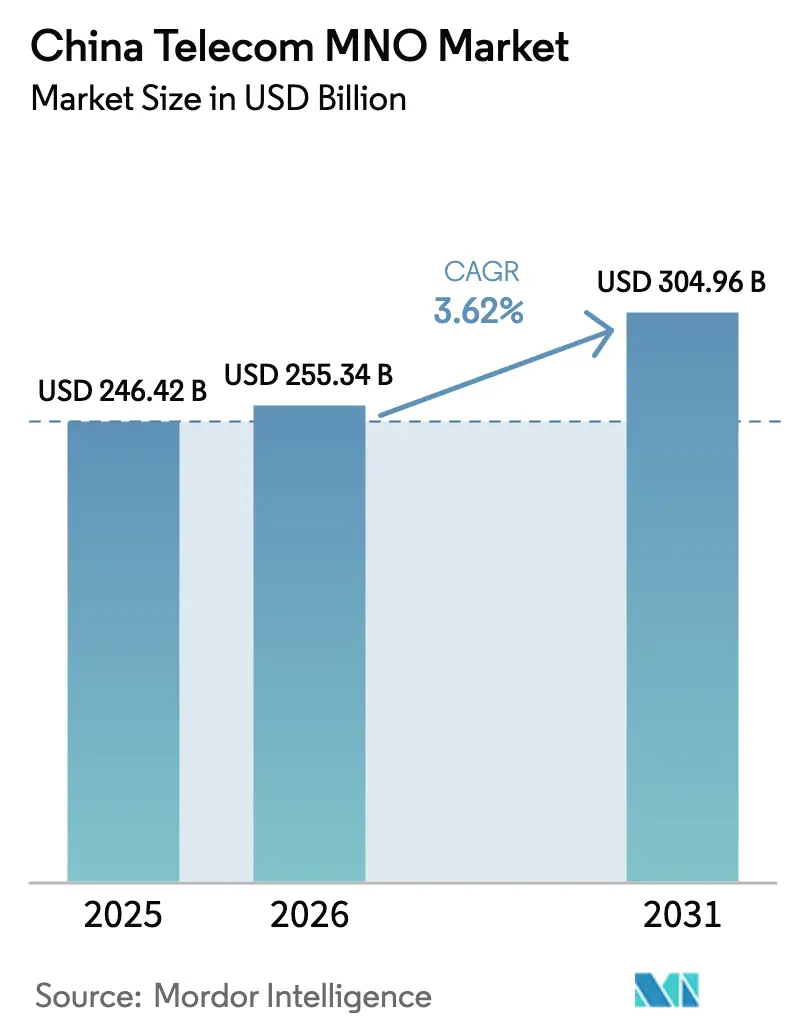

| Base Year Market Size (2025) | USD 246.42 Billion |

| Market Size (2026) | USD 255.34 Billion |

| Market Size (2031) | USD 304.96 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

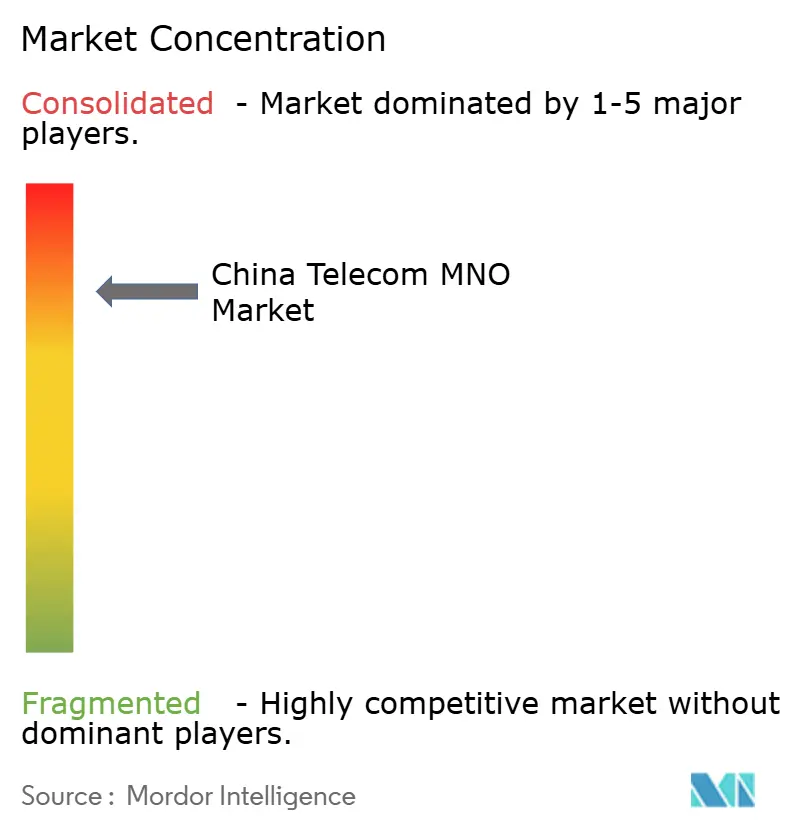

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Telecom MNO Market Analysis by Mordor Intelligence

The China Telecom MNO Market size is expected to grow from USD 246.42 billion in 2025 to USD 255.34 billion in 2026 and is forecast to reach USD 304.96 billion by 2031 at 3.62% CAGR over 2026-2031.

This steady expansion reflects the shift from raw subscriber acquisition toward value-centric monetization as mobile penetration levels exceed the 115% mark nationwide. Investment momentum is pivoting to 5G-Advanced rollout, China Mobile alone targets 2.8 million active 5G sites by end-2025, while operators channel capital toward cloud-native platforms, industrial IoT, and API-based revenue streams. Enterprise digitalization, green-network incentives, and the government-backed 6 GHz spectrum designation collectively underpin mid-term growth, even as OTT substitution and subscriber saturation temper legacy revenues. Competitive focus has moved decisively from coverage expansion to differentiated edge computing, cloud-network convergence, and AI-optimized operations that protect margins in a high-capex environment.

Key Report Takeaways

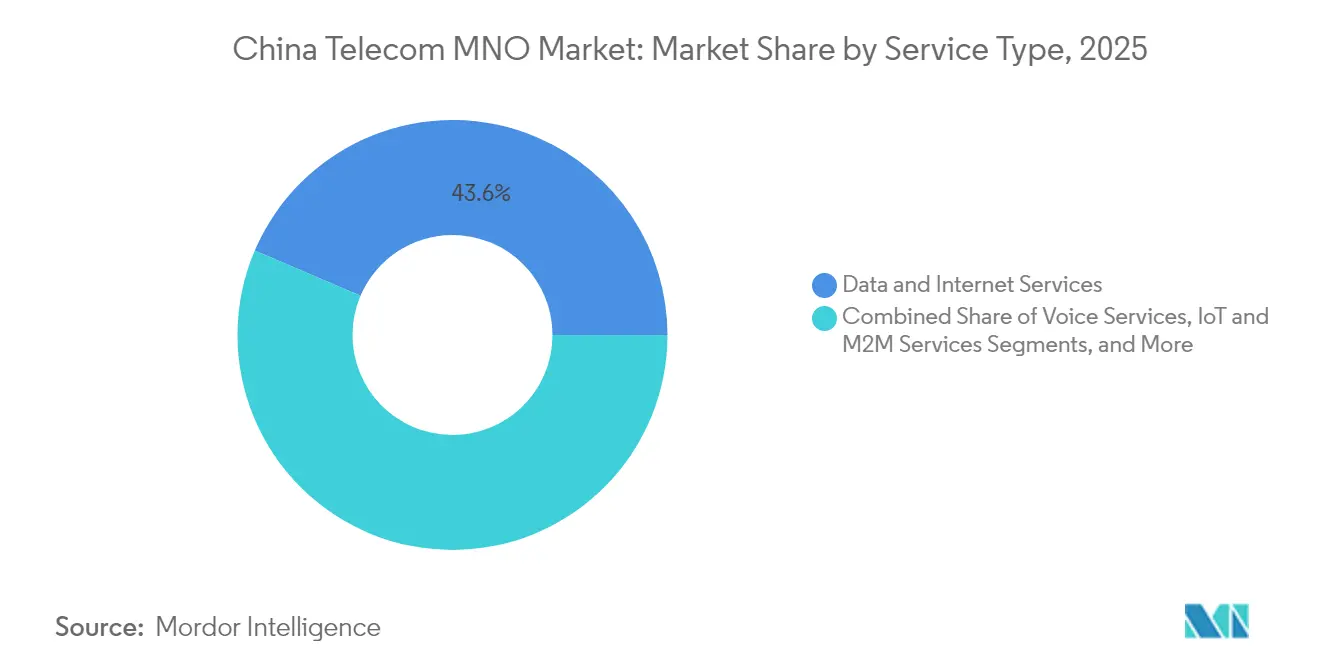

- By service type, data and internet services led with 43.58% of China Telecom MNO market share in 2025, while IoT and M2M services are advancing at a 3.78% CAGR through 2031.

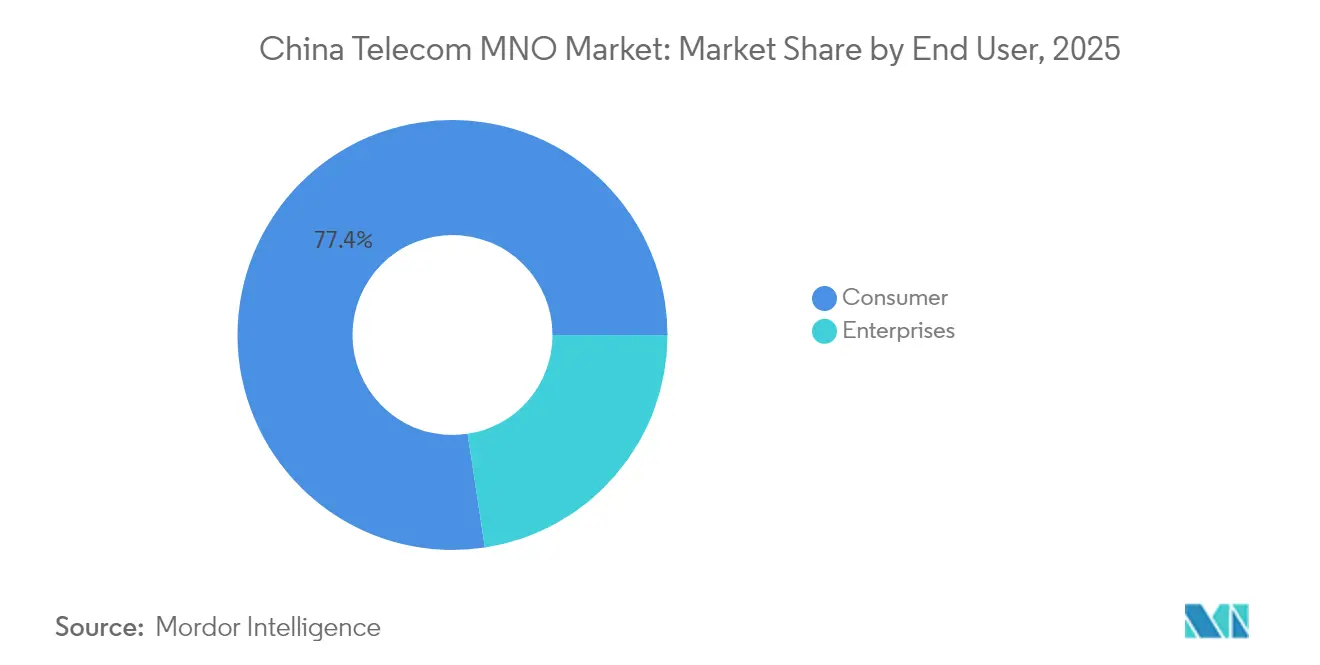

- By end user, consumer connections accounted for 77.41% of the China Telecom MNO market size in 2025, whereas enterprise segments are projected to grow at a 4.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National 5G-Advanced rollout and CAPEX support | +1.2% | Beijing, Shanghai, Guangzhou, national spill-over | Medium term (2-4 years) |

| Enterprise cloud-network convergence demand surge | +0.9% | Tier 1 and Tier 2 urban clusters | Medium term (2-4 years) |

| Gigabit-fiber adoption lifting broadband ARPU | +0.6% | Urban areas, expanding to county towns | Long term (≥ 4 years) |

| Explosive mobile-data traffic from short-video and XR | +0.8% | Youth-dense metropolitan zones | Short term (≤ 2 years) |

| Monetization of open-network APIs (GSMA Open Gateway) | +0.4% | Nationwide, roaming corridors | Long term (≥ 4 years) |

| Green-network incentives for AI-optimised energy savings | +0.3% | Industrial zones, hyperscale data-center provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National 5G-Advanced Rollout and CAPEX Support

China’s three state-owned operators are in the middle of the world’s largest 5G-Advanced build-out, backed by MIIT’s preferential financing and 6 GHz spectrum allocations. China Mobile plans 2.8 million 5G cells, and China Unicom targets blanket coverage across 300 cities by 2025, enabling network slicing and edge-cloud synergies essential for industrial automation. Shared-infrastructure agreements reduce redundant spending, while access to state bank credit lines sustains the multi-year capex cycle. The resulting densification supports ultra-low-latency services, positioning the China Telecom MNO market as the global reference for massive machine-type communications.

Enterprise Cloud-Network Convergence Demand Surge

Digital-transformation mandates across manufacturing and e-government are pushing organizations toward integrated connectivity and cloud stacks. Operators are leveraging nationwide fiber backbones and IDC assets to deliver one-stop SD-WAN, private 5G, and hybrid-cloud offerings, such as China Mobile’s Dayin computing platform [1] South China Morning Post, “China Mobile: Latest News and Updates,” scmp.com. The shift lifts average contract values and deepens stickiness via managed security, accelerating the China Telecom MNO market’s B2B revenue mix. Demand is clustered in Tier 1 tech corridors yet ripples into provincial industrial parks where policy incentives promote smart-factory pilots.

Explosive Mobile-Data Traffic from Short-Video and XR

Short-video apps have reached 1.04 billion monthly users with average watch time above 156 minutes, pushing packet volumes to record highs [2]GSMA Intelligence, “China Telecom: Leveraging Gaming Opportunity,” gsma.com. Emerging XR commerce and holographic livestreams intensify peak-time congestion, compelling operators to deploy AI-assisted traffic management and edge caching. Premium unlimited tiers, differentiated by guaranteed throughput, deliver incremental ARPU that cushions price pressure in the China Telecom MNO market. Enhanced backhaul and MEC nodes are now priority capex items, especially in entertainment-heavy megacities.

Green-Network Incentives for AI-Optimized Energy Savings

Carbon-neutrality pledges obligate operators to trim power intensity per bit. China Mobile and ZTE reported 25% energy cuts through AI-driven base-station sleep modes under the Green Telco Cloud program [3]China Mobile Limited, “Sustainability Report 2024,” chinamobileltd.com. Subsidized green-equipment loans lower the total cost of ownership, letting operators reinvest savings into 5G-Advanced upgrades. AI orchestration also supports predictive maintenance, curbing outages and elevating service reliability, a differentiator in the China Telecom MNO market’s enterprise segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-subscriber saturation | -0.7% | National, most pronounced in Tier 1 cities | Short term (≤ 2 years) |

| OTT substitution of legacy voice and SMS | -0.5% | National, accelerated in urban demographics | Medium term (2-4 years) |

| Provincial price wars in digital-government tenders | -0.4% | Provincial and municipal markets, concentrated in competitive regions | Medium term (2-4 years) |

| Export-control risk for 5G core semiconductor supply | -0.3% | National, with critical impact on infrastructure deployment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mobile-Subscriber Saturation

Penetration exceeding 115% in the largest conurbations leaves little room for organic SIM additions. Growth now hinges on retention, multi-device data plans, and IoT provisioning. While family buckets and smart-device bundles slow churn, ARPU uplift remains modest, pressing operators to extract more lifetime value per account. The saturation ceiling weighs on the consumer slice of the China Telecom MNO market, shifting strategic weight toward enterprise and vertical-IoT contracts.

OTT Substitution of Legacy Voice and SMS

WeChat, DingTalk, and burgeoning video-call apps now mediate most interpersonal communication, crushing high-margin voice and SMS receipts. RCS adoption offers limited recovery, as users perceive OTT features as the default. Operators are redirecting network investments toward data monetization layers, API exposure, slice-based quality of service, and content bundling, to recoup the revenue slide. The pivot is critical to sustain profitability in the China Telecom MNO market as legacy pillars erode.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Dominance Meets IoT Ascendancy

Data and Internet Services held 43.58% China Telecom MNO market share in 2025, reflecting the nation’s mobile-first digital ecosystem anchored by cloud gaming, HD streaming, and cash-light retail. High-capacity 5G-Advanced cells and converged fiber backbones underpin sustained data-traffic growth, while differentiated speed tiers and unlimited bundles sustain incremental ARPU. The rise of edge-computing nodes near manufacturing belts drives premium connectivity demand, converting bandwidth into productivity gains for Industry 4.0 adopters. Conversely, Voice and Messaging revenues continue their structural decline as OTT channels absorb person-to-person communications. Operators mitigate dilution through voice-over-NR and enterprise-grade unified-communications packages that piggyback on existing MPLS circuits.

In parallel, IoT and M2M Services are expanding at a 3.78% CAGR, set to capture outsized incremental value within the China Telecom MNO market size. Over 2 billion licensed cellular IoT endpoints are expected online by 2030, spanning smart-meter clusters, AGV fleets, and connected agriculture zones. Operators exploit platform economics, device management portals, SIM lifecycle automation, and integrated billing to deepen client lock-in. Revenue per connection is lower than consumer lines, yet gross margins improve owing to minimal customer-care overhead. Government mandates for vehicle telematics and electricity metering further institutionalize IoT traffic growth, reinforcing long-run revenue visibility.

By End User: Consumer Scale versus Enterprise Velocity

The consumer segment commanded 77.41% of 2025 billings, yet its expansion is plateauing around low-single-digit rates. Growth depends on premium content bundles, AR/VR media passes, and family-share data vaults designed for multi-SIM households. Subsidized handset plans grew scarce after 2024, signaling a maturation stage where experience quality rather than subsidy size drives retention in the China Telecom MNO market. Operators now emphasize gamified loyalty schemes, video-first data packs, and youth-oriented micro-loans mediated via in-app wallets to defend ARPU.

Enterprise accounts, meanwhile, post the fastest topline acceleration at a 4.12% CAGR, feeding on nationwide smart-factory programs, municipal IoT grids, and digital-government clouds. Private 5G islands inside industrial parks demand stringent latency and SOP-aligned cybersecurity services that command premium fees and multi-year contracts. The segment remains under-penetrated by global benchmarks, suggesting ample runway for the China Telecom MNO market. Bundled offerings that fuse SD-WAN, PaaS, and managed security resonate with mid-size corporates lacking in-house IT depth. Successful bids often bundle consulting, hardware integration, and after-sales analytics dashboards, turning operators into holistic ICT partners.

Geography Analysis

China’s east-coast economic triad, Beijing-Tianjin-Hebei, the Yangtze River Delta, and the Greater Bay Area, accounts for the lion’s share of premium ARPU and early 5G-Advanced usage. Saturated urban footprints fuel experimentation with mmWave small-cells and AI-edge nodes that anchor XR retail and autonomous mobility trials. Provincial governments award spectrum refarming incentives to encourage sub-6 GHz densification, ensuring the China Telecom MNO market maintains nationwide technological parity.

Central provinces such as Hubei, Henan, and Hunan are experiencing a capex-upcycle powered by industrial park digitization grants. High-speed rail corridors double as fiber conduits, enabling gigabit-grade mobile broadband along transit arteries. Operators stage joint-venture data centers near hydropower-rich regions to lower PUE ratios, aligning with carbon-target mandates and securing green power certificates tradable on provincial exchanges.

Western hinterlands, Sichuan, Shaanxi, and Xinjiang, benefit from rural revitalization funds that underwrite 5G tower expansion and satellite-terrestrial hybrid backhaul. Such deployments unlock video-enabled remote healthcare and precision farming, enlarging the addressable China Telecom MNO market size while advancing digital-inclusion objectives. Border prefectures leverage new gateways to neighboring Belt and Road economies, facilitating seamless roaming and low-latency trade data links critical to cross-border e-commerce.

Competitive Landscape

The market remains an oligopoly anchored by China Mobile, China Telecom, and China Unicom; combined, they control well above 90% of aggregate service revenues. China Broadnet, the broadcast player granted 5G spectrum in 2022, piggybacks on shared-infrastructure deals to expedite market entry, yet progress remains measured. Differentiation increasingly rests on enterprise-cloud orchestration, AI-assisted network operations, and cross-border capacity leasing aligned to Belt and Road outbound flows.

China Mobile leverages unrivaled scale to negotiate volume-based vendor discounts, sustaining the lowest network unit cost in the China Telecom MNO market. Its 2024 revenue reached RMB 1,040.8 billion (USD 143.2 billion) on the back of aggressive 5G package upsells. China Telecom positions itself as the integrated cloud-network specialist, operating more than 700 edge nodes nationwide and marketing secure-access service edge (SASE) bundles to multinationals. China Unicom capitalizes on its international cable partnerships, SEA-ME-WE 6 and Pacific Light Cable, to court global hyperscalers requiring resilient Asia-Europe latency routes.

Strategic moves in 2024-2025 highlight a focus on vertical depth over blanket consumer plays. Multi-operator service agreements govern neutral-host indoor DAS in commercial high-rises, reducing redundant capex. Joint energy-storage procurement pools improve bargaining power in the lithium-battery supply chain, helping contain opex in power-hungry 5G-Advanced sites. Partnerships with cloud-native security vendors accelerate zero-trust adoption among SMEs, further differentiating enterprise portfolios in the China Telecom MNO market.

China Telecom MNO Industry Leaders

China Mobile Limited

China Telecom Corporation Limited

China United Network Communications Group Co., Ltd.

China Broadnet (China Broadcast Network Co., Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: China Mobile’s Hong Kong arm purchased a 15% stake in HKBN for USD 155 million, aiming to cross-sell enterprise fiber and managed cloud services in the territory.

- March 2025: The Cyberspace Administration of China released draft amendments to the Cybersecurity Law, imposing higher fines on network operators that fail to meet data-protection benchmarks.

- December 2024: China Mobile tendered a USD 1 billion offer to acquire full control of HKBN, reinforcing its regional growth strategy pending regulatory approval.

- September 2024: The Network Data Security Management Regulation came into force, formalizing incident-reporting timelines and cross-border data-transfer controls for telecom carriers.

China Telecom MNO Market Report Scope

Telecom or Telecommunication is the long-range transmission of information by electromagnetic means.

China Telecom MNO Market includes in-depth trend analysis based on connectivity like Fixed Networks, Mobile Networks, and Telecom Towers. The telecom services are divided into Voice Services (Wired and Wireless), Data and Messaging Services, OTT, and PayTV Services. Several factors, including an increasing demand for 5G, likely drive the adoption of telecom services.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the China Telecom MNO market?

The China Telecom MNO market size is USD 255.34 billion in 2026.

How fast is China’s mobile-network operator segment growing?

Aggregate revenue is projected to rise at a 3.62% CAGR between 2026-2031.

Which service category holds the largest share?

Data and Internet Services command 43.58% China Telecom MNO market share in 2025.

Which service is growing the quickest?

IoT and M2M Services record the highest forecast CAGR at 3.78% through 2031.

How are operators countering subscriber saturation?

Strategies include enterprise cloud-network convergence, IoT platform monetization, and AI-optimized energy savings to lift margins.

What drives enterprise segment momentum?

Nationwide smart-factory programs and e-government cloud mandates are pushing enterprise revenues to a 4.12% CAGR through 2031.

Page last updated on: