Paper Pigment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.71 Billion |

| Market Size (2031) | USD 26.96 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

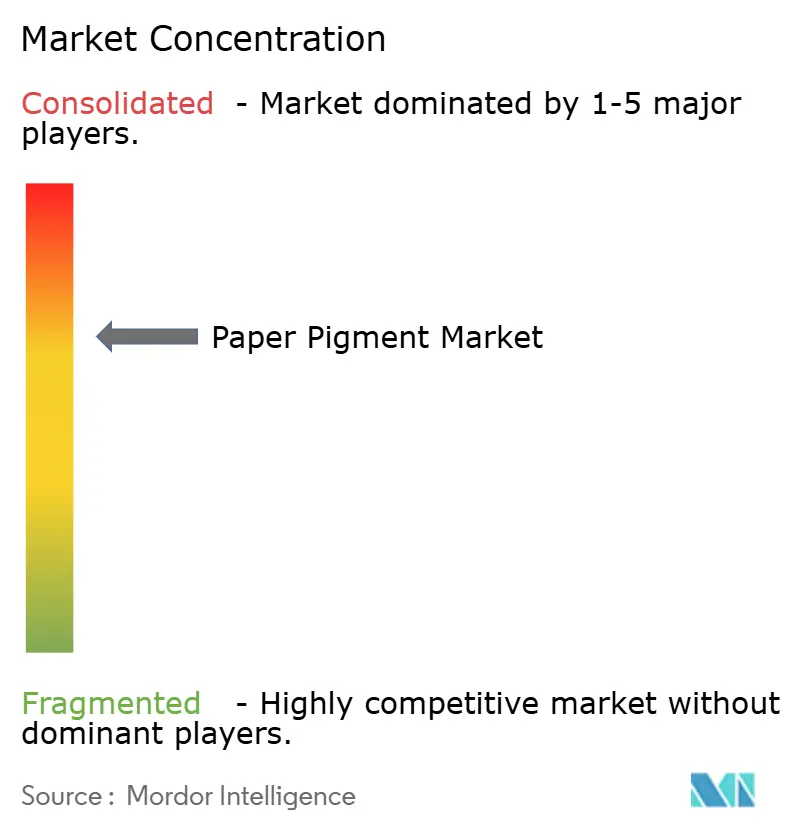

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paper Pigment Market Analysis by Mordor Intelligence

The Paper Pigment Market size was valued at USD 19.65 billion in 2025 and estimated to grow from USD 20.71 billion in 2026 to reach USD 26.96 billion by 2031, at a CAGR of 5.41% during the forecast period (2026-2031). This solid expansion of the paper pigments market reflects manufacturers’ ability to capture value from the surging global packaging segment even as traditional graphic printing wanes. Rising e-commerce volumes, rapid substitution of plastic with paper-based formats, and sustained cost pressure on paper mills are encouraging wider use of calcium carbonate and other cost-efficient fillers. Concurrently, advances in nano-structured and PFAS-free formulations are opening premium niches inside the paper pigments market for functional grades that improve barrier, opacity and hygiene performance. Finally, steady consolidation among pigment suppliers—combined with vertical integration by large mineral processors—supports scale benefits and fosters technology transfer toward low-carbon production.

Key Report Takeaways

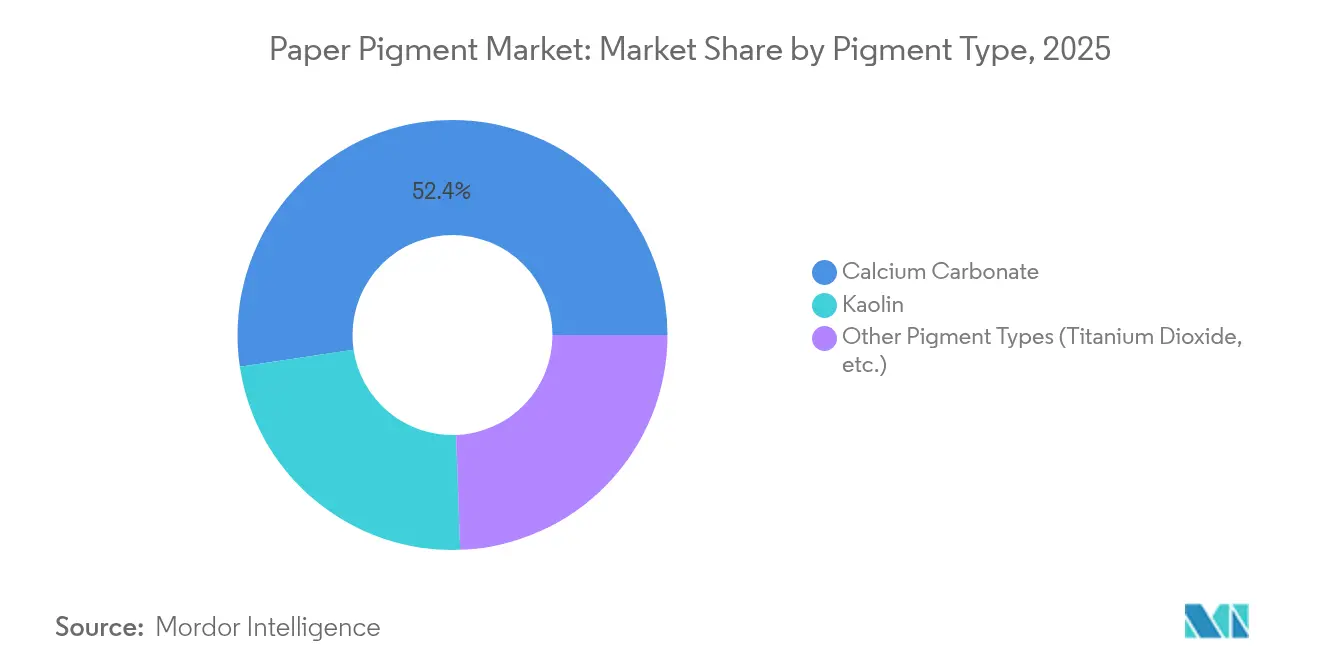

- By pigment type, calcium carbonate held 52.35% of the paper pigments market share in 2025, while the “Other Types” category is projected to grow the fastest at a 6.71% CAGR through 2031.

- By application, coated paper captured 62.55% revenue in 2025; the “Other Applications” segment is set to expand at a 7.34% CAGR to 2031.

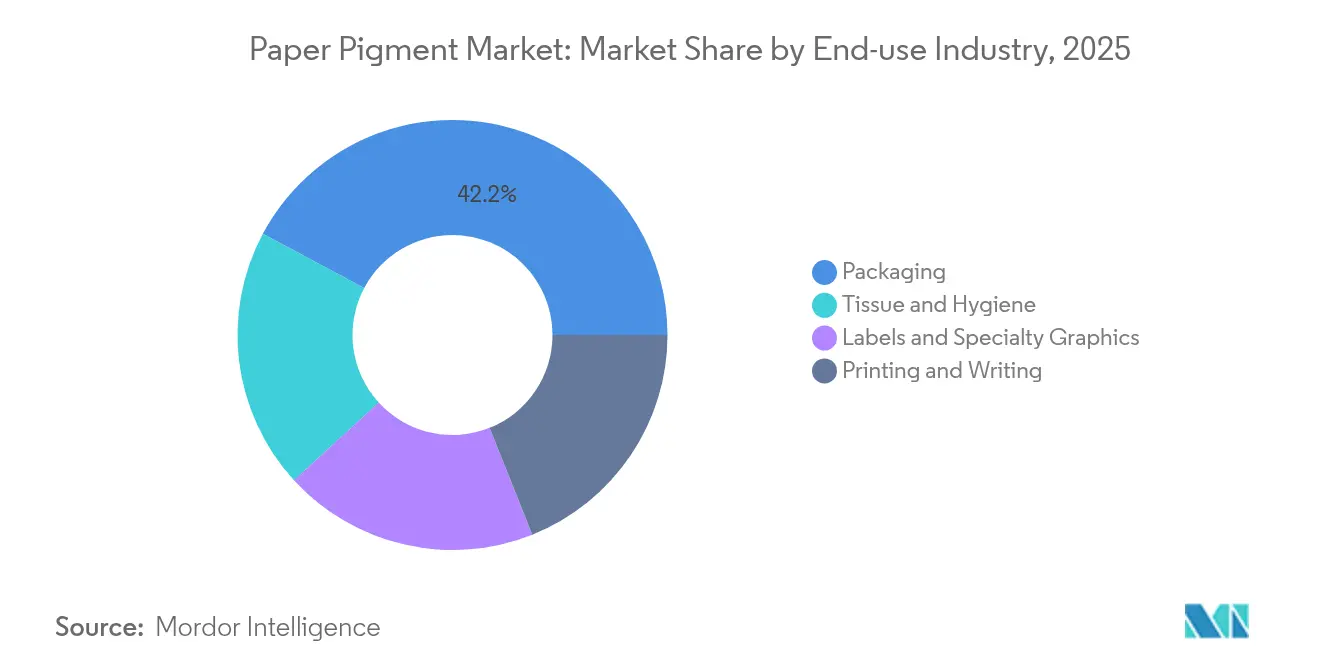

- By end-use industry, packaging accounted for 42.20% of the paper pigments market size in 2025 and is advancing at a 6.75% CAGR during the forecast period.

- By geography, Asia-Pacific led with 44.05% of the paper pigments market share in 2025; the same region is projected to post the highest 6.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paper Pigment Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for paper from the packaging industry | +1.8% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Rising adoption of calcium carbonate fillers to cut production cost | +1.2% | Global, particularly in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Expansion of e-commerce boosting corrugated board output | +1.5% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Increasing consumption of coated & specialty graphic papers | +0.8% | Europe and North America primarily | Long term (≥ 4 years) |

| Nano-structured pigments enabling lighter high-opacity paper | +0.6% | Developed markets with premium applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Paper from the Packaging Industry

Corrugated and folding carton producers now demand pigments that meet printability, brightness and food-contact requirements. Valmet’s OptiConcept M line for Anhui Linping adds 1,808 tonnes per day of recycled linerboard capacity, underscoring the volume pull for pigments that ensure surface uniformity. Brand owners shifting from plastics to fiber packaging rely on highly opaque and migration-safe pigment systems, and BASF’s new water-based dispersion plant in Heerenveen is designed specifically for these substrates[1]BASF, “Heerenveen Water-based Dispersions Expansion,” basf.com. As a result, the paper pigments market is capturing increased tonnage and higher average selling prices in packaging-centric regions.

Rising Adoption of Calcium Carbonate Fillers to Cut Production Cost

Ground and precipitated calcium carbonate can replace titanium dioxide at up to 20 percentage points while preserving brightness, generating immediate margin relief for mills coping with volatile energy charges. Suppliers with captive limestone quarries, such as Imerys and Omya, offer on-site PCC satellite plants that lower logistics costs and help customers to optimize the paper pigments market supply chain. Emerging economies, where converter margins are slimmer, are rapidly pivoting toward GCC-rich formulations, reinforcing calcium carbonate’s dominant share.

Expansion of E-commerce Boosting Corrugated Board Output

Online retail, projected to add roughly 4.4% volume CAGR in printed packaging through 2029, is pushing converters to upgrade graphics on corrugated liners. The shift from brown box to colorful, shelf-ready formats needs pigments that improve ink holdout and dot fidelity. Large packagers such as the combined Smurfit Kappa-WestRock group are harmonizing specifications across a global mill network, giving qualified pigment suppliers sizable long-term contracts.

Increasing Consumption of Coated & Specialty Graphic Papers

Although uncoated printing grades continue to decline, specialty coated papers retain value thanks to catalog, label and luxury print use. Nano-structured titanium dioxide lets producers reach opacity at lower basis weights, cutting fiber cost and reducing transportation emissions. Suppliers that can engineer particle morphology and surface modifications are securing profitable niches within the paper pigments market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitalization reducing demand for printing & writing paper | -2.1% | Developed markets worldwide | Short term (≤ 2 years) |

| Environmental concerns & inadequate recycling infrastructure | -0.9% | Europe and North America | Medium term (2-4 years) |

| Direct-to-package digital printing lowering coating requirements | -1.5% | Global, strongest in packaging-intensive regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digitalization Reducing Demand for Printing & Writing Paper

Digital transformation creates structural headwinds for traditional paper pigment applications, with the US printing industry experiencing 47.3% employment reduction from 2002-2021 as digitalization accelerated [2]International Journal of Technology, “Digitalization and Printing Industry,” ijtech.itb.ac.id. Pigment suppliers built around high-volume offset stocks now face under-utilized plants and must realign toward packaging, tissue or functional papers.

Digitalization Reducing Demand for Printing & Writing Paper

Restrictive PFAS legislation, together with limited pigment recovery in recycling streams, raises compliance costs. Norwegian studies detected up to 971 µg/kg of PFAS in paper products, prompting swift phase-outs across Europe. Clariant’s full PFAS-free portfolio shows the immediate R&D outlay needed to satisfy regulators and brand-owner procurement policies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pigment Type: Calcium Carbonate Dominance Amid Specialty Innovation

Calcium carbonate commanded 52.35% of the paper pigments market in 2025, a share built on its ability to displace high-priced TiO₂ and to double as filler and coating pigment. GCC and PCC variants can cut formulation cost by up to 20%, a critical benefit when energy inflates overall mill expense. The paper pigments market size allocated to calcium carbonate grades is expected to grow in lock-step with new satellite PCC plants coming onstream near Asian board mills.

Meanwhile, the “Other Types” basket—titanium dioxide, kaolin-nano hybrids and emerging bio-based pigments—posts a 6.71% CAGR to 2031. Titanium dioxide remains indispensable in high-grade décor and label stock, yet suppliers add nanotechnology to boost opacity at lower dosages. Specialty players that master surface treatment and dispersion can charge premiums in the paper pigments industry as converters seek lightweight yet vivid sheets.

By Application: Coated Paper Leadership Faces Digital Disruption

Coated papers represented 62.55% of 2025 demand, underscoring pigment intensity where brightness and smoothness are paramount. However, migrating ad budgets and office digitization erode run lengths, compelling mills and pigment vendors to pivot toward premium, shorter-run jobs that tolerate higher pigment spend. The uncoated segment stays price-sensitive, focusing on opacity boosts rather than surface gloss.

Digital printing of labels and folding cartons introduces fresh surface-energy requirements. UV inkjet and electrophotography rely on pigments that anchor ink droplets without excessive absorption, a property now engineered through tailored PCC-kaolin blends. These dynamics sustain a segmented paper pigments market where application dictates formulation complexity.

By End-use Industry: Packaging Sector Drives Growth Momentum

Packaging captured 42.20% revenue in 2025 and rises at 6.75% CAGR to 2031, becoming the backbone of the paper pigments market. Food service, e-commerce and retail makeover campaigns require brighter liners, recyclable barrier coatings and vivid graphics, each pigment-intensive. Major linerboard capacity in China, India and Southeast Asia further underpins regional pigment offtake.

Printing & writing grades, formerly the lion’s share of pigment usage, shrink in absolute terms. Labels, décor and speciality graphics absorb part of the slack through higher unit value and customized color. Tissue and towel grades consume pigments mostly for appearance and softness, giving mineral fillers a niche but steady outlet in the paper pigments industry.

Geography Analysis

Asia-Pacific held 44.05% of the paper pigments market in 2025 and is expanding at a 6.14% CAGR as the region adds board machines and invests in e-commerce-oriented packaging. China’s latest mill upgrades, together with India’s capacity builds, secure long-run volume for PCC and specialty pigments. Suppliers benefit not only from proximity to limestone reserves but also from lower production costs that allow competitive export pricing.

North America remains anchored in packaging and tissue, offsetting graphic decline. Brand sustainability pledges have led converters to phase out plastics in favor of recyclable fiber, leading pigment producers to qualify PFAS-free, migration-safe systems at mills across the United States and Canada. Digital presses for short-run folding cartons and direct-to-corrugate printing require new surface chemistries, prompting collaborative development between pigment suppliers and OEMs.

Europe emphasizes eco-design and carbon-footprint cuts. Despite a 13% fall in paper production during 2023, investment continues in premium barrier coatings and CO₂-optimized mills, such as Smurfit Kappa’s Zülpich upgrade that trims 55,000 tonnes of annual emissions. South America and the Middle East & Africa register smaller bases but above-average growth, supported by mega-pulp projects like ANDRITZ’s 2.55 million-ton Suzano line that boosts pigment demand for high-brightness pulp exports.

Competitive Landscape

The paper pigments market is moderately fragmented, with major players like Imerys, Omya, and Minerals Technologies dominating calcium carbonate and kaolin supply through quarry-to-customer integration and satellite PCC plants, which lower transport costs and ensure quality, creating high entry barriers. Mid-tier companies such as Clariant and BASF focus on functional additives, PFAS-free coatings, and premium nano-structured grades. Larger packaging converters are centralizing procurement, driving suppliers to standardize quality globally and improve logistics. Technology is a key differentiator, with firms investing in VOC-free dispersions, bio-based binders, and antimicrobial pigments, while R&D targets low-carbon PCC, nano-TiO₂ with controlled photoactivity, and hybrid solutions offering barrier and printability. Early commercialization of these innovations could secure significant market share.

Paper Pigment Industry Leaders

Ashapura Group

Omya AG

Minerals Technologies Inc.

Imerys

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: KaMin and Omya AG entered a new agreement to supply kaolin to Europe's packaging and paper market. Omya will continue sales and technical support, while KaMin will manage order processing, logistics, and inventory, strengthening their long-standing partnership to deliver exceptional solutions to customers.

- March 2024: Omya AG announced an increase in prices for its calcium carbonate products in Europe from April 1, 2024, to support sustainability and the Paper & Board sector. Adjustments will vary by product and location, adhering to existing contracts.

Global Paper Pigment Market Report Scope

The paper pigment market report includes:

| Calcium Carbonate |

| Kaolin |

| Other Pigment Types (Titanium Dioxide, etc.) |

| Uncoated Paper |

| Coated Paper |

| Packaging |

| Printing and Writing |

| Labels and Specialty Graphics |

| Tissue and Hygiene |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Malaysia | |

| Philippines | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Pigment Type | Calcium Carbonate | |

| Kaolin | ||

| Other Pigment Types (Titanium Dioxide, etc.) | ||

| By Application | Uncoated Paper | |

| Coated Paper | ||

| By End-use Industry | Packaging | |

| Printing and Writing | ||

| Labels and Specialty Graphics | ||

| Tissue and Hygiene | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the paper pigments market?

The paper pigments market is valued at USD 20.71 billion in 2026.

Which pigment type dominates global demand?

Calcium carbonate leads with 52.35% market share in 2025, owing to its cost and performance advantages.

How fast is the packaging segment growing?

Packaging applications in the paper pigments market are advancing at a 6.75% CAGR through 2031 as e-commerce and plastic substitution accelerate.

What region shows the strongest growth momentum?

Asia-Pacific combines the highest 44.05% share with a leading 6.14% CAGR, supported by board-making capacity expansion.

How are environmental regulations influencing pigment development?

Tighter PFAS and carbon limits push suppliers toward PFAS-free, low-carbon, and nano-structured formulations, reshaping R&D priorities and capital deployment within the industry.

Page last updated on: