Fatty Acid Methyl Ester Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

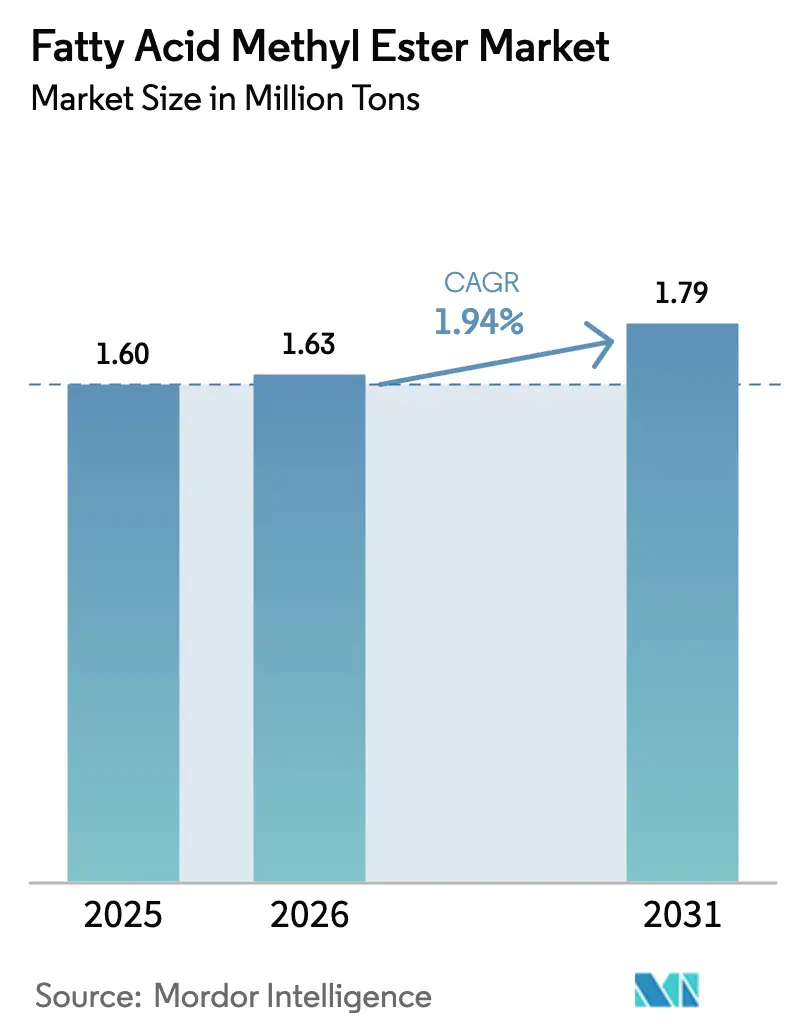

| Market Volume (2026) | 1.63 Million tons |

| Market Volume (2031) | 1.79 Million tons |

| Growth Rate (2026 - 2031) | 1.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fatty Acid Methyl Ester Market Analysis by Mordor Intelligence

The Fatty Acid Methyl Ester Market size is expected to grow from 1.60 million tons in 2025 to 1.63 million tons in 2026 and is forecast to reach 1.79 million tons by 2031 at a 1.94% CAGR over 2026-2031. Solid blend mandates in Indonesia, Brazil, and the European Union safeguard baseline consumption, but widening premiums for used cooking oil over virgin palm oil have turned feedstock arbitrage into the primary driver of producer margins. Renewable diesel investments by large energy companies are redirecting waste oils toward hydro-treating units, shortening supply for traditional trans-esterification plants. Personal-care formulators are auditing ingredient lists for biodegradability, prompting fast growth in oleochemical-grade esters that can command 60–80% price premiums over fuel grades. Against this backdrop, companies that secure long-term waste-oil contracts or pilot algal-oil cultivation gain resiliency as the Fatty Acid Methyl Ester market navigates tightening sustainability criteria under the EU Renewable Energy Directive III and similar frameworks in North America and Asia.

Key Report Takeaways

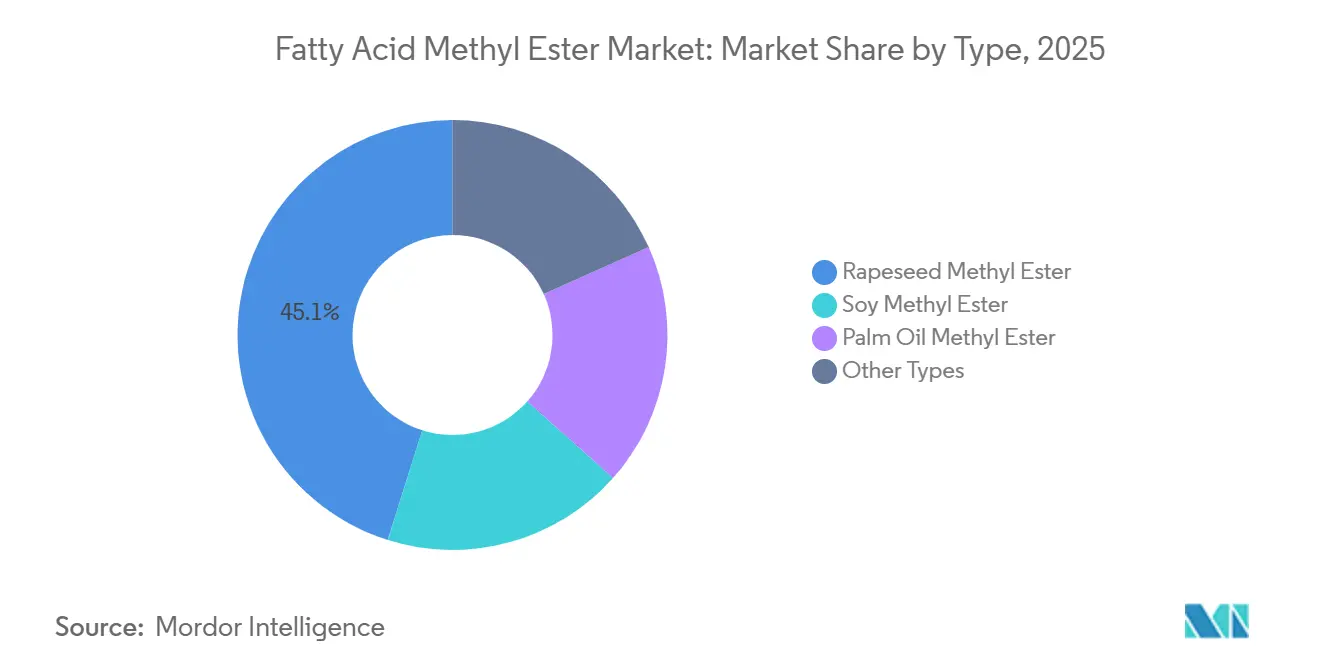

- By type, rapeseed methyl ester led with 45.12% of Fatty Acid Methyl Ester market share in 2025, while the “Other Types” segment is forecast to accelerate at a 2.76% CAGR through 2031.

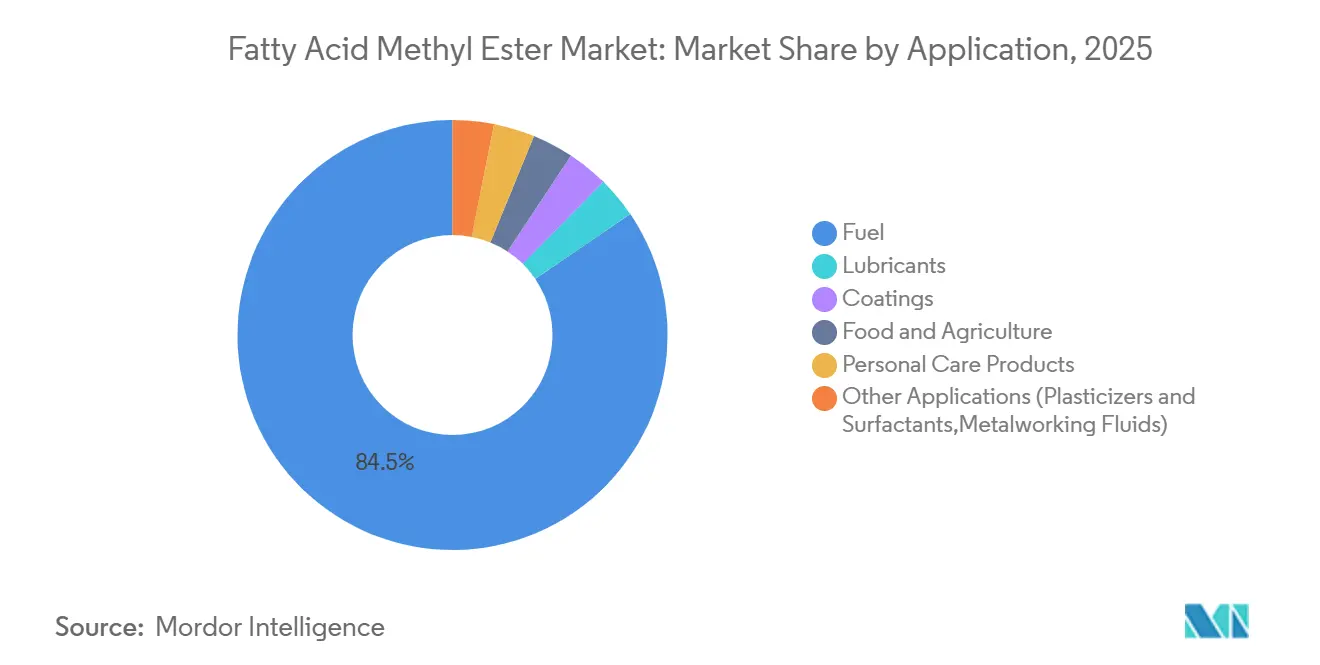

- By application, fuel maintained 84.52% share of the Fatty Acid Methyl Ester market size in 2025, yet personal care products record the fastest expansion at a 3.29% CAGR to 2031.

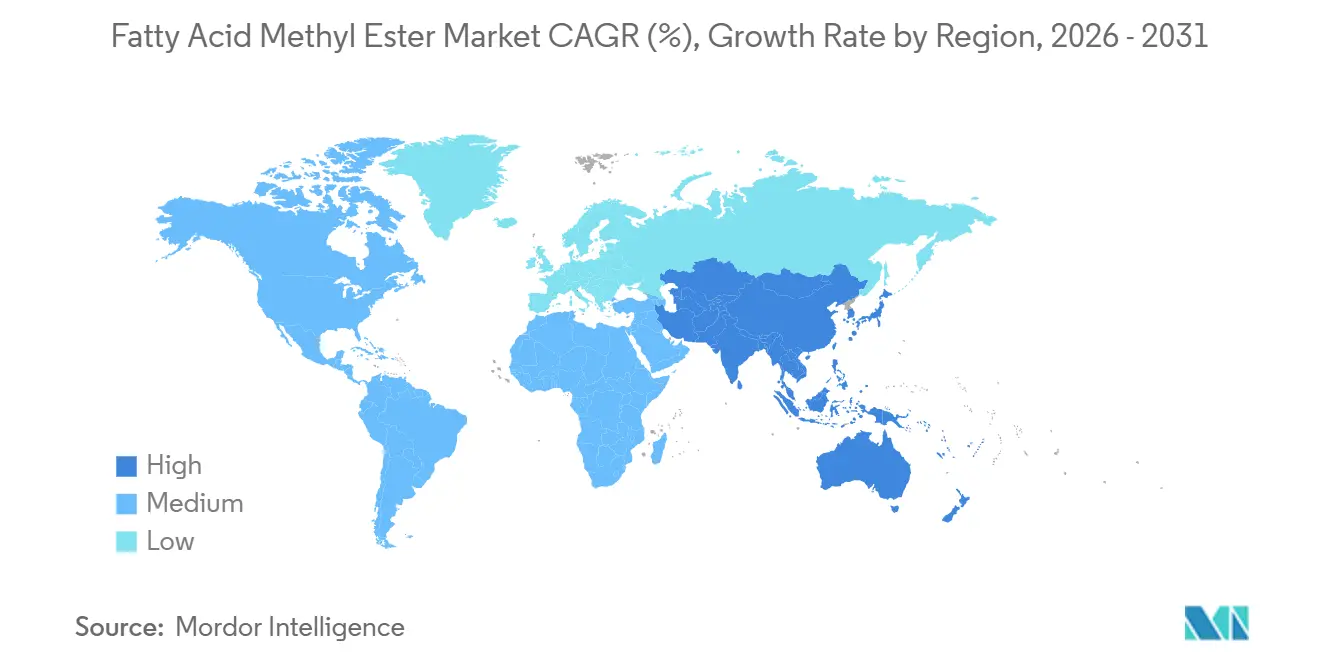

- By geography, Europe accounted for 38.92% of 2025 volume, whereas Asia-Pacific is poised for the briskest regional growth at a 3.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fatty Acid Methyl Ester Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating biodiesel blend mandates | +0.8% | Indonesia, Brazil, EU, India | Medium term (2–4 years) |

| Increasing feedstock availability and cost competitiveness | +0.5% | Indonesia, Malaysia, China, Brazil, Argentina | Short term (≤ 2 years) |

| Rising demand for low-sulfur renewable diesel substitutes | +0.3% | Europe, North America | Medium term (2–4 years) |

| Maritime bio-bunkering pilots adopting FAME blends | +0.2% | Singapore, Rotterdam, Hamburg | Long term (≥ 4 years) |

| Increasing demand from personal care industry | +0.3% | North America, Europe, Asia-Pacific urban centers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Biodiesel Blend Mandates

Indonesia will introduce a B50 requirement in 2026 that is expected to absorb about 11 million tons of palm oil annually, insulating domestic producers from export volatility[1]Indonesian Ministry of Energy and Mineral Resources, “Biodiesel Policy Roadmap,” esdm.go.id. Brazil’s phased move to B15 adds 1.5 billion liters of incremental demand under RenovaBio, while the United States proposes biomass-based diesel volumes of 7.12–7.50 billion RINs but intends to discount credits tied to imported feedstocks[2]United States Environmental Protection Agency, “Proposed Renewable Volume Obligations 2026-2027,” epa.gov. In Europe, RED III preserves a 29% transport-energy target yet caps crop-based biofuels at 7%, nudging investments toward waste-oil esters. Certification schemes such as ISCC and REDcert-EU now cover more than 15,000 sites, shaping global trade access.

Increasing Feedstock Availability and Cost Competitiveness

Municipal collection programs lifted China’s used-cooking-oil exports to the EU to 1.2 million tons in 2024, supported by ISCC approvals. Double-counting credits under RED III keeps European UCO economical despite the average 2024 prices of EUR 950 per ton. Palm oil eased to MYR 3,800–4,000 per ton by late-2024, boosting margins for Southeast Asian producers holding long-term contracts. However, weather shifts in South America or palm-export quotas in Indonesia can swiftly reverse the cost advantage, underscoring the feedstock risk embedded in the Fatty Acid Methyl Ester market.

Rising Demand for Low-Sulfur Renewable Diesel Substitutes

The International Maritime Organization’s 0.5% sulfur cap pushes shipowners to adopt low-sulfur alternatives, and B7–B20 FAME blends offer a retrofit-friendly route for vessels lacking scrubbers. Trials in Singapore validated B24 blends in harbor tugs, demonstrating stable cold-flow behavior at 10 °C. Although renewable diesel outperforms in storage life and cold-flow, its higher price keeps FAME attractive for operators prioritizing cost over performance, especially within coastal shipping corridors.

Maritime Bio-Bunkering Pilots Adopting FAME Blends

Rotterdam and Hamburg inaugurated dedicated bio-bunkering infrastructure in 2024, supplying B30 blends that cut lifecycle emissions by up to 65% when derived from certified waste oils. The EU’s FuelEU Maritime rule imposes a 2% greenhouse-gas reduction from January 2025, and penalties of EUR 2,400 per ton of CO₂-equivalent shortfall strengthen the business case for niche vessels such as ferries and offshore support craft to adopt FAME despite its lower energy density.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vegetable-oil price volatility | –0.4% | Indonesia, Malaysia, Americas | Short term (≤ 2 years) |

| Competition from alternative biofuels and renewable diesel | –0.3% | North America, Europe | Medium term (2–4 years) |

| Regulatory uncertainty and policy dependence | –0.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vegetable-Oil Price Volatility

Palm-oil futures swung from MYR 5,200 per ton in early 2023 to MYR 3,800 per ton by December 2024, slicing FAME margins by as much as 20 percentage points for producers lacking hedges. Soybean oil prices saw a similar pattern in the United States, peaking at 68 cents per pound in March 2024, then sliding to 42 cents by October as Brazilian harvests surged. With feedstock accounting for up to 85% of production cost, such volatility can erode profitability swiftly.

Competition from Alternative Biofuels and Renewable Diesel

Global hydrotreated-vegetable-oil capacity climbed to 12 million tons by end-2024, absorbing waste oils that once flowed to FAME plants. U.S. and California tax credits raise the compliance value of HVO, while RED III awards higher energy multipliers to waste-based HVO versus crop-based FAME. The resulting feedstock bidding war lifted tallow to USD 0.55 per pound by late-2024, squeezing FAME refiners that rely on the same residues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Waste-Derived Esters Gain Traction

Other Types - spanning waste-oil, animal-fat, and algal-oil methyl esters - are set to expand at a 2.76% CAGR through 2031, outpacing the overall Fatty Acid Methyl Ester market. Waste-oil ester output in China totaled 1.8 million tons in 2024, with Sinopec and COFCO exporting certified cargoes to Rotterdam and Hamburg. North American renderers such as Darling Ingredients supplied 400,000 tons of tallow-based FAME, leveraging vertically integrated collection networks.

Rapeseed methyl ester retained 45.12% global volume in 2025 due to Europe’s 8 million-ton refining base and cold-flow advantages that align with EN 14214 norms, while soy methyl ester dominated the Americas. Palm-oil esters, concentrated in Indonesia and Malaysia, face EU ILUC caps that freeze import quotas at 2019 levels. Certification under ISCC and REDcert is therefore pivotal for market access, and producers unable to document zero-deforestation supply chains risk exclusion.

By Application: Personal Care Outpaces Fuel

Fuel remained the largest user at 84.52% of volume in 2025, but its 1.6% CAGR reflects blend-ratio ceilings in mature markets and substitution by renewable diesel. Europe’s B7 ceiling has been unchanged since 2020, the United States broadly operates within B5–B20, and Indonesia’s upcoming B50 adds incremental but not exponential growth. In contrast, personal care products are rising at a 3.29% CAGR as biodegradable esters penetrate shampoos, lotions, and cleansers. Cargill’s BiOH line replaced petroleum-derived isopropyl myristate in 18 brand portfolios during 2024, illustrating the price-inelastic customer base that underpins margin stability within this slice of the fatty acid methyl ester market.

Geography Analysis

Europe commanded 38.92% of global volume in 2025, yet renewable diesel plants and advanced-biofuel quotas are siphoning feedstocks away from traditional FAME. Germany’s 2024 output slipped 4% to 2.8 million tons as UCO shortages pressed margins, while France held flat at 1.6 million tons thanks to Saipol’s integrated rapeseed assets. The United Kingdom issued 1.2 million Renewable Transport Fuel Certificates for FAME in 2024, 8% lower than the prior year as refiners pivoted toward HVO. Nordic demand remains modest but is shifting quickly to waste-based alternatives, reinforcing Europe’s structural feedstock shift.

Asia-Pacific is primed for a 3.54% CAGR through 2031. Malaysia exported surplus volumes to the Philippines and Thailand, but softer palm prices narrowed refinery spreads. China’s domestic output is centered on municipal waste-oil programs, with 80% of production exported to the EU, where double-counting incentives prevail. India lags due to ethanol-blend priorities, while Japan and South Korea import modest cargoes to deliver corporate sustainability pledges.

North America accounted for a significant market share in 2025. The United States led with outstanding volume consumption anchored by rapidly scaled soybean-oil refining in Iowa and Illinois. Canada consumed 320,000 tons under its Clean Fuel Regulations, and Mexico relied on imports for 180,000 tons. South America supplied 3.2 million tons in 2024, with Brazil’s B12 rule absorbing 6.3 billion liters and Argentina exporting 1.2 million tons after trade disputes eased. The Middle East and Africa remain nascent but show potential as Saudi Arabia channels USD 500 million into a 300,000-ton waste-oil project slated for 2026.

Competitive Landscape

The Fatty Acid Methyl Ester market remains moderately consolidated. Specialty players carve profitable niches. Leading players in the market, including KLK OLEO, are directing investments toward molecular distillation that yields ≥99.5% purity and sulfur below 5 ppm, supporting 18–22% EBITDA margins in personal-care and lubricant grades. Start-ups and waste-aggregation platforms such as Olleco and Crimson Renewable Energy disrupt the supply chain by contracting directly with municipalities, capturing up to 30% of feedstock margin, and challenging traditional crushers.

Fatty Acid Methyl Ester Industry Leaders

Wilmar International Ltd

Cargill, Incorporated.

Archer Daniels Midland Co.

BASF

KLK OLEO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Wilmar International inaugurated a 500,000-ton palm-oil methyl ester refinery in Dumai, Indonesia, with continuous reactors and zero-liquid-discharge systems aimed at B50 compliance volumes.

- August 2024: Cargill and Bunge created a joint venture covering 1.8 million tons of soybean-crushing and FAME capacity in Brazil to secure long-term supply for Petrobras auctions.

Global Fatty Acid Methyl Ester Market Report Scope

Fatty acid methyl esters (FAME) are a type of fatty acid ester derived from the transesterification of methanol fats. The biodiesel molecules are mainly fatty acid methyl ester, typically obtained by transesterification from vegetable oils.

The fatty acid methyl ester market is segmented by type, application, and geography. By type, the market is segmented into rapeseed methyl ester, soy methyl ester, palm oil methyl ester, and other types. By application, the market is segmented into fuel, lubricants, coatings, food and agriculture, metalworking fluids, personal care products, and other applications. The report also covers the market sizes and forecasts in 18 countries across the major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Rapeseed Methyl Ester |

| Soy Methyl Ester |

| Palm Oil Methyl Ester |

| Other Types (Waste-Oil Methyl Ester, Animal-Fat-Derived Methyl Ester, Algal-Oil Methyl Ester) |

| Fuel |

| Lubricants |

| Coatings |

| Food and Agriculture |

| Personal Care Products |

| Other Applications (Plasticizers and Surfactants,Metalworking Fluids) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Type | Rapeseed Methyl Ester | |

| Soy Methyl Ester | ||

| Palm Oil Methyl Ester | ||

| Other Types (Waste-Oil Methyl Ester, Animal-Fat-Derived Methyl Ester, Algal-Oil Methyl Ester) | ||

| By Application | Fuel | |

| Lubricants | ||

| Coatings | ||

| Food and Agriculture | ||

| Personal Care Products | ||

| Other Applications (Plasticizers and Surfactants,Metalworking Fluids) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What volume does the Fatty Acid Methyl Ester market target by 2031?

Global demand is forecast to reach 1.79 million tons by 2031, growing at a 1.94% CAGR.

Which feedstock segment is expanding fastest?

Waste-derived esters—encompassing used cooking oil, animal fat, and algal oil—are projected to rise at a 2.76% CAGR to 2031.

Why is personal care demand increasing for these esters?

Formulators favor biodegradable, silicone-free ingredients that comply with EU and Ecocert standards, driving a 3.29% CAGR in personal-care usage.

How will Indonesia’s B50 mandate influence the market?

B50, starting 2026, will absorb about 11 million tons of palm oil per year, securing domestic offtake and supporting Asia-Pacific growth.

Which regions are poised for the highest growth rates?

Asia-Pacific leads with a projected 3.54% CAGR through 2031, supported by Indonesia’s escalating mandates and China’s UCO export infrastructure.

What strategic moves are producers making to sustain margins?

Companies are locking in long-term waste-oil contracts, investing in high-purity oleochemical lines, and pursuing process-intensification patents to cut conversion costs.

Page last updated on: