Global Telecom Cable Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 115.3 Billion |

| Market Size (2031) | USD 161.39 Billion |

| Growth Rate (2026 - 2031) | 6.96% CAGR |

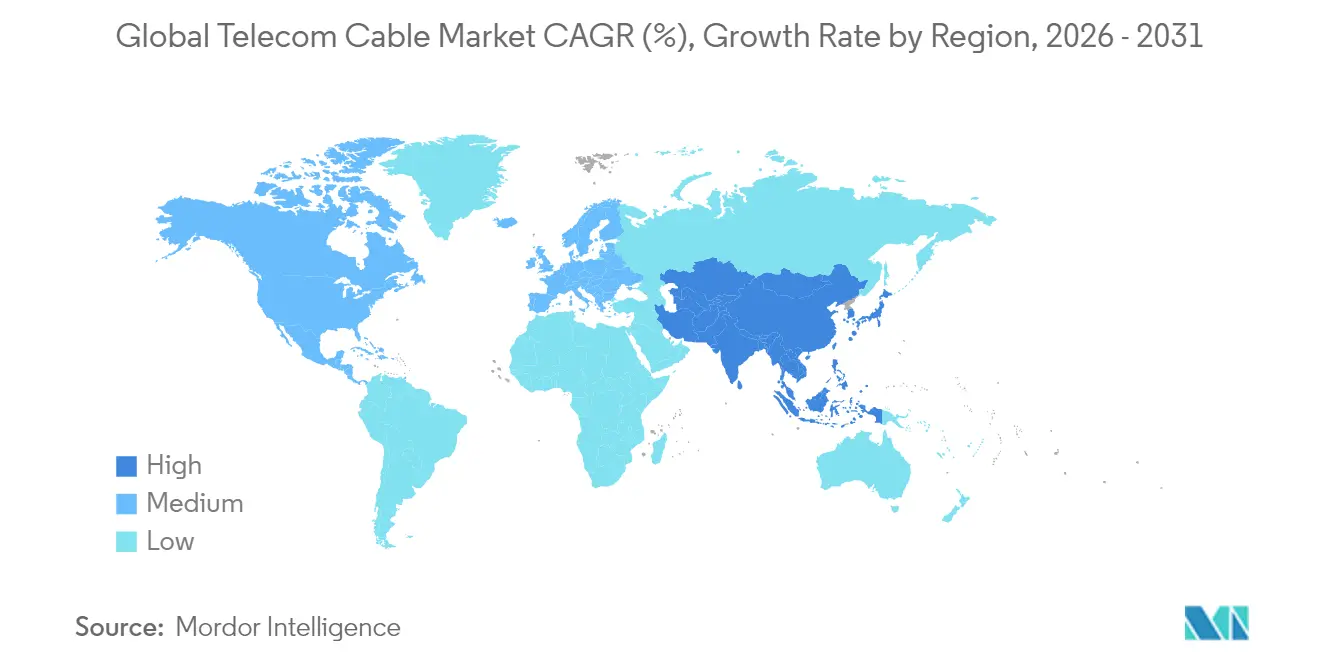

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

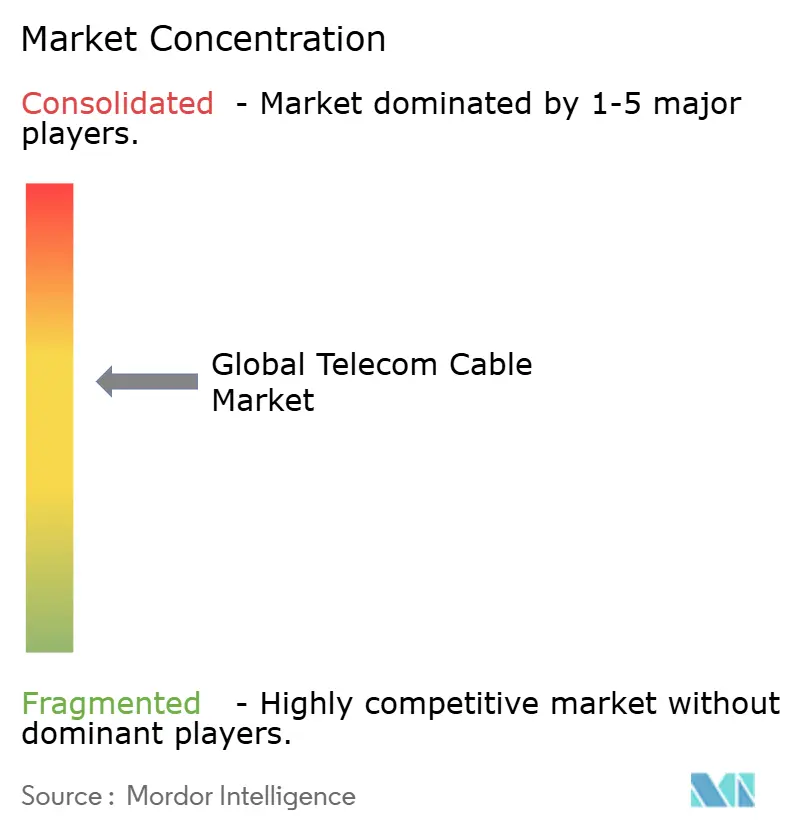

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Telecom Cable Market Analysis by Mordor Intelligence

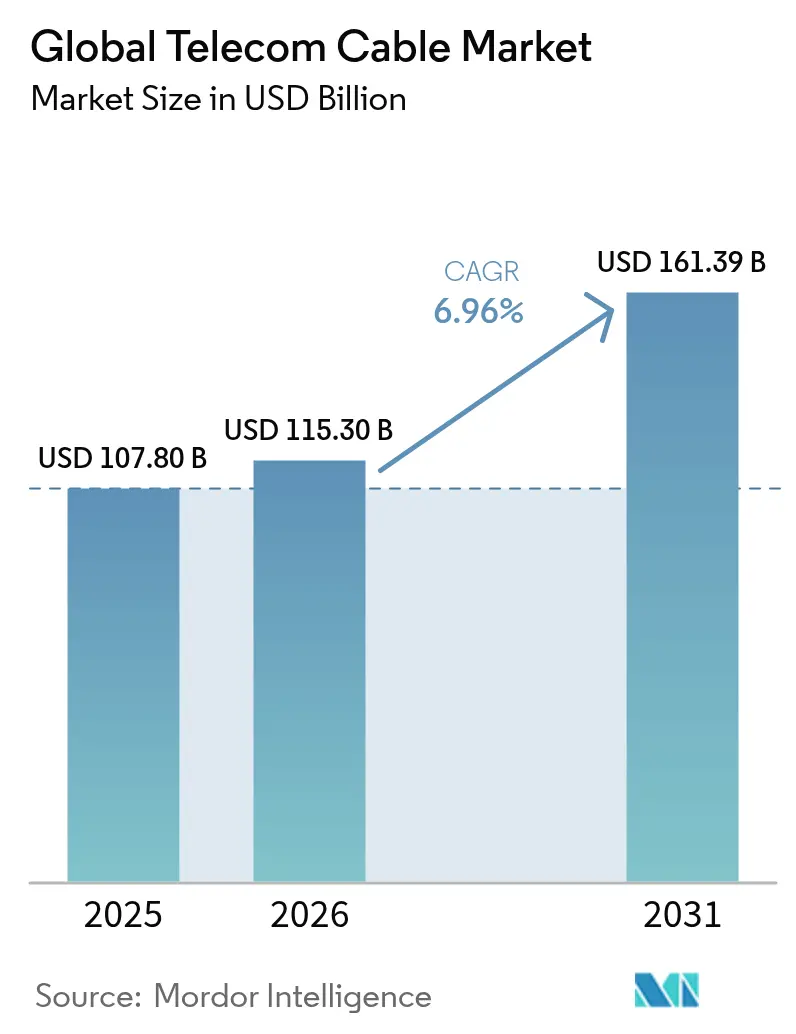

Global Telecom Cable Market size in 2026 is estimated at USD 115.3 billion, growing from 2025 value of USD 107.80 billion with 2031 projections showing USD 161.39 billion, growing at 6.96% CAGR over 2026-2031.

Healthy demand stems from relentless bandwidth growth tied to artificial intelligence processing, 5G footprint densification, and hyperscale data-center expansion. Operators are phasing out legacy copper, accelerating fiber roll-outs even as capital intensity rises. Private submarine networks commissioned by hyperscalers add another growth pillar, while rural broadband subsidies in North America and Europe inject long-tail demand. At the same time, cost inflation for underground civil works and skilled-labor scarcity temper the near-term pace, forcing firms to pursue innovative installation techniques and automation.

Key Report Takeaways

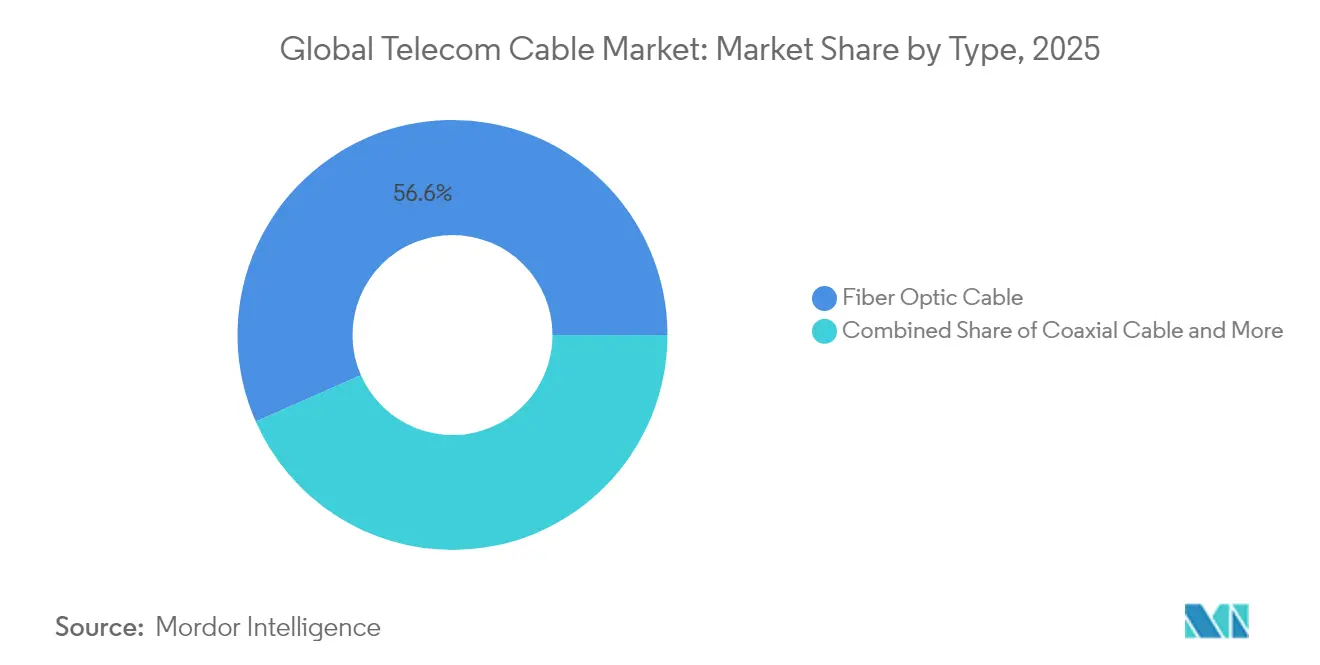

- By product type, fiber-optic cables led with 56.60% revenue share in 2025; coaxial held 2nd place, yet fiber is advancing at an 8.63% CAGR to 2031.

- By application, core and access networks captured 45.55% of the telecom cable market size in 2025; data center and distributed cloud infrastructure are growing fastest at 7.48% CAGR through 2031.

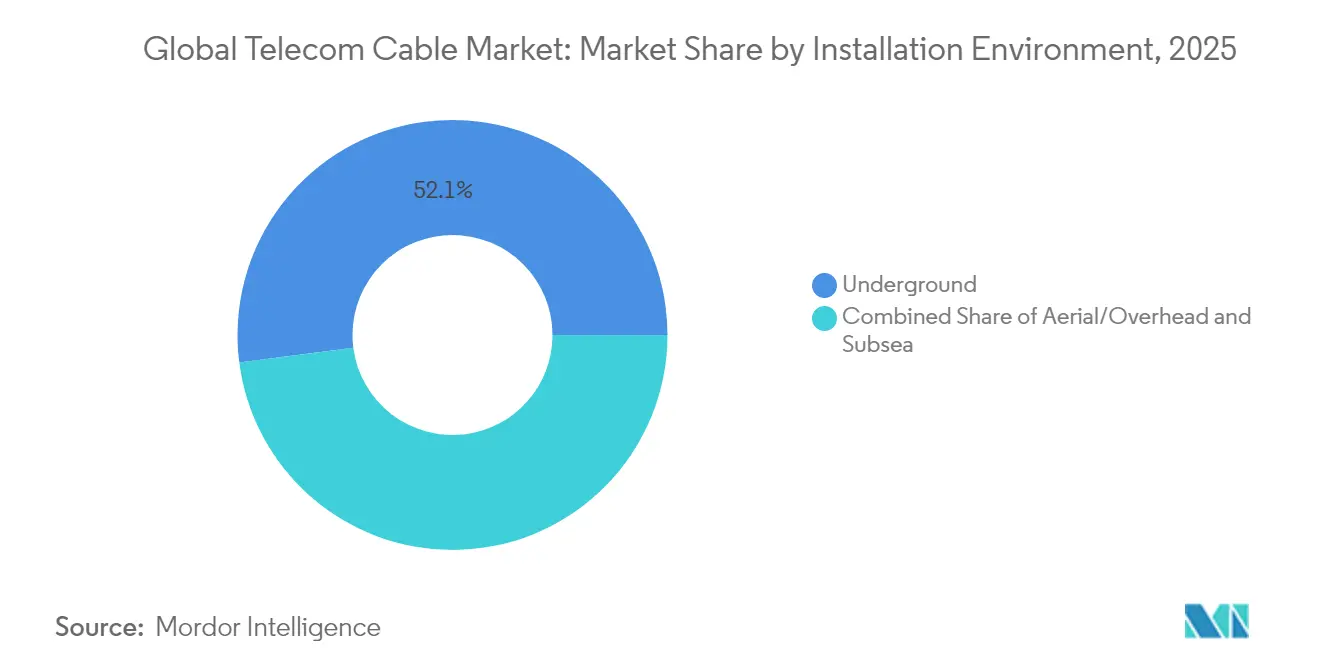

- By installation environment, underground deployments held 52.05% of the telecom cable market share in 2025, while subsea systems posted the quickest 7.99% CAGR.

- By end-user, telecom operators commanded a 58.90% share in 2025; hyperscalers and cloud providers recorded the highest 7.18% CAGR.

- By geography, Asia-Pacific dominated with a 47.10% share in 2025 and will expand at a 7.75% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Telecom Cable Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G backhaul surge and densification needs | +1.80% | Global, APAC & North America | Medium term (2-4 years) |

| Hyperscale data-center interconnect bandwidth boom | +1.50% | Global, concentrated in North America, Europe, APAC | Long term (≥ 4 years) |

| Government-funded broadband build-outs | +1.20% | North America & EU | Medium term (2-4 years) |

| IoT and smart-city connectivity proliferation | +0.80% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Backhaul Surge and Densification Needs

China’s 4.4 million live 5G sites each require far denser fiber than 4G towers, and comparable densification waves are unfolding at Verizon, NTT Docomo, and Reliance Jio. Operators embrace cloud-RAN architectures where baseband units are centralized, further multiplying fiber strands per site. Multicore fibers demonstrated by NTT at 455 Tbps over 1,017 km underscore the technology path needed to satisfy mobile traffic[1]NTT Corporation, “Multicore fiber shatters 455 Tbps record,” ntt.com.

Hyperscale Data-Center Interconnect Bandwidth Boom

GPU clusters used for AI training exchange massive data sets that overwhelm yesterday’s 100 G links. Meta’s Project Waterworth and Corning’s 1.6T component roadmap highlight how demand is spilling into completely new cable geometries, including multicore fiber designs able to support 800G and beyond.

Government-Funded Broadband Build-Outs

The USD 42.45 billion BEAD program in the United States and the European Union’s Digital Decade both stipulate gigabit targets that require fiber to every locality. Domestic-sourcing rules prompt manufacturers such as Prysmian to expand Tennessee and North Carolina plants, while training programs aim to mitigate labor gaps.

IoT and Smart-City Connectivity Proliferation

Municipalities deploy edge-dense networks linking cameras, traffic sensors, and utility meters. Projects in Morrow, Georgia, and Cambridge, England, show how smart-city fiber grids handle everything from public Wi-Fi to real-time telemetry. Enterprise campuses replicate the model, using Fiber-to-the-Edge topologies to power occupancy sensors and building automation.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Underground deployment costs two-to-three times aerial | -1.10% | Global, acute in dense urban areas | Short term (≤ 2 years) |

| Skilled-labor shortages are delaying rollouts | -0.90% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Underground Deployment Costs Two to Three Times More Than Aerial Alternatives

Median underground placement now costs USD 18.25 per foot versus USD 6.55 for aerial lines, with labor accounting for up to 80 % of the trenching bill. Rocky terrain or downtown utility congestion pushes figures past USD 20 per foot, compelling operators to postpone projects or pivot toward micro-trenching where regulators allow.

Skilled-Labor Shortages Delaying Fiber Rollouts

Tens of thousands of fiber splicers, linemen, and network engineers are missing from payrolls despite record wage offers. Training consortia in 23 US states, plus AT&T-Corning academies, are scaling up, yet graduation pipelines lag near-term demand. The gap inflates project budgets and elongates delivery timelines, especially for rural builds under BEAD[2]Fiber Broadband Association, “Workforce initiative expands to 23 states,” lightwaveonline.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fiber-Optic Dominance Accelerates

Fiber-optic solutions captured 56.60% of the telecom cable market share in 2025 and are advancing at an 8.63% CAGR toward 2031. Suppliers lean on physics: Glass can carry terabits over kilometers without repeaters, a feat copper cannot match. High-density designs such as Prysmian’s 864-fiber Sirocco Extreme push 11.5 fibers per square millimeter, allowing operators to squeeze capacity into existing ducts.

Coaxial and twisted-pair sections of the telecom cable market continue serving hybrid fiber-coax networks and niche PoE+ runs, yet their relevance dwindles as enterprises migrate to all-optical LANs. Composite cables that fuse power conductors with glass strands are a bridge technology, easing building-automation upgrades while preserving legacy endpoints.

By Application: Data Centers Drive Innovation

Core and access networks accounted for 45.55% of the telecom cable market size in 2025, reflecting decades of operator investment. Data center and distributed cloud interconnects, however, are the fastest-rising slice at 7.48 % CAGR through 2031. AI clusters require topologies where every server GPU must reach others at 800G or 1.6T speeds, pushing multicore and hollow-core fiber trials from China Telecom and ZTE into pre-production.

Video broadcast and CATV still consume bandwidth as 4K and 8K streams proliferate, but growth is muted compared with hyperscale and enterprise AI needs. Campus LANs also pivot to fiber thanks to reduced electromagnetic interference and simplified pathways for converged building systems.

By Installation Environment: Subsea Surge Reflects AI Investments

Underground plant retained 52.05% of 2025 revenue, driven by urban regulations and weather resilience. Yet subsea networks will rise fastest, at 7.99% CAGR, as hyperscalers lay private trans-oceanic systems that bypass carriers and tailor routes for machine learning replication cycles. Meta’s latest Pacific cable exemplifies the shift, coupling 24-fiber pairs with space-division multiplexing amplifiers.

Aerial builds remain vital for cost-sensitive rural runs, particularly across North America’s corn belt and India’s semi-urban corridors, where poles exist and trench rights are scarce. Meanwhile, incidents such as the Red Sea cable cut that disrupted 90 % of Europe-Asia traffic underscore the strategic value and vulnerability of subsea corridors.

By End-User Industry: Hyperscaler Transformation

Telecom operators still bought 58.90% of cables in 2025, but hyperscalers and cloud providers display the fastest 7.18% CAGR. Giants like Google and Microsoft increasingly negotiate directly with producers for custom ribbon counts and tailored attenuation specs. Operator responses include mergers and fiber asset grabs, witness Verizon’s Frontier purchase to shore up scale and bargaining power.

Government and utility entities maintain stable demand as they digitize grids and municipal services. Defense contracts, such as Verizon’s multi-base 5G roll-out, introduce stringent cybersecurity and ruggedization criteria that only a narrow supplier bench can meet.

Geography Analysis

Asia-Pacific held 47.10% of the telecom cable market share in 2025 and is projected to post a 7.75% CAGR through 2031, buoyed by China’s additional 4.5 million 5G macro-cells planned for 2025 and India’s data-center construction wave. Japan’s NTT continues to pioneer multicore fiber, securing national capacity gains and exporting patents to allies. Regional manufacturing clusters in Shenzhen, Guangzhou, and Hsinchu further cement APAC scale advantages.

North America ranks second, fueled by BEAD subsidies and hyperscaler outlays. Operators target 30 million new fiber passings by 2025, while private-equity financing of middle-mile routes across the Midwest underpins long-haul demand. Cross-border systems such as C3ntro’s Tikva network strengthen US-Mexico integration, supporting latency-sensitive fintech and content applications.

Europe shows patchy progress: France and Spain exceed 60 % FTTH take-up, whereas Germany sits under 30 %, necessitating EUR 44.3 billion additional spend. Anti-dumping duty on Indian cable imports raises costs but shields local firms. Channel traffic reallocations around the Baltic and Mediterranean underscore geopolitical sensitivity, spurring redundant landing sites in Portugal and Greece.

Competitive Landscape

The telecom cable market features moderate consolidation. The top five groups, Prysmian, Corning, CommScope, Fujikura, and Nexans, have a significant presence in the market. Their vertical integration, from optical preform pulling to finished cable, delivers cost leverage and fast lead times. Prysmian’s EUR 5 billion Amprion offshore grid contract and Corning’s AI-enabled demand-planning system showcase leadership positions.

Asian challengers such as Hengtong and ZTT compete aggressively on price and fast-cycle innovation, pressuring margins in commodity single-mode fiber. Western buyers in security-sensitive projects nevertheless favor established incumbents with long compliance track records. Patent filings on multicore, rollable-ribbon, and bend-insensitive designs hit record levels in 2025, signaling continuous differentiation.

Strategic moves include factory localization, Belden’s new 300,000-square-foot Tucson fiber hub and automation, with Prysmian rolling out robotic ribbon stackers. Alliances between cable makers and cloud companies deepen; STL’s partnership with Lumos accelerates BEAD-compliant passings in the US mid-Atlantic.

Global Telecom Cable Industry Leaders

Sumitomo Electric Industries, Ltd.

Prysmian Group

Fujikura Ltd.

Furukawa Electric Co.

Leoni AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: C3ntro Telecom unveiled the 2,500 km Tikva route linking the United States and Mexico, boosting cross-border capacity.

- February 2025: Prysmian introduced Sirocco Extreme 864f microduct cable offering 11.5 fibers/mm² density.

- December 2024: Prysmian released EcoSpan FlexRibbon rural broadband cables spanning 300 feet between poles.

- September 2024: CommScope debuted the All-in-One Cabinet and 36-fiber flat cable, winning Diamond Technology honors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study considers telecom cables as purpose-built fiber-optic, coaxial, twisted-pair, and hybrid fiber-coax lines that move voice, data, or video traffic across long-haul, metro, access, and data-center interconnect networks.

Scope Exclusions: Premise-grade patch cords and short internal device jumpers lie outside our scope.

Segmentation Overview

- By Type

- Fiber-optic Cable

- Coaxial Cable

- Twisted Pair Cable

- Hybrid Fiber-Coax (HFC)

- By Application

- Telecommunication Core and Access Networks

- Data Centers and DCI

- CATV and Broadcast

- Enterprise/Campus LAN

- Others (Defense, Oil and Gas, Energy)

- By Installation Environment

- Underground

- Aerial/Overhead

- Subsea

- By End-user Industry

- Telecom Operators

- Hyperscalers and Cloud Providers

- SMEs

- Government and Utilities

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview network planners at tier-1 telcos, procurement heads at cable manufacturers, back-haul contractors, data-center engineers, and regional regulators across Asia-Pacific, North America, Europe, and the Middle East. These discussions confirm deployment run-rates, price dispersion, and upcoming project pipelines, filling gaps that pure desk work leaves open.

Desk Research

We start with widely trusted public sources such as the ITU's telecommunication indicators, TeleGeography's submarine cable maps, the FCC and Ofcom deployment filings, Eurostat trade data, and regional fiber associations, which allow our team to benchmark route-kilometer growth, import volumes, and regulatory triggers. Company 10-Ks, quarterly calls, investor decks, and large carrier build-out announcements yield shipment and average-selling-price clues. When deeper intelligence is needed, our analysts tap D&B Hoovers for supplier financials and Dow Jones Factiva for deal flow and cost trends. The sources listed illustrate our inputs; many additional references were screened to validate and clarify figures.

Market-Sizing & Forecasting

We apply a top-down build that reconstructs demand from active fiber route miles, coax plant density, and new 5G base-station back-haul needs, then cross-check the totals with sampled vendor revenue (ASP × volume) and channel audits. Key variables include 5G cell site additions, hyperscale data-center capex, submarine-cable kilometers laid, copper and silica price indices, and broadband penetration shifts. An ARIMA-based forecast, stress-tested through scenario analysis and expert consensus, projects values from the base year. Gaps in bottom-up inputs are bridged with regional penetration proxies that are subsequently re-validated by primary contacts.

Data Validation & Update Cycle

Model outputs undergo variance checks against external shipment, trade, and capex signals before senior-analyst sign-off. We refresh every twelve months and issue interim revisions whenever material events, major policy funding, or large-scale outages alter demand assumptions. A final sense-check precedes each client delivery, ensuring the freshest view reaches users.

Why Our Telecom Cable Baseline Commands Reliability

Published figures often diverge because firms pick different cable types, installation environments, or price conventions, and they refresh numbers on contrasting cadences.

Key gap drivers include narrower scopes that omit data-center links, aggressive or conservative ASP trajectories, and older currency translations that mask recent copper and fiber cost swings. Our analysts ground definitions early, blend real-time primary checks with transparent variables, and update yearly, which keeps Mordor's baseline balanced and repeatable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 107.8 B (2025) | Mordor Intelligence | - |

| USD 56.05 B (2024) | Regional Consultancy A | Excludes subsea cables and uses historical ASPs, leading to lower value. |

| USD 52.9 B (2024) | Global Consultancy B | Omits hyperscaler demand and models only telco spending. |

| USD 51.98 B (2024) | Trade Journal C | Applies conservative 3% fiber-price decline every year and lacks regional cross-checks. |

In short, by locking scope early, triangulating numbers through both network statistics and supplier signals, and refreshing on a strict cycle, Mordor Intelligence delivers a dependable starting point for strategy and investment decisions.

Key Questions Answered in the Report

What is the current value of the telecom cable market?

The telecom cable market is valued at USD 115.3 billion in 2026 and is forecast to reach USD 161.39 billion by 2031 at a 6.96% CAGR.

Which cable type is growing the fastest?

Fiber-optic cables lead growth with an 8.63% CAGR, holding 56.60% of 2025 revenue.

How much of the market do hyperscalers represent today?

Hyperscalers and cloud providers are the fastest-growing end-user group, expanding at a 7.18% CAGR while still trailing telecom operators’ 58.90% share.

Why are subsea cable deployments accelerating?

Private submarine systems built by hyperscalers support global AI clusters, driving a 7.99% CAGR for subsea installations.

What region dominates global demand?

Asia-Pacific accounts for 47.10% of market revenue in 2025 and is set to grow at 7.75% CAGR through 2031.

What is the key cost challenge in fiber roll-outs?

Underground construction averages USD 18.25 per foot about triple aerial costs, making civil works the largest expense component.

Page last updated on: