Dyes And Pigments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

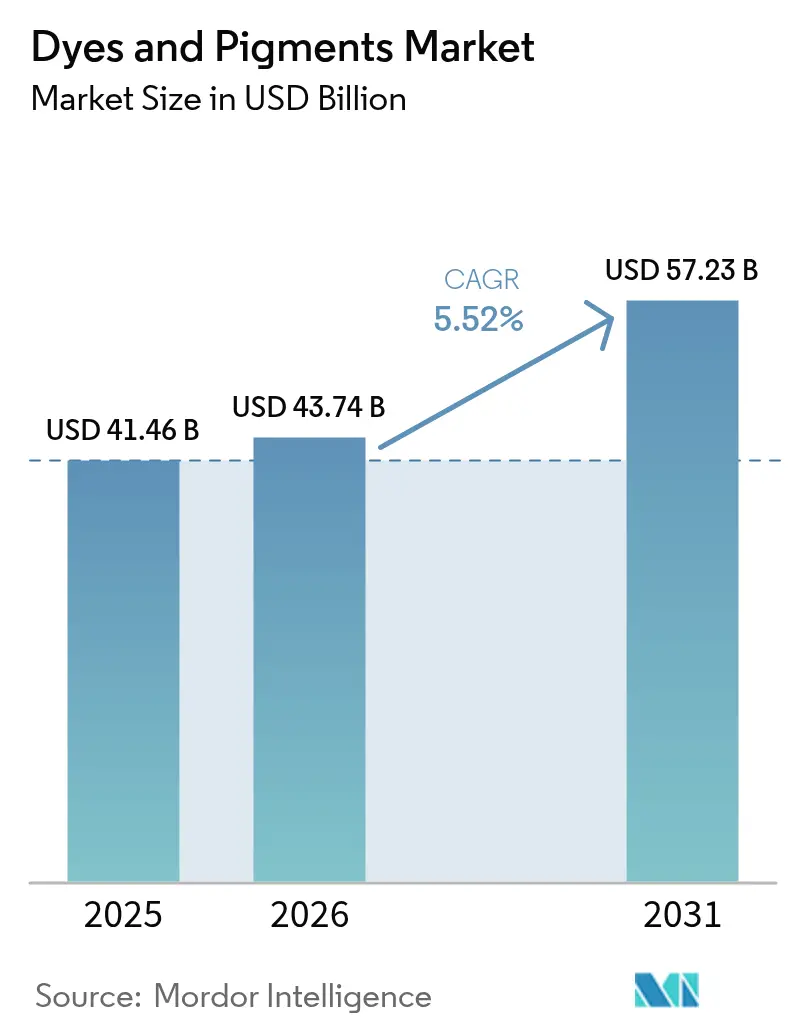

| Market Size (2026) | USD 43.74 Billion |

| Market Size (2031) | USD 57.23 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dyes And Pigments Market Analysis by Mordor Intelligence

The Dyes and Pigments Market size was valued at USD 41.46 billion in 2025 and estimated to grow from USD 43.74 billion in 2026 to reach USD 57.23 billion by 2031, at a CAGR of 5.52% during the forecast period (2026-2031). Strengthening environmental rules, rapid technology adoption in manufacturing, and continuous capacity additions across Asia-Pacific drive this trajectory. Asia-Pacific commands production leadership, underpinned by infrastructure spending that amplifies pigment consumption in paints, coatings, and plastics. Liquid dispersion technologies enable finer particle distribution for 3D printing and waterborne coating systems, strengthening their foothold. Consolidation among key suppliers, exemplified by Sudarshan Chemical’s purchase of Heubach Group, points to portfolio optimization amid raw-material price volatility. Natural colorant commercial viability is still emerging; however, stricter REACH and EPA rules are accelerating research and development around bio-based chemistries that diversify the supply base.

Key Report Takeaways

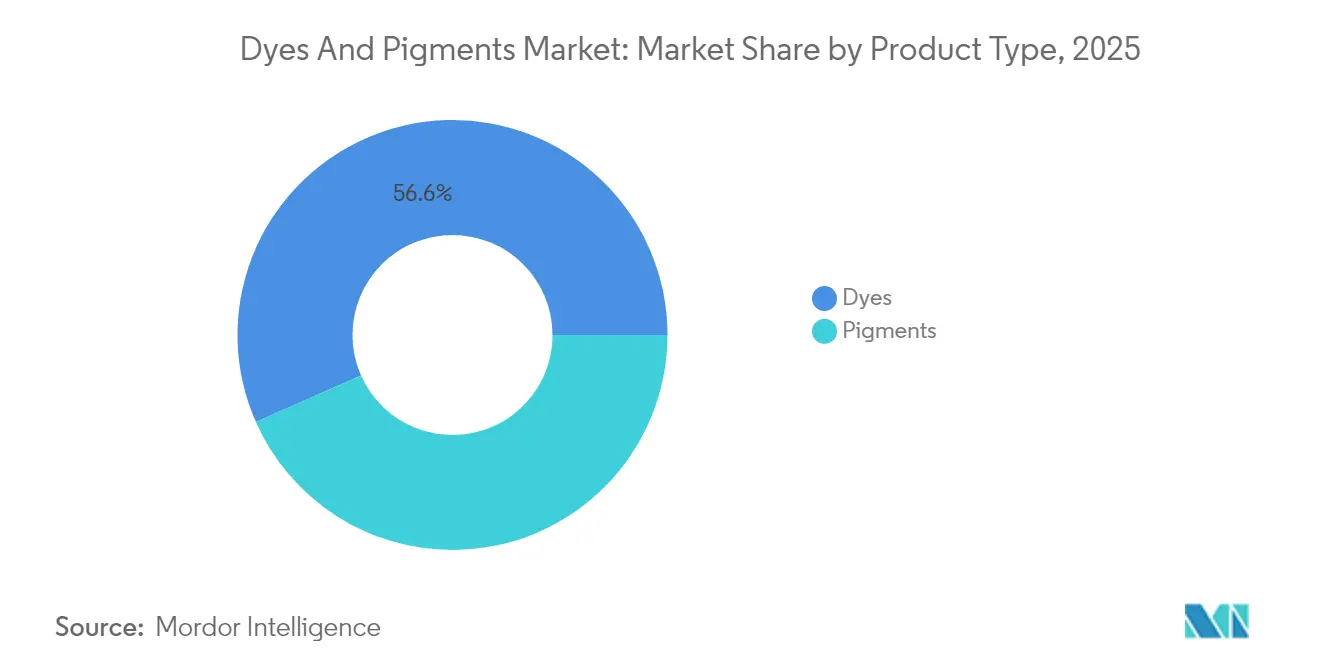

- By product type, dyes led with 56.63% of dyes and pigments market share in 2025, and are expected to record the highest projected CAGR at 5.76% to 2031.

- By source, synthetic colorants accounted for 84.55% of the dyes and pigments market size in 2025, and natural/bio-based are forecast to expand at a 6.74% CAGR through 2031.

- By formulation, liquid dispersions secured 35.68% share of the dyes and pigments market size in 2025 and are rising at a 6.32% CAGR on the back of 3D printing and low-VOC coatings adoption.

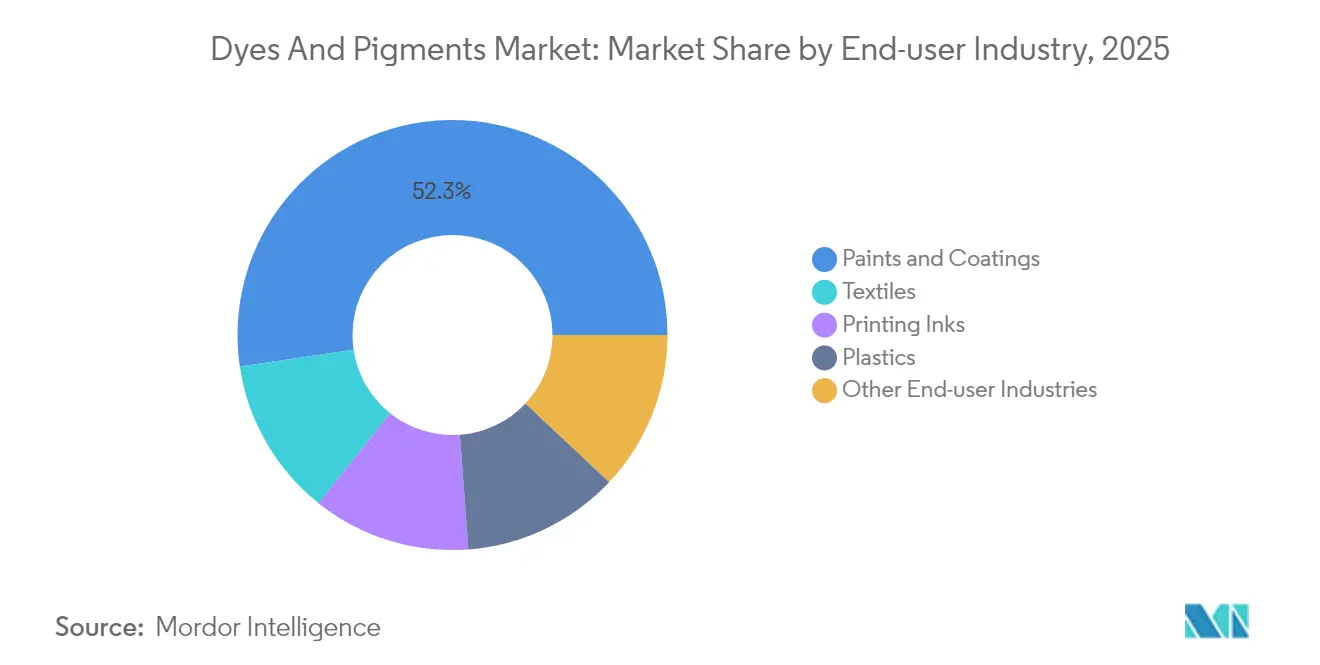

- By end-user industry, paints and coatings commanded 52.34% share of the dyes and pigments market size in 2025 and are advancing at a 5.88% CAGR through 2031.

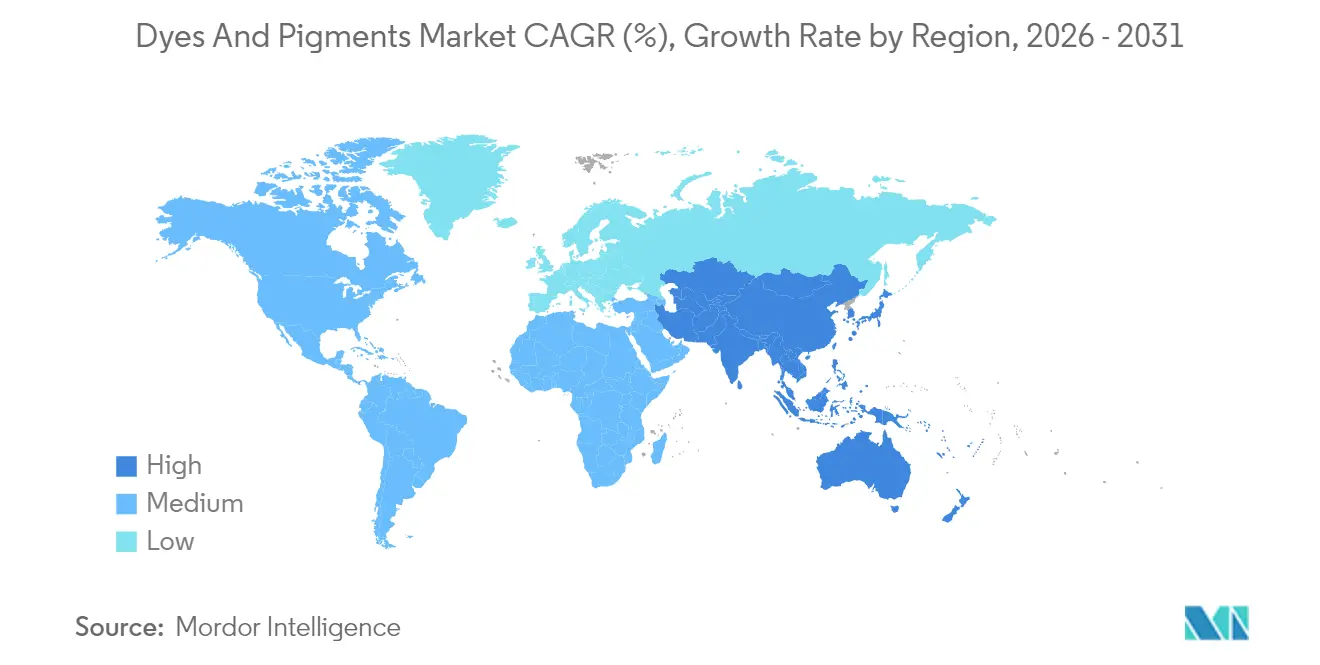

- By geography, Asia-Pacific dominated with 46.88% of the dyes and pigments market share in 2025; the region is also the fastest growing at 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dyes And Pigments Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from paints and coatings in APAC | +1.8% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Expanding textile production | +1.2% | Global, concentrated in APAC | Long term (≥4 years) |

| Infrastructure-led rise in construction pigments | +0.9% | Global, early gains in APAC and MEA | Medium term (2-4 years) |

| Shift toward low-VOC, waterborne formulations | +0.7% | North America and EU, expanding globally | Short term (≤2 years) |

| Adoption of dye-infused filaments for additive manufacturing | +0.4% | North America and EU, tech hubs in APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Paints and Coatings in APAC

Asia-Pacific infrastructure pipelines are propelling titanium dioxide and iron oxide pigment volumes in architectural and protective coatings. Regional policy initiatives that prioritize waterborne formulations, such as China’s 2035 low-carbon guideline, accelerate substitutions away from solvent-borne dispersions. LANXESS expanded iron-oxide capacities and published Environmental Product Declarations that help specifiers meet ecolabel requirements. Multinational paint makers partner with regional formulators to localize color standards, ensuring regulatory alignment and faster market entry.

Expanding Textile Production

Textile capacity additions in China, India, and Vietnam are reshaping demand for reactive and disperse dyes, particularly for technical textiles with moisture-management and antimicrobial finishes. India targets USD 45 billion in textile exports by 2025, encouraging mills to adopt digital printing platforms that cut water consumption and broaden color gamut. Archroma’s acquisition of Huntsman Textile Effects merged 5,000 employees across 42 countries, creating a portfolio that combines high-performance dyes with sustainability certifications. Circularity initiatives, including dye reclamation systems and Cold Pad-Batch processing, are gaining traction as fast-fashion brands disclose environmental footprints. Research into energy-saving dyeing routes for ramie and cotton fabrics continues to improve levelness and fixation rates.

Infrastructure-Led Rise in Construction Pigments

Megaprojects in transport, utilities, and housing elevate demand for durable inorganic pigments that withstand ultraviolet exposure and alkaline cement environments. Calcined clay technologies yield natural mineral pigments with enhanced chroma and low embodied carbon, aligning with green-building codes. The USGS lists China, Germany, Brazil, and Canada as leading iron oxide suppliers to the USA, underscoring import diversification strategies[1]USGS, “Mineral Commodity Summary Iron Oxide Pigments,” usgs.gov. Nanopigments for roofing exhibit cool-color performance that lowers surface temperatures and supports building-energy codes. Water-based roof-tile coatings containing iron oxides meet emerging VOC thresholds, further anchoring inorganic pigment demand in construction.

Shift Toward Low-VOC, Water-Borne Formulations

VOC caps under the US National Architectural Coatings rule are triggering a shift to water-borne binder systems that demand finely milled, surface-treated pigments for stability at high pH. DIC introduced VOC-free aluminum pigments tailored for latex paints, delivering metallic aesthetics without solvent carriers. Lubrizol commercialized aqueous dispersants that improve viscosity control in highly filled systems, mitigating sedimentation during storage. Adoption of water-borne dispersions enables manufacturers to meet Ecolabel criteria and access procurement incentives in EU member states. Companies with robust dispersion technologies gain a first-mover edge as retrofit conversions of solvent lines incur lengthy validation timelines.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent REACH and EPA restrictions on heavy-metal pigments | -1.4% | Global, most severe in the EU and North America | Short term (≤2 years) |

| Volatile crude-derived feedstock prices | -0.8% | Global, acute in import-dependent regions | Medium term (2-4 years) |

| Ban on certain azo dyes in children's apparel | -0.3% | Global, strictest in the EU and North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent REACH and EPA Restrictions on Heavy-Metal Pigments

Cadmium, chromium VI, and lead compounds face near-zero tolerance in coatings and plastics, with REACH limiting cadmium in polymer matrices to 0.01 wt%. Tattoo-ink rules effective in 2024 widened the scope to more than 4,000 substances, including phthalocyanine Blue 15 and Green 7, pushing formulators to explore organic alternatives[2]European Chemicals Agency, “Cadmium Restrictions under REACH,” ecomundo.eu. The US Modernization of Cosmetics Regulation Act grants the FDA the ability to request safety data and recall pigment-containing products, elevating compliance costs. Companies holding portfolios of chromium-free yellows or bismuth vanadate substitutes are gaining share in regulated markets. Heavy-metal pigment producers confront shrinking volumes and margin compression as markets pivot to safer chemistries.

Volatile Crude-Derived Feedstock Prices

Crude oil volatility directly influences benzene and naphthalene costs, representing up to 70% of synthetic dye raw-material expenditure. Synthesia cited energy and logistics surcharges when raising organic pigment prices in 2021, illustrating feedstock exposure. Cotton doubled in price since 2020, while polyester fiber prices have also increased, pressuring textile margin structures that cascade to dyestuff orders. Printing-ink majors, including Sun Chemical and DuPont, implemented double-digit price hikes to offset raw-material shortages. Producers are evaluating biomass-based aromatic precursors and waste-derived solvents as hedges against petrochemical volatility, though commercialization timelines remain uncertain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dyes Dominate Market Dynamics

Dyes control 56.63% of the global dyes and pigments market in 2025 and will advance at 5.76% CAGR to 2031, fueled by penetrating textile, leather, and paper workflows that need molecular-level color dispersion. Reactive dyes dominate cotton and ramie applications due to strong covalent bonding, supporting e-commerce demand for vibrant apparel. Azo dye proliferation is now curbed in children’s wear, with Danish rules capping aromatic amines at 0.003 wt%.

The dyes subsegment showcases a widening specialty range, from fluorescent optical brighteners to near-infrared absorbers for laser-markable plastics. Meanwhile, pigments keep gaining ground in functional coatings that demand corrosion resistance or thermal control. Technological barriers between the two categories blur as nano-engineered hybrid colorants deliver soluble-like brilliance with pigment-level lightfastness. Brands pursuing cradle-to-cradle certification gravitate toward metal-free recipes, stimulating cross-disciplinary innovation.

By Source: Synthetic Maintains Industrial Supremacy

Synthetic colorants represented 84.55% of total volume in 2025 and continue to lead due to predictable shade strength, wide color coverage, and cost efficiency. Petroleum-based intermediates support high-scale production that meets just-in-time logistics for fast-fashion and packaging converters. Natural alternatives grow at a 6.74% CAGR, buoyed by consumer preference for clean labels and regulatory incentives.

Microbial fermentation advances enable production of betalains and carotenoids from waste glycerol, enhancing supply security. Synthetic producers are hedging with renewable routes, investing in bio-aromatics derived from lignocellulose. Pilot lines for bio-based indigo and anthraquinone intermediates are entering validation stages. Stakeholders anticipate carbon-border adjustment mechanisms in the EU that could penalize high-footprint imports, making low-carbon synthetic routes financially attractive.

By Formulation: Liquid Dispersion Drives Innovation

Liquid dispersions held 35.68% of 2025 sales and are on track for a 6.32% CAGR, outperforming powders and granules. Superior wetting and deagglomeration enable consistent color development in waterborne systems, making them the preferred format for low-VOC paints. Dye-infused filaments rely on liquid masterbatches to secure homogenous color without post-process painting, streamlining 3D printing workflows. Technological advances in bead-milling and inline monitoring raise yield and lower energy consumption in dispersion plants, amplifying the sustainability profile of liquid forms.

Regulatory pushes for zero-solvent stains and inks accentuate liquid dispersion relevance. Manufacturers leverage rheology modifiers to attain spray-ready viscosities while maintaining sag resistance on vertical surfaces. Smart inks embed conductive or thermochromic particles, expanding application horizons in IoT devices and aerospace interiors.

By End-user Industry: Paints Coatings Lead Demand

Paints and coatings accounted for 52.34% of 2025 demand and should register a steady 5.88% CAGR to 2031, energized by government-backed infrastructure rollouts and renovation cycles in mature economies. BASF’s Refinity cloud suite captures precise color data with handheld spectrophotometers, minimizing mismatches and paint waste for automotive refinishing.

Plastics benefit from lightweighting in automotive exteriors and consumer electronics casings, though legacy cadmium-based reds face replacement pressure. Construction materials are pivoting to inorganic pigment blends that satisfy solar reflectance index targets for green roofs. Cosmetics are shifting to nature-derived pigments to meet clean beauty claims, while still demanding high chroma and sensory aesthetics.

Geography Analysis

Asia-Pacific dominates the dyes and pigments market, holding 46.88% share in 2025 and expanding at 6.05% CAGR through 2031. China’s program to reach 70% textile automation by 2025 fuels orders for digitally compatible liquid dyes that shorten batch cycles and cut water usage. Regional pigment supply investments, such as VOXCO Pigments’ USD 60 million expansion in chrome yellow and molybdate orange, target export markets and reduce lead times for global customers.

Europe retains strategic significance despite stringent regulation. Anti-dumping duties on Chinese titanium dioxide recalibrate sourcing, offering openings for domestic producers in France, Germany, and the Netherlands. Germany remains a critical source of iron oxides, while Tronox’s idling of a Dutch plant reflects cost pressures in energy-intensive processes.

North America is mature yet dynamic, with EPA VOC standards catalyzing waterborne formulation upgrades. LANXESS markets iron-phosphate intermediates for lithium iron phosphate cathodes, expanding pigment reach into battery applications.

South America leans on Brazil’s iron oxide output, supporting domestic construction. The Middle East and Africa observe pigment demand growth from megaprojects such as Saudi Arabia’s NEOM, combined with coatings demand for climate-resilient facades.

Value Chain Analysis

The dyes and pigments value chain starts with upstream feedstocks such as petrochemical aromatics (notably benzene and naphthalene) for synthetic dyes and organic pigments, alongside mineral and metal-oxide precursors for inorganic pigments (for example, titanium dioxide and iron oxides). Producers convert these inputs through multi-step synthesis, finishing (filtration, drying), and application-specific conditioning (surface treatment and dispersion into powders, granules, or liquid dispersions). Manufacturing remains concentrated in Asia, especially China and India, where scale and cost advantages support high-volume output, while North America and Europe tend to be more focused on high-purity, specialty grades and R&D-intensive formulations that meet tight end-use specifications in coatings, plastics, and regulated applications.

Downstream, colorants move through direct sales to large paint, coatings, plastics, ink, and textile customers, and through distributors and formulators that tailor shades, rheology, and compliance documentation for local markets. Key bottlenecks include volatility in petrochemical-derived intermediates, wastewater and emissions compliance requirements in dye and pigment plants, and documentation burdens tied to substance restrictions, including EU REACH Annex XVII limitations affecting heavy-metal pigments and related compounds. Supplier qualification is also shifting toward auditable sustainability criteria, including Sudarshan Chemical Industries reporting ISO 20400:2017 certification for sustainable procurement and an ESG evaluation tool for critical suppliers (ESG Report 2024-25, published December 2025), alongside Solvay highlighting efforts to shorten and regionalize supply chains and explore recycled feedstocks in its 2025 integrated reporting (published June 2026).

Competitive Landscape

Market structure remains moderately fragmented. Advanced synthesis, including continuous hydrothermal processing, supports nanoparticle uniformity essential for effect pigments. Backward integration into intermediates and energy management remains a hedge against route-to-market disruptions. Intellectual property portfolios covering dispersion aids and polymer-compatible surface treatments reinforce barriers to entry, especially in aerospace, electronics, and medical device coatings that require strict qualification.

Dyes And Pigments Industry Leaders

BASF

Archroma

DIC Corporation

Sudarshan Chemical Industries Limited

Tronox Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory tightening and customer procurement requirements are opening opportunities for compliant, lower-footprint colorants and higher-performance dispersions. In the United States, the EPA finalized national pollution limits for industrial dye and pigment manufacturing in July 2026, targeting a 65% reduction in hazardous air emissions, which in turn increases the value of process upgrades, closed-loop wastewater treatment, and higher-efficiency chemistries that reduce residuals. In the European Union, nano-form documentation requirements under REACH (ECHA updates referenced in 2026) also elevate the importance of dossier-ready products, validated toxicology packages, and traceable supply chains, benefiting suppliers that can pair technical service with compliance data for coatings, plastics, inks, and specialty applications.

Investment activity points to opportunities in bio-based alternatives as well as regional capacity additions for strategic intermediates and white pigments. Sensient Technologies commenced expansion of its St. Louis natural color manufacturing plant (Project Prism) in March 2026, which supports scaling of natural and bio-based colorant supply beyond pilot volumes. Ultramarine & Pigments approved a USD 30 million greenfield inorganic pigments plant in Tamil Nadu, India (May 2026), while Lubei Chemical commissioned a 60,000 tpa chloride-process titanium dioxide expansion in Xianghai, China (June 2026), supporting import substitution and shorter lead times in high-consumption regions. Product innovation is also widening addressable niches, including ACTEGA and Living Ink Technologies launching ACTExact UV Black Algae Ink (March 2026), which aligns with converter qualification needs around sustainability claims and traceability in packaging and printing inks.

Recent Industry Developments

- June 2026: BASF completed the divestiture of its Coatings division to Carlyle, with the transaction closing on June 30, 2026, at an enterprise value of EUR 7.7 billion. The shift changes BASF's portfolio exposure to downstream coatings markets, while the broader pigments, dispersions, and color-matching solutions landscape continues to be shaped by how the separated coatings business sources and qualifies colorant technologies.

- March 2025: Sudarshan Chemical Industries Limited, through its wholly owned subsidiary Sudarshan Europe B.V., completed the acquisition of Germany-based Heubach Group. The combination broadened Sudarshan's inorganic pigment portfolio and expanded its customer access in regulated markets where product breadth and compliance documentation support supplier consolidation.

- February 2024: The European Union implemented tattoo-ink restrictions that widened the scope of regulated substances, extending to thousands of chemicals including certain pigment identifiers referenced by industry. This broadened compliance requirements for specialty pigment suppliers serving personal care and adjacent applications, reinforcing demand for reformulation support and traceable, restriction-ready product lines.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the dyes and pigments market covers colorants sold for industrial coloring and coating needs, counted at the point of sale in value terms, across major end-use industries and regions.

Scope exclusions: We do not count downstream finished goods value (such as textiles, paints, plastics, or printed packaging) and we exclude internal transfers that do not reflect an external sale price.

Segmentation Overview

- By Product Type

- Dyes

- Reactive

- Disperse

- Vat

- Sulfur

- Acid

- Azo

- Pigments

- Organic Pigments

- Inorganic Pigments

- Dyes

- By Source

- Synthetic

- Natural / Bio-based

- By Formulation

- Powder

- Granular

- Liquid Dispersion

- By End-user Industry

- Paints and Coatings

- Textiles

- Printing Inks

- Plastics

- Other End-user Industries (Construction Materials, Paper and Pulp, Cosmetics and Personal Care)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base and to avoid building the model on assumptions alone. We reviewed public sources such as USGS and other government mineral and chemical statistics, UN Comtrade trade flows for relevant HS codes, EPA and ECHA regulatory updates affecting colorant use, and technical literature in peer-reviewed journals on pigment and dye chemistry and performance.

Along with those, we also used company annual reports, investor presentations, press releases, and trade association publications to map capacity additions, plant shutdowns, and major application shifts by geography. For hard-to-track company financial splits and patent activity signals, a paid subscription database was used in a limited way to support cross-checks on revenue exposure and innovation direction. The desk sources listed here are illustrative only, and we relied on other public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what desk research cannot fully show, mainly the application demand mix, pricing movement, and how compliance costs are being passed through. We spoke with a balanced mix of manufacturers, distributors, formulators, and large end users across APAC, EMEA, and the Americas, so assumptions could be corrected when buying patterns differed by region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 43% |

| Mid tier: 49% | Functional/Unit leaders: 41% | EMEA: 30% |

| Smaller Players: 22% | Managers: 47% | Americas: 27% |

Market-Sizing & Forecasting

Market sizing was built using a top-down and bottom-up approach, where we first reconstructed the demand pool by linking colorant consumption to end-use production signals, then stress-tested the totals with selective supplier and channel roll-ups. In practice, the top-down side leaned on indicators such as textile output and fiber mix trends, paints and coatings demand linked to construction and industrial activity, plastics conversion volumes, and printing ink demand tied to packaging growth.

Once demand was framed, pricing and mix were applied carefully because dyes and pigments do not move at one uniform price. Inputs included average selling price direction by product type, the share shift between synthetic and natural or bio-based sources, the adoption of liquid dispersions versus powder or granular formats, and major regulatory constraints that influence reformulation and cost. Where a bottom-up check was possible, sampled company revenues, capacity utilization signals, and distributor feedback were used to adjust gaps, especially in smaller country blocks where public data is thinner.

For forecasting, scenario analysis was used around a base case, with near-term assumptions anchored to industry expectations shared by interviewees and supported by macro indicators. The scenarios mainly flexed end-use growth, raw material cost pass-through into pricing, and the speed of substitution between dye classes and pigment families as compliance requirements evolve.

Data Validation & Update Cycle

Outputs were validated through several checks so we did not rely on one line of evidence. We compared the modeled totals against independent signals such as trade movement, capacity announcements, and visible shifts in key end-use production, and then investigated variances that fell outside expected ranges.

Before sign-off, the model and assumptions go through step-by-step analyst reviews, and respondents are re-contacted when pricing, mix, or regional demand patterns look inconsistent with the rest of the evidence. Reports are refreshed annually, and interim updates are triggered when material events occur, such as regulation changes, major outages, or sharp feedstock swings. Right before delivery, a final pass is done so the most recent public releases and market events are reflected.

Mordor Intelligence's Dyes and Pigments Market Estimate Compared With Other Published Estimates

Published market sizes for dyes and pigments can vary even when the topic sounds identical, because the scope boundary and the pricing logic are not always handled the same way. Differences usually show up in whether adjacent colorant uses are included, how regions are treated, and whether the number is built from real end-use demand signals or from broad industry totals.

By tracking end-use demand drivers and refreshing price and mix assumptions with interview checks, Mordor Intelligence keeps the 2025 value tied to measured consumption signals across textiles, paints and coatings, plastics, and printing inks, rather than expanding scope into downstream finished product value. Some estimates appear to apply a wider inclusion set or a faster price ramp, which can lift the starting year even if the growth rate looks similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 41.46 B (2025) | |

| Global Consultancy A | USD 44.29 B (2025) | This estimate appears to apply a broader application roll-up and higher implied starting ASPs in large-volume uses, which can increase the 2025 total even if category boundaries are described similarly. |

| Industry Publisher B | USD 46.84 B (2025) | The higher value is consistent with counting additional adjacent uses and a more aggressive pricing progression into 2025 to 2026, which can inflate the base year when cross-checks are not tightly linked to end-use output. |

The comparison shows that most of the spread comes from scope edges and how price and mix are carried into the base year. Our approach stays traceable to a defined demand pool and a repeatable set of checks, which helps buyers understand what is included and why the number moves over time.

Key Questions Answered in the Report

What is the current size of the Dyes and Pigments Market?

The Dyes and Pigments Market size stand at USD 43.74 billion in 2026 and is projected to reach USD 57.23 billion by 2031.

Which region leads global consumption?

Asia-Pacific holds 46.88% of global volume and is also the fastest growing region at 6.05% CAGR through 2031.

Why are liquid dispersion formulations gaining traction?

Liquid dispersions deliver superior stability in water-borne systems and enable precise color control for 3D printing, supporting a 6.32% CAGR growth in this formulation segment.

How will regulations affect heavy-metal pigments?

Stricter REACH and EPA limits are phasing out cadmium-, chromium-, and lead-based pigments, prompting manufacturers to invest in safer organic and inorganic substitutes.

Which end-use sector commands the largest demand?

Paints and coatings account for 52.34% of total demand owing to robust construction and automotive refinishing activity.

Page last updated on: