Paint Remover Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.11 Billion |

| Growth Rate (2026 - 2031) | 5.93% CAGR |

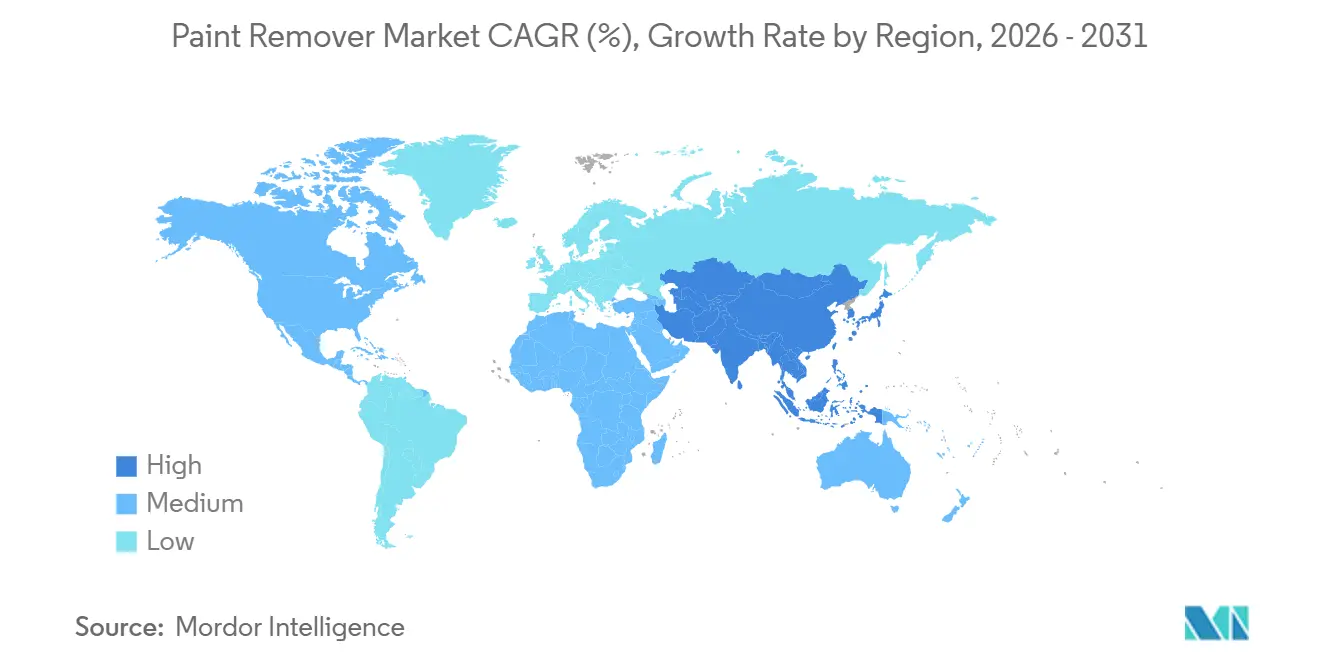

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

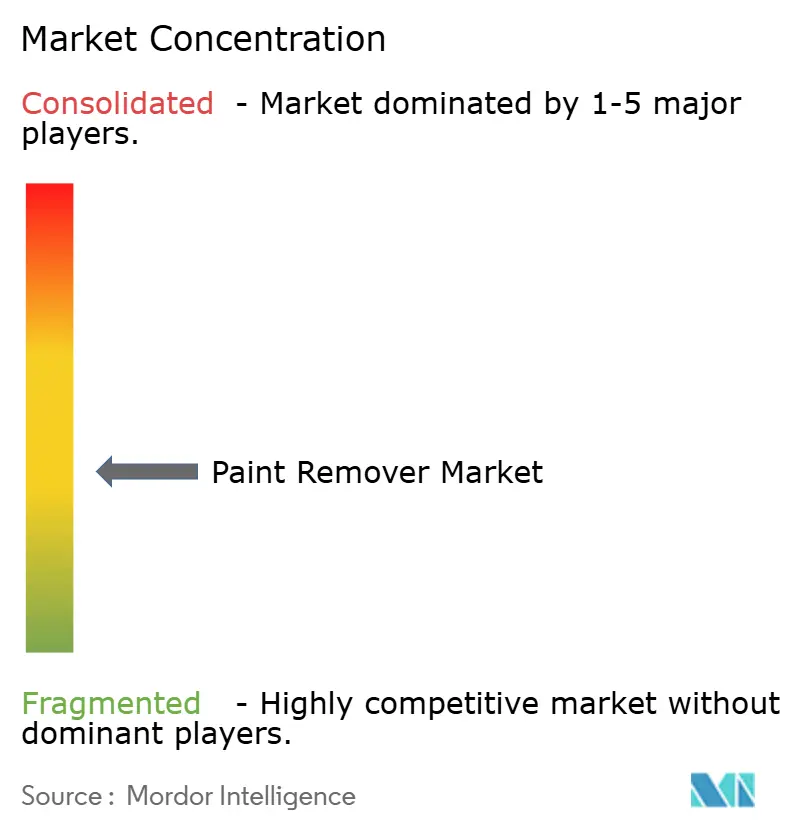

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paint Remover Market Analysis by Mordor Intelligence

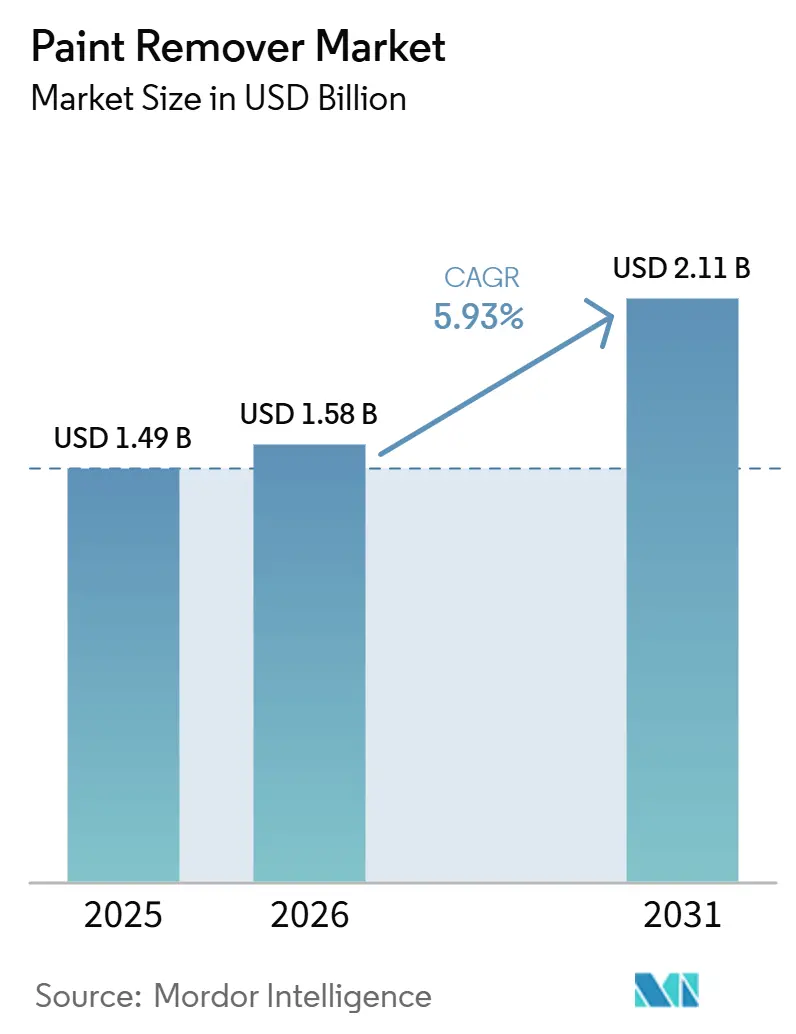

The Paint Remover Market size is expected to grow from USD 1.49 billion in 2025 to USD 1.58 billion in 2026 and is forecast to reach USD 2.11 billion by 2031 at 5.93% CAGR over 2026-2031. Increasing regulatory scrutiny on methylene chloride is driving a transition toward bio-based and caustic alternatives. This shift is creating opportunities for suppliers who can demonstrate low-VOC performance. As electric vehicles require more delicate, water-washable gels, demand from automotive collision-repair shops is rising. Additionally, renovation activities in China and North America are supporting consistent volumes of strippers for building maintenance. In the aerospace MRO sector, hybrid laser-chemical systems are being adopted, but their high capital requirements ensure that chemical consumables maintain a significant role throughout the forecast period. Asia-Pacific, currently leading in revenue, is also experiencing the fastest growth through 2031, supported by housing upgrades and recovery in automotive production.

Key Report Takeaways

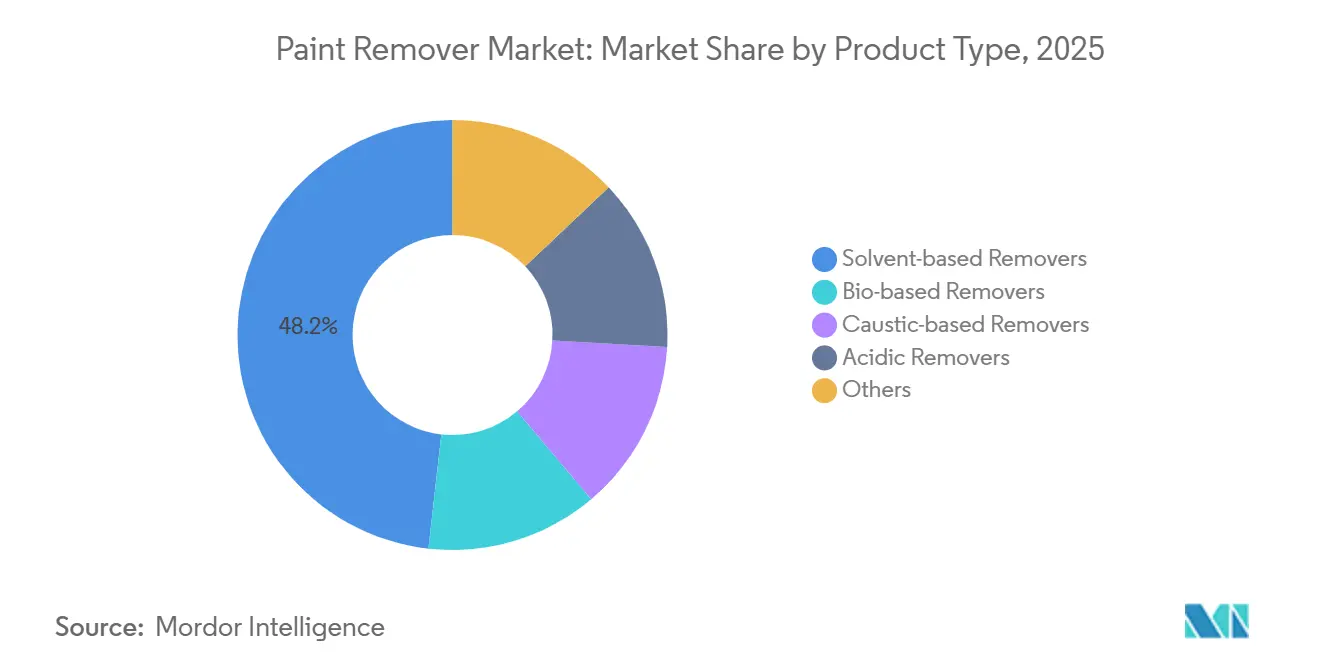

- By product type, solvent-based removers led with 48.22 % of the Paint Remover market share in 2025; bio-based removers are projected to expand at a 6.44 % CAGR from 2026 to 2031.

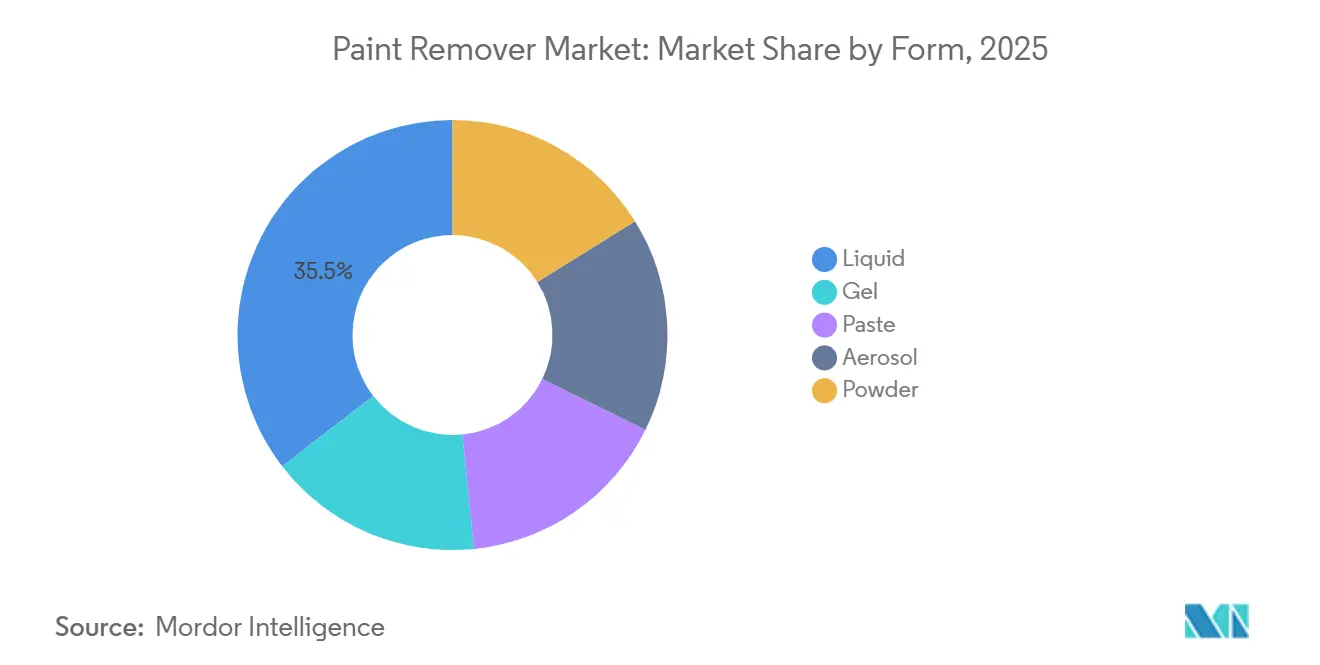

- By form, liquid products held 35.45 % of the Paint Remover market size in 2025, while paste formulations are anticipated to rise at a 6.47 % CAGR from 2026 to 2031.

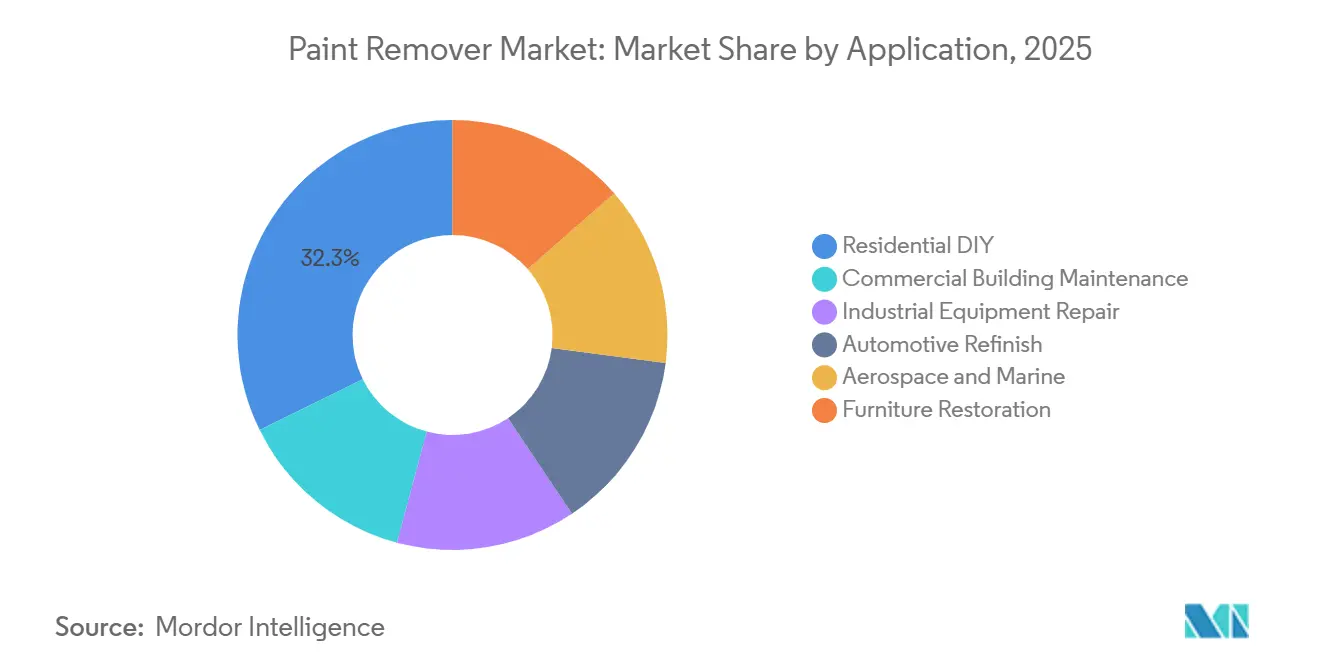

- By application, residential DIY accounted for 32.29 % of 2025 demand, whereas automotive refinish is advancing at a 6.49 % CAGR from 2026 to 2031.

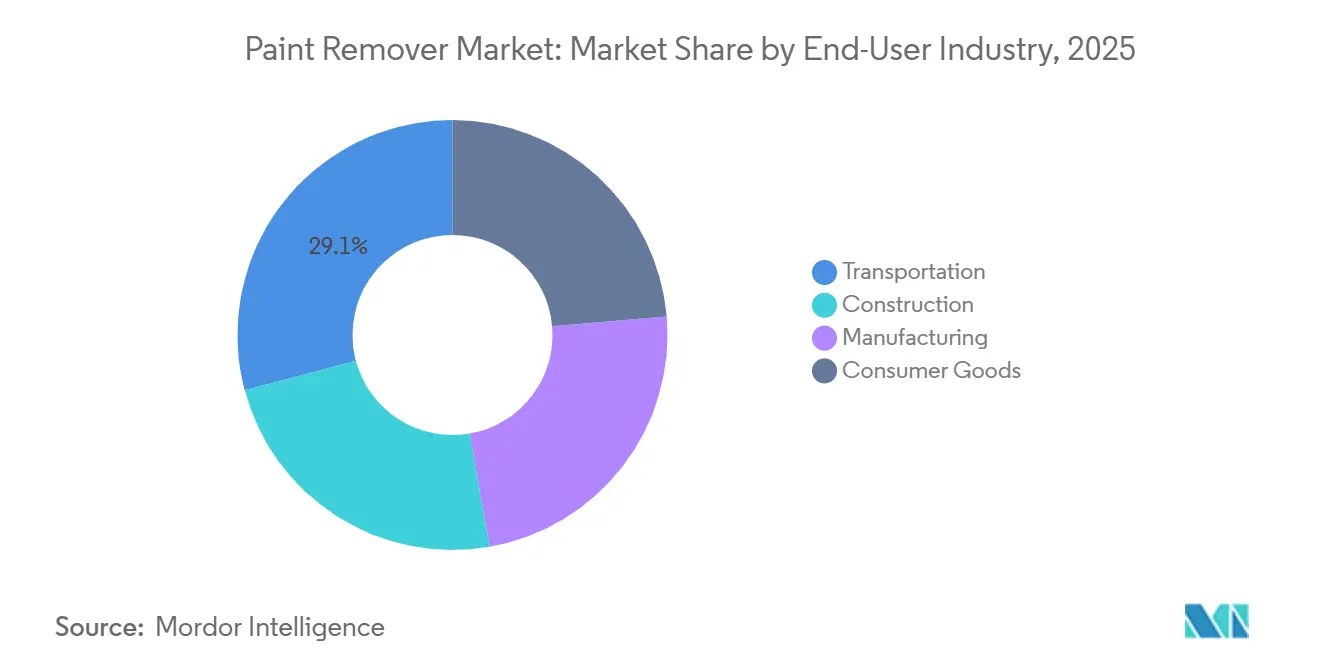

- By end-user industry, transportation dominated with 29.13 % share in 2025; consumer-goods demand is set to climb at a 6.11 % CAGR from 2026 to 2031.

- By geography, Asia-Pacific commanded 44.28 % of 2025 revenue and is on track for a 6.93 % CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Paint Remover Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on methylene chloride | +1.8% | North America & EU, spillover to APAC hubs | Short term (≤ 2 years) |

| Renovation and remodeling boom | +1.5% | Global, centered on North America and China | Medium term (2-4 years) |

| Automotive refinish demand | +1.2% | APAC core, North America collision centers | Medium term (2-4 years) |

| Aerospace and marine refurbishment | +0.9% | North America, EU, Middle East hubs | Long term (≥ 4 years) |

| Hybrid laser-chemical systems adoption | +0.5% | North America & EU aerospace OEMs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans on Methylene Chloride

In May 2024, the EPA announced a rule to phase out consumer use of methylene chloride by May 2025, with most commercial applications to follow by April 2026[1]EPA, “EPA Takes Final Steps to Protect People from Methylene Chloride,” epa.gov. This regulation is driving formulators to explore alternatives such as soy methyl ester, d-limonene, and caustic blends. Companies maintaining certain limited exempted uses are required to implement engineering controls and real-time air monitoring, which is projected to increase compliance costs by approximately 15-20%. Litigation in the Fifth Circuit, reopened in early 2026, has introduced delays in some bio-based capacity investments. Furthermore, the FDA's related action against the solvent in food processing indicates a broader federal shift, prompting faster substitution within coatings value chains.

Renovation and Remodeling Boom

China plans to upgrade 53,000 aging urban residential complexes, with initiatives to strip and repaint extensive facade areas by 2028. In the U.S., Harvard’s Joint Center for Housing Studies anticipates remodeling expenditures to remain steady through 2026, driven by an aging housing stock exceeding 40 years. Maintenance budgets in commercial buildings are increasing to comply with green-building certifications, which require the use of low-VOC, biodegradable strippers. Additionally, the growing interest in furniture restoration, influenced by social media trends, is driving demand for gel and paste products considered safer for indoor use.

Automotive Refinish Demand

Body shops are increasingly using prolonged-dwell gel removers to prevent substrate warping, as electric-vehicle architectures restrict bake-oven temperatures to 80 °C. India's vehicle parc is projected to reach 40 million units in 2025, which is expected to drive repaint cycles due to the rising average vehicle age. The complexities of multi-material joining and selective stripping are supporting the adoption of pH-neutral, thixotropic gels. Furthermore, the global transition toward water-based basecoats is driving the demand for chemical stripping. This trend is due to the higher adhesion strength of water-based basecoats compared to solvent-borne paints, resulting in greater chemical usage per repair job.

Aerospace and Marine Refurbishment

International Aerospace Coatings plans to add 32 paint lines by Q3 2026, addressing the need for airline livery refreshes and drag-reduction topcoats. Gel strippers approved by Boeing and Airbus continue to be widely used, as they adhere effectively to vertical fuselage surfaces and prevent aluminum etch. Marine operators are focusing on extending vessel life cycles through mid-life upgrades rather than investing in new builds, which sustains the demand for chemical anti-fouling coating removal. Although laser stripping trials indicate potential, their costs remain a limiting factor for adoption in most shipyards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VOC limits constrain solvents | -0.7% | California, U.S. Northeast, EU zones | Short term (≤ 2 years) |

| Health-liability litigation | -0.5% | North America, EU under REACH | Medium term (2-4 years) |

| Rise of mechanical and laser stripping | -0.4% | North America & EU aerospace | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

VOC Limits Constrain Solvents

California's South Coast Air Quality Management District has implemented a cap on paint-remover VOC content at 50 g/L, restricting the use of traditional methylene chloride and N-methyl-pyrrolidone blends. Similar regulations in the U.S. Northeast and under the EU's Industrial Emissions rules are driving reformulation efforts toward acetone, dimethyl carbonate, or water-based systems. These alternatives, however, are priced 20-30% higher on a per-gallon basis. Suppliers are encountering longer R&D cycles, while national distributors are managing a broader range of SKUs to comply with varying regulations, which is increasing logistics costs.

Health-Liability Litigation

A report from Frontiers in Pharmacology in 2024 highlighted cardiac arrest incidents tied to dichloromethane exposure, raising concerns over solvent safety[2]Frontiers in Pharmacology, “Dichloromethane Toxicity Case Report,” frontiersin.org. Between 1980 and 2018, 85 fatalities associated with the solvent support plaintiff claims for a mass-tort action, drawing comparisons to past asbestos cases. The Supreme Court's Loper Bright ruling, which removes Chevron deference, prompts courts to reassess EPA methodologies, potentially slowing enforcement actions. As a result, insurers are limiting coverage, and smaller formulators are reconsidering the inclusion of dichloromethane in their portfolios due to increasing liability premiums.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bio-Based Gains Outpace Legacy Solvents

In 2025, solvent-based products accounted for 48.22% of the revenue share. However, increasing compliance costs and a shift in consumer preference toward low-odor profiles are driving demand for bio-based alternatives, which are growing at an annual rate of 6.44%. Within the bio-based segment, products such as soy-methyl-ester gels are gaining traction in e-commerce channels. These products meet state VOC regulations while maintaining effective dwell-time performance. Caustic products continue to be widely used in the heavy industrial stripping segment due to their high pH, which facilitates rapid film breakdown. However, rising disposal fees for corrosive sludge present a challenge. Enzymatic formulations occupy a niche in the heritage conservation segment, as their extended dwell times help prevent substrate damage while avoiding VOC and toxicity concerns.

Second-generation solvent lines, which incorporate acetone or dimethyl carbonate with proprietary surfactants, face challenges related to higher raw material costs that narrow profit margins. In contrast, bio-based feedstocks derived from soy and citrus benefit from agricultural subsidies in several regions. Regulatory exemptions under the EPA rule and EU REACH provide opportunities for plant-derived solvents to increase their market share. However, the supply of d-limonene remains vulnerable to fluctuations in citrus crop yields.

By Form: Paste Products Climb on Vertical-Surface Demand

In 2025, liquids represented 35.45% of the revenue, primarily due to their suitability for automated spray or dip operations that require low viscosity and quick rinse-off. Between now and 2031, paste and gel variants are expected to grow at a rate of 6.47%, driven by demand from aerospace, marine, and residential DIY sectors for non-sag rheology that adheres to vertical panels. Thixotropic modifiers contribute to increased film thickness, extended contact duration, and reduced labor hours per square meter. Manuals from aerospace manufacturers such as Boeing and Airbus are specifying gel strippers to address VOC emissions in enclosed hangars, leading MRO depots to include paste SKUs alongside liquids.

Aerosols are used for spot repairs but face challenges due to propellant restrictions, which increase manufacturing costs by 10-15%. Powders remain a limited option in industrial applications, where on-site concentrate mixing helps reduce freight costs but requires operator training. Paste sludge is simpler to handle and poses a lower spill risk, aligning with OSHA safety audits that address liquid splash incidents.

By Application: Automotive Refinish Accelerates Amid EV Transition

In 2025, residential DIY projects contributed 32.29% of the revenue, supported by increased home-improvement activities and the growing popularity of furniture restoration trends on social media. The automotive refinish segment is experiencing notable growth, with a 6.49% CAGR. This growth is driven by collision centers adapting to the requirements of aluminum and composite body repairs, which involve the use of gentle, water-washable gels. Thermal limitations in electric vehicle (EV) batteries have increased the importance of extended-dwell paste strippers. The commercial building maintenance segment maintains stable demand, primarily due to facade repaint cycles and graffiti removal programs in urban areas.

In industrial equipment repair, solvent liquidity is valued for enhancing dip-tank throughput. However, VOC regulations are prompting some facilities to shift toward enclosed spray booths with solvent-recovery systems. The aerospace and marine segments, although smaller in volume, achieve higher pricing due to the need for formulations that meet multi-year approvals from OEMs and the International Maritime Organization (IMO). In the furniture restoration segment, low-odor gels are gaining acceptance. These gels help preserve the wood's grain and patina while creating additional revenue opportunities for consumer brands.

By End-User Industry: Consumer Goods Segment Gains Momentum

Transportation, which contributed 29.13% of 2025 revenue, is expected to remain a significant segment of the paint remover market through 2031. This is primarily due to the global vehicle and aircraft fleets requiring regular maintenance cycles. The consumer goods segment is projected to grow at a 6.11% CAGR, driven by furniture, appliances, and sports equipment manufacturers adopting refurbishment programs aligned with circular-economy policies. In the construction segment, strippers are used for renovation activities, lead-paint abatement, and graffiti removal. Demand in this segment is closely linked to public-works spending and private building permits.

In the manufacturing segment, strippers are applied to rework defective components and clean tools. However, lean production practices and increased automation are moderating consumption growth. In the EU, extended producer responsibility schemes are increasing the volume of returned products for refurbishment, expanding the customer base for low-odor gel removers.

Geography Analysis

In 2025, the Asia-Pacific region represented 44.28% of global revenue and is expected to grow at a rate of 6.93% through 2031. This growth is attributed to residential upgrades in China and the increasing vehicle parc in India. Japan's industrial sector is advancing thermal-decomposition services to align with chemical consumption. In South Korea, shipyards are driving demand for marine strippers during hull refurbishments. Southeast Asian countries are increasing budgets for building upgrades, while local suppliers are utilizing palm-oil feedstocks to develop bio-based gels.

In North America, regulatory changes, such as the EPA's ban on methylene chloride, are driving portfolio turnover. California's 50 g/L VOC cap is altering the product landscape, with similar restrictions being implemented in Northeastern states. Residential repair spending remains significant due to the median age of U.S. homes exceeding 40 years. Aerospace MRO capacity expansions are contributing to higher demand for gel volumes. Canada and Mexico are addressing cross-border demand from automotive production, although potential tariff risks on imported specialty chemicals remain a concern.

In Europe, the Industrial Emissions Directive and REACH authorizations are accelerating the shift away from legacy solvents. Germany is generating refinish consumption from its internal combustion engine vehicle stock. The United Kingdom is increasing commercial maintenance activities through infrastructure programs. In France and Italy, heritage restorations are favoring pH-neutral gels. Spain's tourism sector is maintaining hotel repaint cycles, while Eastern Europe is seeing moderate growth tied to industrial upgrades. In South America, Brazil is the primary market for demand, with currency fluctuations influencing sourcing strategies. The Middle East is experiencing growth from infrastructure projects in Saudi Arabia, although logistical challenges persist in sub-Saharan Africa.

Competitive Landscape

The market for Paint Remover is fragmented in nature. The top 5 companies in the market includes 3M, Sherwin-Williams Company, Akzo Nobel N.V., Henkel AG & Co. KGaA, Jasco. Market fragmentation remains evident as the top five suppliers account for less than half of global revenue. This creates opportunities for regional specialists and private-label brands to expand through e-commerce and contractor loyalty programs. AkzoNobel and Axalta announced a merger in November 2025, finalizing a USD 25 billion deal aimed at achieving USD 600 million in synergies across their architectural and refinish lines. BASF is preparing to complete a EUR 7.7 billion acquisition of Carlyle’s automotive coatings assets in Q2 2026, which will enable cross-sales of strippers with OEM primers.

Technology advancements are shaping competitive dynamics. In February 2025, 3M and General Motors introduced a robotic paint-repair cell that integrates automated stripping and recoating, reducing line rework time and demonstrating the potential of factory-floor automation. Hempel invested EUR 19 million in a Jeddah plant, increasing its annual capacity by 32 million liters to meet the needs of the Middle East construction sector. Niche brands such as Franmar and Citristrip are leveraging their bio-based positioning to attract DIY consumers online. Equipment manufacturers are testing lease programs for mobile hybrid laser rigs, aiming to lower adoption costs for mid-sized MRO shops.

Competitive pressures are pronounced in North America and Europe, where regulatory changes benefit suppliers offering field-validated bio-based and caustic formulas. In the Asia-Pacific region, local producers are using lower feedstock costs to offer more competitive pricing, particularly in small-contractor and residential markets. Plasma-based and enzymatic technologies, while currently limited by high costs and slow throughput, could disrupt the market if scaling challenges are addressed.

Paint Remover Industry Leaders

3M

Akzo Nobel N.V.

The Sherwin-Williams Company

Henkel AG & Co. KGaA

Jasco

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: AkzoNobel and Axalta Coating Systems have announced an all-stock merger of equals, creating a global coatings company with an enterprise value of roughly USD 25 billion. The deal combines AkzoNobel’s architectural paints with Axalta’s refinish and mobility coatings, targeting USD 600 million in annual cost synergies, with 90% expected within three years.

- March 2025: 3M and General Motors deployed a robotic paint-repair cell at the Spring Hill, Tennessee plant to automate stripping and recoating.

Global Paint Remover Market Report Scope

Paint remover is a chemical product designed to break down, dissolve, or lift paint, varnish, and coatings from surfaces like wood, metal, and concrete. It works by weakening the bond between the paint and the substrate, allowing the coating to be easily scraped or wiped away.

The market is segmented by product type, form, application, end-user industry, and geography. By product type, the market is segmented into solvent-based removers, bio-based removers, caustic-based removers, acidic removers, and other product types. By form, the market is segmented into liquid, gel, paste, aerosol, and powder. By application, the market is segmented into residential DIY, commercial building maintenance, industrial equipment repair, automotive refinish, aerospace and marine, and furniture restoration. By end-user industry, the market is segmented into construction, transportation, manufacturing, and consumer goods. The report also covers the market size and forecasts for Paint Remover in 16 countries across the world. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| Solvent-based Removers |

| Bio-based Removers |

| Caustic-based Removers |

| Acidic Removers |

| Others |

| Liquid |

| Gel |

| Paste |

| Aerosol |

| Powder |

| Residential DIY |

| Commercial Building Maintenance |

| Industrial Equipment Repair |

| Automotive Refinish |

| Aerospace and Marine |

| Furniture Restoration |

| Construction |

| Transportation |

| Manufacturing |

| Consumer Goods |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Solvent-based Removers | |

| Bio-based Removers | ||

| Caustic-based Removers | ||

| Acidic Removers | ||

| Others | ||

| By Form | Liquid | |

| Gel | ||

| Paste | ||

| Aerosol | ||

| Powder | ||

| By Application | Residential DIY | |

| Commercial Building Maintenance | ||

| Industrial Equipment Repair | ||

| Automotive Refinish | ||

| Aerospace and Marine | ||

| Furniture Restoration | ||

| By End-user Industry | Construction | |

| Transportation | ||

| Manufacturing | ||

| Consumer Goods | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the paint remover market?

The paint remover market size stands at USD 1.58 billion in 2026 and is forecast to reach USD 2.11 billion by 2031.

How fast will demand grow through 2031?

Revenue is projected to rise at a 5.93% CAGR from 2026 to 2031, led by regulatory-driven formulation shifts and remodeling activity.

Which product type is gaining share fastest?

Bio-based removers are advancing at a 6.44% CAGR as buyers prioritize low-VOC and biodegradable chemistries.

Why is automotive refinish an important application?

Electric-vehicle body materials need low-temperature, water-washable gels, pushing automotive refinish to a 6.49% CAGR through 2031.

How will regulations shape supplier strategy?

The EPA methylene-chloride ban, VOC caps, and EU REACH authorizations are accelerating reformulation toward bio-based or caustic products and favoring suppliers with validated alternatives.

Page last updated on: