Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Uruguay Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, Other Services), End User (Enterprises, Consumers). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

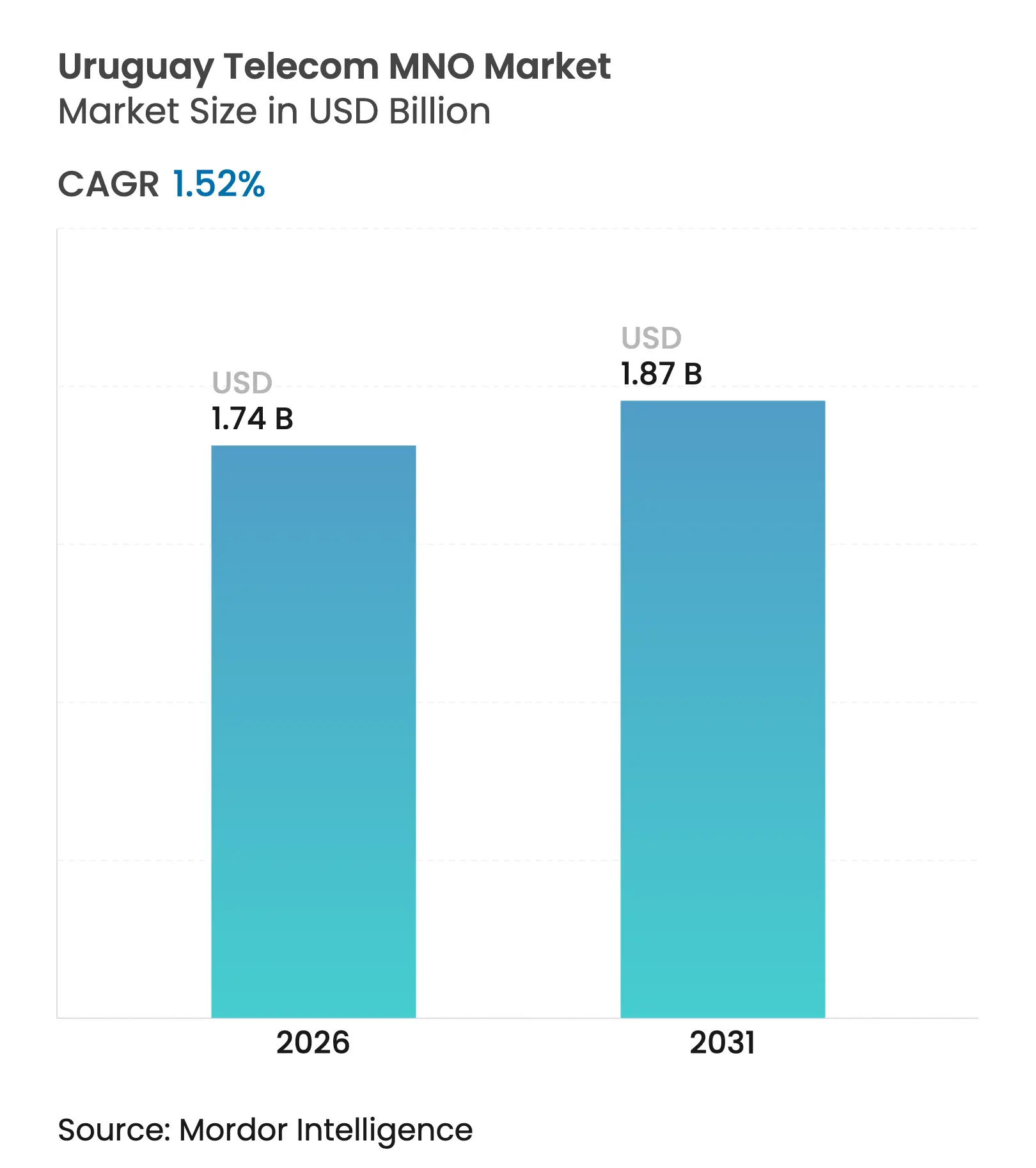

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 1.87 Billion |

| Growth Rate (2026 - 2031) | 1.52 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

This moderate expansion stems from a mature subscriber base, the end of ANTEL’s internet monopoly in 2022, and Millicom’s USD 440 million purchase of Telefónica’s local unit in 2025. Accelerated fiber-to-the-home (FTTH) build-outs already cover 60% of fixed connections, while 5G densification aims for 500 base stations by February 2025. Median download speeds of 225.50 Mbps for fixed and 169.57 Mbps for mobile services reinforce Uruguay’s position as a regional digital leader. Enterprise demand for secure, high-capacity links is rising under the Digital Agenda 2025, and an improved international gateway via the new Firmina submarine cable reduces IP-transit costs, making cross-border cloud connectivity more affordable.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Accelerated FTTH roll-out & 5G densification Accelerated FTTH roll-out & 5G densification | +0.4% | National, Montevideo & coastal regions | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.4% | Geographic Relevance :National, Montevideo & coastal regions | Impact Timeline :Medium term (2-4 years) |

Enterprise digitalisation demand for secure connectivity Enterprise digitalisation demand for secure connectivity | +0.3% | National, Montevideo business district | Long term (≥ 4 years) | |||

Surge in mobile data usage & content streaming Surge in mobile data usage & content streaming | +0.2% | National, urban areas | Short term (≤ 2 years) | |||

Government’s Uruguay Digital 2025 incentives Government’s Uruguay Digital 2025 incentives | +0.2% | National, rural connectivity focus | Long term (≥ 4 years) | |||

Maldonado-to-US submarine cable lowers IP transit costs Maldonado-to-US submarine cable lowers IP transit costs | +0.1% | National, enterprise segment | Medium term (2-4 years) | |||

Blockchain-enabled digital-ID pilots boost IoT/M2M Blockchain-enabled digital-ID pilots boost IoT/M2M | +0.1% | Pilot cities | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Accelerated FTTH roll-out and 5G densification

ANTEL’s network-upgrade program moved from 300 to a planned 500 5G sites within a single year, supporting mass-market low latency applications and enterprise private-network use cases.[1]RCR Wireless News Editors, “ANTEL targets 500 5G sites by 2025,” rcrwireless.com Fiber already powers 77% of fixed broadband subscriptions, giving Uruguay average fixed speeds above 225 Mbps and allowing operators to bundle 400 Mbps to 1 Gbps plans profitably. Rapid densification also enables nationwide carrier aggregation, which lifts spectral efficiency and helps meet surging video demand. The result is a virtuous cycle: each incremental tower raises utilization of existing fiber backhaul, improving the payback period of earlier capital outlays. Political debate on fiber rollout pace has revived, yet bipartisan consensus recognizes that nationwide gigabit connectivity remains vital to economic resilience. [2]El Observador Newsroom, “ANTEL’s data-center revenues soar,” elobservador.com.uy

Enterprise digitalisation demand for secure connectivity

Corporate cloud migration, a USD 1 billion IT-export ambition for 2025, and mandatory cybersecurity standards under the Digital Agenda 2025 are turning connectivity into a board-level priority. [3]Trade.gov Country Commercial Guide, “Uruguay Telecommunications Services,” trade.gov Large banks, logistics firms, and agri-exporters now seek direct fiber links into ANTEL’s Tier III data center, which earned USD 39 million between 2016–2020 and has doubled capacity for hyperscalers. Private wireless networks for ports and special economic zones are emerging, while managed SD-WAN and SASE bundles position carriers as end-to-end digital-transformation partners. This higher-value traffic supports average revenue per line well above consumer levels, offsetting slow retail growth.

Surge in mobile data usage and content streaming

Streaming services account for most incremental traffic as Netflix, Prime Video, and Disney+ take 83% of Latin America’s SVoD market. Uruguay’s over 2.5 million social-media users—Over 75% of the population—create constant uplink demand for short-form video on TikTok and Instagram. Operators respond with zero-rated bundles, dynamic video-quality management, and premium unlimited plans that monetize heavy usage without congesting networks. The move to 5G Standalone further lowers latency for gaming and AR, strengthening customer willingness to upgrade. Mobile broadband lines topped 3.67 million in 2024, surpassing 212% penetration, proving that usage intensity, rather than new SIM additions, drives revenue growth.

Government’s Uruguay Digital 2025 incentives

The Digital Agenda targets universal fixed-line coverage, rural 5G pilots, and a national cybersecurity center to protect critical infrastructure. Tax credits and spectrum-fee rebates encourage private-sector investment in underserved districts, while public-service digitization forces ministries to adopt secure connectivity. Monthly e-government transactions already exceed 10 million, so maintaining platform uptime directly affects citizen satisfaction. Google’s classification of Uruguay as a “digital sprinter” validates policy success and attracts new OTT and hyperscale edge investments. Together, these factors lengthen the growth runway for enterprise and wholesale segments of the Uruguay telecom market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

ANTEL’s legal monopoly over fixed last-mile limits competition ANTEL’s legal monopoly over fixed last-mile limits competition | -0.3% | National | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-0.3% | Geographic Relevance :National | Impact Timeline :Long term (≥ 4 years) |

Sub-scale population curbs ROI for private operators Sub-scale population curbs ROI for private operators | -0.2% | National, rural areas | Long term (≥ 4 years) | |||

High 3.5 GHz spectrum reserve prices delay 5G expansion High 3.5 GHz spectrum reserve prices delay 5G expansion | -0.1% | National | Medium term (2-4 years) | |||

Peso-USD volatility tightens capital expenditure Peso-USD volatility tightens capital expenditure | -0.1% | National | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

ANTEL’s legal monopoly over fixed last-mile limits competition

Although ISPs won the right to resell broadband in 2022, ANTEL still controls the copper and fiber loops, forcing rivals onto wholesale resale models that compress margins. Its 96.2% share of fixed internet lines underscores limited contestability, leaving price and product innovation below regional peers. Small cable operators face long payback horizons because duct access and co-location fees often exceed retail revenue in sparsely populated areas. Without structural separation, incentives to open ducts or cut wholesale prices remain weak, slowing service diversification and capping future broadband CAGR.

Sub-scale population curbs ROI for private operators

Uruguay’s over 3.3 million citizens are 96% urban and already own an average of two SIMs per person, translating into saturation that deters large-scale green-field builds. Telefónica’s 2025 exit indicates how limited scale undermines operator economics despite a stable regulatory climate. Rural coverage economics remain unattractive because cell-site costs cannot be amortized across sufficient subscribers. Consequently, operators prioritize Montevideo and coastal resorts, delaying equal-quality coverage for remote farming regions. The Uruguay telecom industry therefore relies on policy subsidies rather than pure market forces to reach smaller communities.

By Service Type: Data Services Lead Digital Transformation

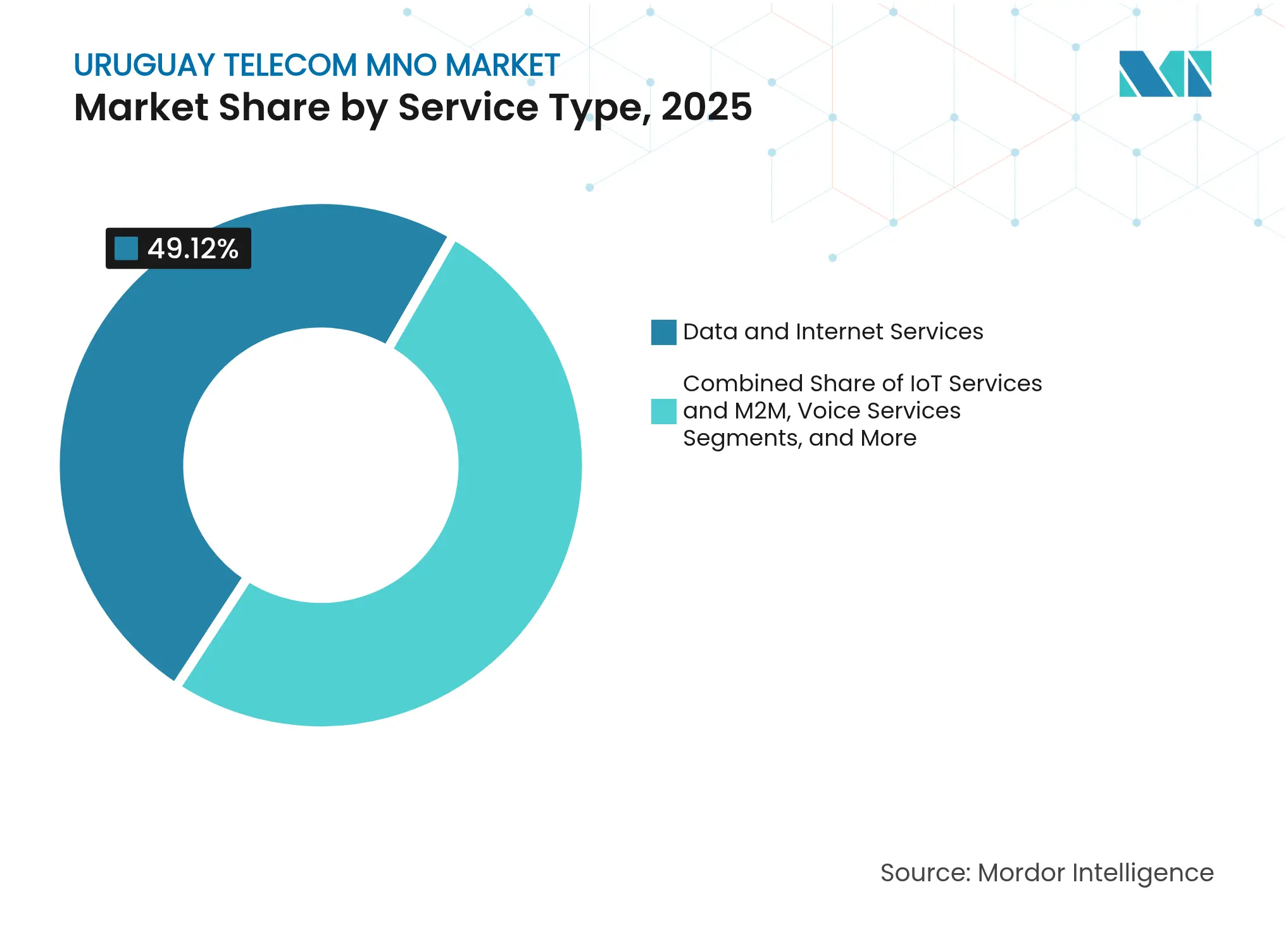

Data services commanded 49.12% of Uruguay telecom market share in 2025, underpinning the country’s reputation for advanced connectivity. The sub-segment is projected to expand at a 1.53% CAGR to 2031 as FTTH penetration deepens and 5G Standalone lifts network efficiency. Uruguay telecom market size gains in this category are tied to ARPU growth from gigabit fiber plans bundled with streaming content. Voice services, still holding 25.07% share, are transitioning to VoIP and Wi-Fi calling, stabilizing revenue despite falling minutes of use. OTT and PayTV, with 12.44% share, benefit from SVOD tie-ins yet face higher churn as younger viewers drop linear packages. Messaging and value-added services at 9.52% retain niche relevance through enterprise SMS authentication and premium mobile content.

IoT services, though only 3.85% of 2025 revenue, are the fastest-growing line at a 1.68% CAGR. Uruguay telecom market size for IoT will rise as smart-metering mandates, +Colonia eco-city, and cattle-tracking solutions scale. Operators are launching network-slice-as-a-service options that guarantee latency below 10 ms for industrial control. Regulatory clarity on spectrum for massive-IoT bands and exemptions on SIM tax for machine nodes encourage experimentation. Over the forecast horizon, IoT could shift from connectivity fee-based income to platform subscriptions that bundle device management, security, and analytics, widening operator margins.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Enterprise Segment Drives Premium Growth

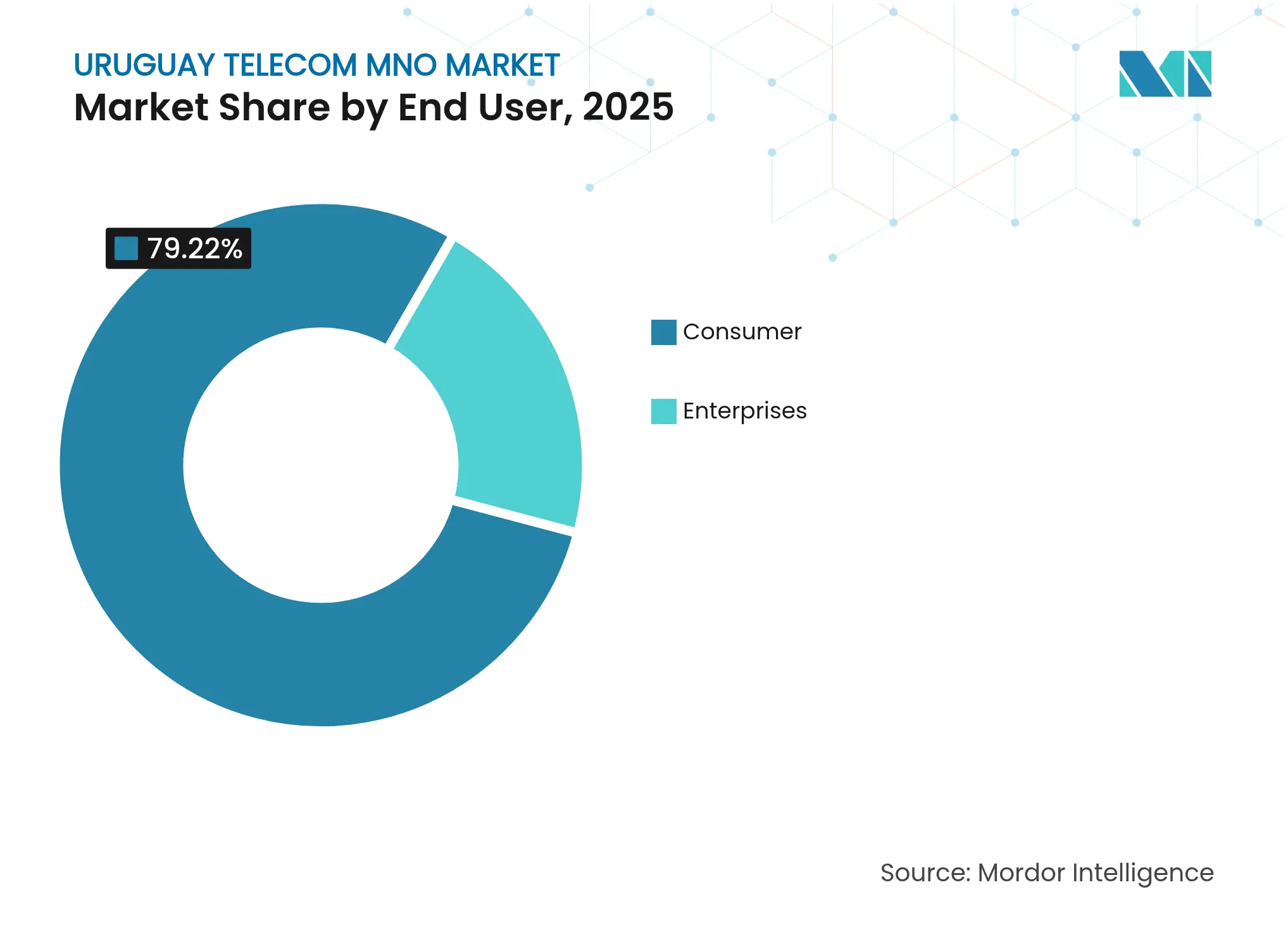

The enterprise segment held 20.78% of the Uruguay telecom market size in 2025 and is on track for a 2.02% CAGR through 2031, outpacing consumer growth. Large agribusiness exporters demand resilient SD-WAN links to U.S. cloud regions, while fintechs require low-latency fiber paths for real-time fraud detection. Data-center colocation and managed security services deepen wallet share, with ANTEL reporting 68% private-sector revenue mix in its collocation business. Uruguay’s goal to make ICT 5% of GDP in 2025 further tilts investment toward high-value corporate solutions.

Consumer services, still 79.22% of revenue, advance at a muted 1.42% CAGR as 93% internet saturation leaves limited room for new accounts. Operators defend ARPU by combining Disney+ Standard, Paramount+, and unlimited-data 5G plans, raising perceived value and lowering churn. Prepaid-to-postpaid migration continues, but incremental revenue comes chiefly from speed-tier upgrades and multi-play discounts rather than subscriber additions. The Uruguay telecom market therefore balances slow unit growth with richer per-user monetization.

Note: Segment shares of all individual segments available upon report purchase

Montevideo generates well above 50% of national telecom revenue because it hosts 1.4 million residents, the main financial district, and the bulk of data-center capacity. Fiber penetration exceeds 90% of households, and 5G coverage is nearly blanket, making the capital the earliest adopter of premium gigabit plans. Operators funnel small cells into densely populated downtown corridors to handle lunchtime video spikes, reinforcing Montevideo’s role as the profit engine of the Uruguay telecom market.

The coastal corridors of Maldonado, Punta del Este, and Rocha provide seasonal traffic surges tied to tourism. The Firmina cable’s Punta del Este landing station has turned the resort town into an unexpected wholesale hub by lowering backhaul costs to Miami. Local authorities leverage this link to attract fintech and BPM companies seeking latency below 60 ms to U.S. East Coast clouds. Infrastructure sharing among operators reduces duplicate trenching, enabling FTTH coverage to extend into smaller beach communities previously served only by coax.

Interior departments such as Tacuarembó and Rivera remain broadband-constrained, with fewer than 30 fixed lines per 100 inhabitants despite satisfactory 4G coverage. Universal-service obligations under Uruguay Digital 2025 fund microwave backhaul and passive-tower sharing, yet unit economics stay challenged. Operators pilot 5G fixed-wireless access to deliver 100 Mbps service without trenching fiber. Over time, rural digital inclusion could add incremental revenue by enabling precision agriculture and e-health, but immediate impact on the Uruguay telecom market remains modest.

Market Concentration

ANTEL continues to dominate with a 49% mobile share, a 96.2% fixed-internet share, and an unrivaled wholesale fiber footprint. Its public-sector backing unlocks low-cost capital, allowing rapid expansion to 500 5G sites by end-2025 and aggressive FTTH rollouts that keep rivals in catch-up mode. Content bundling with Disney+ and Paramount+ complements its infrastructure edge, pushing blended churn below 1.4% annually.

Millicom’s entry through its USD 440 million takeover of Telefónica’s Movistar arm consolidates private-sector resources and adds 1.8 million mobile customers overnight. Regional scale across nine Latin American markets gives it bargaining power on network equipment and roaming, positioning the company to challenge ANTEL in enterprise ICT, where global multinationals prefer multi-market suppliers. Immediate integration priorities include spectrum refarming and retail-brand migration, after which Millicom aims to exploit Uruguay’s high ARPU environment.

Claro, part of América Móvil, leverages pan-Latin roaming and handset subsidies to retain prepaid users but trails in fiber presence. It focuses on mobile-led convergence for cost-sensitive households, bundling fixed-wireless with PayTV. Under URSEC’s new infrastructure-sharing mandates, Claro negotiates dark-fiber leases from ANTEL to speed FTTH expansion. Competitive intensity is limited by overlapping network footprints and a highly penetrated subscriber base, so price wars remain rare.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Telecommunication involves transmitting information at a speed akin to face-to-face conversations. It encompasses exchanging data, voice, and video over long distances through electronic mediums.

The Uruguayan telecom market is segmented by services (voice services (wired and wireless), data and messaging services, OTT, and pay TV services.

The report provides the market sizes and forecasts in terms of value in USD for all the segments mentioned above.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Growth in India’s Luxury Beauty & Skincare Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.