Palmitic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

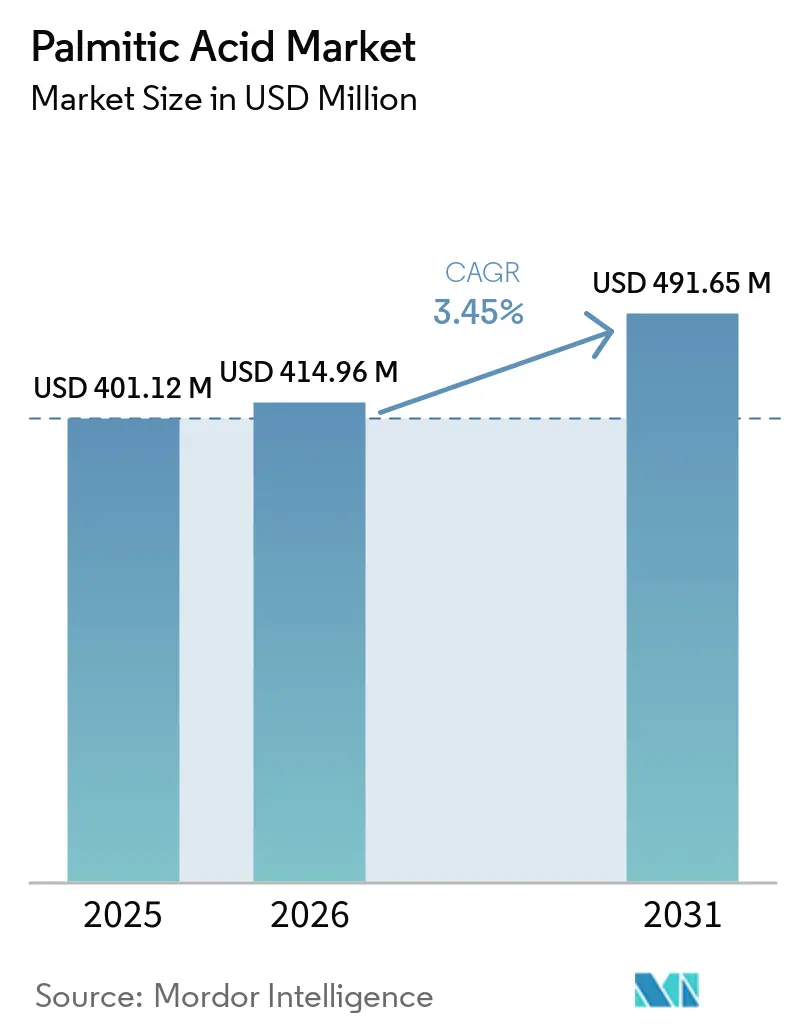

| Market Size (2026) | USD 414.96 Million |

| Market Size (2031) | USD 491.65 Million |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Palmitic Acid Market Analysis by Mordor Intelligence

The Palmitic Acid Market size is expected to grow from USD 401.12 million in 2025 to USD 414.96 million in 2026 and is forecast to reach USD 491.65 million by 2031 at 3.45% CAGR over 2026-2031. Recent price swings triggered by Indonesia’s biodiesel blend escalation, European Union Deforestation Regulation (EUDR) compliance costs, and tightening smallholder feedstock have reshaped procurement strategies across the palmitic acid market. Precision-fermentation offtake agreements signed during 2025 and capacity additions exceeding 600,000 tons per year in Asia-Pacific illustrate how producers are pivoting toward low-carbon routes and regional self-sufficiency. Meanwhile, vertically integrated refiners are capturing EUDR premiums through blockchain-based traceability, leaving mid-tier traders vulnerable to margin compression. Intensifying downstream demand from clean-beauty brands and bio-lubricant blenders continues to reinforce the defensive, moderately growing profile of the palmitic acid market.

Key Report Takeaways

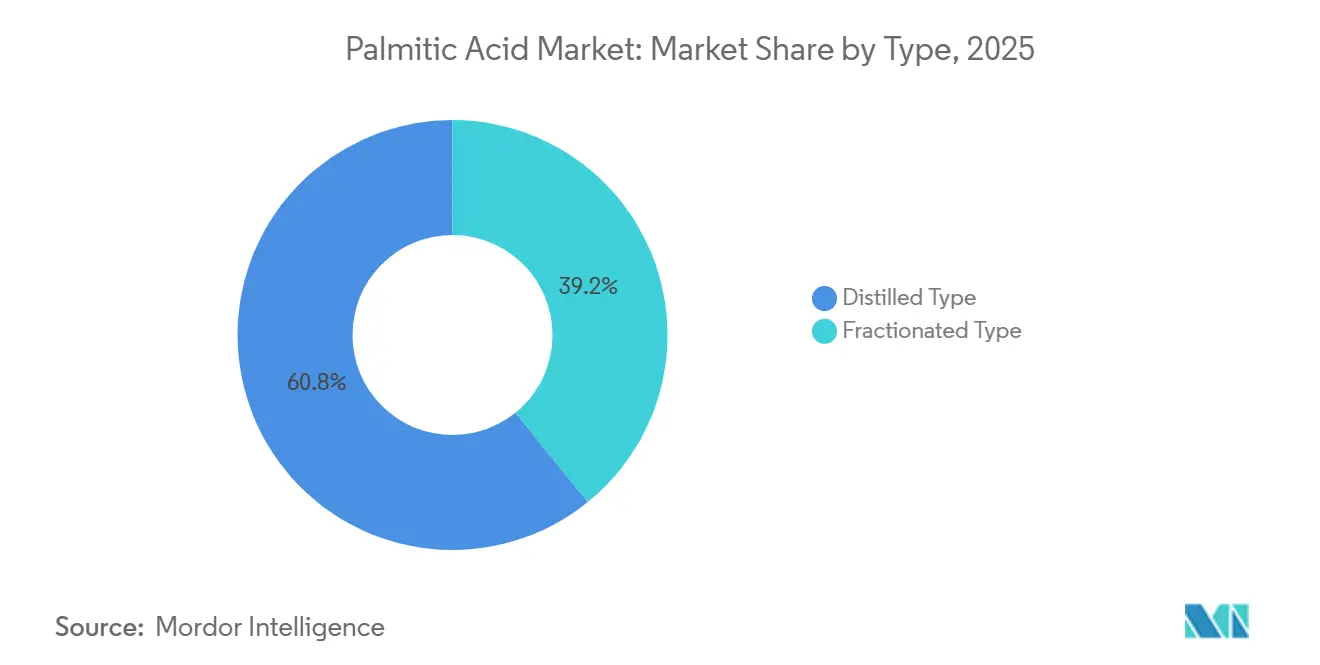

- By type, Distilled grades led with 60.84% of palmitic acid market share in 2025, while Fractionated grades are projected to grow at a 4.21% CAGR through 2031.

- By source, Plant-Based feedstocks commanded 75.62% share of the palmitic acid market size in 2025 and are expanding at a 3.98% CAGR to 2031, driven by RSPO supply-chain certification gains.

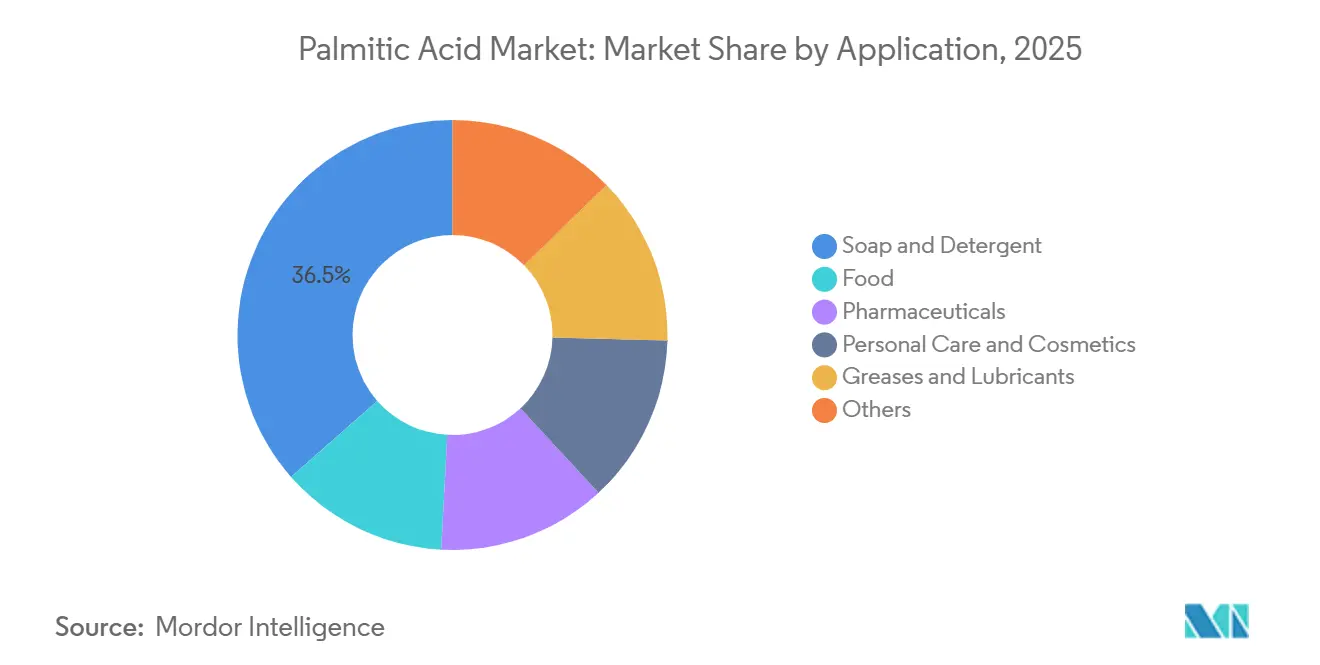

- By application, Soap and Detergent held 36.47% revenue share in 2025; Personal Care and Cosmetics is advancing at a 4.74% CAGR through 2031.

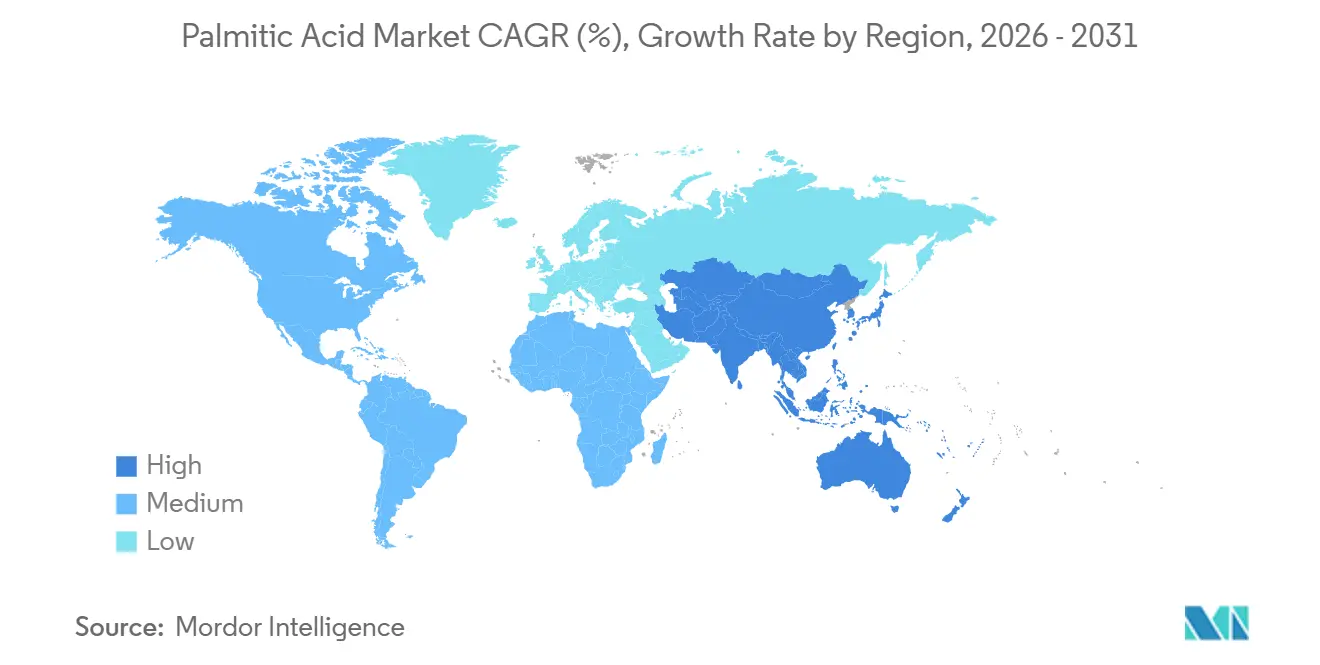

- By geography, Asia-Pacific captured 46.28% share of the palmitic acid market in 2025 and is forecast to post a 4.32% CAGR to 2031 on the back of new Chinese and Malaysian oleochemical projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Palmitic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand in personal care and cosmetics | +0.6% | Global, with concentration in North America and Europe for clean-beauty formulations | Medium term (2-4 years) |

| Rising use in processed food and beverage formulations | +0.4% | Global, particularly Asia-Pacific for bakery and confectionery applications | Medium term (2-4 years) |

| Expansion of oleochemical capacity in Asia-Pacific | +0.8% | Asia-Pacific core, with spillover to Middle East and Africa via export corridors | Short term (≤ 2 years) |

| Surge in bio-lubricants using palmitic esters | +0.5% | North America and Europe for automotive applications; Asia-Pacific for industrial machinery | Long term (≥ 4 years) |

| Precision-fermentation routes lowering carbon footprint | +0.3% | North America and Europe early adoption; Asia-Pacific scale-up post-2028 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand in Personal Care and Cosmetics

Clean-beauty labels increasingly specify cetyl palmitate at 99% purity, integrating it at 10-15% in barrier creams and 5-20% in lip balms to substantiate natural-origin claims[1]Cosmetics Info, “Cetyl Palmitate Safety Profile,” cosmeticsinfo.org. RSPO-certified supply climbed 22% year-on-year to a projected 1.5 million tons in Q4 2025, yet European retailers now reject Mass Balance and Book-and-Claim models and instead require Identity Preserved or Segregated material that can satisfy forthcoming EUDR traceability thresholds. This bifurcation lifts certified palmitic acid premiums by USD 80 per ton and raises EUDR-compliant isopropyl palmitate quotes by USD 10-15 per ton, motivating formulators either to absorb the costs or swap to rapeseed-derived emollients. With moisturizers using 5-10% palmitic acid and cleansers 2-5%, personal-care formulations position the segment as the fastest-growing slice of the palmitic acid market to 2031. The shift underscores how ESG (Environmental, Social, and Governance)-linked buying standards are translating directly into top-line growth for traceable feedstock producers.

Rising Use in Processed Food and Beverage Formulations

Fractionated palm stearin containing 60.6% C16:0 is deployed widely in bakery shortenings and chocolate compounds to replace partially hydrogenated oils banned across multiple jurisdictions[2]Cargill, “Port Klang Specialty Fats Expansion Fact Sheet,” cargill.com. Cargill’s 2026 expansion in Port Klang introduces low-trans offerings formulated with higher palmitic fractions that solidify at ambient temperature without post-hardening. Concurrently, margarine and confectionery manufacturers in China benefit from GB/T 18009-2025 harmonization that streamlines import clearance for palm-derived intermediates, supporting incremental demand within the palmitic acid market. Although sugar-reduction drives may temper confectionery volumes, functional fat systems relying on palmitic acid continue to underpin texture, mouthfeel, and oxidative stability in shelf-stable foods. As a result, processed food demand is expected to deliver a steady, mid-single-digit uplift to global volumes during the forecast period.

Expansion of Oleochemical Capacity in Asia-Pacific

Asia-Pacific’s 46.28% share of the palmitic acid market in 2025 reflects heavy capital deployment by integrated agribusinesses. KLK OLEO commissioned 500,000 tons of new fatty-acid capacity in Zhangjiagang, China, during March 2026 and earmarked CNY 706 million (USD 178.53 million) for specialty esters and fatty alcohols in Malaysia. IOI Oleochemicals followed with a EUR 89.4 million (USD 105.39 million) purchase of Cremer Oleo Germany, adding 39,200 tons a year and diversifying into tallow feedstocks. Cargill and Emery Oleochemicals likewise unveiled expansions and sukuk-financed debottlenecking that collectively push regional supply above 600,000 tons per year. China’s updated palm kernel oil standard, effective March 2026, eliminates quality mismatches that previously hindered imports and thus anchors long-term raw-material availability. These moves keep freight advantages inside the region while exporting surplus volumes to price-sensitive Middle Eastern and African buyers.

Surge in Bio-Lubricants Using Palmitic Esters

Automotive and industrial grease blenders leverage 2-ethylhexyl palmitate to achieve greenhouse-gas reductions of up to 84% compared with mineral-oil basestocks. Lithium-complex greases formulated with palmitic-acid soaps record drop points beyond 260°C and adhere to IS 14847-2000 protocols for extreme-pressure bearings. Emery Oleochemicals’ 2024 portfolio expansion introduced crop-care and oil-field palmitate esters, extending addressable markets into heavy-duty lubricants. Cost premiums of 15-25% and limited OEM (Original Equipment Manufacturer) homologations restrain penetration, although likely carbon-pricing schemes in Europe and the United States could close the delta by 2030. Consequently, bio-lubricants are expected to deliver a long-term pull for the palmitic acid market without overshadowing conventional soap or food-grade demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability and deforestation concerns around palm oil | -0.50% | Global, with acute pressure in Europe and North America from corporate sustainability commitments and consumer activism | Medium term (2-4 years) |

| Volatility in crude palm-oil prices | -0.50% | Global, particularly Asia-Pacific producers and importers in Europe and North America facing feedstock cost pressures | Short term (≤ 2 years) |

| European Union Deforestation Regulation compliance costs | -0.60% | Europe primary impact; spillover to Asia-Pacific exporters (Indonesia, Malaysia) and global supply chains serving EU markets | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

Sustainability and Deforestation Concerns Around Palm Oil

The EUDR, coming into effect on 30 December 2026, obliges operators to supply geolocation polygons for plantations larger than 4 hectares and imposes penalties reaching 4% of European Union (EU) turnover for non-compliance. Palmitic acid under HS 2915 70, therefore, attracts full deforestation-risk scrutiny similar to crude palm oil. Smallholders representing roughly 41% of Indonesian and 27% of Malaysian acreage often lack reliable land-use records, creating procurement gaps that favor integrated majors equipped with satellite verification tools. Military seizures of 3.7 million hectares in Indonesia during late 2025 further depressed yields on affected plots to just 23 tons of fresh-fruit bunches per month, well below typical 80-100 tons benchmarks, increasing supply tightness. With only 20% of global palm oil bearing RSPO status in 2025, exposure to reputational and regulatory risk remains high and tempers the underlying growth of the palmitic acid market.

Volatility in Crude Palm-Oil Prices

Benchmark crude palm-oil prices oscillated between USD 915 per ton in January 2026 (Indonesia) and MYR 4,514 per ton, or roughly USD 1,010, in October 2025 (Malaysia) due to La Niña yield swings and biodiesel blends rising toward B60. Tightening palm-acid-oil supply, down 11-12% year-on-year in 2025, pushed premiums for ISCC-certified volumes to USD 50-100 per ton. Such volatility compresses margins for mid-size oleochemical players without secure estates or multi-year offtake contracts. Integrated refiners with switching optionality between biodiesel, oleochemical, and food markets can arbitrage spreads, yet the broader palmitic acid market faces periodic input-cost shocks that impede long-range planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Purity Thresholds Drive Distilled Dominance

Distilled grades accounted for 60.84% of the palmitic acid market share in 2025, anchored by USP monograph requirements specifying greater than or equal to 92% palmitic content and less than or equal to 6% stearic content for pharmaceutical and personal-care uses. The palmitic acid market size for distilled products is forecast to grow steadily as dermatological and OTC drug formulators insist on trace metal levels measured in parts per million. Vacuum distillation at 200-260°C raises production energy outlays by as much as 20% over fractionation, yet purity premiums routinely offset operational expenditure. In contrast, fractionated grades, derived through controlled crystallization, serve confectionery and bakery fats where a 60.6% C16:0 profile emulates cocoa butter functionality.

Fractionated grades, though smaller, are projected to enjoy a 4.21% CAGR through 2031 as multinational bakers phase out partially hydrogenated oils in favor of palm-stearin substitutes. Cargill’s Port Klang line, commissioned in 2026, exemplifies how blend-optimized palmitic fractions deliver solid-fat indexes that resist post-bloom in chocolate coatings. While price competition restrains fractionated margins, rising food-safety standards across Asia and Africa should underpin volume gains and diversify the downstream exposure of the broader palmitic acid market.

By Source: Certification Premiums Widen Plant-Based Lead

Plant-Based material secured 75.62% share of the palmitic acid market in 2025 on the back of RSPO-certified volumes expanding year-on-year to 1.5 million tons. EUDR enforcement pushes European buyers toward Identity Preserved and Segregated flows, lifting premiums by USD 80 per ton for certified batches and rewarding estates that can deliver GPS-verified data. The palmitic acid market size tied to Plant-Based inputs is therefore poised to grow at a CAGR of 3.98% during the forecast period (2026-2031), despite biodiversity scrutiny.

Animal-Based supply carved out the remaining share, tapping tallow and lard streams in specialty grease and soap noodles. KLK OLEO’s EUR 40.5 million (USD 36 million) buyout of a German tallow facility in March 2026 equips it with feedstock optionality, yet methane-tax proposals and flexitarian consumer preferences limit upside. Over the outlook period, certification economics and deforestation safeguards are expected to entrench Plant-Based dominance across the palmitic acid market.

By Application: Personal Care Outpaces Traditional Soap

Soap and Detergent maintained a 36.47% slice of global revenue in 2025, relying on sodium palmate bases conforming to pH 9.8-10.3 and free fatty acids less than or equal to 0.8%. Demand growth will remain linked to emerging-market hygiene initiatives, but value realization is capped by high price elasticity and private-label competition. Conversely, Personal Care and Cosmetics is projected to log a 4.74% CAGR through 2031, underscoring how RSPO-segregated, high-purity palmitic derivatives anchor clean-beauty positioning. This segment increasingly leverages palmitic-acid esters in moisturizers (5-10% loadings), cleansers (2-5%), and lip-care lines (5-20%) to satisfy vegan and cruelty-free claims, reinforcing premiumization inside the palmitic acid market.

Food-grade uses, particularly chocolate, margarine, and bakery fat systems, benefit from palm-derived solid-fat indices that replicate cocoa butter while avoiding trans-fats. Pharmaceuticals add a niche demand vector via USP-grade palmitic acid (greater than or equal to 92%) for controlled-release excipients, with Drug Master Files registered by SAFC and Avanti Polar Lipids. Grease and lubricant adoption will accelerate in line with OEM approvals for bio-based esters, but still lag household and personal-care volumes in absolute terms.

Geography Analysis

Asia-Pacific accounted for 46.28% of the palmitic acid market in 2025 and is on track for a 4.32% CAGR to 2031 as regional producers widen self-sufficiency and exploit freight savings. KLK OLEO’s Zhangjiagang complex adds 500,000 tons, while IOI’s German purchase injects 39,200 tons of specialty esters into its Asian network. Golden Agri-Resources booked FY 2025 revenue of USD 12.95 billion and rolled out 11 methane-capture units, yet La Niña droughts and military land seizures saw Indonesian fresh-fruit bunch yields on seized plots fall to just 23 tons per month, unsettling certified-supply forecasts. India’s IS 12067:1987 quality order and FSSAI free-fatty-acid caps further influence import blending decisions.

Europe’s share remains smaller but yields superior unit margins thanks to EUDR-driven premiums. IOI Oleochemicals’ EUR 89.4 million (USD 96.5 million) Cremer deal, Musim Mas’ sustainability-linked loan, and retailer requirements for RSPO-IP or SG material sharpen competitive edges for traceable suppliers. Nonetheless, gaps in smallholder mapping risk constrain compliant throughput, potentially inflating price spreads inside the palmitic acid market.

North America focuses on low-carbon innovation, spotlighted by Kao’s precision-fermentation offtake and Checkerspot’s algae platform cutting lifecycle emissions by half. South America and the Middle East and Africa presently capture modest shares but plan oleochemical expansions linked to soybean by-products and petrochemical decarbonization. Collectively, geographical dynamics underscore that regulatory stringency, traceable feedstocks, and on-site value addition will dictate the competitive map of the palmitic acid market through 2031.

Competitive Landscape

The Palmitic Acid market is moderately concentrated. Digital traceability, methane abatement, and AI-guided lipid optimization are the dominant innovation avenues. Players investing in end-to-end satellite and blockchain data management appear best positioned to claim USD 80 per ton certified premiums, whereas mid-tier refiners without estate coverage face exit or acquisition. Accordingly, the palmitic acid market will likely consolidate further as compliance deadlines tighten and novel fermentation volumes scale post-2030.

Palmitic Acid Industry Leaders

Wilmar International Ltd

KLK OLEO

IOI Oleochemical

Musim Mas Group

Emery Oleochemicals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Wilmar International Limited, a supplier of Palmitic Acid, announced that its wholly owned subsidiary, Lence Pte. Ltd., inked a deal with Adani Commodities LLP. This agreement grants Lence the option to acquire up to 31.06% of the paid-up equity share capital of Adani Wilmar Limited.

- July 2024: Kuala Lumpur Kepong Bhd inaugurated a new plant in Zhangjiagang, China, dedicated to high-purity fatty acids (such as Palmitic Acid) and glycerin. This launch increases the facility’s annual processing capacity to 500,000 metric tons.

Global Palmitic Acid Market Report Scope

Palmitic acid is a common 16-carbon saturated fatty acid found in animals, plants, and microorganisms. It is the primary saturated fat in the human diet and metabolism, prevalent in palm oil, dairy, and meat. It is used in manufacturing soaps, cosmetics, and processed foods, and can play a role in metabolic health.

The palmitic acid market is segmented by type, source, application, and geography. By type, the market is segmented into distilled type and fractionated type. By source, the market is segmented into plant-based and animal-based. By application, the market is segmented into soap and detergent, food, pharmaceuticals, personal care and cosmetics, greases and lubricants, and others. The report also covers the market size and forecasts for palmitic acid in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Distilled Type |

| Fractionated Type |

| Plant-Based |

| Animal-Based |

| Soap and Detergent |

| Food |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Greases and Lubricants |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Distilled Type | |

| Fractionated Type | ||

| By Source | Plant-Based | |

| Animal-Based | ||

| By Application | Soap and Detergent | |

| Food | ||

| Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Greases and Lubricants | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global palmitic acid demand be by 2031?

Palmitic Acid is forecast to reach USD 491.65 million by 2031, reflecting a 3.45% CAGR from 2026.

Which region contributes the most production capacity?

Asia-Pacific accounts for 46.28% of current volumes and is expanding fastest due to sizeable Chinese and Malaysian builds.

What is driving premium pricing in Europe?

EUDR plot-level traceability and retailer insistence on RSPO-IP or Segregated supply lift certified-grade premiums by about USD 80 per ton.

Why are distilled grades preferred in pharmaceuticals?

USP monographs demand greater than or equal to 92% palmitic purity and tight heavy-metal limits, standards met only by vacuum-distilled material.

Page last updated on: