Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 34.73 Billion |

| Market Size (2031) | USD 42.70 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

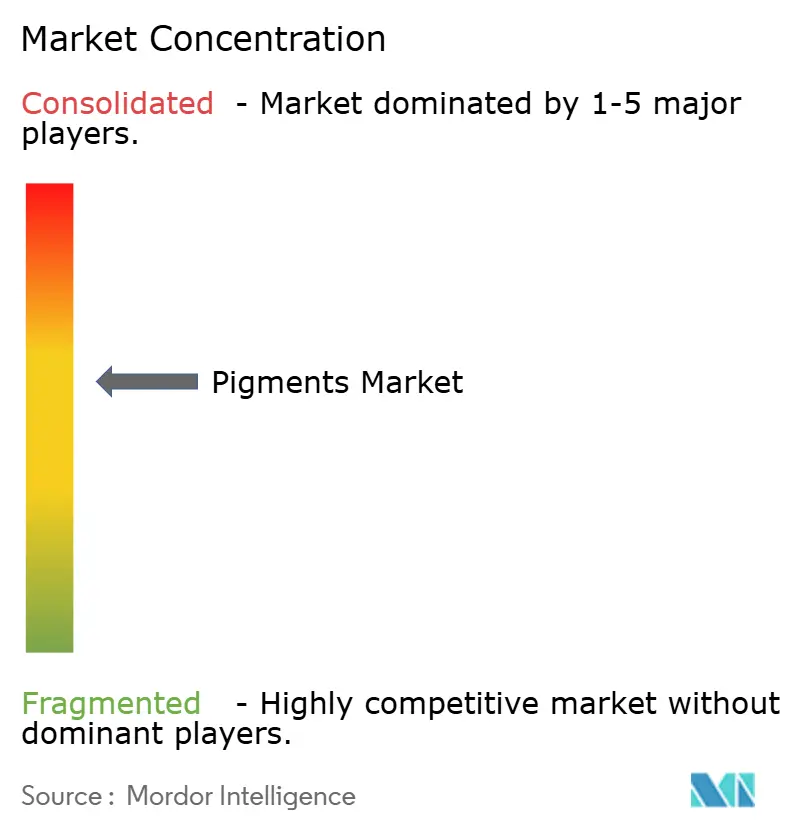

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pigments Market Analysis by Mordor Intelligence

The Pigments Market size is projected to be USD 33.32 billion in 2025, USD 34.73 billion in 2026, and reach USD 42.70 billion by 2031, growing at a CAGR of 4.22% from 2026 to 2031. Expansion stems from a simultaneous rationalization of high-cost titanium dioxide (TiO₂) lines and a clear shift toward organic colorants across plastics and packaging. Anti-dumping duties in the European Union, raw-material price volatility, and tightening nanomaterial rules are reshaping procurement models, prompting vertical integration among commodity producers and targeted acquisitions among specialty suppliers. Demand tailwinds remain strongest in Asia-Pacific, where domestic consumption upgrades are eclipsing export-led volumes. In parallel, brand owners are prioritizing lightfast, low-VOC formulations to comply with eco-labeling regimes, pushing organic and effect pigments into double-digit value share gains.

Key Report Takeaways

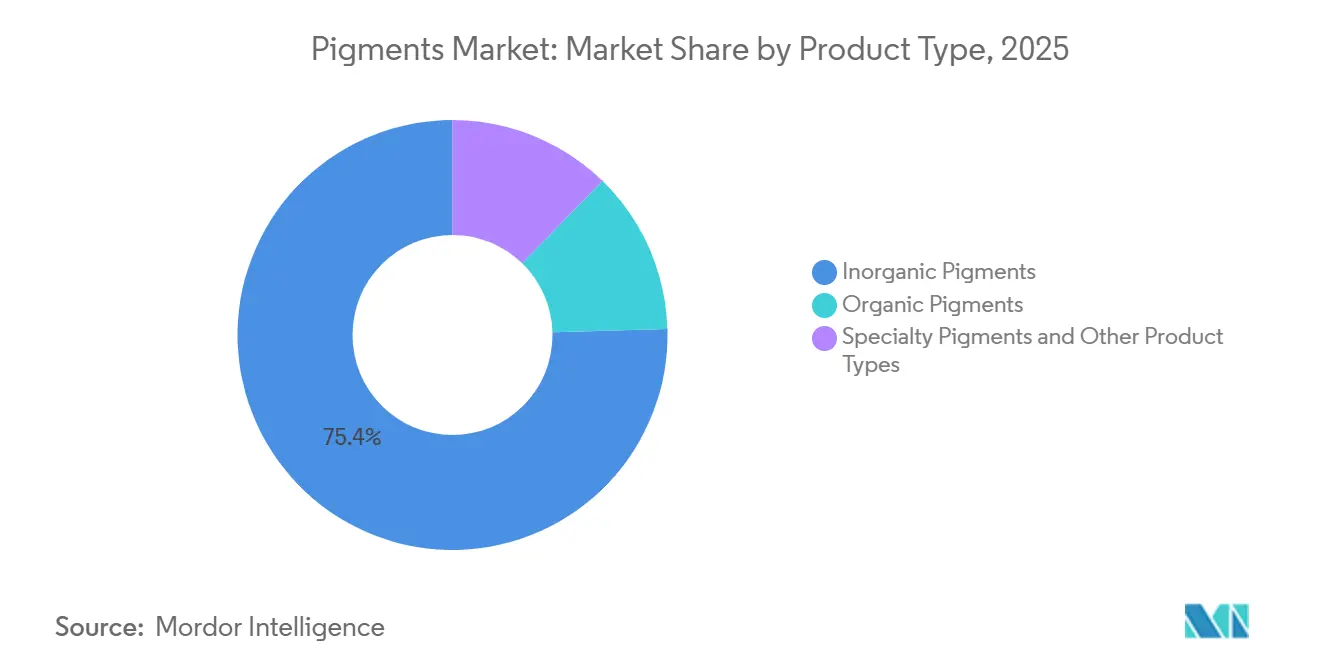

- By product type, inorganic pigments led with 75.45% of the pigments market share in 2025, while organic pigments are projected to post a 5.21% CAGR through 2031.

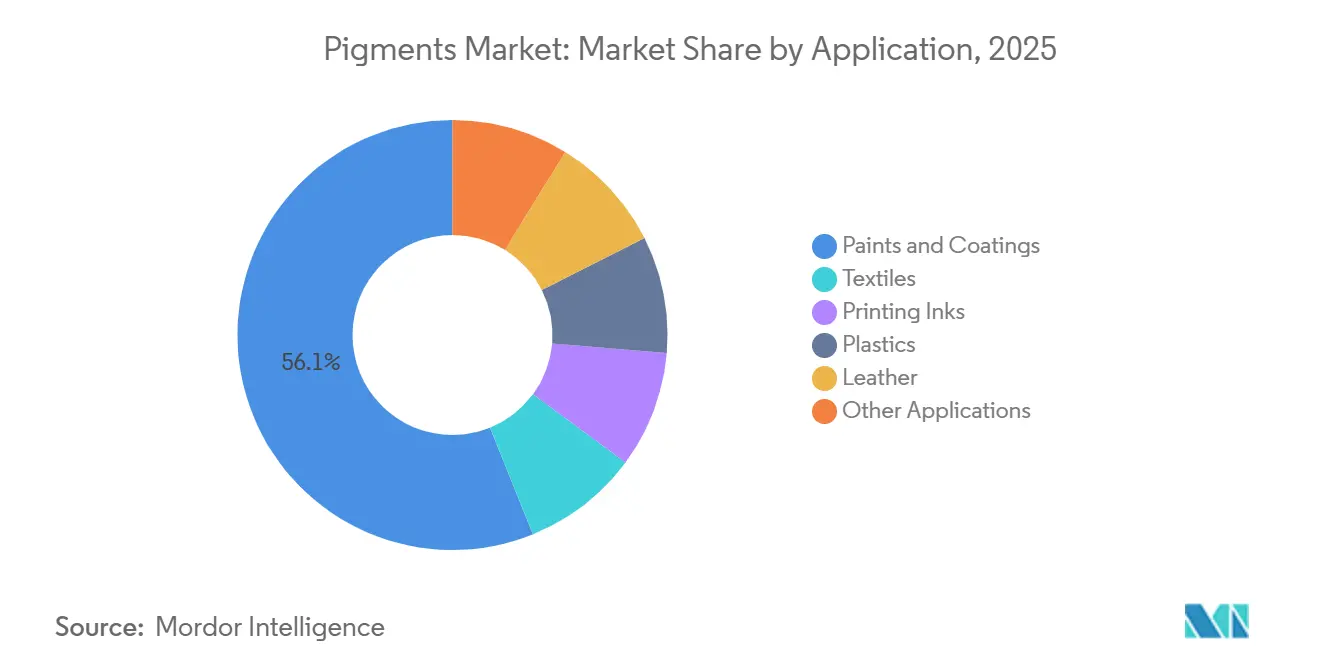

- By application, paints and coatings absorbed 56.12% of global volume in 2025; plastics applications are advancing at a 5.13% CAGR to 2031.

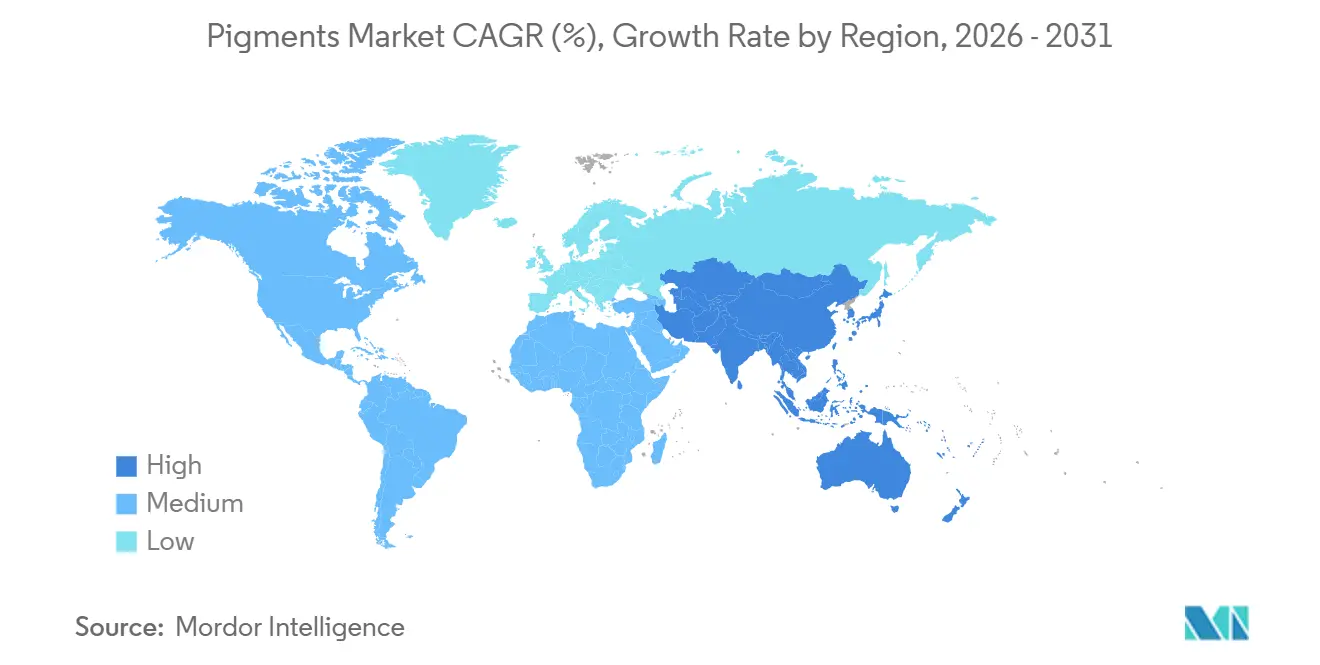

- By geography, Asia-Pacific accounted for 45.68% of revenue in 2025 and is set to expand at a 5.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pigments Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging paints and coatings demand in emerging economies | +1.2% | APAC core (China, India, ASEAN), spill-over to South America | Medium term (2-4 years) |

| Regulatory push toward eco-friendly/bio-based pigments | +0.8% | EU and North America, expanding to APAC cosmetics | Long term (≥ 4 years) |

| Rising adoption of high-performance and effect pigments | +0.7% | Global, concentrated in automotive and electronics hubs | Medium term (2-4 years) |

| Nano-enabled digital and 3D printing applications | +0.5% | North America, Western Europe, Japan | Long term (≥ 4 years) |

| Supply-chain localization incentives in US-EU | +0.6% | United States, EU-27 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Paints and Coatings Demand in Emerging Economies

Strong infrastructure outlays in India and Southeast Asia are scaling architectural-coating volumes that require high-hiding rutile TiO₂ and iron-oxide tints. India’s public capital expenditure pipeline continues to run ahead of GDP, and government stimulus in Chinese urban-renewal programs is cushioning the residential slowdown[1]Ministry of Statistics and Programme Implementation, “GDP Growth Forecast 2024-25,” mospi.gov.in. Tier-2 and tier-3 Chinese cities are additionally shifting toward low-VOC emulsions, elevating organic pigment loading in tinting systems. Vietnam’s construction-sector momentum feeds similar demand for water-based latex paints that observe volatile-organic-compound ceilings[2]World Bank, “Vietnam Economic Update 2024,” worldbank.org. Collectively, these developments reinforce a sturdy consumption base for both commodity and specialty grades, bolstering the pigments market across Asia-Pacific.

Regulatory Push Toward Eco-Friendly/Bio-Based Pigments

The European Food Safety Authority’s 2022 enforcement of the TiO₂ (E171) food ban is cascading into cosmetics and personal-care reformulations. Brands are piloting microalgal and fungal colorants despite unresolved scaling hurdles. In the United States, nanomaterial-specific reporting under TSCA intensifies compliance costs. The dual pressure is bifurcating strategies: commodity producers double down on rutile TiO₂ for construction paints, while specialty houses channel research and development toward bio-fermentation routes that can command premium pricing once commercialized.

Rising Adoption of High-Performance and Effect Pigments

Electric-vehicle OEMs specify infrared-reflective pigments that lower battery-pack and cabin temperatures, aligning with aggressive thermal-management targets. Complex inorganic color pigments containing chromium, cobalt, and titanium deliver the necessary durability but face cobalt-content scrutiny under REACH, catalyzing manganese- or iron-substituted variants. Consumer-electronics brands, meanwhile, deploy pearlescent and metallic finishes to refresh mature product lines, reinforcing volume gains for effect pigments even as price premiums persist.

Nano-Enabled Digital and 3D Printing Applications

Sub-200 nm dispersions are essential in digital textile printing and additive manufacturing, preventing nozzle clogging and ensuring vivid coloration at microscale layers. Quinacridone and DPP organic chemistries, known for their thermal stability, can endure processing temperatures exceeding 200 °C, a common benchmark in fused-deposition modeling, giving them an edge over azo derivatives. While this application accounts for a small percentage of the pigment volume, its projected growth positions it as a significant driver of innovation spending in the pigments industry.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental and toxicology regulations | -0.9% | EU, North America, extending to APAC cosmetics | Medium term (2-4 years) |

| Raw-material price volatility (TiO₂, iron-oxide feedstocks) | -1.1% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Nano-particle food-grade bans (E171, cosmetics limits) | -0.4% | EU, UK, potential adoption in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental and Toxicology Regulations

Mid-tier producers, lacking dedicated regulatory teams, find their margins pinched as compliance with REACH and TSCA can push dossier costs to significant levels per pigment. In the U.S., PMN reviews for nanomaterials have extended to 12 months, causing delays in new-product launches and shifting procurement focus to pre-approved pigments. Meanwhile, larger suppliers, with their diversified portfolios, seamlessly absorb these costs, further fueling consolidation trends in the pigments market.

Raw-Material Price Volatility (TiO₂, Iron-Oxide Feedstocks)

In 2024, disruptions in Mozambique and South Africa led to a spike in ilmenite and rutile ore prices. However, due to an oversupply, TiO₂ producers couldn't fully capitalize on this price surge. Buyers in Western Europe are paying a premium on Chinese TiO₂, a consequence of anti-dumping duties. Furthermore, European specialty grades, primarily sourcing iron-oxide feedstock from China, are vulnerable to fluctuations between the yuan and dollar. While coatings formulators are reducing TiO₂ content and turning to substitutes like calcium carbonate, they still face technical challenges due to opacity penalties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Inorganic Dominance Faces Organic Encroachment

Inorganic pigments held 75.45% of 2025 revenue, illustrating the entrenched role of TiO₂ in architectural and industrial coatings, the largest sub-segment within the pigments market share. Organic pigments, however, are advancing 5.21% annually, driven by plastics and packaging applications that demand lightfastness and regulatory compliance. Electric vehicles and consumer electronics are driving a premium for specialty sub-categories like infrared-reflective complex inorganic color pigments over commodity TiO₂. While the market size for these specialty-grade pigments is relatively modest, their significant value contribution fuels robust research and development efforts across the industry.

Regulatory fragmentation is spurring rapid substitution trends. Cosmetics brands are now experimenting with iron-oxide blends and bio-derived colorants. Meanwhile, while carbon black has long dominated printing inks and automotive underbodies, it is now facing competition from graphene dispersions and recycled alternatives, which aim to reduce furnace-black particulate emissions. Earth-based siennas and ultramarine blues, though still cherished in artistic circles, make up a small portion of the overall pigments market.

By Application: Paints Anchor Volume, Plastics Drive Growth

Paints and coatings consumed 56.12% of global volume in 2025, a testament to TiO₂’s opacity and weathering performance. Growth, however, is shifting toward plastics, which are advancing at a 5.13% CAGR on the back of legislation mandating recyclable masterbatches. Printing-ink demand remains steady as flexible-packaging and digital-inkjet formats offset declines in publication gravure, pushing the pigments market size for nano-dispersions in inks into mid-single-digit growth territory. Textiles and leather yet deliver incremental opportunities in digital textile printing and automotive interior color consistency.

Regional construction booms in India and Vietnam continue to buttress architectural coatings, while EU and California plastic regulations underpin the plastics-application surge. Ink formulators strive to meet food-contact compliance and high-speed press compatibility, reinforcing demand for stabilized organic pigments. Leather remains tethered to automotive and luxury-goods segments that prioritize durability and resistance to cracking under thermal cycling.

Geography Analysis

Asia-Pacific accounted for 45.68% of revenue in 2025 and will outpace all other regions at a 5.36% CAGR through 2031. China’s stimulus programs in urban-renewal projects offset softness in new-build construction, sustaining mid-single-digit gains in interior emulsions. India’s infrastructure agenda spurs demand for high-performance epoxy and polyurethane coatings requiring specialty iron-oxide and organic pigments. Japan’s incremental innovations in thermochromic and photochromic chemistries and South Korea’s automotive and shipbuilding specifications for infrared-reflective and anti-corrosive grades enhance specialty-pigment penetration. ASEAN manufacturing expansions further pull volume through maintenance coatings and plastics.

North America and Europe are mature yet premiumizing markets. The Inflation Reduction Act’s production credits entice U.S. TiO₂ capacity restarts, while Europe’s CBAM and anti-dumping levies on Chinese inputs drive localized sourcing, albeit at higher costs. Germany, the United Kingdom, Italy, France, and Spain anchor European demand across automotive refinish, architectural renovation, and industrial maintenance. Russia, isolated by sanctions, remains reliant on local iron-oxide and carbon-black supply.

South America’s pigments demand centers on Brazil’s construction and automotive production, with infrastructure concessions sustaining protective-coating needs. Argentina and Chile add smaller yet rising contributions. The Middle-East and Africa hold the smallest share but see episodic spikes tied to mega-projects such as NEOM in Saudi Arabia and mining ventures in South Africa. Regulatory regimes in these regions remain less stringent, allowing continued use of lead chromate and cadmium pigments in select industrial niches, although multinational brands are voluntarily phasing them out.

Competitive Landscape

The pigments market is moderately consolidated in nature. Technology adoption is increasingly a differentiator. ALTANA’s machine-learning-enabled milling lines reduce color variance and facilitate just-in-time batches for automotive OEMs. DIC Corporation’s investment in nano-pigment dispersions positions the company to exploit digital textile and 3D-printing growth, leveraging sub-200 nm stabilization know-how. Regulatory cost burdens catalyze supplier consolidation, as dossier expenses under REACH skew in favor of multinationals able to amortize compliance across high volumes.

Pigments Industry Leaders

LB Group

Tronox Holdings Plc

Kronos Worldwide, Inc.

Venator Materials PLC

DIC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Sudarshan Chemical Industries Limited, via its subsidiary Sudarshan Europe B.V., completed the acquisition of Germany-based Heubach Group.

- January 2024: ALTANA finalized the acquisition of Silberline, broadening its aluminum pigment manufacturing and distribution capabilities across North America and Asia.

Global Pigments Market Report Scope

Pigments are molecules or substances that absorb specific wavelengths of visible light to produce a particular hue. Pigments can be found in paintings, inks, cosmetics, and other items. Pigments are found in various products and services associated with coloring materials and related technology. Pigments are used in various sectors, including coatings, plastics, printing inks, building, paper, leather, and cosmetics.

The pigments market is segmented by product type, application, and geography. The market is segmented by product type into inorganic, organic, and specialty pigments, and other product types. By application, the market is segmented into paints and coatings, textiles, printing inks, plastics, leather, and other applications. The report also covers the market size and forecasts for the pigments market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD).

By Product Type

| Inorganic Pigments | Titanium Dioxide |

| Zinc Oxide | |

| Other Product Types (Carbon Pigments, Dry Earth, Ultramarine Pigments, Cadmium, Lead Chromate, and Others) | |

| Organic Pigments | |

| Specialty Pigments and Other Product Types (Functional Pigments, Magnetic Pigments, and Others) |

By Application

| Paints and Coatings |

| Textiles |

| Printing Inks |

| Plastics |

| Leather |

| Other Applications |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Inorganic Pigments | Titanium Dioxide |

| Zinc Oxide | ||

| Other Product Types (Carbon Pigments, Dry Earth, Ultramarine Pigments, Cadmium, Lead Chromate, and Others) | ||

| Organic Pigments | ||

| Specialty Pigments and Other Product Types (Functional Pigments, Magnetic Pigments, and Others) | ||

| By Application | Paints and Coatings | |

| Textiles | ||

| Printing Inks | ||

| Plastics | ||

| Leather | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is global demand for pigments projected to grow from 2026 to 2031?

The pigments market is forecast to expand at a 4.22% CAGR, reaching USD 42.70 billion by 2031 from USD 34.73 billion in 2026, as new specialty applications offset rationalization in commodity TiO₂.

Which region is expected to deliver the highest incremental pigment consumption by 2031?

Asia-Pacific leads with a 5.36% CAGR, driven by infrastructure expansion and rising demand for premium coatings in China, India, and ASEAN.

What drives the shift from inorganic to organic colorants in plastics?

Single-use packaging bans require recyclable masterbatches that keep brand colors intact over multiple melt cycles, favoring organic pigments with superior heat stability.

How are environmental regulations influencing pigment formulation strategies?

REACH, TSCA, and E171 bans are pushing formulators toward bio-based, low-nanoparticle alternatives and raising compliance costs that encourage supplier consolidation.

Which end-use segment currently anchors pigment volume, and which is growing fastest?

Paints and coatings remain the largest consumer, while plastics exhibit the fastest growth, expanding at a 5.13% CAGR through 2031.

Page last updated on: