Bio-Acetic Acid Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

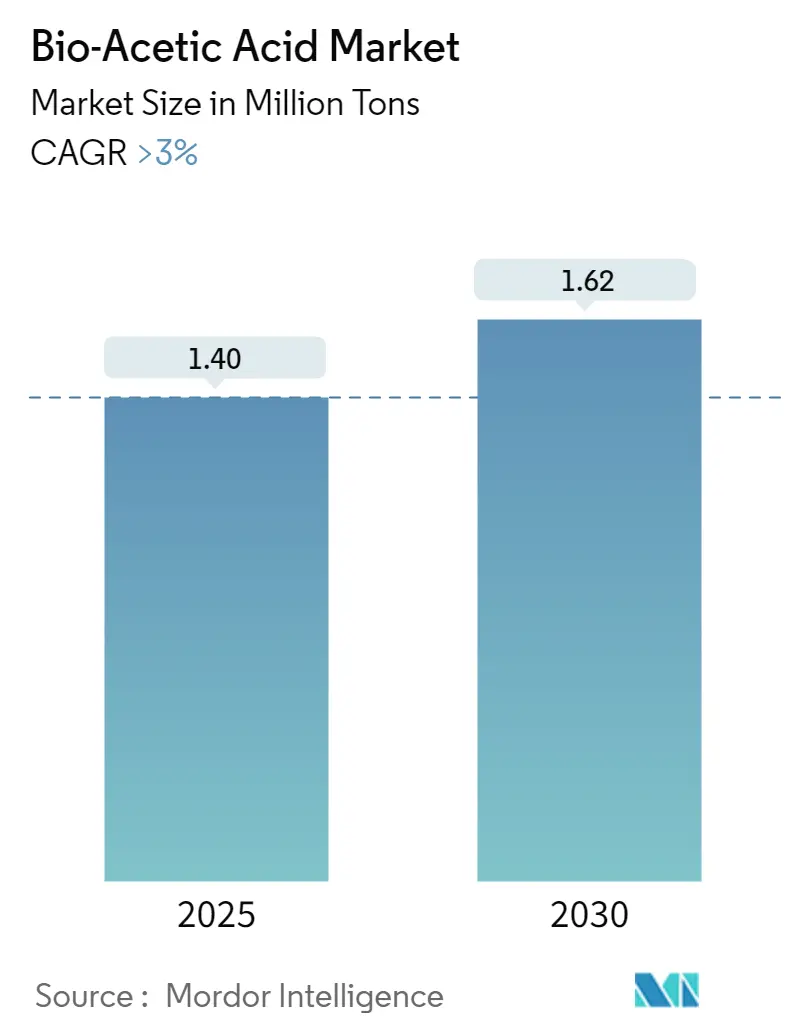

| Market Volume (2025) | 1.40 Million tons |

| Market Volume (2030) | 1.62 Million tons |

| Growth Rate (2025 - 2030) | 3.00% CAGR |

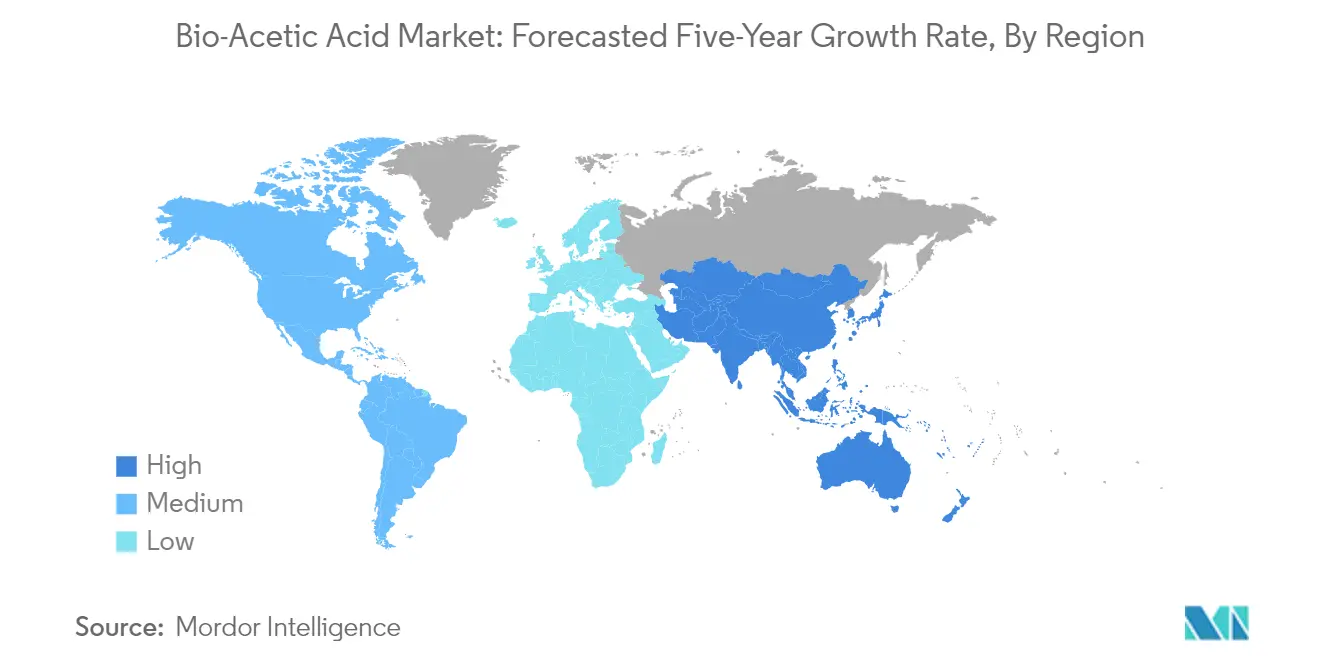

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

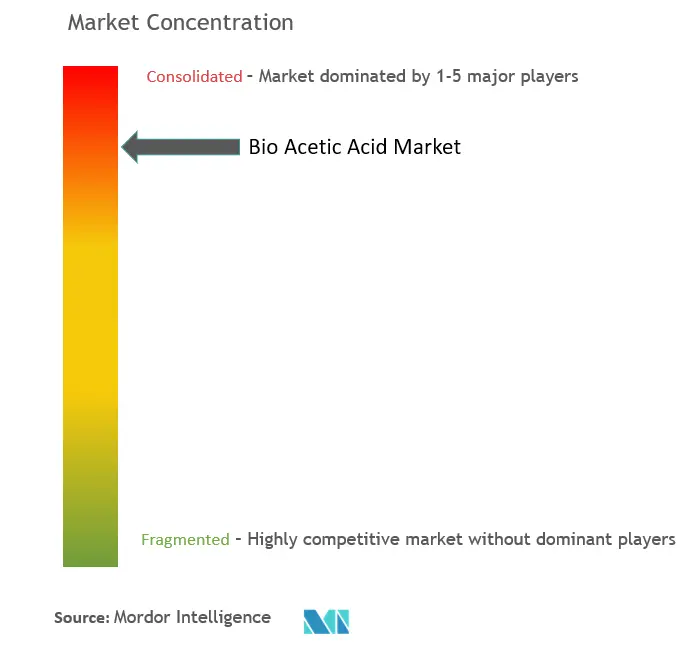

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bio-Acetic Acid Market Analysis by Mordor Intelligence

The Bio-Acetic Acid Market size is estimated at 1.40 million tons in 2025, and is expected to reach 1.62 million tons by 2030, at a CAGR of greater than 3% during the forecast period (2025-2030).

The European bio acetic acid industry is experiencing a significant transformation driven by the broader shift towards the sustainable chemical industry. Major chemical manufacturers are increasingly adopting mass-balance approaches to replace fossil raw materials with renewables, while implementing life cycle assessment (LCA) methodologies to evaluate and improve their environmental impact. This transition is particularly evident in the food and beverage sector, which remains a cornerstone of European manufacturing, employing 4.6 million individuals and generating a remarkable turnover of EUR 1.1 trillion as of December 2023. The industry's commitment to sustainability has catalyzed investments in biobased chemical production facilities and green chemistry initiatives.

The market is witnessing a surge in strategic partnerships and technological collaborations aimed at scaling up bio acetic acid market production. In August 2023, a significant development occurred when C.P.L. Prodotti Chimici SRL became the first licensing partner of LENZING Acetic Acid, marking a crucial step in expanding the bio-based acetic acid distribution network. Companies are increasingly focusing on developing innovative production techniques, with several manufacturers investing in advanced biorefinery technologies that can convert various renewable feedstocks into high-quality bio-acetic acid.

The textile and apparel industry has emerged as a significant growth driver for bio-acetic acid applications, with the European sector comprising 192,000 companies and employing 1.3 million workers, generating a turnover of EUR 167 billion. The industry's push towards sustainable practices has led to increased adoption of biobased chemical in textile processing and finishing applications. Manufacturers are developing specialized bio-acetic acid formulations that meet the specific requirements of textile processing while maintaining environmental sustainability standards.

The market is characterized by increasing integration across the value chain, with producers expanding their capabilities from raw material sourcing to end-product manufacturing. The European food processing sector, particularly in France, which encompasses approximately 15,500 companies generating over USD 215 billion in annual sales, has been at the forefront of adopting bio-based ingredients. This integration has been supported by significant investments in research and development, with the European cosmetics industry alone dedicating EUR 2.35 billion to R&D initiatives, focusing on developing sustainable and bio-based alternatives for various applications. This aligns with the broader goals of the circular economy chemical industry, emphasizing a closed-loop system for resource efficiency.

Global Bio-Acetic Acid Market Trends and Insights

Rising Demand for Bio-Acetic Acid from the Food Industry

The European food and beverage sector has emerged as a significant driver for bio-acetic acid demand, with the industry employing 4.6 million individuals and generating a remarkable turnover of EUR 1.1 trillion as of December 2023. The sector's robust export performance, exceeding EUR 182 billion and resulting in a trade surplus of approximately EUR 73 billion, demonstrates the strong market potential for bio-based ingredients like natural acetic acid. This growth is further supported by the increasing consumer preference for natural and environmentally friendly food additives, with fermentation acetic acid serving multiple functions including preservation, flavor enhancement, and pH regulation in various food products.

The industry's commitment to sustainable practices is evidenced by significant investments in research and development, exemplified by Kerry's establishment of an innovation hub in 2023 at the renowned "Food Valley" at Wageningen University in the Netherlands. This facility focuses on developing cutting-edge food preservation solutions and clean-label ingredient alternatives, directly supporting the adoption of green acetic acid in food applications. Bio-acetic acid's versatility in food applications spans across vinegar production, pickled vegetables, sauces, and various condiments, while its natural origin and absence of heavy metals and carcinogenic elements make it particularly attractive for manufacturers focused on clean-label products.

Other Drivers

The chemical industry's increasing focus on environmental sustainability serves as a crucial driver for bio-acetic acid adoption, particularly given that the sector ranks as the third-largest industrial emitter of CO2, releasing over 2.5 gigatons of greenhouse gas annually. Fermentation acetic acid offers significant environmental advantages, with studies showing up to an 85% reduction in carbon footprint compared to fossil fuel-based alternatives, while food-grade applications demonstrate an even more impressive 110% lower carbon footprint. This environmental benefit has catalyzed partnerships and innovations across the industry, with companies like Evonik leveraging natural acetic acid in the production of peracetic acid, significantly reducing their environmental impact.

The industry's transformation is further evidenced by major chemical companies' strategic shifts toward sustainable production methods. Wacker Chemie has pioneered the use of sustainable chemicals such as bio-based acetic acid and ethylene in vinyl acetate monomer production, while Celanese has expanded its ECO-B variants across various acetyl chain intermediate chemicals. These initiatives are complemented by certification programs and sustainability frameworks, such as the PEFC certification for wood-sourced bio-acetic acid and ISCC+ mass balance certification for sustainable solutions. The growing emphasis on plant-derived chemicals and materials as climate change mitigation tools has positioned bio-acetic acid as a key component in the industry's transition toward renewable resources and reduced environmental impact.

Segment Analysis: Raw Material

Corn Starch and Maize Segment in Bio-Acetic Acid Market

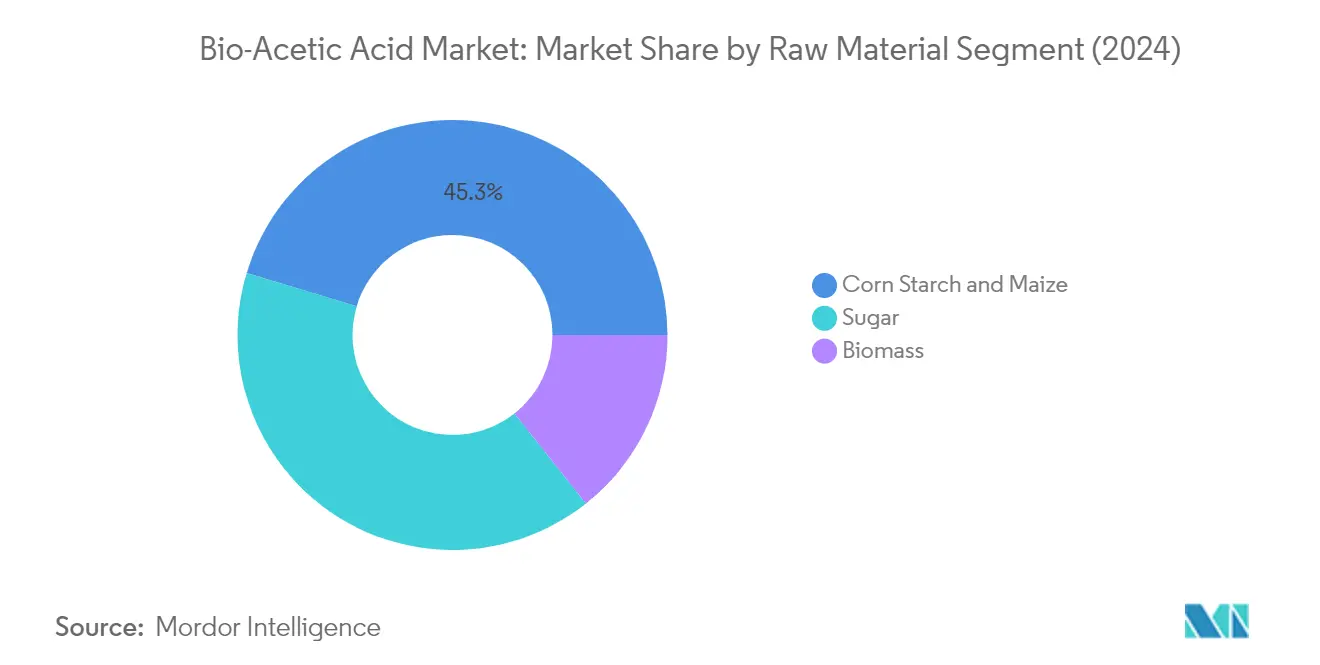

Corn starch and maize maintain their dominance in the European bio-acetic acid market, commanding approximately 45% of the total market share in 2024. The segment's leadership position is primarily attributed to the widespread availability and abundant production of corn in Europe, making it a reliable and cost-effective raw material source for bio-acetic acid production. The large-scale availability of these raw materials in Europe effectively supports the production of bio-based acetic acid, with major manufacturers like Jubilant Ingrevia Limited utilizing corn starch for their production processes. The segment's strength is further reinforced by the well-established infrastructure for corn processing and the optimization of conversion processes from corn starch to natural acetic acid. Companies employing corn starch and maize as feedstock benefit from the material's high conversion efficiency and consistent quality, which are crucial factors in maintaining stable production outputs.

Biomass Segment in Bio-Acetic Acid Market

The biomass segment is emerging as the fastest-growing raw material category in the European bio-acetic acid market, projected to expand at approximately 4% CAGR from 2024 to 2029. This growth is driven by increasing emphasis on sustainable production methods and the segment's ability to utilize diverse feedstock sources, including wood industry byproducts and agricultural residues. Companies like LENZING AG are leading the innovation in this space, utilizing sustainably sourced beech wood pulp through their biorefinery technology. The segment's growth is further supported by its superior environmental credentials, with biomass-derived natural acetic acid demonstrating significantly lower carbon footprints compared to conventional production methods. The increasing adoption of closed-loop production systems and the development of more efficient conversion technologies are expected to further accelerate the segment's growth trajectory in the coming years.

Remaining Segments in Raw Material

The sugar-based raw material segment continues to play a vital role in the European bio-acetic acid market, offering unique advantages in terms of process efficiency and product quality. This segment leverages fermentation acetic acid processes to convert sugar-based feedstocks into bio-acetic acid, with companies like Godavari Biorefineries Ltd and Jubilant Ingrevia Limited leading the way in sugar-based production methods. The segment benefits from the well-established sugar industry infrastructure in Europe and the high purity levels achievable through sugar-based fermentation acetic acid processes. Additionally, the sugar-based production route offers advantages in terms of process control and consistency, making it particularly suitable for applications requiring high-purity bio-acetic acid, such as food and pharmaceutical applications.

Segment Analysis: Application

Vinyl Acetate Monomer (VAM) Segment in Europe Bio-Acetic Acid Market

The Vinyl Acetate Monomer (VAM) segment dominates the Europe bio-acetic acid market, commanding approximately 35% of the total market share in 2024. VAM's prominence stems from its crucial role in producing homopolymers and copolymers essential for diverse industrial applications. The segment's strength is particularly evident in its extensive use in manufacturing water-based paints, adhesives, waterproofing coatings, and paper and paperboard coatings. Through homopolymerization, VAM transforms into polyvinyl acetate (PVA), accounting for about 40% of total consumption, offering exceptional properties like high initial tack and biodegradation resistance. When copolymerized with ethylene, VAM serves as a key component in producing ethylene vinyl acetate (EVA), which excels in crack and puncture resistance for sealants, coatings, and adhesive formulations. The segment's dominance is further reinforced by VAM's versatility in hot melt adhesives, where it demonstrates superior bonding capabilities across diverse substrates while maintaining stability over a wide temperature spectrum.

Acetate Esters Segment in Europe Bio-Acetic Acid Market

The Acetate Esters segment is projected to exhibit the highest growth rate in the Europe bio-acetic acid market from 2024 to 2029, with an expected CAGR of approximately 4%. This robust growth is driven by the segment's diverse applications across multiple industries. Acetate esters, derived from bio-based acetic acid through esterification reactions with various alcohols, are gaining prominence due to their desirable properties such as pleasant fragrance, low toxicity, and excellent solvent characteristics. The segment's growth is particularly notable in the adhesives, paints and coatings, and printing inks industries. Additionally, these esters play a crucial role as flavoring agents in food products, imparting sweet and fruity aromas, and are extensively utilized in perfume manufacturing. Their significance extends to pharmaceutical applications, where they are essential in extracting and purifying compounds and medicine formulations. The segment's expansion is further supported by its applications in industrial and household cleaning products, textiles, and various other sectors.

Remaining Segments in Europe Bio-Acetic Acid Market

The remaining segments in the Europe bio-acetic acid market include Purified Terephthalic Acid (PTA), Food and Beverage Additives, and Other Applications. The PTA segment plays a vital role in the chemical and polymer industry, particularly in the creation of polyester coatings for various industrial applications. The Food and Beverage Additives segment is crucial for natural preservation and flavor enhancement, offering a sustainable chemical alternative to conventional preservatives. The Other Applications segment encompasses diverse uses including acetic anhydride production, textile processing and printing, pharmaceuticals, and personal care products. Each of these segments contributes uniquely to the market's diversity, with PTA supporting the polymer industry's growth, food additives meeting the increasing demand for natural preservatives, and other applications driving innovation across multiple industrial sectors.

Bio-Acetic Acid Market Geography Segment Analysis

Bio-Acetic Acid Market in Germany

Germany dominates Europe's bio acetic acid landscape, commanding approximately 25% of the market share in 2024, while demonstrating robust growth potential with a projected CAGR of about 4% from 2024 to 2029. The country's leadership position is reinforced by its strong chemical manufacturing infrastructure, particularly in vinyl acetate monomer (VAM) production, with facilities like Wacker Chemie AG's Burghausen site producing over 150,000 tons annually. The German government's stringent regulations on conventional acetic acid, classified under the Hazardous Substances Ordinance, have accelerated the shift toward bio-based chemical alternatives. This regulatory framework, coupled with the country's commitment to sustainable development, has created a favorable environment for bio acetic acid adoption. The presence of major players like Wacker Chemie AG, which utilizes bio acetic acid in its innovative dispersible polymer powder production, further strengthens Germany's market position. The country's emphasis on green chemistry and sustainable manufacturing practices continues to drive innovation in bio acetic acid applications across various industries.

Bio-Acetic Acid Market in Belgium

Belgium has established itself as a crucial hub for bio acetic acid market production and consumption in Europe, supported by its robust chemical manufacturing infrastructure and strategic location. The country's food processing industry, employing 91,000 people and generating substantial turnover, represents a significant end-user segment for bio acetic acid. Belgium's prominence in the market is particularly notable in the production of purified terephthalic acid (PTA), with facilities like INEOS Aromatics producing around 750,000 tons annually in Geel. The country's well-developed distribution networks and logistics infrastructure facilitate efficient supply chain management for bio acetic acid producers and consumers alike. The presence of major players like Jubilant Ingrevia Limited and various VAM manufacturers, including Solventis and INEOS, has created a dynamic market environment. Belgium's commitment to sustainable chemical production and its strong industrial base continue to drive the adoption of bio-based alternatives across various applications.

Bio-Acetic Acid Market in United Kingdom

The United Kingdom's bio acetic acid market is characterized by its strong regulatory framework and growing emphasis on sustainable chemical production. The country's market is governed by the Control of Substances Hazardous to Health (COSHH) Regulations 2002, which has created a favorable environment for bio-based alternatives. The UK's diverse industrial base, including manufacturers of VAM, acetate esters, and purified terephthalic acid, provides multiple avenues for bio acetic acid applications. Companies like Seqens Custom Specialties Trading AS, INEOS, Solventis, and Ravago Chemicals form a robust network of potential consumers. The presence of established suppliers such as Lenzing AG, Godavari Biorefineries Ltd, and Wacker Chemie AG ensures steady market development. The UK's commitment to reducing environmental impact and promoting sustainable chemistry continues to drive innovation and adoption of bio-based alternatives across various industrial sectors.

Bio-Acetic Acid Market in Other Countries

The bio acetic acid market extends across various other European countries, each contributing uniquely to the regional landscape. France's market is characterized by its strong food and beverage industry, with companies like Afyren SAS leading innovation in bio-based solutions. Italy's position is strengthened by its significant food processing sector and growing emphasis on sustainable manufacturing practices. Spain's market demonstrates potential through its industrial base and commitment to environmental sustainability. The Nordic countries, particularly Sweden, contribute through innovative companies like Sekab, while Eastern European nations provide emerging opportunities for market expansion. Countries like the Netherlands, Poland, and Portugal also play important roles through their chemical manufacturing capabilities and growing adoption of sustainable practices. This diverse geographic spread ensures continued market development and innovation in fermentation acetic acid production and applications across Europe.

Competitive Landscape

Top Companies in Bio-Acetic Acid Market

The European bio-acetic acid market is characterized by companies focusing intensively on sustainable production methods and bio-based feedstock innovations. Market leaders are investing substantially in research and development to enhance production efficiency and reduce carbon footprints, with several players introducing certified bio-based products with significantly lower environmental impacts. Companies are strategically expanding their manufacturing capacities and distribution networks across Europe to meet growing demand, particularly evident through new facility launches and capacity expansions. Strategic partnerships and licensing agreements have become increasingly common, enabling companies to strengthen their market positions and expand their geographical reach. The industry has witnessed a notable shift towards developing proprietary technologies and processes for converting various bio-based chemical feedstocks into acetic acid, demonstrating the sector's commitment to technological advancement and sustainability.

Consolidated Market with Strong Regional Players

The European bio-acetic acid market exhibits a consolidated structure dominated by established manufacturers with a strong regional presence and specialized biochemical expertise. The market features a mix of global chemical conglomerates and specialized bio-based chemical producers, with companies like SEKAB, LENZING AG, and Jubilant Ingrevia Limited holding significant market positions through their dedicated bio-acetic acid production facilities and extensive distribution networks. The competitive landscape is characterized by high entry barriers due to substantial technological requirements, capital investments, and the need for established distribution channels, which naturally limits new entrant potential.

The market demonstrates a trend toward vertical integration, with several key players maintaining control over their raw material supply chains and downstream applications. Companies are increasingly focusing on developing direct relationships with end-users and establishing long-term supply agreements to ensure market stability. The industry has witnessed strategic collaborations between established players and regional distributors to enhance market penetration and service capability, rather than traditional merger and acquisition activities, indicating a preference for organic growth and partnership-based expansion strategies.

Innovation and Sustainability Drive Future Success

Success in the bio-acetic acid market increasingly depends on companies' ability to develop cost-effective and environmentally sustainable production processes while maintaining product quality and consistency. Market incumbents are strengthening their positions by investing in advanced biorefinery technologies, expanding their raw material base to include various sustainable feedstocks, and developing proprietary production processes. Companies are also focusing on obtaining sustainability certifications and developing closer relationships with end-users in key application segments like food and beverages, vinyl acetate monomer production, and other industrial applications.

The competitive landscape is evolving with increasing emphasis on regulatory compliance and environmental standards, particularly regarding carbon emissions and sustainable sourcing practices. Companies seeking to gain market share must address the growing end-user preference for certified bio-based products while managing production costs and maintaining supply chain reliability. The industry's future success factors include the ability to secure stable bio-based raw material supplies, develop efficient production processes, and build strong relationships with key end-users while maintaining flexibility to adapt to changing market demands and regulatory requirements. The risk of substitution from conventional acetic acid remains a significant factor, making price competitiveness and a clear value proposition crucial for market success. The sustainable chemical industry is poised to benefit from these advancements, aligning with the goals of the circular economy chemical industry.

Bio-Acetic Acid Industry Leaders

Godavari Biorefineries Ltd.

LENZING AG

Airedale Group

Novozymes A/S (Novonesis Group)

Sekab

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2023: Sekab launched expanded production of bio-based acetic acid. Sekab’s bio-based acetic acid can reduce the carbon footprint by up to 50%. Sekab’s investment in new production capacity is now up and running, enabling faster and larger deliveries.

Global Bio-Acetic Acid Market Report Scope

Bio-acetic acid is used to process substrates in many manufacturing processes. It is also used as a chemical reagent for producing various chemical compounds such as acetic anhydride, ester, monomer vinyl acetate, vinegar, and many other polymer products.

The bio-acetic acid market is segmented by raw material, application, and geography. By raw material, the market is segmented into biomass, corn, maize, sugar, and other raw materials. By application, the market is segmented into vinyl acetate monomer, acetate esters, purified terephthalic acid, acetic anhydride, and other applications. The report also covers the market size and forecasts for the bio-acetic acid market in 27 countries across major regions. For each segment, the market sizing and forecasts are done based on volume (tons).

| Biomass |

| Corn |

| Maize |

| Sugar |

| Other Raw Materials |

| Vinyl Acetate Monomer (VAM) |

| Acetate Esters |

| Purified Terephthalic Acid (PTA) |

| Acetic Anhydride |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Qatar |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa | |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| Raw Material | Biomass | |

| Corn | ||

| Maize | ||

| Sugar | ||

| Other Raw Materials | ||

| Application | Vinyl Acetate Monomer (VAM) | |

| Acetate Esters | ||

| Purified Terephthalic Acid (PTA) | ||

| Acetic Anhydride | ||

| Other Applications | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Qatar | |

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Bio-Acetic Acid Market?

The Bio-Acetic Acid Market size is expected to reach 1.40 million tons in 2025 and grow at a CAGR of greater than 3% to reach 1.62 million tons by 2030.

What is the current Bio-Acetic Acid Market size?

In 2025, the Bio-Acetic Acid Market size is expected to reach 1.40 million tons.

Who are the key players in Bio-Acetic Acid Market?

Godavari Biorefineries Ltd., LENZING AG, Airedale Group, Novozymes A/S (Novonesis Group) and Sekab are the major companies operating in the Bio-Acetic Acid Market.

Which is the fastest growing region in Bio-Acetic Acid Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Bio-Acetic Acid Market?

In 2025, the Europe accounts for the largest market share in Bio-Acetic Acid Market.

What years does this Bio-Acetic Acid Market cover, and what was the market size in 2024?

In 2024, the Bio-Acetic Acid Market size was estimated at 1.36 million tons. The report covers the Bio-Acetic Acid Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Bio-Acetic Acid Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: