Butyric Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

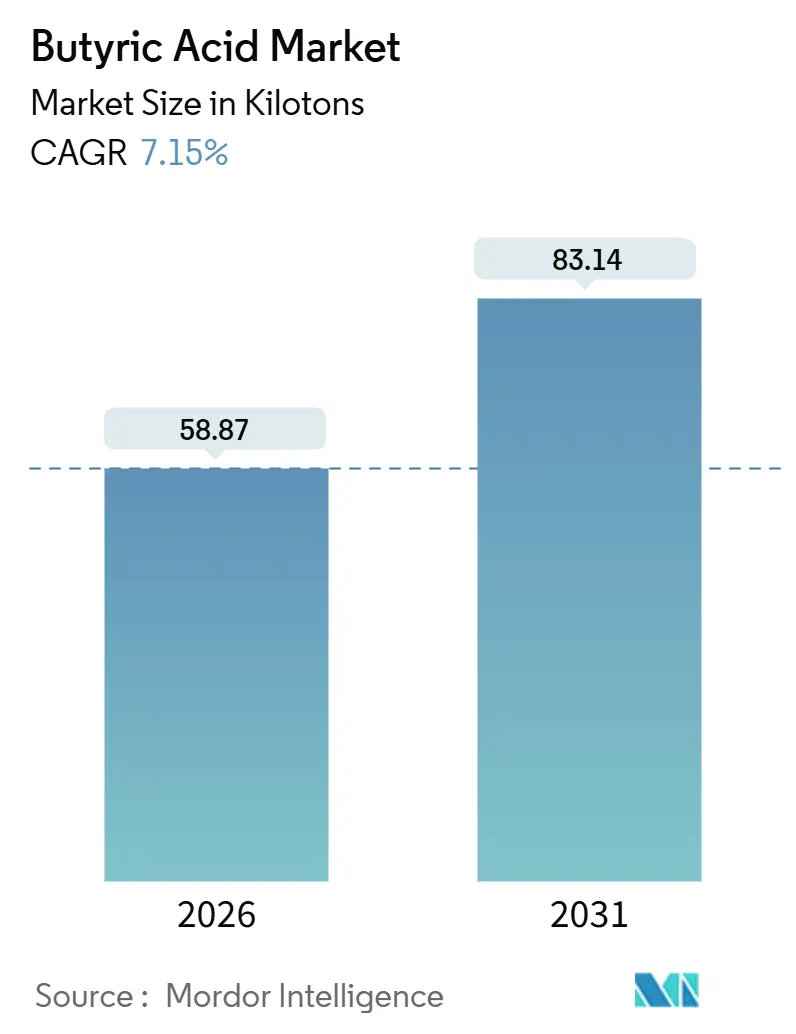

| Market Volume (2026) | 58.87 kilotons |

| Market Volume (2031) | 83.14 kilotons |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Butyric Acid Market Analysis by Mordor Intelligence

The Butyric Acid Market size is estimated at 58.87 kilotons in 2026, and is expected to reach 83.14 kilotons by 2031, at a CAGR of 7.15% during the forecast period (2026-2031). Heightened demand for precision-livestock feed additives, clean-label food preservatives, and pharmaceutical-grade short-chain fatty acids underpins this steady climb. Synthetic routes remain dominant because of scale efficiencies, yet incremental carbon-pricing mechanisms and brand commitments to circular sourcing continue to steer investment toward renewable fermentation capacity. Food formulators favor butyric esters that deliver authentic butter notes while lowering reliance on synthetic diacetyl, whereas clinical developers value the compound’s histone-deacetylase-inhibiting properties in gastrointestinal therapeutics. Nevertheless, price swings in butanol and propylene feedstocks, coupled with stringent odor-abatement requirements, keep operating costs volatile and pose barriers for new entrants.

Key Report Takeaways

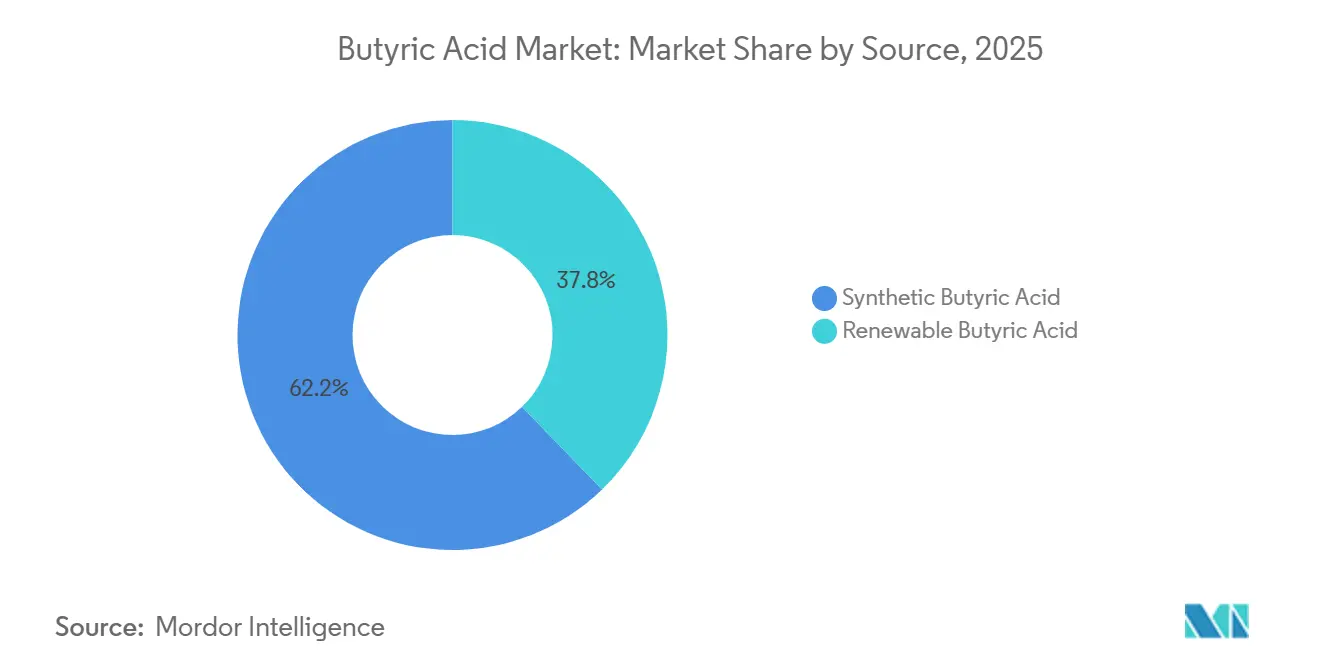

- By source, synthetic butyric acid accounted for 62.24% of the Butyric Acid market share in 2025, while renewable butyric acid is projected to expand at an 8.92% CAGR through 2031.

- By grade, food grade led with 40.67% share in 2025, whereas pharmaceutical grade is forecast to post a 9.10% CAGR during 2026-2031.

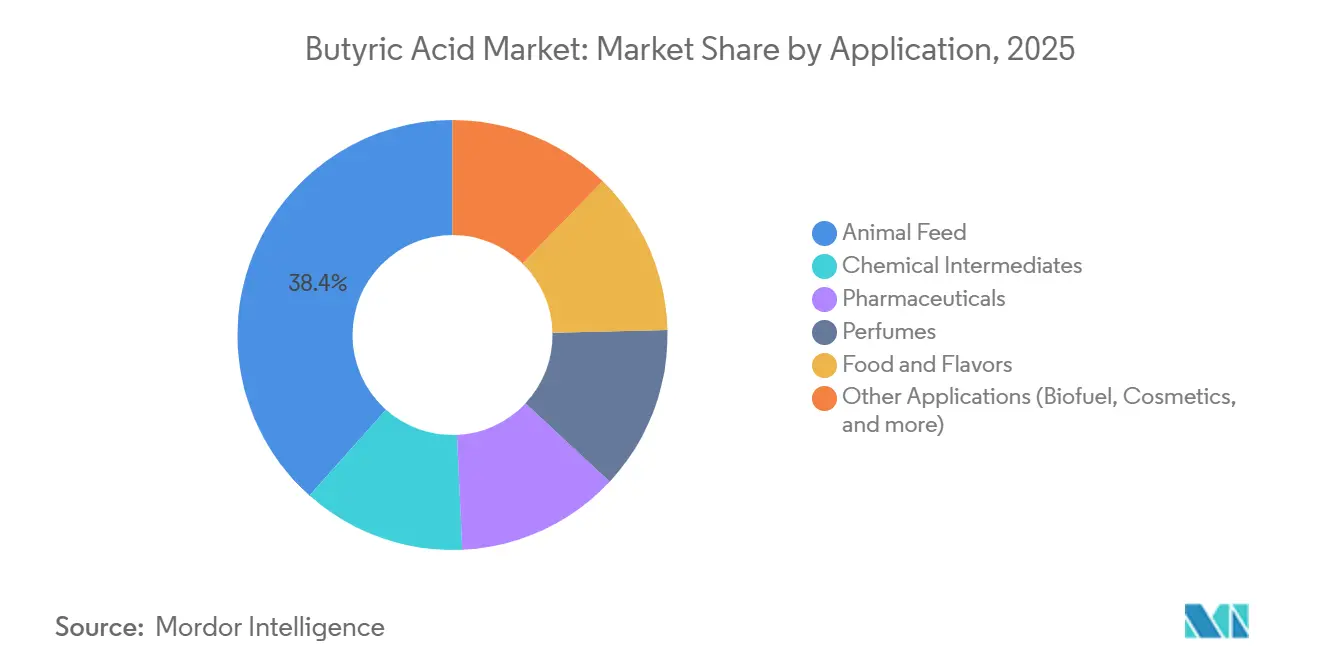

- By application, animal feed held 38.41% of the Butyric Acid market size in 2025 and is set to grow at a 9.61% CAGR to 2031.

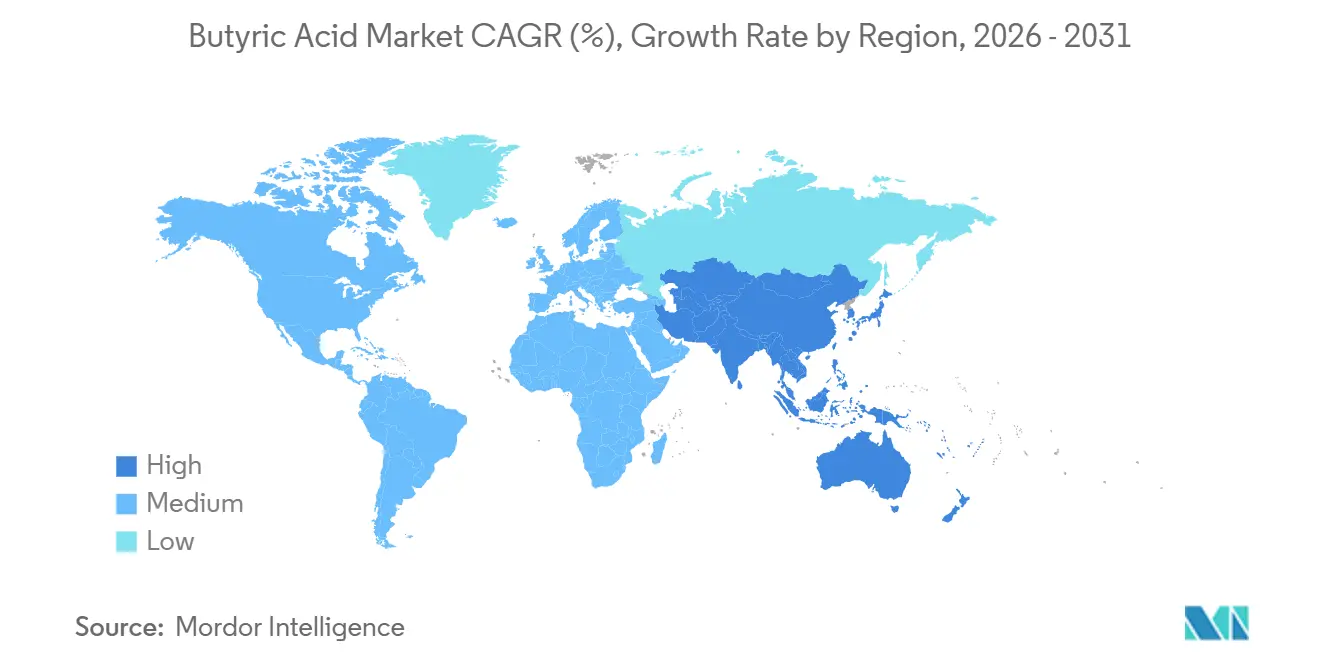

- By geography, Asia-Pacific commanded 38.82% share of the Butyric Acid market in 2025, and the region is expected to progress at an 8.14% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Butyric Acid Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing utilization in animal-feed gut-health additives | +2.8% | Global, led by Asia-Pacific and North America | Medium term (2–4 years) |

| Demand as natural flavoring & clean-label preservative | +1.5% | North America & Europe | Short term (≤2 years) |

| Pharma interest in SCFA-based therapeutics & pro-drugs | +1.2% | North America & Europe | Long term (≥4 years) |

| Adoption of precision-livestock farming enabling butyrate-based tools | +1.0% | Asia-Pacific core, spill-over to South America | Medium term (2–4 years) |

| Circular bio-economy push: fermentation of ag-waste to butyrate | +0.9% | Global, early gains in China, Europe, Brazil | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Utilization in Animal-Feed Gut-Health Additives

Regulatory bans on growth-promoting antibiotics in Europe and voluntary phase-outs in North America have accelerated the switch to sodium butyrate and tributyrin, which improve intestinal barrier function and microbiome balance, translating into 5%–8% stronger feed conversion ratios. Precision-feeding platforms dose protected butyrate in real time, lifting per-animal consumption by up to 15% over static rations. Kemin Industries disclosed a 22% year-over-year rise in protected butyrate sales into Asian aquaculture during 2025 as shrimp farmers sought antibiotic-free mortality control[1]Kemin Industries, “Technical Bulletin: Protected Butyrate in Shrimp Health,” kemin.com. China’s Ministry of Agriculture streamlined additive registrations in 2025, triggering local fermentation capacity additions due online in 2027.

Demand as Natural Flavoring & Clean-Label Preservative

Food manufacturers in the United States and European Union continue to replace synthetic diacetyl with butyric acid esters to satisfy transparent-label expectations. The US Food and Drug Administration reaffirmed the compound’s GRAS status for flavoring in 2024, and the European Food Safety Authority removed concentration caps on butyrate esters for dairy applications in 2025[2]European Food Safety Authority, “Re-evaluation of Butyrate Esters for Use in Dairy Applications,” efsa.europa.eu. Formulators report being able to cut potassium sorbate loadings by 30% when leveraging butyric acid’s mild antimicrobial action, reducing both cost and label length. Clean-label positioning propelled a 12% jump in North American and European food-grade demand during 2025.

Pharma Interest in SCFA-Based Therapeutics & Pro-Drugs

Phase II clinical data published in 2025 showed enteric-coated sodium butyrate tablets lowering ulcerative colitis activity scores by 40% against placebo, stimulating investigational new drug applications for butyrate-centered therapies. Pro-drug versions such as tributyrin enhance systemic bioavailability by bypassing rapid hepatic metabolism, while high-purity feedstock must meet stringent USP or Ph.Eur. heavy-metal and solvent specifications. Merck KGaA’s launch of ≥99.5%-pure butyric acid in 2024 underscores confidence in impending regulatory approvals.

Adoption of Precision-Livestock Farming Enabling Butyrate-Based Productivity Tools

Sensor-equipped feeding lines and wearable gut-health trackers let producers titrate butyrate inclusion in response to live inflammatory markers, trimming overuse during low-stress periods and intensifying supplementation during weaning or heat stress. A 2025 journal study found that dynamic dosing reduced feed cost per kilogram of broiler weight gain by 8% compared to fixed protocols. Swine nurseries recorded three-point mortality reductions when applying targeted butyrate delivery in the first 10 days post-weaning. Asia-Pacific integrators increasingly employ blockchain tracing to certify antibiotic-free meat, commanding 15%–20% export premiums in Japan and South Korea.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile butanol & propylene feedstock prices | -1.8% | Global | Short term (≤2 years) |

| Odor-control & handling challenges limiting plant adoption | -1.0% | Global, acute in densely populated regions | Medium term (2–4 years) |

| Competition from propionic & valeric acids in feed and preservation | -0.7% | Global, strongest in cost-sensitive markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Volatile Butanol & Propylene Feedstock Prices

Petrochemical routes tie production costs to butanol and propylene spot prices, which swung 25% in early 2025 amid US Gulf Coast and Middle East refinery outages, squeezing margins for producers lacking long-term contracts. Chinese electrolytic pathways starting from maleic anhydride also experienced a 12% cost hike after domestic butane shortages. While fermentation insulation exists, current separation costs keep renewable butyric acid near the upper end of competitive price bands outlined in a 2025 techno-economic study.

Odor-Control & Handling Challenges Limiting Plant Adoption

The compound’s rancid-butter odor is detectable at parts-per-billion, necessitating sealed reactors, vapor scrubbers, and specialized storage, adding 20%–30% to greenfield capital outlays. A proposed 15,000-tonne German plant required a EUR 4 million odor-abatement upgrade before permitting approval in 2024. Downstream additive suppliers rely on lipid microencapsulation to mask odor, adding USD 0.80–1.20 per kilogram to finished product cost. Tokyo Chemical Industry’s SDS lists the flash point at 75°C and a corrosive classification, underlining stringent handling needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Renewable Routes Gain Traction Amid Sustainability Mandates

Synthetic pathways controlled 62.24% of total volume in 2025, reflecting mature propylene-oxidation infrastructure. Nevertheless, renewable butyric acid is rising at an 8.92% CAGR as carbon pricing and circular-bioeconomy targets push brands to decouple from fossil feedstocks. The butyric acid market size for renewable supply is projected to expand from 22.2 kilotons in 2026 to 36.3 kilotons by 2031, equating to 44% of incremental demand. Fermentation titers exceeding 70 g/L have been demonstrated, yet downstream separation still represents around 60% of total cost. The butyric acid market share for synthetic feedstock could slip below 55% by 2031 if European carbon tariffs and Chinese subsidy programs materialize as scheduled.

Renewable developers are forging partnerships with municipal waste processors, exemplified by Perstorp’s Swedish demonstration plant that ferments sorted food waste to pharmaceutical-grade butyric acid. China’s Ministry of Industry and Information Technology embedded butyric acid in its 2024–2027 Fine Chemical Innovation Plan, offering tax rebates and pilot funding for non-food biomass routes. Synthetic producers retain an edge on cost and scale for industrial-grade sales, but brand owners in food and pharma now pay premiums of 15%–25% for verified renewable material.

By Grade: Pharmaceutical Purity Commands Premium as Therapeutic Pipelines Advance

Food-grade butyric acid accounted for 40.67% of 2025 demand, supplying butter-flavor esters and clean-label preservatives. Pharmaceutical-grade volumes remain smaller but carry gross margins roughly double those of food-grade. The butyric acid market size for pharmaceutical applications is forecast to climb from 5.9 kilotons in 2026 to 9.7 kilotons in 2031, reflecting a 9.10% CAGR. Clinical trials have moved into Phase III for ulcerative colitis, and drug sponsors require more than or equal to 99.5% purity and sub-ppm heavy-metal limits. Merck and Tokyo Chemical Industry expanded chromatography capacity during 2024–2025 to service this exacting niche.

Industrial-grade users, particularly cellulose butyrate and plasticizer manufacturers, value price over purity, purchasing products that permit higher aldehyde content. Regulatory tailwinds may eventually raise baseline purity thresholds even for industrial buyers, narrowing the cost gap but benefiting players with existing high-purity infrastructure. Food-grade remains the largest slice of the butyric acid market, but pharmaceuticals deliver the strongest profit uplift per unit of installed capacity.

By Application: Animal Feed Leads Volume and Growth as Antibiotic Alternatives Gain Traction

Animal feed held 38.41% of 2025 consumption and is expanding at a 9.61% CAGR, bolstered by antimicrobial resistance regulations and rising protein demand in Asia. The butyric acid market share for feed additives is projected to grow as precision-dosing platforms integrate real-time gut-health data, raising per-animal inclusion rates. Kemin Industries reported double-digit annual growth in protected butyrate adoption among Vietnamese and Thai shrimp farms, confirming cross-species applicability.

Chemical intermediates captured roughly one-quarter of volumes, but their cyclical link to downstream polymer demand tempers growth prospects. Food-flavor esters market share is underpinned by clean-label bakery and dairy reformulations in Europe following EFSA’s positive 2025 opinion.

Perfume applications remain mature and price sensitive. Biofuel pathways that convert butyric acid to 1-butanol or heavier hydrocarbons have cleared technical hurdles, yet remain niche until policy credit values widen.

Geography Analysis

Asia-Pacific retained 38.82% of worldwide demand in 2025 and is on track for an 8.14% CAGR through 2031. China accounts for almost half of global capacity, leveraging proximity to maleic anhydride and butanol feedstocks, while new fermentation projects aim to meet tightening sustainability targets. India’s poultry expansion, coupled with antibiotic-restriction policies, adds 1,200–1,500 tonnes per year of incremental butyrate demand. Japanese and South Korean pharmaceutical importers rely on high-purity products from Tokyo Chemical Industry and European partners. A gradual shift to renewable sourcing is expected as Chinese provinces implement carbon-trading schemes and Europe applies border adjustments.

US producers such as Eastman Chemical invest in high-chromatography purification to meet clinical-trial needs, leveraging the FDA’s reaffirmed GRAS status for flavoring applications. Europe’s circular-economy directives provide grants for waste-fed fermentation plants, epitomized by Perstorp’s Swedish demo unit. Precision-livestock platforms that modulate butyrate based on gut-health biomarkers expand rapidly in the U.S. broiler and swine sectors, supporting annual feed-grade growth.

South America benefits from Brazil’s broiler export ambitions and Argentina’s recovery in animal husbandry investment. Producers test protected-butyrate feed additives to satisfy European importers’ antibiotic-free requirements. In the Middle East and Africa, Saudi Arabia and South Africa are scaling the dairy and poultry sectors. Infrastructure constraints and climate factors slow adoption relative to other regions, yet pharmaceutical imports continue to rise.

Competitive Landscape

The Butyric Acid market exhibits a moderate concentration. Rising renewable entrants such as Kemin Industries and multiple Chinese biorefineries target fermentation niches backed by policy incentives. BASF’s green-hydrogen integration plan at Ludwigshafen could halve CO₂ intensity and protect its premium in low-carbon markets. Innovative white-space includes odor-masking encapsulation for feed additives and pro-drug chemistry that releases butyric acid in the colon. Patent filings highlight membrane separation and in-situ product removal as cost-cutting levers for fermentation plants, with a 2025 study projecting 20%–25% unit-cost reductions once energy-efficient separations move to industrial scale.

Butyric Acid Industry Leaders

Eastman Chemical Company

OXEA GmbH

Perstorp

BASF

Celanese Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kemin industries, Inc., launched ButiShield in Europe after securing EU approval for its antioxidant system, marking the firm’s first controlled-release butyrate additive targeted at companion-animal nutrition.

- January 2025: Perstorp increased the price of its butyric acid in January. The company cited escalating costs as the primary reason behind the price increase.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global butyric acid market as commercial-grade straight-chain C4 fatty acid produced through synthetic oxo routes or renewable fermentation, sold in liquid form above 96 % purity for use in feed additives, food flavors, chemical intermediates, perfumes, and regulated pharmaceutical preparations.

Scope exclusion: Salts and esters (for example, sodium, calcium, or ethyl butyrate), isobutyric acid, and captive in-house consumption are purposely left outside the sizing to maintain a clean like-for-like baseline.

Segmentation Overview

- By Source

- Renewable Butyric Acid

- Synthetic Butyric Acid

- By Grade

- Food Grade

- Industrial Grade

- Pharmaceutical Grade

- By Application

- Chemical Intermediates

- Animal Feed

- Pharmaceuticals

- Perfumes

- Food and Flavors

- Other Applications (Biofuel, Cosmetics, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed animal-nutrition formulators across China, Germany, and Brazil, specialty chemical distributors in the US Gulf Coast, and fermentation technology suppliers in Japan. These dialogues clarified typical inclusion rates, current average selling prices (ASP), utilization levels at new bio-based plants, and regional demand triggers. Findings were looped back into the desk-research grid to close data gaps.

Desk Research

We began with production and trade statistics from UN Comtrade, FAO feed balance sheets, and Eurostat PRODCOM to map supply flows and end-use footprints. Process economics and capacity data were pulled from USITC propylene reports, Asia Metal refinery bulletins, and company 10-Ks. These were then sanity-checked against patent families in Questel and news archives in Dow Jones Factiva. Regulatory context, such as the EU ban on growth-promoter antibiotics, came from EFSA and USDA GAIN notices. The listings above illustrate, but do not exhaust, the secondary sources mined for trend lines and base metrics.

Market-Sizing & Forecasting

A top-down capacity-utilization build starts with nameplate synthetic and renewable output by plant, subtracts captive use, and matches the balance against verified trade plus modeled domestic demand pools. We corroborate results with bottom-up signals such as sampled ASP × volume from channel checks and feed-mill inclusion audits, adjusting totals where variances exceed 7 %. Key variables include global broiler and swine feed tonnage, propylene feedstock prices, fermentation yield improvements, average inclusion rates in antibiotic-free diets, and regulatory milestone dates. A multivariate regression links these drivers to historic uptake. Scenario analysis then extends forecasts to 2030. Gaps where supplier roll-ups are opaque are bridged using regional import parity pricing and three-year moving-average ASPs.

Data Validation & Update Cycle

Outputs pass a two-step peer review, followed by variance checks against independent price dashboards and customs tallies. Reports refresh annually; interim updates are triggered by >=10 % capacity additions, material policy shifts, or ASP swings beyond one standard deviation. A final analyst pass occurs before each client delivery.

Why Our Butyric Acid Baseline Earns Industry Trust

Published figures often diverge because firms pick dissimilar chemical scopes, ASP assumptions, and refresh cadences.

According to Mordor Intelligence, we stick to neat butyric acid only, report the first fully post-pandemic year (2025), and blend volume with live ASP inputs. Others fold in derivatives, apply constant prices, or anchor older base years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 54.98 KT (2025) | Mordor Intelligence | - |

| USD 317 M (2022) | Global Consultancy A | Includes isobutyric acid and derivatives; outdated base year; no primary validation |

| USD 422 M (2025) | Trade Journal B | Uses constant ASPs across regions; omits pharmaceutical uptake |

| USD 263 M (2024) | Regional Consultancy C | Excludes China and India demand; single-source desk research |

These contrasts show why our carefully delimited scope, blended price-volume model, and yearly refresh provide decision-makers with the most balanced, reproducible benchmark available.

Key Questions Answered in the Report

How big is the butyric acid market in 2026?

How big is the butyric acid market in 2026?

Which segment grows fastest through 2031?

Which segment grows fastest through 2031?

What drives renewable butyric acid capacity?

What drives renewable butyric acid capacity?

Why is pharmaceutical-grade butyric acid important?

Why is pharmaceutical-grade butyric acid important?

Which region leads consumption?

Which region leads consumption?

Page last updated on: