Fumaric Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

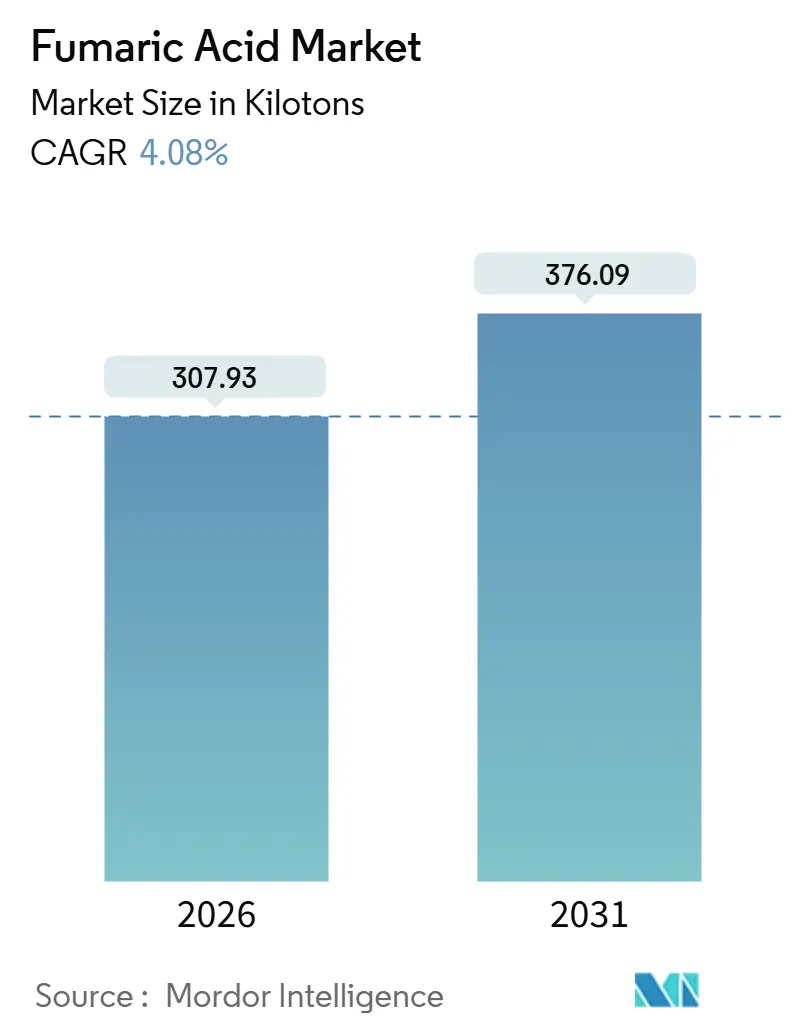

| Market Volume (2026) | 307.93 kilotons |

| Market Volume (2031) | 376.09 kilotons |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

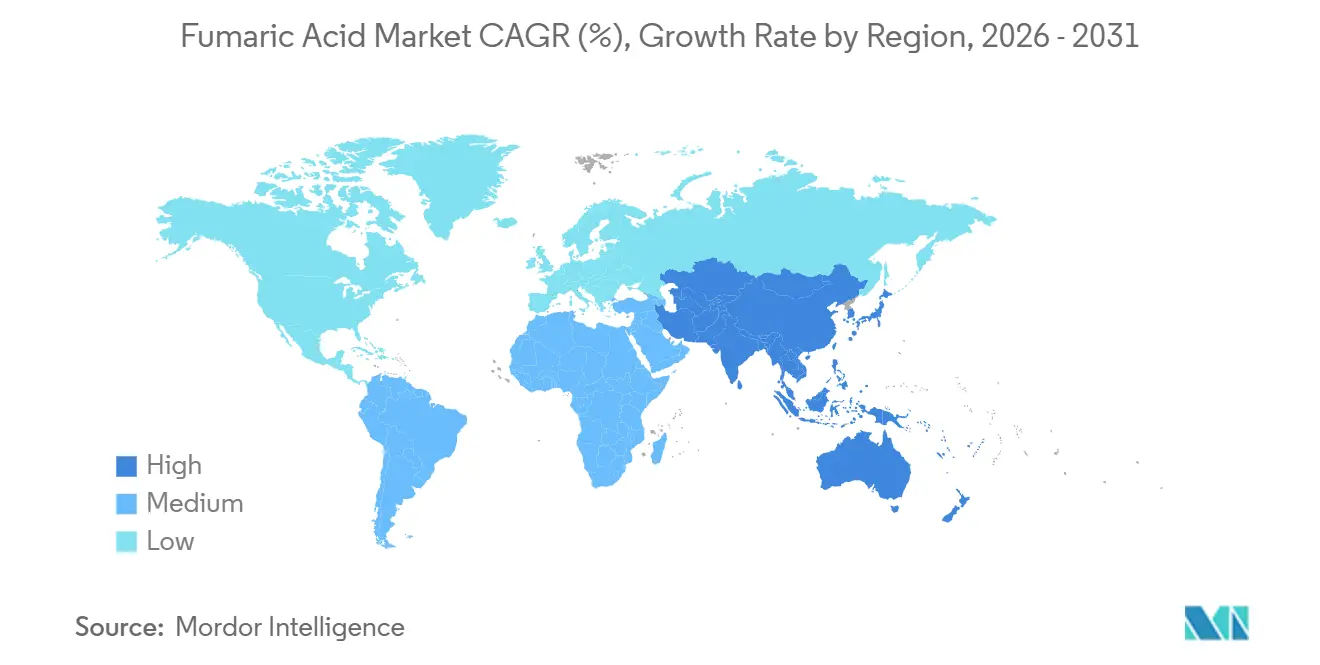

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

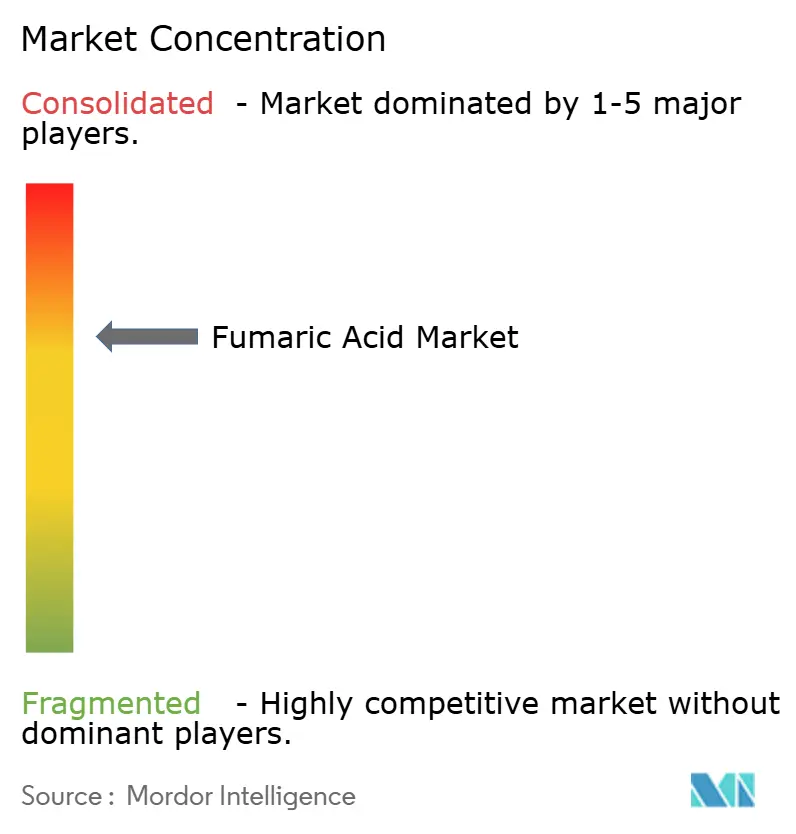

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fumaric Acid Market Analysis by Mordor Intelligence

The Fumaric Acid Market size is estimated at 307.93 kilotons in 2026, and is expected to reach 376.09 kilotons by 2031, at a CAGR of 4.08% during the forecast period (2026-2031). Strong clean-label adoption in packaged foods, escalating EU and U.S. pressure to curb antibiotic use in livestock, and rapid scale-up of carbon-negative fermentation routes are steering demand toward bio-based supply. At the same time, maleic-anhydride feedstock volatility and the European Union’s Carbon Border Adjustment Mechanism (CBAM) are squeezing petro-route margins, encouraging backward integration and new regional capacity. Automotive lightweighting and wind-energy investments are underpinning unsaturated polyester resin (UPR) demand, while semiconductor fabs are creating a lucrative niche for ultra-high-purity polymers. Competitive intensity is moderate; the top five producers account for roughly 69% of global capacity, yet more than 20 sub-scale Chinese firms still vie for share in Asia-Pacific.

Key Report Takeaways

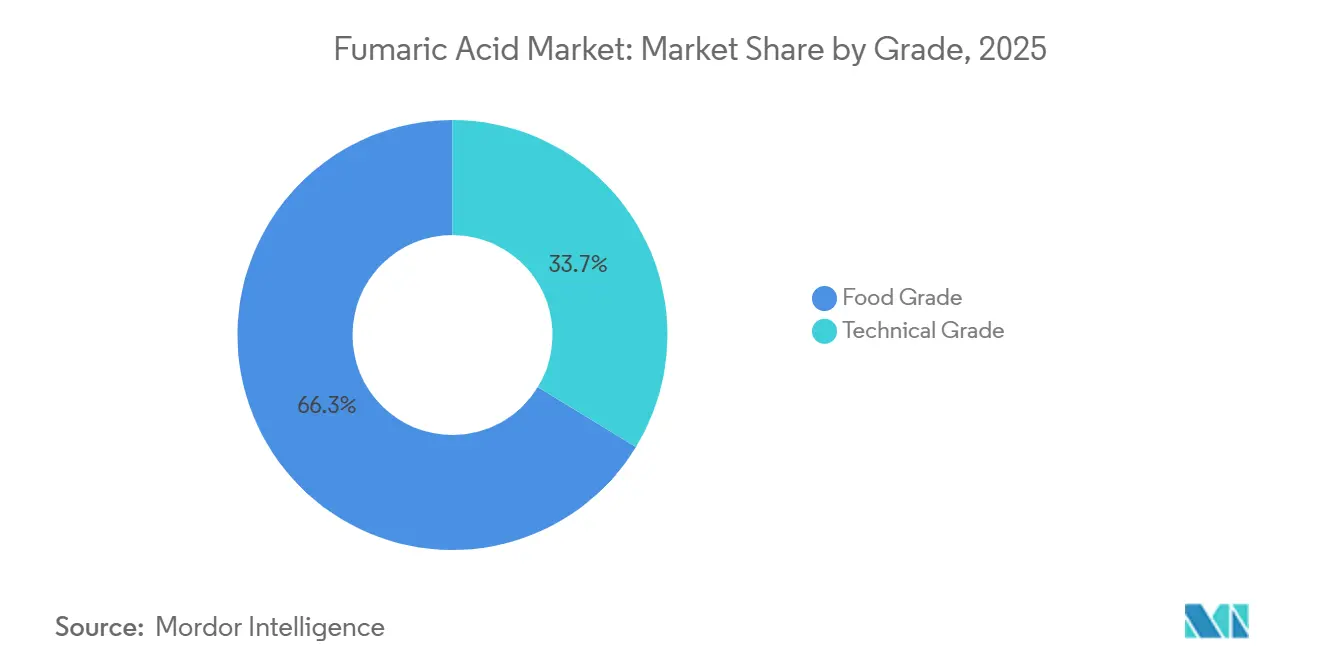

- By grade, food-grade held 66.28% of Fumaric Acid market share in 2025; and is projected to expand at a 4.51% CAGR to 2031.

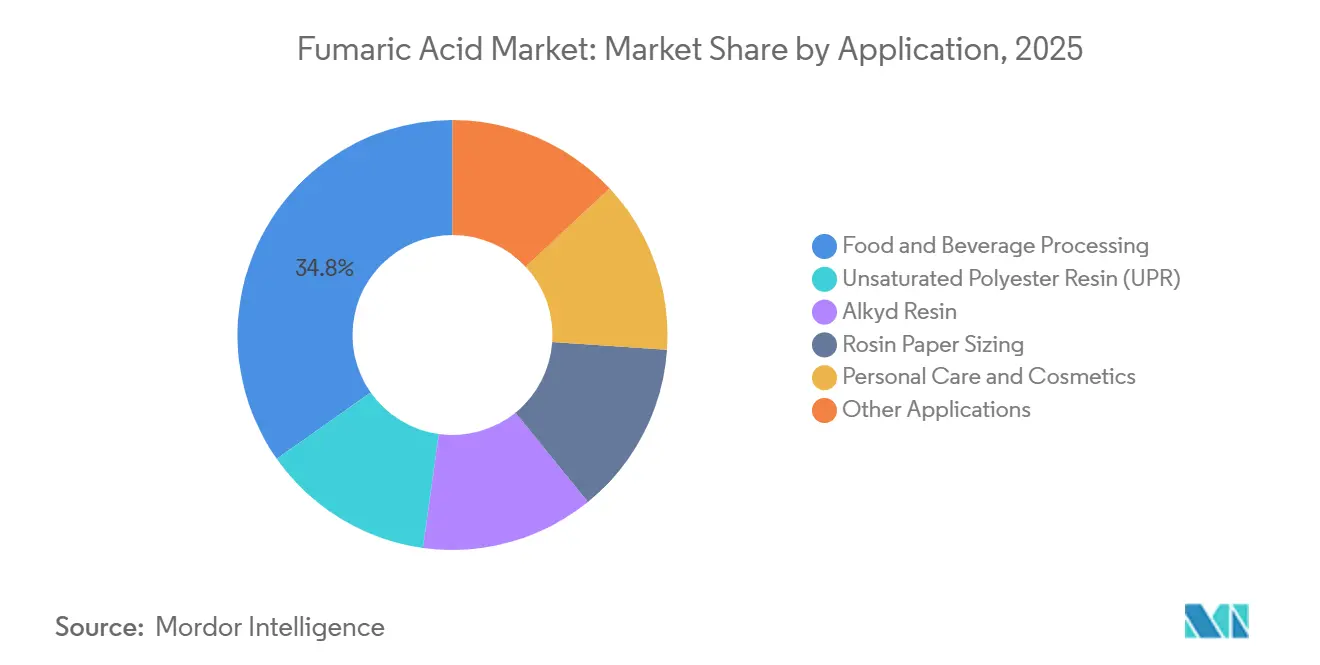

- By application, food and beverage processing led with 34.76% of Fumaric Acid market share in 2025 and is set to rise at a 4.74% CAGR through 2031.

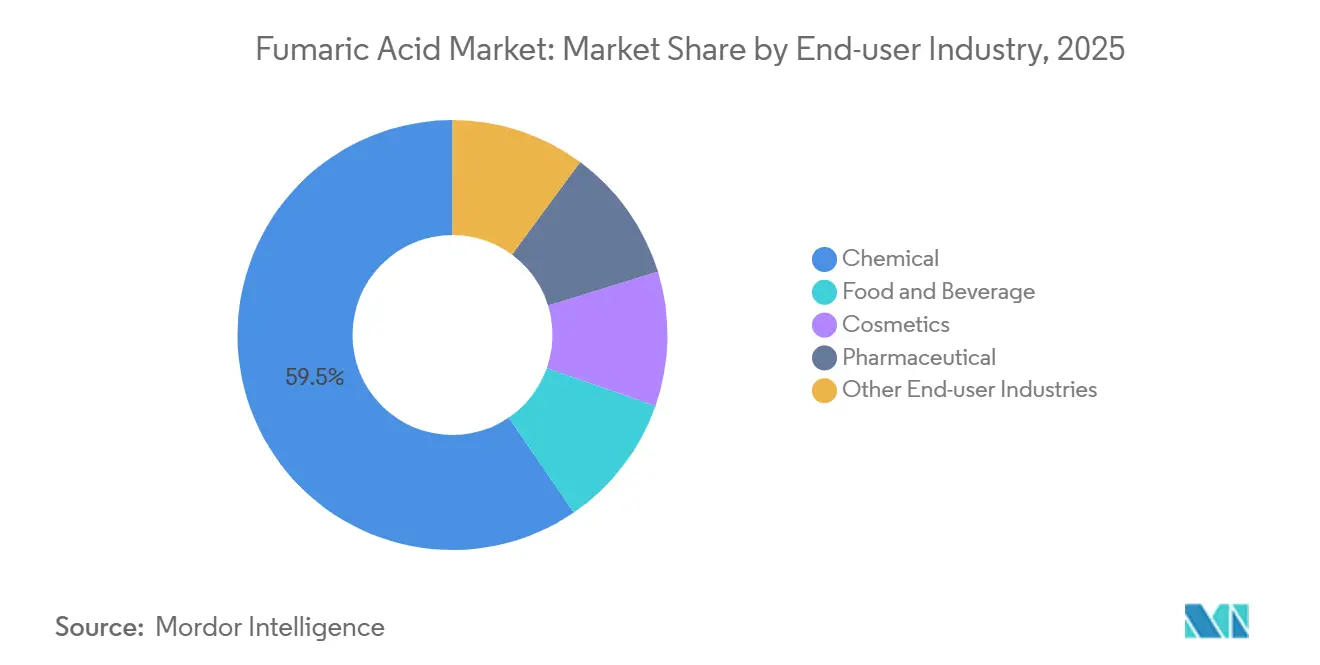

- By end-user industry, the chemical segment commanded 59.54% of Fumaric Acid market size in 2025; pharmaceuticals represent the fastest-growing end-user industry at a 4.96% CAGR through 2031.

- By geography, Asia-Pacific captured 60.21% of global Fumaric Acid market share in 2025; and is forecast to post the highest regional CAGR at 4.88% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fumaric Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label demand for bio-fermented fumaric acid in Asian convenience foods | +0.9% | Asia-Pacific (China, Japan, South Korea, ASEAN), spill-over to North America | Medium term (2-4 years) |

| Shift to unsaturated polyester resins for lightweight EV and wind-blade composites | +0.7% | Global, with concentration in China, Europe, North America | Long term (≥ 4 years) |

| Europe and North America antibiotic-free feed laws boosting demand for fumaric acid as an acidulant | +0.6% | Europe, North America | Short term (≤ 2 years) |

| Growth of specialty water-treatment polymers in semiconductor fabs | +0.3% | Asia-Pacific (Taiwan, South Korea, Japan), North America | Medium term (2-4 years) |

| Cradle-to-gate carbon-negative fermentation technologies attracting green finance | +0.5% | Europe, North America, emerging in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clean-Label Demand for Bio-Fermented Fumaric Acid in Asian Convenience Foods

Spiking consumer scrutiny over ingredient declarations is reshaping acidulant sourcing in Japan, South Korea, and China. Japan’s April 2024 Food Sanitation Act amendments require explicit labeling of synthetic additives, spurring a reformulation wave among convenience-store chains. South Korea’s November 2024 guidance encourages producers to disclose production routes, further nudging demand toward fermentation-derived material. Chinese firms such as Yantai Hengyuan and Changmao Biochemical added an estimated 15,000 tons of bio-capacity across 2024-2025, narrowing the historical 25% price premium for food-grade bio-material to roughly 12% by 2025. Rising middle-class incomes in ASEAN are expected to mirror this trend, expanding regional uptake.

Shift to Unsaturated Polyester Resins for Lightweight EV and Wind-Blade Composites

Electric-vehicle platforms now incorporate about 450 pounds of plastics and composites compared with 310 pounds in ICE vehicles, a delta largely driven by weight-offsetting battery mass. European automakers seeking to meet 2025 fleet-wide CO₂ targets are specifying glass-fiber UPR parts that contain 8%-12% fumaric-based co-monomers. Offshore wind projects similarly favor fumaric-modified UPR for blades over 80 meters long, where enhanced fatigue resistance is critical. Counterbalancing forces include premium-segment moves to carbon-fiber prepregs and bio-epoxy systems, but the overall pull from mass-market EVs supports continued volume growth.

Europe and North America Antibiotic-Free Feed Laws Boosting Fumaric-Acid Acidulants

The European Food Safety Authority’s October 2024 opinion validated fumaric acid at inclusion rates up to 2% for all livestock species[1]European Food Safety Authority, “Scientific Opinion on the Safety and Efficacy of Fumaric Acid as Feed Additive,” efsa.europa.eu . Parallel U.S. initiatives in California and Oregon set stricter antibiotic reduction targets, encouraging integrators to switch to organic acids. Fumaric acid’s hydrophobic profile prolongs gut acidification, enabling lower inclusion rates than formic or propionic alternatives and giving it an 8%-10% share of a USD 2.5 billion feed-acidulant pool in 2025. Producers such as Bartek Ingredients and Thirumalai Chemicals expanded feed-grade lines in 2024 to capture rising demand.

Growth of Specialty Water-Treatment Polymers in Semiconductor Fabs

Migration to sub-3-nanometer process nodes is tightening particle and metal-ion thresholds in fab water systems. Fumaric-based polyacrylic copolymers provide superior chelation for calcium and magnesium, critical for ultrapure-water loops. Each advanced fab commissioned by Taiwan Semiconductor Manufacturing Company or Samsung Electronics requires roughly 10-15 tons of these polymers annually. Japan’s 2024 Economic Security Promotion Act further incentivizes domestic production of critical materials, providing a high-margin outlet for pharmaceutical-grade or higher purity fumaric feedstock.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in maleic-anhydride feedstock and benzene spot prices | -0.8% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| EU CO₂-footprint taxation on petro-route acids (CBAM) | -0.5% | Europe, indirect impact on global trade flows | Medium term (2-4 years) |

| Competitive threat from succinic and malic acid in shelf-stable foods | -0.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Maleic-Anhydride Feedstock and Benzene Spot Prices

Spot maleic-anhydride quotations see-sawed between USD 1,050 and USD 1,400 per ton in China during 2024-2025, mirroring benzene price swings. Several small Chinese fumaric acid producers idled units in Q1 2024 when benzene briefly spiked past CNY 7,200 per ton. European operators faced a double hit from volatile benzene and natural-gas prices that averaged EUR 35-45 per MWh in 2024. Lacking long-term maleic contracts, producers struggle to lock in stable margins, prompting vertical integration and portfolio diversification.

EU CO₂-Footprint Taxation on Petro-Route Acids (CBAM)

Full enforcement of CBAM in January 2026 imposes a levy equivalent to EUR 80-90 per ton CO₂ on imports under CN 2917. With petro-route fumaric acid carrying around 2.8 kg CO₂-eq/kg, Chinese shipments face a USD 50-70 per ton landing-cost increase. European buyers are now qualifying suppliers able to certify ISO 14067 footprints or offer bio-based alternatives, tilting the trade balance toward regional and carbon-negative production.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Food grade drives the clean-label revolution

Food-grade accounted for 66.28% of the Fumaric Acid market in 2025, expanding at a 4.51% CAGR to 2031. Bartek’s new line is devoted wholly to food-grade output, illustrating strategic emphasis on higher-margin, regulation-intensive channels. Technical-grade demand, tied closely to UPR and alkyd resins, lags amid CBAM costs and volatile maleic feedstocks, yet remains vital for construction and automotive coatings.

Bio-fermentation has compressed the historic 20-25% price premium down to 12-15% by 2025, increasing addressable demand in price-sensitive developing markets. BASF expects its CO₂-negative process to reach commercial readiness by 2027, potentially redefining the carbon disclosure landscape for food additives. Producers with dual-spec plants can toggle between grades to cushion swings in either segment, a hedge increasingly favored by integrated chemical houses.

By Application: Food and Beverage Processing leads Multi-sector Growth

Food and beverage processing commanded 34.76% of Fumaric Acid market size in 2025 and is advancing at a 4.74% CAGR, buoyed by clean-label momentum and hydrophobic leavening properties in bakery mixes. UPR benefits from EV and wind-blade adoption yet faces eventual substitution from carbon-fiber prepregs in high-end vehicles.

By End-user Industry: Chemical Segment Faces Substitution Pressure

Chemical absorbed 59.54% of global volume in 2025, but growth is slowing as bio-epoxy and carbon-fiber systems advance. Food and beverage end-users are the main growth engine, switching from synthetic acidulants to fermentation-based options under label-cleaning programs. The pharmaceutical end-user pool, though smaller, expands most rapidly on DMF uptake, while cosmetics gain traction as brands emphasize naturally derived actives. Animal nutrition and semiconductor polymers collectively add a steady, regulation-driven uplift.

Pharmaceutical industry is growing at 4.96% CAGR through 2031 as dimethyl fumarate consolidates its role in multiple sclerosis and psoriasis therapies. Premium pricing of USD 3,500-4,500 per ton under GMP standards lures producers able to clear pharmacopeial hurdles. Specialty polymers for semiconductor water treatment and rosin-sizing agents for food-contact paper round out a portfolio of high-margin, lower-volume uses.

Geography Analysis

Asia-Pacific controlled 60.21% of global volume in 2025 and is set for a 4.88% CAGR through 2031. China alone contributes major world capacity, with clusters in Shandong, Hebei, and Jiangsu and a growing share of bio-fermentation units. India is scaling output to meet pharmaceutical and food-grade demand, while Japan and South Korea rely on imports aligned with stringent purity laws. ASEAN nations, especially Vietnam and Thailand, are emerging demand bases as rising urban incomes fuel convenience-food uptake.

North America benefits from Bartek’s capacity doubling, positioning the region as a net exporter of bio-grade material. Europe is reshaping supply chains in response to CBAM. Germany, France, and Italy are key consumption nodes, with regional resin producers qualifying low-carbon feedstock. EFSA’s favorable feed-additive ruling further enlarges the European addressable pool.

South America and the Middle East and Africa together account for lower global demand. Brazil leads South America via its food sector, while Argentina trials fumaric acid in livestock rations. Gulf Cooperation Council nations are exploring backward integration for construction-grade resins, and South Africa provides incremental pharmaceutical and food-processing demand.

Mordor Intelligence provides coverage of the fumaric acid market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Value Chain Analysis

Upstream supply for fumaric acid is split between petro and bio routes. The petro route starts with benzene and butane value chains that feed maleic anhydride (or maleic acid), followed by isomerization to fumaric acid, making producer economics sensitive to maleic-anhydride and aromatics volatility. This has been associated with periodic operating-rate cuts among sub-scale producers during high feedstock-price periods. The bio route uses carbohydrate inputs (glucose, sucrose, starch hydrolysates) and increasingly agro-industrial byproducts (for example, apple pomace or lignocellulosic biomass) fermented with Rhizopus strains, which creates scope to localize supply around sugar and biomass availability while targeting lower footprint grades.

Midstream operations typically include reaction or fermentation, crystallization, filtration, drying, milling or granulation, and packaging (bags, big bags, and in some cases bulk). Quality systems and compliance act as a key value-chain gate for higher-margin outlets, with food additive specifications aligned to Codex Alimentarius (INS 297), EU E 297, and US FDA requirements, plus additional pharmacopeial and GMP expectations for pharma-related intermediates. Downstream distribution combines direct supply to large food, resin, and chemical accounts with regional distributors and traders, with Asia-Pacific, notably China, functioning as the largest supply hub. Seasonality and logistics, including holiday-related shutdowns in Chinese production clusters, can tighten spot availability and push buyers toward contracted volumes or diversified sourcing.

Competitive Landscape

The Fumaric Acid market exhibits a moderate concentration: Bartek Ingredients, Polynt, Thirumalai Chemicals, FUSO Chemical, and Yantai Hengyuan together control roughly 69% of installed capacity. Bartek’s Stoney Creek plant, online since September 2024, delivers an 80% emissions cut and solidifies the firm’s position as the largest bio-based producer. BASF’s CO₂-negative FUMBIO pilot, backed by EUR 2.6 million in federal funding, illustrates big-chemistry bets on stricter carbon policies[2]BASF SE, “FUMBIO Project Targets Carbon-Negative Organic Acids,” basf.com .

Niche opportunities in semiconductor polymers and pharma-grade intermediates provide attractive margins but demand stringent quality systems, limiting easy entry. Chinese start-ups such as Huaheng Bio and Xuelang Bio are piloting 2,000-10,000 ton bio-plants, though export penetration hinges on meeting Western regulatory audits. Vertical integration is accelerating in both directions: resin producers such as Polynt consider backward moves into fumaric acid, while acid producers eye forward integration into specialty resins and pharma esters.

Fumaric Acid Industry Leaders

Bartek Ingredients Inc.

Polynt S.p.A.

Thirumalai Chemicals

FUSO CHEMICAL CO., LTD.

Yantai Hengyuan Biotechnology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace is emerging for verified low-carbon and traceable-route fumaric acid across food, feed, and resin applications as buyers respond to carbon disclosure requirements and EU import cost adders such as the EU Carbon Border Adjustment Mechanism (fully enforced in January 2026). This is tightening supplier qualification around footprint documentation, including ISO 14067-aligned reporting mentioned in the market context, and it is increasing investment attention on fermentation-based acids that can be positioned as drop-in alternatives where labeling and sustainability claims carry weight.

Commercial and technical signals also support new outlets for bio-based organic acids within existing acidulant portfolios and specialty polymers. BASF launched the FUMBIO project in June 2024 with German university partners to develop CO2-neutral, bio-based fumaric acid using Basfia succiniciproducens, reinforcing the pathway from pilot programs to scalable production know-how. In Europe, Afyren reported in June 2026 that it ramped output at its Neoxy biorefinery in Carling Saint-Avold and reached 20% of its planned 16,000-tonne annual capacity, indicating that industrial bio-acid capacity is being brought onstream in the region. On the application side, tighter ultrapure-water specifications in advanced semiconductor fabs and ongoing material substitution toward UPR composites create demand pockets that reward consistent purity and supply reliability, favoring producers with dual-grade flexibility and stronger QA and audit readiness.

Recent Industry Developments

- March 2026: Thirumalai Chemicals reported that scrubber solution generated from its phthalic anhydride operations is repurposed as a raw material input for fumaric acid production as part of its FY2025-26 sustainability disclosures. This illustrates circular integration within large acid platforms and supports tighter control over input availability and waste handling for cost and compliance advantages.

- December 2025: ICL Group signed a definitive agreement to acquire Bartek Ingredients in a two-phase transaction, starting with an investment of about USD 90 million for a 50% stake, with the first phase targeted to close in Q1 2026. The deal strengthens ICLs position in specialty food ingredients and shelf-life solutions while adding a scaled acidulants manufacturing footprint that is directly relevant to food-grade fumaric acid supply dynamics.

- November 2024: The Government of Canada announced CAD 27 million in support for Bartek Ingredients 192.5 million CAD project to build a new food ingredient manufacturing facility in Ontario. This public funding supports a major North American capacity and capability buildout, improving regional supply resilience for regulated food-grade organic acids and related value-added ingredients.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the global demand for fumaric acid sold as a finished chemical product, across food, industrial, and related downstream uses, tracked in physical volume where grades and end-use suitability are comparable.

Scope exclusions: We exclude in-process reuse and non-qualifying derivatives where the material is not traded or consumed as finished-grade fumaric acid.

Segmentation Overview

- By Grade

- Food Grade

- Technical Grade

- By Application

- Food and Beverage Processing

- Unsaturated Polyester Resin (UPR)

- Alkyd Resin

- Rosin Paper Sizing

- Personal Care and Cosmetics

- Other Applications

- By End-user Industry

- Chemical

- Food and Beverage

- Cosmetics

- Pharmaceutical

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a simple fact base on fumaric acid supply, trade movements, and end-use pull, so later assumptions could be checked against observable signals. We relied on public sources such as customs and tariff-line trade statistics, national statistical offices for chemicals output indices, and regulatory or standards references that clarify food additive and industrial-grade usage rules.

To understand how volume is likely to distribute by region, we also reviewed trade association publications, peer-reviewed chemistry and materials papers on production routes and yield ranges, and broader macro indicators such as processed food output and resin production proxies. Company annual reports, investor decks, and credible press releases were used to sense capacity changes, outages, and debottlenecking timing. Where helpful, we also used paid databases for company financials and for shipment-level import and export checks to sanity-test trade flows. These sources are illustrative, and we consulted additional public references during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary conversations were used to pressure-test volume splits by grade and application, and to confirm how pricing is actually handled, including contracting behavior, spot exposure, and pass-through of feedstock changes. We spoke with producers, distributors, and large end users, and then rechecked the regional logic across APAC, EMEA, and the Americas so the final model aligned with buying and supply patterns seen in practice.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 19% | APAC: 46% |

| Mid tier: 45% | Functional/Unit leaders: 21% | EMEA: 35% |

| Smaller Players: 20% | Managers: 60% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where production and trade data reconstruct the available finished-grade fumaric acid pool, which is then aligned to the most probable end-use consumption by region. To keep the totals realistic, we also ran selective bottom-up approximations, including sampled supplier roll-ups and simple ASP times volume checks by grade, and then adjusted for gaps where coverage was thin.

Key inputs used in the model included global and regional output signals for resins and processed foods, import and export movements by major trading routes, operating rate and capacity change timing, typical grade mix by end-use, and observed price ranges by contract cycle. Forecasts were developed using scenario analysis supported by a light multivariate regression overlay, where demand drivers such as packaged food output and industrial production indices were stress-tested with interview feedback. When a country-level data point was missing, we bridged it using nearest-neighbor trade patterns and consumption intensity, and then revalidated the implied per-capita and per-industry usage levels before finalizing.

Data Validation & Update Cycle

Outputs were checked through triangulation across independent signals, including trade balances, regional supply additions, and downstream activity indicators, so no single noisy input could dominate the result. Variance checks were run on implied prices, yield assumptions, and regional consumption splits, and anything that looked off was reviewed again and corrected with a second pass.

Before sign-off, the model is reviewed in steps, with peer checks on calculations and logic and a final consistency review against recent market events. The report is refreshed annually, and interim updates are triggered when there are material capacity moves, policy shifts, or demand shocks. Right before delivery, a fresh validation sweep is completed so clients receive the most current view.

Mordor Intelligence's Fumaric Acid Market Size Compared Against Other Published Estimates

Published market sizes for fumaric acid can look far apart because sources do not always measure the same scope, and the same year can be priced and converted differently. Differences show up most often when one estimate is value-based and another is volume-based, or when adjacent acids and derivatives are quietly included.

A second set of gaps comes from how pricing is carried through the model, since contract cycles, currency timing, and regional grade mix can change the value even if the physical tons remain stable. When refresh cadence is slower, capacity additions and trade dislocations can sit outside the model for months, which then affects implied utilization and the final market size.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.31 M (2026) | |

| Global Consultancy A | USD 0.56 B (2023) | This figure is published in revenue terms, and the public summary does not clarify the price basis, grade boundaries, or currency conversion timing, which can inflate or compress the value relative to a volume-led view. |

| Industry Publisher B | USD 0.62 B (2025) | The estimate uses a later base year and a higher growth path, and the disclosed summary does not specify whether captive internal reuse, derivative streams, or broader organic acids are filtered out consistently. |

The spread in the table is mainly explained by unit choice and pricing mechanics rather than a single demand disagreement. For that reason, our checks focus on timing, conversions, and realistic grade mix before totals are finalized. By refreshing currency and ASP assumptions around the latest contract windows and then validating the implied tons against trade and capacity signals, Mordor Intelligence keeps the 2026 level tied to what is actually being produced, traded, and consumed as finished-grade material.

Key Questions Answered in the Report

What is the current global volume for the Fumaric Acid market?

It stood at 307.93 kilotons in 2026 and is projected to reach 376.09 kilotons by 2031.

How does CBAM affect pricing in Europe?

The mechanism adds USD 50-70 per ton to high-carbon imports, narrowing the historical price gap with European bio-based supply.

Why is food-grade fumaric acid gaining share?

Clean-label regulations in Asia-Pacific and Europe favor fermentation-derived material with verified purity and low carbon footprints.

What competitive advantage do carbon-negative processes offer?

They qualify for green-finance incentives and help buyers meet scope-3 emission targets, supporting premium pricing and market access.

Page last updated on: